How to “Fix” a Bad Credit Score

Quick Answer

You can “fix” a bad credit score by paying bills on time, keeping credit card balances low and adding positive payment history to your credit report with a secured credit card or credit-builder loan.

Having a bad credit score can make it difficult to borrow money and cost you more in interest. However, you can fix a bad credit score by paying bills on time, keeping credit card balances low and using credit-strengthening products like secured credit cards.

Before you can work on improving your credit score, it's crucial to check your credit report and score to better understand the basic factors that go into calculating your credit score. You can then identify what is making the biggest negative impact and take a targeted approach to address it.

Here's how to improve a bad credit score so you can enjoy all the advantages good credit provides.

What Is a Bad Credit Score?

A bad credit score is a FICO® ScoreΘ below 580. A bad VantageScore® credit score is a score below 600. That said, lenders may have different ideas of what a bad credit score is when they're reviewing a loan application. The credit scoring models separate credit scores into ranges so you can gauge where you stand and take action to improve your credit.

Here are more specifics. The FICO® Score, the credit score used by 90% of top lenders, ranges from 300 to 850. A score from 300 to 579 is considered poor, while a score from 580 to 669 is fair credit. Here are the different credit score ranges:

| Credit Score | Rating |

|---|---|

| 300 - 579 | Poor |

| 580 - 669 | Fair |

| 670 - 739 | Good |

| 740 - 799 | Very good |

| 800 - 850 | Exceptional |

VantageScore, a credit scoring model developed by the three credit bureaus (Experian, TransUnion and Equifax), also uses a scale ranging from 300 to 850. But the score ranges vary slightly. A VantageScore credit score from 300 to 499 is considered very poor, from 500 to 600 is poor and 601 to 660 is fair. Here's a full breakdown:

| Credit Score | Rating |

|---|---|

| 300 - 499 | Very poor |

| 500 - 600 | Poor |

| 601 - 660 | Fair |

| 661 - 780 | Good |

| 781 - 850 | Excellent |

Consequences of a Bad Credit Score

A low credit score can make it more difficult to get approved for a loan or credit card. If you do get approved, you'll be less likely to qualify for the lowest rates and best terms. A bad credit score can lead to these roadblocks:

- Potential rejection when applying for credit: That includes credit cards, lines of credit, mortgages, car loans, personal loans, private student loans and some federal student loans for parents and graduate students.

- Difficulty getting a rental application approved: Many landlords conduct credit checks to evaluate your payment history and debt-to-income ratio (DTI), with an eye to whether you're likely to pay rent on time.

- Required security deposits: When moving into a new home, utility companies—like those that provide gas, electricity and water—may require you to make a security deposit. Another option is to supply a letter of guarantee from someone who will be responsible for your utility bills if you don't make payments.

- Trouble getting a new cellphone or phone contract: Many wireless providers check credit when you apply for a new cellphone plan or even get a new device. But you can often opt for a prepaid plan that doesn't require a credit check.

- Pause during an employment background check: Employers may view a limited version of your credit report as part of the background screening process. They may want to confirm information on your application or evaluate how you manage money if you're applying for a job that involves handling money. They won't see your credit score, but activities that lead to a poor score—such as recent bankruptcies or high debt—will be visible on your credit report and could affect whether you're hired for finance-related roles.

- Higher insurance premiums in some states: Car insurance companies in most states use information from your credit report, in addition to your driving history, to assess your potential risk of submitting a claim. There are restrictions on how your credit history can be factored into car insurance applications or rates in California, Hawaii, Maryland, Massachusetts, Michigan, Nevada, Oregon and Utah.

Learn more: Why Do You Want a Good Credit Score?

How to Improve a Bad Credit Score

No matter where your current credit score falls, you can boost your financial health starting now. Try these short- and long-term strategies to take control of your credit and improve your scores.

1. Check Your Credit Score

First, check your credit score for free to see where you stand. Your FICO® Score is most impacted by the following factors:

| Factors That Impact Your FICO® Score | |

|---|---|

| Payment history (35%) | Whether you always pay bills on time or have had late or missed payments in the past |

| Amounts owed (30%) | How much total credit you have available and how much of it you're actively using |

| Length of credit history (15%) | How long you've been using credit, plus the age of your oldest and newest credit accounts and average age of all your accounts |

| Credit mix (10%) | The different types of installment and revolving credit accounts you've had and are currently managing |

| New credit (10%) | The number of recent credit accounts you've opened and applications you've made |

It's also important to check your credit report for any inaccuracies. You have the right to dispute items on your credit report, including inaccurate personal information or accounts fraudulently opened in your name.

