Credit Score Basics: What Impacts Your Score and Why It Matters

Quick Answer

A credit score is a three-digit numerical representation of your creditworthiness. Scores typically range from 300 to 850 and provide lenders with a snapshot of your history of borrowing and repaying debts. Understanding your FICO Score® and VantageScore® credit scores and how they’re calculated can help you improve your credit and qualify for more offers.

Your credit scores can affect many aspects of your life, and learning more about how credit scores actually work can take some of the mystery and confusion out of managing your credit. In this guide, we'll cover all the basics you need to know: what a credit score is, why there are multiple credit scores, what affects your credit scores and how to improve your credit.

What Is a Credit Score?

A credit score is a simple-to-read number that can help creditors understand credit risk—the risk that they won't get repaid in full. It also helps consumers get a better understanding of their overall credit health.

Credit scores are calculated by credit scoring models. These scoring models are trained to analyze a consumer's credit report from one of the three consumer credit bureaus: Experian, TransUnion or Equifax. Specifically, many models are designed to predict the likelihood that someone will miss a payment by at least 90 days during the next 24 months.

Learn more: Understanding Your Experian Credit Report

Credit Score Ranges

Many credit scores range from 300 to 850, and a higher score is better because it indicates a person is less likely to fall behind on bill payments. However, a score doesn't consistently correlate with a specific likelihood of missing a payment. Instead, credit scores are a ranking system that tries to list consumers from most to least risky.

Example: Consider someone with a FICO® ScoreΘ 8 of 700. The score doesn't necessarily mean the person is a specific percentage less likely to miss a payment than someone else. However, in aggregate, people with a 700 FICO® Score 8 are less likely to miss a payment than those with a score of 600 and more likely to miss a payment than those with a score of 800.

Why Lenders Check Your Credit Scores

Lenders use credit scores to help assess risk and automate credit decisions.

For example, credit card companies may use your credit scores for:

- Preapproved credit offers: A credit card issuer that's marketing a credit card might send preapproved credit offers to people who have at least a minimum credit score and meet other requirements.

- Credit application reviews: Card issuers will also often check credit scores when people apply for a new credit card. The issuer might use scores to approve or deny applications, set interest rates and determine the credit limit on approved accounts.

- Ongoing credit monitoring: Once you get a credit card, the issuer might monitor your credit reports and scores. Changes in your credit score could prompt the lender to offer you additional credit accounts, send you promotional offers or change your credit limit.

Auto lenders, mortgage lenders and other financial institutions use credit scores in similar ways.

FICO® Score vs. VantageScore®

Many creditors use one or more credit scores from credit scoring companies FICO and VantageScore. Although most of their credit scores rely on the same underlying data to make predictions, the two companies take a slightly different approach to credit scoring.

Here's an overview of some of the similarities and differences.

| FICO® Score | VantageScore | |

|---|---|---|

| Typical score range | Base scores: 300 to 850 Industry-specific scores: 250 to 900 | 300 to 850 |

| Recent scoring models | FICO® Score 8, 9, 10 and 10T | VantageScore 3, 4 and 4plus™ (the newly released 5.0 is not in use yet) |

| Minimum scoring requirements |

|

|

| Hard inquiry treatment |

|

|

Learn more: The Difference Between VantageScore Scores and FICO® Scores

Why Are There So Many Different Credit Scores?

There are several reasons that there are so many credit scores. One is that FICO and VantageScore regularly develop and release new credit scores—FICO alone has dozens of credit scoring models. Additionally, other companies develop and sell credit scores to creditors, and some creditors develop their own scores as well.

As a result, you might find that when you check your credit scores, you get different results. And now you know that's not necessarily a mistake or error. The score you receive can depend on the scoring model, which of your credit reports it analyzed and when the score was generated. Any changes in one of those factors could lead to a different score.

Learn more: Why Are My Credit Scores Different?

Types of Credit Scores

Here are examples of five common types of credit scores lenders might use:

- Base FICO® Scores: Base FICO credit scores include the FICO® Score 8, 9, 10 and 10T; FICO designs these scores for any type of lender to use. Unlike the others, FICO® Score 10T considers trends in your credit history, such as changes in your balances or credit utilization ratio over time.

- Industry-specific FICO® Scores: FICO also creates industry-specific scores for auto lenders and credit card issuers. These build a base score to better predict the likelihood of someone missing an auto loan or credit card payment.

