847 Credit Score: Is it Good or Bad?

Your 847 FICO® ScoreΘ falls in the range of scores, from 800 to 850, that is categorized as Exceptional. Your FICO® Score is well above the average credit score, and you are likely to receive easy approvals when applying for new credit.

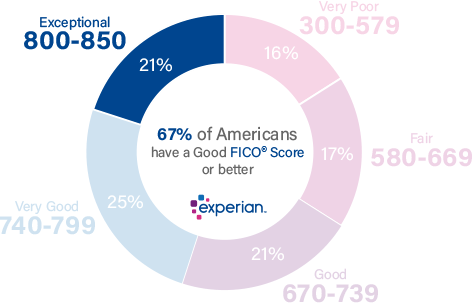

21% of all consumers have FICO® Scores in the Exceptional range.

Less than 1% of consumers with Exceptional FICO® Scores are likely to become seriously delinquent in the future.

How to improve your 847 Credit Score

A FICO® Score of 847 is well above the average credit score of 714. An 847 FICO® Score is nearly perfect. You still may be able to improve it a bit, but while it may be possible to achieve a higher numeric score, lenders are unlikely to see much difference between your score and those that are closer to 850.

Among consumers with FICO® credit scores of 847, the average utilization rate is 4.7%.

The best way to determine how to improve your credit score is to check your FICO® Score. Along with your score, you'll receive a report that uses specific information in your credit report that indicates why your score isn't even higher.

Because your score is extraordinarily good, none of those factors is likely to be a major influence, but you may be able to tweak them to get even closer to perfection.

Why you should be pleased with an Exceptional FICO® Score

Your 847 FICO® Score is nearly perfect and will be seen as a sign of near-flawless credit management. Your likelihood of defaulting on your bills will be considered extremely low, and you can expect lenders to offer you their best deals, including the lowest-available interest rates. Credit card issuers are also likely to offer you their most deluxe rewards cards and loyalty programs.

Late payments 30 days past due are rare among individuals with Exceptional credit scores. They appear on just 0.4% of the credit reports of people with FICO® Scores of 847.

An Exceptional credit score can mean opportunities to refinance older loans at more attractive interest, and excellent odds of approval for premium credit cards, auto loans and mortgages.

Keep watch over your hard-earned credit score

A FICO® Score of 847 is an accomplishment built up over time. It takes discipline and consistency to build up an Exceptional credit score. Additional care and attention can help you keep hang on to it.

Whether instinctively or on purpose, you're doing a remarkable job navigating the factors that determine credit scores:

Utilization rate on revolving credit. Utilization, or usage rate, is a measure of how close you are to “maxing out” credit card accounts. You can calculate it for each of your credit card accounts by dividing the outstanding balance by the card's borrowing limit, and then multiplying by 100 to get a percentage. You can also figure your total utilization rate by dividing the sum of all your card balances by the sum of all their spending limits (including the limits on cards with no outstanding balances).

| Balance | Spending limit | Utilization rate (%) | |

|---|---|---|---|

| MasterCard | $1,200 | $4,000 | 30% |

| VISA | $1,000 | $6,000 | 17% |

| American Express | $3,000 | $10,000 | 30% |

| Total | $5,200 | $20,000 | 26% |

If you keep your utilization rates at or below 30%— on all accounts in total and on each individual account—most experts agree you'll avoid lowering your credit scores. Letting utilization creep higher will depress your score, and approaching 100% can seriously drive down your credit score. Utilization rate is responsible for nearly one-third (30%) of your credit score.

Late and missed payments matter a lot. If late or missed payments played a major part in your credit history, you wouldn't have an Exceptional credit score. But keep on mind that no single factor helps your credit score more significantly than prompt payment behavior, and few things can torpedo a near-perfect score quicker than missing a payment.

Time is on your side. Length of credit history is responsible for as much as 15% of your credit score.If all other score influences hold constant, a longer credit history will yield a higher credit score than a shorter one.

Credit applications and new credit accounts typically have short-term negative effects on your credit score. When you apply for new credit or take on additional debt, credit-scoring systems flag you as being at greater risk of being able to pay your bills. Credit scores drop a small amount when that happens, but typically rebound within a few months, as long as you keep up with all your payments. New credit activity can contribute up to 10% of your overall credit score.

Debt composition. The FICO® credit scoring system tends to favor multiple credit accounts, with a mix of revolving credit (accounts such as credit cards that enable you to borrow against a spending limit and make monthly payments of varying amounts) and installment loans (e.g., car loans, mortgages and student loans, with set monthly payments and fixed payback periods). Credit mix is responsible for about 10% of your credit score.

When public records appear on your credit report they can have severe negative impacts on your credit score. Entries such as bankruptcies do not appear in every credit report, so they cannot be compared to other credit-score influences in percentage terms, but they can overshadow all other factors and severely lower your credit score.

The average mortgage loan amount for consumers with Exceptional credit scores is $233,324. People with FICO® Scores of 847 have an average auto-loan debt of $18,481.

Shield your credit score from fraud

People with Exceptional credit scores can be prime targets for identity theft, one of the fastest-growing criminal activities.

The average synthetic identity theft loss is $6,000 according to data from Experian.

Credit-monitoring and identity theft protection services can help ward off cybercriminals by flagging suspicious activity on your credit file. By alerting you to changes in your credit score and suspicious activity on your credit report, these services can help you preserve your excellent credit and Exceptional FICO® Score.

By using credit monitoring to keep track of your credit score, you'll also know if it starts to dip below the Exceptional range of 800-850, and you can act quickly to try to help it recover.

Learn more about your credit score

An 847 credit score is Exceptional. Get your free credit report from Experian and check your credit score to better understand why it’s so good, and how to keep it that way. Read more about score ranges and what a good credit score is.