What Is Credit Mix?

Quick Answer

- Your credit mix is the variety of credit account types you have on your credit report.

- A good credit mix includes both revolving accounts, like credit cards, and installment accounts, like auto loans. It makes up 10% of your FICO Score.

Credit mix refers to the different types of credit accounts on your credit report, and it's one of the factors that help determine your credit scores.

While credit mix carries less weight than payment history or credit utilization, maintaining a healthy combination of revolving and installment accounts over time can help nudge a good credit score into excellent territory. Here's what you need to know about how credit mix works.

What Is Credit Mix?

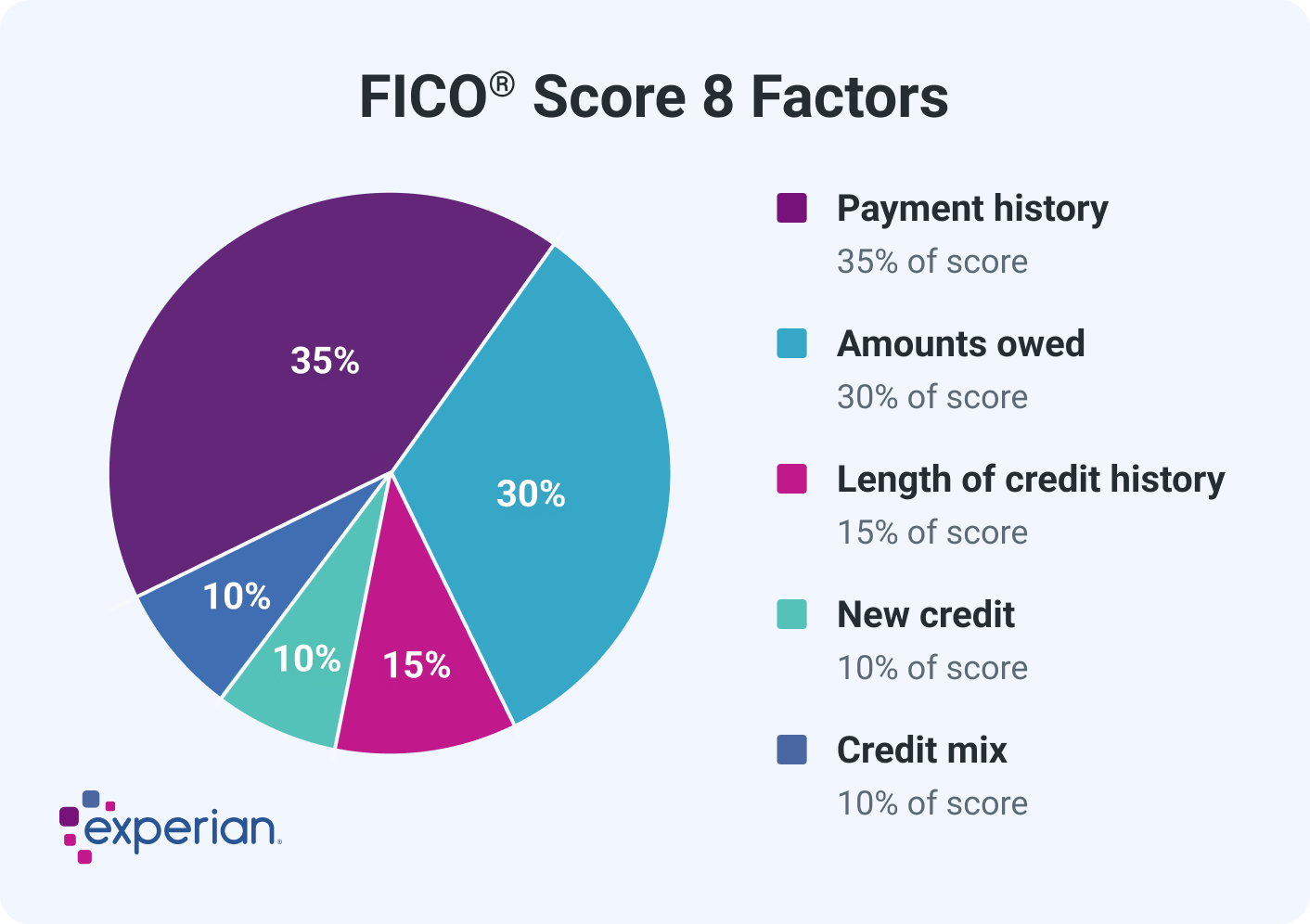

Credit mix measures how diverse your borrowing experience is across different account types. It's one of the five factors that determine your FICO® ScoreΘ, the score used by 90% of top lenders, and it accounts for 10% of your score.