- VantageScore credit scores: VantageScore currently offers five credit scores: VantageScore 1 through 4 and VantageScore 4plus. (VantageScore introduced its 5.0 version in April 2025, but the version is not "live" yet.) The VantageScore 4plus stands apart from the others because it gives consumers the option of connecting their bank or credit card accounts and using the data from these accounts to potentially adjust their score.

- Credit scores that use alternative data: Many credit scores only consider the information in one of your credit reports. But some scores can consider alternative credit data, such as your utility bill payment history, public records, banking history or history with payday loans. VantageScore 4plus and FICO XD scores are two examples.

- Proprietary credit risk scores: Some financial institutions create their own credit scores. These scores might consider internal data the company has about you alongside information from your credit report and one of your FICO or VantageScore credit scores. The additional insight could make the scores more predictive than using a generic credit score from FICO or VantageScore on its own.

Companies often use these types of credit scores to make lending decisions and manage accounts after someone receives a loan or credit card. Additionally, insurance companies in many states can use credit-based insurance scores to help determine who to offer insurance and how much to charge.

Learn more: Facts About Credit You May Not Know

How Are Credit Scores Calculated?

Credit scoring models generally calculate your score by reviewing the information in one of your credit reports from Experian, TransUnion or Equifax. Various models may consider slightly different information or use different weighting when scoring your credit report.

However, the factors that can affect your credit scores are generally grouped into several categories. Even if the precise details differ from one score to another, focusing on the big picture could help you improve all your credit scores.

Your Payment History

Your debt payment history is the most important factor in your credit scores, making up 35% of your FICO® Score. This category includes whether you've made payments on time, which can help your credit, or missed payments, which can hurt it. How far behind you've fallen on past-due accounts can also affect your scores.

Bankruptcy filings and collection accounts are additional negative items related to your payment history that could hurt your credit scores.

How Much You Owe

The amounts you owe on various credit accounts is also an important factor in your credit score calculation. This factor makes up 30% of your FICO® Score. Scoring models might consider how many accounts you have with balances, how much you owe overall and the current balance relative to the starting balance on a loan.

Your revolving credit utilization is also a major influence in this category. Your credit utilization rate is the percentage of available credit you're using on revolving accounts such as credit cards. A lower utilization rate—ideally under 10%—is best for your scores.

Learn more: How to Calculate Credit Card Utilization

Your History With Credit Accounts

Having a lengthy history with credit could help your credit scores. Scoring models consider the age of the oldest and newest accounts in your credit report, along with the average age of all your credit accounts. These age-related factors may consider the ages of opened and closed accounts, which can stay on your credit report for up to 10 years if they're in good standing when the account is closed or paid off. Length of credit history counts for 15% of your FICO® Score.

Your Experience With Different Types of Credit

Having open installment and revolving credit accounts, such as loans and credit cards, might help your credit scores because it shows you can manage different types of debt. Credit mix accounts for 10% of your FICO® Score. Your experience with particular types of accounts, such as an auto loan, could also be important for industry-specific FICO® Scores.

Recent Credit Activity

New credit applications can result in hard inquiries, a record of when a creditor checks your credit before making a lending decision. New hard inquiries could hurt your credit scores a little, typically just a few points. Having multiple new accounts and how long it's been since you opened different types of accounts could also affect your scores.

New credit makes up about 10% of your FICO® Score.

Reminder: Payment history makes up 35% of your FICO® Score, and credit utilization is responsible for 30%. Because they are the two most impactful factors in your score, be sure you're making on-time payments and keeping your credit card balances low for the most benefit.

Some Things Don't Affect Your Credit Scores

Most credit scores don't consider certain pieces of personal or financial information, including:

- Income, employer or employment status

- Age, gender, race, ethnicity or disabilities

- Nationality, citizenship status or marital status

- Religious or political affiliations

Some of this information doesn't affect your credit scores because it isn't in your credit report, such as your income. However, creditors might ask about your income on a credit application, and it could affect your eligibility and offers.

Learn more: What's Not Included in Your Credit Report?