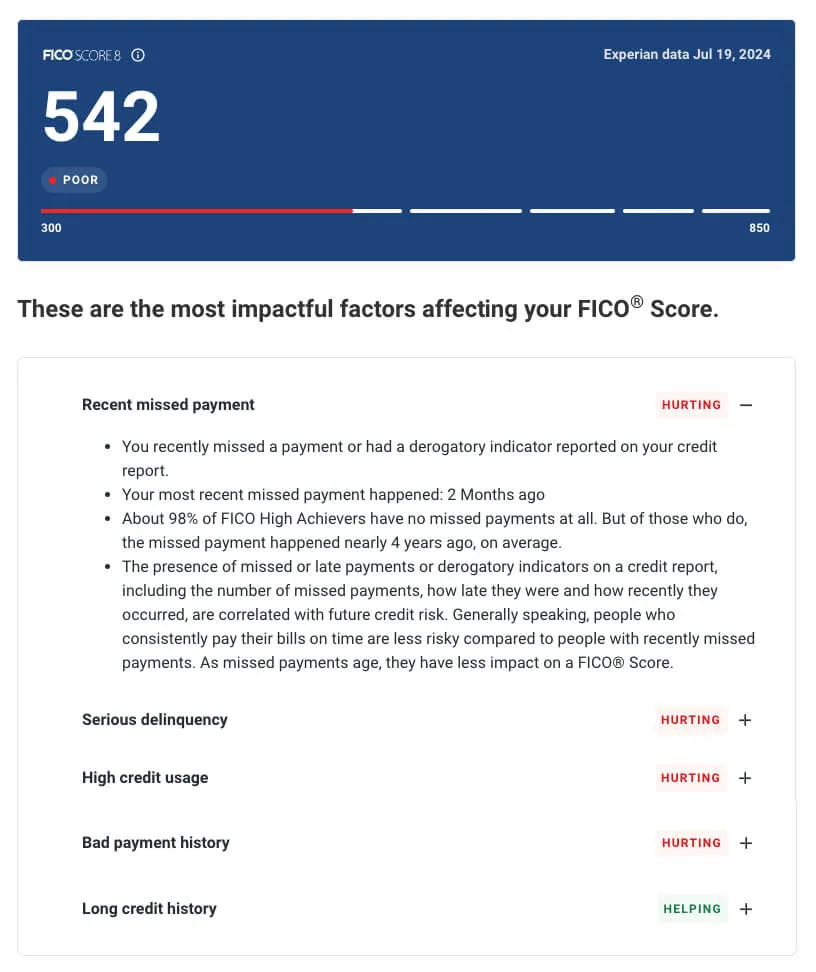

When reviewing your Experian credit report, you'll receive a summary of the factors affecting your credit. For the example below, factors like recent missed payments, delinquencies, bad payment history and high credit usage are all contributing to a bad credit score. Meanwhile, a long credit history is a positive factor helping the credit score.

2. Pay Your Bills on Time

Because payment history is the biggest contributor to your score, take steps to ensure you never pay late:

- Set up autopay. Opt for autopay for recurring bills, such as credit card and car payments. Your bill will come directly from your bank account on the day it's due, meaning you don't have to remember to log in to a payment portal or send a check. Ensure you have enough money in your checking account to cover your payments, or you could be subject to overdraft fees.

- Change your payment due date. If many of your bills are due on the same day of the month, making it more difficult to pay them on time, you may be able to change the payment due dates with your creditors. It could take a few billing cycles for the change to go into effect. Continue paying as required until the company has confirmed the update.

- Set calendar reminders. Create a payment reminder in your phone or calendar app at a time when you'll be able to make the payment right away.

- Ask for help. If you're concerned you're going to miss a payment, contact your creditor before it happens to explore what's possible. Federal student loans, for instance, come with alternative payment plans that can lower the amount you owe each month. Credit card issuers also may be able to reduce your payment or interest rate if you're experiencing financial hardship.

Learn more: Can One 30-Day Late Payment Hurt Your Credit?

3. Pay Down Debt

Work on paying down revolving debt, such as credit card debt. Ideally, you'll pay off your credit card bill in full at the end of every month. But if you can't, and you're currently carrying a balance, bring down that debt with these approaches:

- Debt avalanche method: Send extra money to the highest-interest card first, then continue to the next-highest-rate card when the first is paid off. This can save the most money in interest.