Lenders see a diverse credit mix as a sign that you can handle multiple kinds of debt responsibly. Managing a credit card, which lets you borrow and repay flexibly, is a different skill from making a fixed monthly payment on an installment loan such as an auto loan or mortgage. Demonstrating both can mark you as a more reliable borrower.

That said, it's unwise to open new accounts just to boost this factor. Credit mix carries a relatively small impact compared with other scoring categories, and lenders are unlikely to focus on it when deciding whether to approve your application. The downsides of a new account include the hard inquiry associated with the application, reduced average account age or possibly even missed payments. These factors can easily outweigh any small gain from an improved credit mix.

Learn more: How Is Your Credit Score Calculated?

What Are the Different Types of Credit?

There are two main types of credit: revolving credit and installment credit. Having both on your credit report can help your credit mix.

Revolving Credit

With a revolving credit account, you're assigned a credit limit and can borrow, repay and re-borrow up to that limit. Common examples include:

Installment Credit

Installment credit provides a lump sum that you repay in fixed payments over a set term. Common examples include:

What Isn't Part of Credit Mix?

A few common borrowing products typically aren't part of your credit mix, mainly because they don't appear on your credit report or aren't factored into standard credit score calculations. These are:

It's important to note that some BNPL providers do report your payments to the credit bureaus, and lenders can see those accounts. They don't contribute to your basic credit scores, however, so they're not included in your credit mix.

Even though BNPL products don't help your credit mix, they can still hurt your credit indirectly. If you default and the lender sends the debt to a collection agency, it'll be reported as a collection account. That can be a serious negative mark on your payment history, which is the single biggest factor in your credit score.

What Is a Good Credit Mix?

There's no formal definition of an ideal credit mix, but at a minimum, having at least one revolving account and one installment account on your credit report is a solid foundation.

Often, a strong credit mix evolves organically as you make normal financial moves over time. A recent college graduate paying off a student loan, for example, will improve their credit mix when the time comes to open their first credit card.

Later, financing a car or buying a home can diversify the mix further. The takeaway is that a good credit mix is something you build through real life, not by chasing tradelines (credit accounts listed on your credit report).

How to Improve Your Credit Mix

As mentioned, your credit mix isn't likely to make or break a credit application, so it's generally not worth opening new accounts solely to diversify it. If you're aiming for a top-tier credit score, though, these strategies can help your mix improve responsibly over time:

- Apply for credit only when you need it. Diversifying your credit mix is a long game—it naturally improves as you add new accounts to your credit file. As you take on a new credit card for better rewards, an auto loan to buy a car or a mortgage to buy a home, your mix will broaden on its own

- Become an authorized user. If you're just starting to build credit and can't qualify for a credit card on your own, ask a financially responsible loved one to add you as an authorized user on their credit card. The account can show up on your credit reports and help with both your credit mix and other scoring factors.

- Avoid frequent credit applications. Opening multiple accounts in a short period can damage your score and make it harder to qualify for credit when you actually need it. Space out applications and only apply when there's a clear reason.

- Pay every account on time. A diverse credit mix means nothing if you fall behind. Since payment history is the most influential credit scoring factor, on-time payments protect the gains a stronger mix can deliver.

Frequently Asked Questions

Monitor Your Credit Score to Track Your Progress

Whether you're working to build your credit score or maintain a good credit score, regularly monitoring your credit is one of the smartest habits you can build. With Experian, you can check your Experian credit report and FICO® Score for free anytime.

You can also receive real-time alerts when changes are made to your Experian credit report, which makes it easier to catch potential identity theft and other issues.

Instantly raise your FICO® Score for free

Use Experian Boost® to get credit for the bills you already pay like utilities, mobile phone, video streaming services and now rent.

No credit card required

About the author

Ben Luthi

Ben Luthi has worked in financial planning, banking and auto finance, and writes about all aspects of money. His work has appeared in Time, Success, USA Today, Credit Karma, NerdWallet, Wirecutter and more.

Read more from Ben