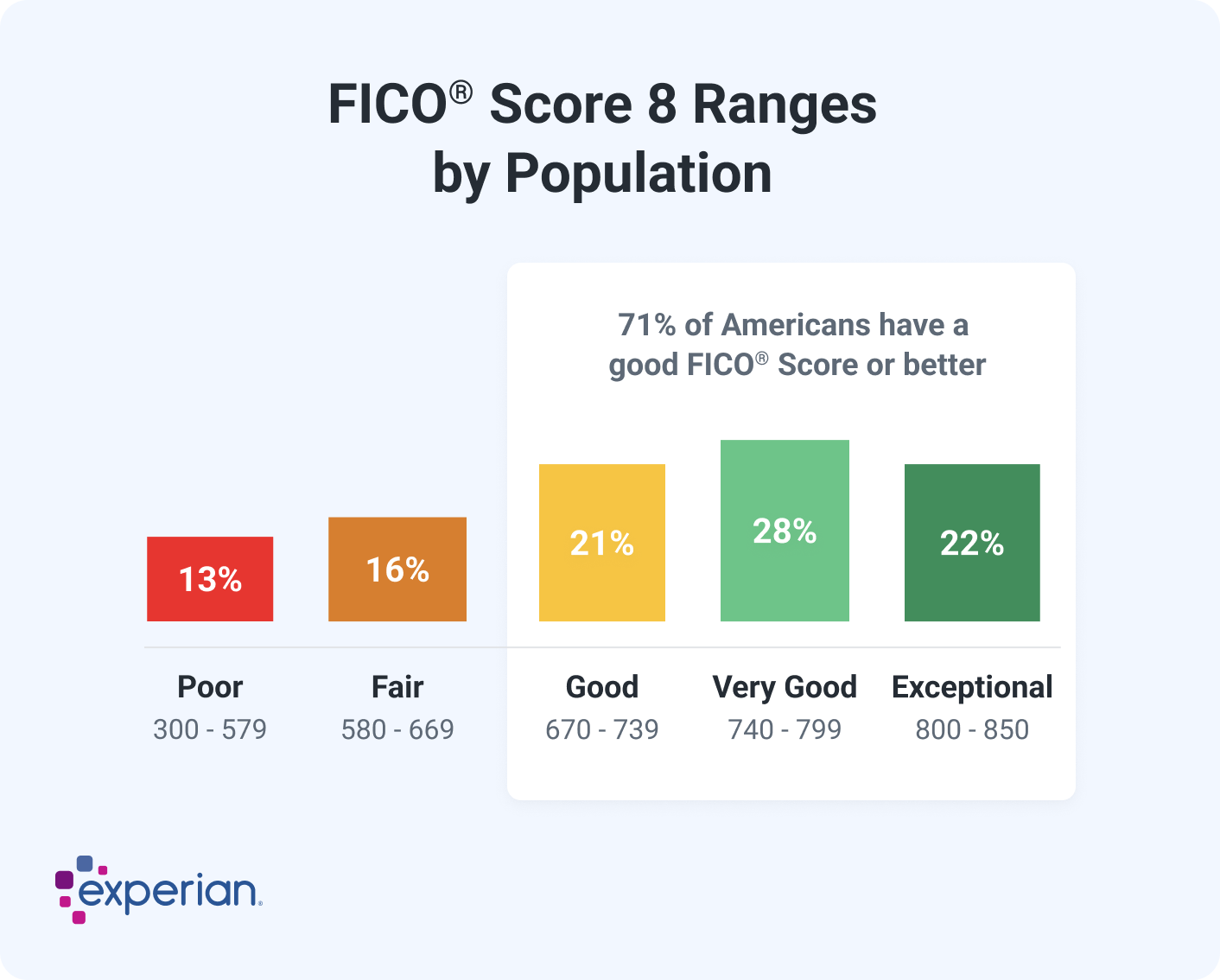

What Is a Good Credit Score?

FICO and VantageScore share general guidelines for what they consider to be a good score—670 and up for FICO, and 661 or higher for VantageScore. However, creditors can set their own standards for what they consider to be poor, good and excellent credit scores.

Here's how FICO and VantageScore ranges compare.

| FICO® Score | VantageScore |

|---|---|

| Exceptional 800-850 | Excellent 781-850 |

| Very good 740-799 | Good 661-780 |

| Good 670-739 | Fair 601-660 |

| Fair 580-669 | Poor 500-600 |

| Poor 300-579 | Very poor 300-499 |

Why Does Your Credit Score Matter?

Having a good credit score can be important because it can help you qualify for more financial products and receive better offers. A higher score can help you get:

- Higher loan and credit limits

- Lower interest rates

- Lower or fewer fees

But good credit can come into play even when you don't need to borrow. For example:

- Landlords may check and consider your credit when you apply for housing.

