523 Credit Score: Is it Good or Bad?

Your score falls within the range of scores, from 300 to 579, considered Very Poor. A 523 FICO® ScoreΘ is significantly below the average credit score.

Many lenders choose not to do business with borrowers whose scores fall in the Very Poor range, on grounds they have unfavorable credit. Credit card applicants with scores in this range may be required to pay extra fees or to put down deposits on their cards. Utility companies may also require them to place security deposits on equipment or service contracts.

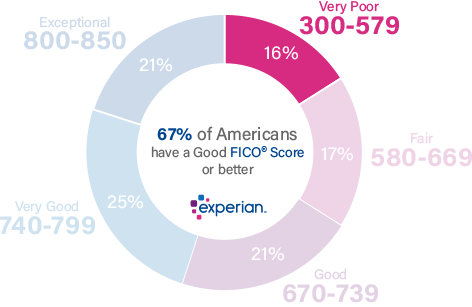

16% of all consumers have FICO® Scores in the Very Poor range (300-579).

Roughly 62% of consumers with credit scores under 579 are likely to become seriously delinquent (i.e., go more than 90 days past due on a debt payment) in the future.

How to improve your 523 Credit Score

The bad news about your FICO® Score of 523 is that it's well below the average credit score of 714. The good news is that there's plenty of opportunity to increase your score.

99% of consumers have FICO® Scores higher than 523.

A smart way to begin building up a credit score is to obtain your FICO® Score. Along with the score itself, you'll get a report that spells out the main events in your credit history that are lowering your score. Because that information is drawn directly from your credit history, it can pinpoint issues you can tackle to help raise your credit score.

How to get beyond a Very Poor credit score

FICO® Scores in the Very Poor range often reflect a history of credit missteps or errors, such as multiple missed or late payments, defaulted or foreclosed loans, and even bankruptcies.

Among consumers with FICO® Scores of 523, 19% have credit histories that reflect having gone 30 or more days past due on a payment within the last 10 years.

Once you're familiar with your credit report, its contents and their impact on your credit scores, you can begin taking steps to build up your credit. As your credit behaviors improve, your credit scores will tend to follow suit.

What affects your credit score

While it’s useful to know the specific behaviors in your own credit history, the types of behaviors that can lower your credit score are well-known in general terms. Understanding them can help you focus your credit score-building tactics:

Public Information: If bankruptcies or other public records appear on your credit report, they typically hurt your credit score severely. Settling the liens or judgments at the first opportunity can reduce their impact, but in the case of bankruptcy, only time can lessen their harmful effects on your credit scores. A Chapter 7 bankruptcy will remain on your credit report for up to 10 years, and a Chapter 13 bankruptcy will stay there for 7 years. Even though your credit score may begin to recover years before a bankruptcy drops off your credit file, some lenders may refuse to work with you as long as there’s a bankruptcy on your record.

The average credit card debt for consumer with FICO® Scores of 523 is $2,734.

Credit utilization rate. To calculate the credit utilization rate on a credit card, divide the outstanding balance by the card's borrowing limit, and multiply by 100 to get a percentage. To calculate your overall utilization rate, add up the balances on all your credit cards and divide by the sum of their borrowing limits. Most experts recommend keeping utilization below 30%, on a card-by-card basis and overall, to avoid hurting your credit score. Utilization rate contributes as much as 30% of your FICO® Score.

Late or missed payments. Paying bills consistently and on time is the single best thing you can do to promote a good credit score. This can account for more than a third (35%) of your FICO® Score.

Length of credit history. All other things being equal, a longer credit history will tend to yield a higher credit score than a shorter history. The number of years you've been a credit user can influence up to 15% of your FICO® Score. Newcomers to the credit market cannot do much to about this factor. Patience and care to avoid bad credit behaviors will bring score improvements over time.

Total debt and credit mix. Credit scores reflect your total outstanding debt, and the types of credit you have. The FICO® credit scoring system tends to favor users with several credit accounts, and a mix of revolving credit (accounts such as credit cards, that borrowing within a specific credit limit) and installment credit (loans such as mortgages and car loans, with a set number of fixed monthly payments). If you have just one type of credit account, broadening your portfolio could help your credit score. Credit mix is responsible for up to 10% of your FICO® Score.

Recent credit activity. Continually applying for new loans or credit cards can hurt your credit score. Credit applications trigger events known as hard inquiries, which are recorded on your credit report and reflected in your credit score. In a hard inquiry, a lender obtains your credit score (and often a credit report) for purposes of deciding whether to lend to you. Hard inquiries can make credit scores drop a few points, but scores typically rebound within a few months if you keep up with your bills—and avoid making additional loan applications until then. (Checking your own credit is a soft inquiry and does not impact your credit score.) New credit activity can account for up to 10% of your FICO® Score.

Improving Your Credit Score

There are no quick fixes for a Very Poor credit score, and the negative effects of some issues that cause Very Poor scores, such as bankruptcy or foreclosure, diminish only with the passage of time. You can begin immediately to adopt habits that favor credit score improvements. Here are some good starting points:

Consider a debt-management plan. If you're overextended and have trouble paying your bills, a debt-management plan could bring some relief. You work with a non-profit credit counseling agency to negotiate a workable repayment schedule and effectively close your credit card accounts in the process. This can severely lower your credit scores, but it's less draconian than bankruptcy, and your scores can rebound from it more quickly. Even if you decide this is too extreme a step for you, consulting a credit counselor (as distinct from credit-repair company) may help you identify strategies for building stronger credit.

Think about a credit-builder loan. Credit unions offer several variations on these small loans, which are designed to help people establish or rebuild their credit histories. In one of the more popular options, the credit union deposits the amount you borrow into a savings account that bears interest (rather than giving you the cash outright). When you've paid off the loan, you get access to the money, plus the interest it has generated. It's a clever savings method, but the real benefit comes as the credit union reports your payments to the national credit bureaus. Make sure before you apply for a credit builder loan that the lender report payments to all three national credit bureaus. As long as they do, and as long as you make regular on-time payments, these loans can lead to credit-score improvements.

Look into obtaining a secured credit card. When you open a secured credit card account, you put down a deposit in the full amount of your spending limit—typically a few hundred dollars. As you use the card and make regular payments, the lender reports them to the national credit bureaus, where they are recorded in your credit files and reflected in your FICO® Score. Making timely payments and avoiding “maxing out” the card will promote improvements in your credit scores.

Pay your bills on time. There's no better way to improve your credit score.

Avoid high credit utilization rates. Try to keep your utilization across all your accounts below about 30% to avoid lowering your score.

Among consumers with FICO® credit scores of 523, the average utilization rate is 93.8%.

Try to establish a solid credit mix. The FICO® credit-scoring model tends to favor users with multiple loan accounts, and a blend of different types of loans, including installment loans like mortgages or auto loans and revolving credit such as credit cards and some home-equity loans.

Learn more about your credit score

Every growth process has to start somewhere, and a 523 FICO® Score is a good beginning point for improving your credit score. Boosting your score into the fair range (580-669) could help you gain access to more credit options, lower interest rates, and reduced fees and terms. You can get rolling by getting your free credit report from Experian and checking your credit score to find out specific issues that are keeping your score from increasing. Read more about score ranges and what a good credit score is.