- Debt snowball method: Alternatively, pay off small balances first with any extra money, which may motivate you more as you pay off accounts more quickly.

- Balance transfer credit card: Once you have good enough credit to qualify, a balance transfer card provides a 0% introductory APR period that lets you pay off your balances without accruing more interest. To make the most of the card, come up with a plan that gets you debt-free within the interest-free time frame.

Learn more: What's the Best Strategy to Pay Off Debt?

4. Limit New Credit Inquiries

If you're focused on increasing your score, consider limiting or pausing new applications for credit. A hard inquiry happens when a lender checks your credit to evaluate you for a financial product. It will appear on your credit report and may knock a few points off your credit score. Lenders could also consider you a greater credit risk if you're attempting to borrow money from many different sources.

Soft inquiries don't affect your credit scores. They occur when you check your own credit score or when a lender or credit card issuer checks your credit to preapprove you for a product.

Learn more: Hard Inquiry vs. Soft Inquiry: What's the Difference?

5. Boost Your Credit

Signing up for Experian Boost®ø for free can help you strengthen credit using your existing financial history. Experian will search your bank account data for cellphone, utility, rent, insurance and popular streaming service payments, and you can choose which accounts to add to your Experian credit file. Once the accounts are added, a new credit score is instantly generated. Those who have little or poor credit could see an increase to their FICO® Score powered by Experian thanks to the addition of new positive payment history.

Instantly raise your credit scoresø

Add any bank accounts you use to pay your bills. Your information remains private.

We’ll detect bills with on-time payments, and you can add them to your Experian credit file.

You’ll find out right away if your credit scores increased and by how many points.

6. Get Help Building Credit

If you're having trouble getting approved for a credit card or loan on your own, you can build credit history with the help of others or with a secured credit card or credit-builder loan. Here's how:

- Become an authorized user on someone else's account. A trusted family member or friend can add you to their credit card account as an authorized user, and that account's credit limit and payment history will then appear on your credit report and possibly boost your credit score.

- Work with a cosigner who has good credit. When you have a cosigner for a loan, the lender considers their credit history in the application, improving your chances of approval and of adding positive payment history to your credit report. The lender then considers the cosigner jointly responsible for the debt.

- Apply for a secured credit card. With a secured credit card, you make a cash deposit that usually becomes your credit limit. That allows you to use the card like a traditional credit card and build credit history.

- Apply for a credit-builder loan. A credit-builder loan is a loan in reverse: You'll make payments to a lender and at the end of the loan's term, that money will be available to you in a savings account. Most important, like a secured card, it adds positive payments to your credit file without the risk of going into debt. Before you get a credit-builder loan, make sure the company reports to all three credit bureaus.

How Long Does It Take to Improve Your Credit Score?

There's no hard-and-fast rule that states when you can expect to see credit score improvements. But if you stick with responsible credit behavior and add positive payment history to your credit report, you can start to see improvements in a month. Large increases can take several months or more.

Learn more: How Long Does It Take to Build Credit?

How to Maintain a Good Credit Score

Once you've done the hard work to fix a bad credit score, keeping up the momentum is the next step. To get the best access to low rates and favorable terms on a range of financial products, aim for good credit or better. A good FICO® Score ranges from 670 to 739, while a very good score is 740 to 799.

Here's how to keep your credit strong:

- Pay all bills on time.

- Maintain low balances on credit cards, ideally by paying off your whole balance each month.

- Only seek out new credit when necessary.

- Keep your oldest credit card account open to lengthen your credit history.

- Make a budget that helps you spend less than you earn and also set aside money for savings, debt repayment and other goals.

The Bottom Line

Poor credit isn't a reflection of who you are as a person; it's merely data about your personal financial history, and it's never too late to tell a new story. Start with strategies that improve your score, and then use your newfound knowledge and confidence to keep your score robust. Once you start seeing the positive effects of having good credit, you may be even more motivated to continue on the journey.

Instantly raise your FICO® Score for free

Use Experian Boost® to get credit for the bills you already pay like utilities, mobile phone, video streaming services and now rent.

No credit card required

About the author

Brianna McGurran

Brianna McGurran is a freelance journalist and writing teacher based in Brooklyn, New York. Most recently, she was a staff writer and spokesperson at the personal finance website NerdWallet, where she wrote "Ask Brianna," a financial advice column syndicated by the Associated Press.

Read more from Brianna