- Cellphone companies might consider your credit if you want to finance a phone or get a postpaid phone plan.

- Utility companies may even consider your credit when deciding if and how much to require for a security deposit when you want to open a new account.

Tip: Prospective employers may check your credit during the application process to verify your identity and gauge your reliability and financial management skills. However, employers cannot see your credit score.

Learn more: Reasons You Want a Good Credit Score

How to Improve Your Credit Score

The following actions can help improve your credit scores over time.

Pay Bills on Time

On-time loan and credit card payments are crucial to helping you build a long and positive credit history. Even one 30-day late payment can hurt your scores, so make at least the minimum payment by the due date every month if possible. Even other non-credit bills can hurt your scores if a company sends a past-due account to collections and the collection account gets reported to the credit bureaus.

Pay Down Credit Card Debt

If you're carrying credit card balances from month to month, try to pay off your balances and start paying your bills in full. Doing so can help you save money on interest and lower your credit utilization rate.

Make Credit Card Payments Early

You might have a high utilization rate even if you pay your credit card balance in full every month. Credit card issuers usually report your balance to the bureaus when your billing cycle ends, which could be several weeks before your bill's due date.

If you're using your credit cards to earn rewards and get purchase protections, you might want to pay down your balance early to lower your utilization rate. You could also request a credit line increase or apply for another credit card to increase your available credit and lower your utilization rate.

Learn more: Ways to Keep Your Credit Utilization Low

Bring Past-Due Accounts Current

Catching up on an account that's past due might help your credit scores even if it won't remove the late payments from your credit history. Late payments, along with most negative marks, can stay on your credit reports for seven years from when they first occur. If you have accounts in collections, settling or paying off the debt could also help your credit scores—though the negative marks for the overdue balances will remain for seven years.

Strategically Apply for Credit

New credit applications typically lead to hard inquiries that may hurt your credit scores slightly. Hard inquiries are often a minor scoring factor, and you don't necessarily need to hold off on applications when there's a great offer or you need a loan. But try to be strategic when you apply.

You could start by looking for card issuers and lenders that will prequalify or preapprove you with a soft credit check, which can tell you if you'll likely get approved without affecting your credit scores. If you're shopping for an auto loan or mortgage, you could also group your applications with different lenders to limit the impact of the hard inquiries.

Learn more: Do Multiple Loan Inquiries Affect Your Credit Score?

Add Eligible Bills to Your Credit Report

You could use the free Experian Boost®ø feature to add eligible rent, utility, phone, insurance and certain streaming services payments to your Experian credit report. The additional accounts and payments could improve credit scores calculated by many of the latest FICO and VantageScore scoring models.

Review Your Credit Reports for Errors

Regularly review your credit reports and look for errors that might be hurting your credit scores. For example, if you notice a late payment in an account's history when you made the payment on time, you may want to have it corrected. You have the right to file disputes with the creditors or credit bureaus, and they'll investigate the reported information and either verify that it's accurate, correct it or remove it from your credit reports.

Will Checking Your Credit Reports Affect Your Credit Scores?

No, checking your credit reports or scores won't affect your credit scores. A record of when you check your own credit report or score will be added to the report each time, but it will be a soft credit check. Unlike hard inquiries, soft inquiries never affect your credit scores.

Learn more: How Do You Check Your Credit Score?

Frequently Asked Questions

Keep an Eye on Your Credit for Free

The specifics of how credit scores work can quickly get complicated, but building good credit is often straightforward. You can monitor your credit as you take steps to improve your credit scores, such as paying down credit card balances and making on-time payments. A free Experian account can also give you insights into what factors are helping and hurting your FICO® Score the most based on your unique credit profile.

If you're brand new to credit and want to learn more about the basics of credit and why it's important, the Experian Credit Course: A Complete Guide to Credit can help you get up to speed.

What makes a good FICO® Score?

Learn what it takes to achieve a good credit score. Review your FICO® Score for free and see what’s helping and hurting your score.

Get your FICO® ScoreNo credit card required

About the author

Louis DeNicola

Louis DeNicola is freelance personal finance and credit writer who works with Fortune 500 financial services firms, FinTech startups, and non-profits to teach people about money and credit. His clients include BlueVine, Discover, LendingTree, Money Management International, U.S News and Wirecutter.

Read more from Louis