What’s the Difference Between a Credit Report and Credit Score?

Quick Answer

Credit reports and credit scores are both important, but they’re not the same. Your credit report is the underlying personal and account information that a credit bureau organizes into a report. A credit score is a three-digit number credit scoring companies calculate based on an analysis of information in one of your credit reports.

Your credit reports and scores can both be important, but they're not the same thing. Your credit report contains information about your history repaying and managing debt. A credit score is a three-digit number based on the information in a credit report, and it gives organizations an easy way to assess risk associated with lending someone money.

What Is a Credit Report?

A credit report contains information about a person and their history of paying credit accounts, such as loans and credit cards. The major consumer credit bureaus—Experian, TransUnion and Equifax—collect and store data to create credit reports.

The information in your credit report is organized in different sections:

- Personal information: This includes your name, address, year of birth and possibly employer.

- Accounts: These could include loans and credit cards, and potentially other types of monthly bills. Your open, closed and collection accounts are generally separated.

- Public records: Bankruptcy filings from the last seven to 10 years are the only public records on your credit report.

- Recent inquiries: Records of when someone (including yourself) checks your credit report.

Your credit report will also have details about each account, such as the date you took out a loan, the loan amount, your monthly payment amount and your history of making late or on-time payments. The credit bureaus receive most of the information that appears on your credit reports from creditors.

For example, when you apply for a loan, the lender may report the personal information from your application, such as your name and address. Once you take out the loan, it reports the account information and regularly sends updates about your payments and your account's status (whether it's being paid on time or not). The credit bureaus can then include this information in your credit reports.

In addition to information from your creditors on your credit reports, you can use Experian Boost®ø to add certain phone, utility and popular streaming service payments to your Experian credit report. These accounts can add positive payment information, which can help your credit.

Your credit report is important because organizations can request a copy before making a decision on whether to approve your application for a loan, a credit card or even a rental home or job. Someone can only check your credit if they have a permissible purpose.

The information in your credit reports provides the basis for your credit scores.

See your latest credit information

Better understand your creditworthiness with an overview of your total debt.

Check for any changes with customized alerts and an updated report daily.

Reviewing your credit report can help you spot potential fraud or identity theft.

What Is a Credit Score?

A credit score is the numerical result of a mathematical formula that evaluates the information in one of your credit reports. Companies build these formulas, called scoring models, based on historical data from millions of anonymized credit reports. By analyzing the data, they can create complex models to help predict the likelihood that someone will miss a payment in the future.

FICO and VantageScore® are the two main companies that create consumer credit scoring models. Both companies maintain multiple versions of their credit scores, which is why you may have many different credit scores. Lenders may also create their own credit score models.

Creditors can request a credit score—they can choose one or request multiple scores—along with your credit report when deciding whether to lend you money. For example, if you apply for a loan, the lender might check your Experian credit report and a FICO® ScoreΘ 8 8 based on that specific report.

What Impacts Credit Scores?

Each credit scoring model uses slightly different criteria to determine a score. However, many scoring models use similar factors, and these are commonly grouped into several categories:

- Payment history: Your history of making debt payments on time or missing payments.

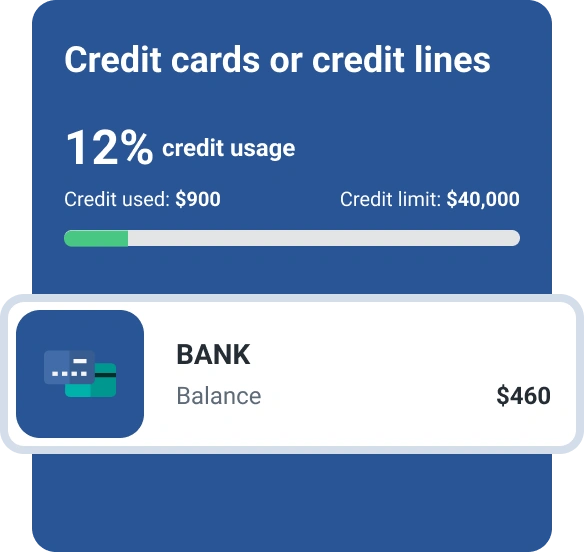

- Amounts owed: How much you owe on loans and how your credit cards' balances compare with their credit limits.

- Length of credit history: The age of your credit account history, which could include the age of your oldest and newest accounts and the average age of all your accounts.

- Recent activity: How many accounts you've applied for and opened recently.

- Types of credit accounts: Whether you have experience with different types of accounts, such as credit cards and loans.

Credit scoring models only look at the information in your credit report when calculating a score, and different types of information might help or hurt your credit scores. For example, paying down a credit card balance could help your scores, but missing a loan payment could hurt them.

Closing an account won't keep it from impacting your credit score. If you pay off a loan or close a credit card that doesn't have a balance, the account can remain on your report for 10 years. The federal Fair Credit Reporting Act allows most negative information to stay on your credit report for up to seven years, but the impact of negative items can decrease as time passes.

What's a Good Credit Score?

Many credit scores range from 300 to 850. A higher score is better because it indicates the person is less likely to fall 90 or more days late on one of their bills—in other words, that they manage debt responsibly. This is why having a good credit score, such as a score above 700, can help you get approved for new accounts with more favorable terms.

How Are Credit Scores and Credit Reports Different?

Here's a brief overview and recap of how consumer credit reports and credit scores differ:

| Credit Reports | Credit Scores | |

|---|---|---|

| Who creates them? | Experian, TransUnion and Equifax | FICO and VantageScore are the main credit scoring companies |

| What are they based on? | Information from a credit bureau's database, which primarily includes information reported by creditors | A credit report |

| When are they created? | When someone with a permissible purpose requests a credit report from a bureau | When someone with a permissible purpose requests a credit score |

| How are they used? | To understand a person's creditworthiness. Could impact your eligibility or payments for a loan, credit card, job, insurance and other types of accounts. | To quickly understand the likelihood that someone will miss a payment. May impact your eligibility and terms for a credit account or rental home. |

Why Are Your Credit Score and Credit Report Important?

Your credit reports and credit scores are both parts of your overall creditworthiness. Having good credit can be important because it helps you:

- Qualify for more accounts. Your credit can impact your eligibility for credit cards, loans, mobile phone accounts and rental homes.

- Save money on loans and insurance. Your credit report and score can impact how much you pay in fees and interest on credit accounts. Credit-based insurance scores may also impact how much you pay for insurance premiums.

- Save on security deposits. You may have to pay more fees or a larger security deposit for utility and telecom accounts if you don't have good credit.

- Get a job in some cases. Your credit report (but not a credit score) may impact your ability to get a job or a promotion.

Even if you don't plan on taking out a loan or opening a credit card, establishing and building good credit could give you more options and save you money.

How to Check Your Credit Report and Score

You can check your credit reports and scores from various sources, some of which may require you to pay for access. Experian offers you a free credit report, free FICO® Score and free credit monitoring. You'll also receive insight into how the information in your credit report is helping or hurting your credit score.

If you don't have a credit report yet, you can get started with Experian Go™. This new program helps you create a credit file and start building your credit with a personalized credit path. Once you have six months of credit history on your report, FICO can create a credit score for you.

What’s on your credit report?

Stay up to date with your latest credit information—and get your FICO® Score for free.

Get your free reportNo credit card required

About the author

Louis DeNicola

Louis DeNicola is freelance personal finance and credit writer who works with Fortune 500 financial services firms, FinTech startups, and non-profits to teach people about money and credit. His clients include BlueVine, Discover, LendingTree, Money Management International, U.S News and Wirecutter.

Read more from Louis