Why Is Building Credit Important?

Quick Answer

Building credit demonstrates financial responsibility and helps you access loans, favorable interest rates, better housing options, lower insurance premiums and more financial opportunities.

Building good credit demonstrates financial responsibility and unlocks access to loans, favorable interest rates, better housing options and more. Your credit history and credit score serve as a financial report card that lenders, landlords and even some employers use to evaluate your reliability.

Whether you're planning to buy a home, finance a car or simply rent an apartment, your credit plays a crucial role in your financial life. Understanding why credit matters—and how to build it effectively—can help you achieve your financial goals while saving money along the way.

Benefits of Building Good Credit

Establishing a strong credit history offers numerous advantages that extend far beyond simply qualifying for a credit card. Here are the key benefits of building good credit.

Access to Loans

Good credit is essential when applying for significant loans like mortgages, auto loans and personal loans. Lenders use your credit history to assess the risk of lending you money. A solid credit profile demonstrates that you've borrowed responsibly in the past and are likely to repay future debts.

Without established credit, you may struggle to qualify for these loans or face limited options with less favorable terms. Some lenders may even require a cosigner if your credit history is thin or nonexistent, which can complicate the borrowing process.

Learn more: What Is a Thin Credit File?

More Favorable Interest Rates

Your credit score could directly impact the interest rates you're offered on loans and credit cards. Borrowers with higher credit scores typically qualify for lower interest rates, which can translate to substantial savings over the life of a loan.

Example: On a 30-year mortgage, even a difference of one percentage point in your interest rate can mean tens of thousands of dollars in additional interest costs. The same principle applies to auto loans, personal loans and credit cards: Better credit usually means less money paid in interest.

Learn more: Ways to Pay Less Interest on an Auto Loan

Better Credit Card Options

Building good credit opens the door to premium credit cards with valuable rewards, perks and benefits. These cards often offer cash back, travel points, trip protections and other features that can enhance your purchasing power.

Without good credit, you'll likely be limited to cards with higher interest rates, annual fees and fewer rewards. Some people without established credit may need to start with a secured credit card, which requires a cash deposit.

Easier Approval for Rental Housing

Many landlords and property management companies review credit reports and scores when evaluating rental applications. A good credit history signals that you're likely to pay rent on time and fulfill your lease obligations.

Poor credit or no credit history can make it harder to secure desirable rental housing. Some landlords may require larger security deposits or deny applications altogether based on credit concerns.

Learn more: Can I Rent an Apartment Without a Credit Check?

Employment Opportunities

Some employers check credit reports as part of the hiring process, particularly for positions that involve financial responsibilities or access to sensitive information. While employers cannot see your credit score, they can review your credit report for signs of financial distress.

A history of missed payments, collection accounts or bankruptcies might raise concerns for certain employers. Building good credit helps ensure your credit report won't become an obstacle in your career.

Lower Insurance Premiums

In most states, insurance companies can use credit-based insurance scores to help determine auto and homeowners insurance premiums. These scores are calculated using information from your credit report, though they differ from traditional credit scores.

Studies have shown a correlation between credit history and insurance claims, which is why insurers consider this factor. Better credit could lead to lower insurance costs, saving you money on necessary coverage.

Utility Services Without Deposits

When setting up utilities like electricity, gas or internet service, providers often check your credit to evaluate your payment history. Customers with good credit can typically activate services without paying a security deposit.

Those with limited or poor credit may need to pay deposits upfront, tying up money that could be used elsewhere. Building credit helps you avoid these additional costs when establishing essential services.

Learn more: How Utility Bills Can Boost Your Credit Score

Instantly raise your credit scoresø

Add any bank accounts you use to pay your bills. Your information remains private.

We’ll detect bills with on-time payments, and you can add them to your Experian credit file.

You’ll find out right away if your credit scores increased and by how many points.

How to Build Credit

Building credit takes time and consistent financial habits, but the following strategies can help you establish and strengthen your credit profile:

- Pay all your bills on time. Payment history is the most important factor in your FICO® ScoreΘ. Set up automatic payments or reminders to ensure you never miss a due date, as even one late payment can significantly damage your credit.

- Keep your credit utilization low. Credit utilization—the percentage of your available credit you're using on revolving accounts like credit cards—also affects your credit score. Aim to use less than 30% of your credit limits, and ideally keep utilization in the single digits for the best impact.

- Become an authorized user. If someone with good credit adds you as an authorized user on their credit card, the card's account history may appear on your credit report. This can help you build credit even if you don't use the card.

- Get a secured credit card. Secured cards require a cash deposit, usually equal to your desired credit limit. They work like regular credit cards and can help you establish a payment history when you're starting from scratch.

- Maintain older credit accounts. The length of your credit history matters, so keep older accounts open even if you don't use them frequently. Closing old accounts can shorten your credit history and potentially lower your scores.

- Limit new credit applications. Each credit application typically results in a hard inquiry on your credit report, which can temporarily lower your scores a few points. Apply for new credit only when necessary.

- Monitor your credit reports. Review your credit reports from all three major credit bureaus (Experian, TransUnion and Equifax) regularly to check for errors or signs of identity theft. You have the right to dispute inaccuracies, which helps protect your credit.

- Diversify your credit mix. Having different types of credit, such as credit cards, installment loans and retail accounts, can positively impact your scores. However, don't open accounts you don't need just for the sake of variety. You can naturally diversify your credit mix over time.

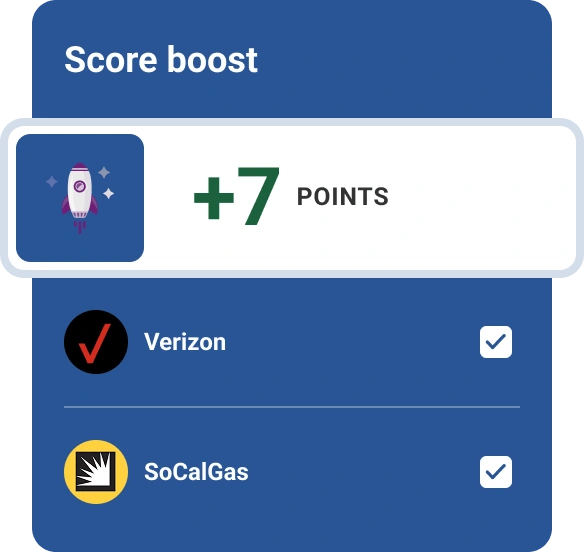

- Try Experian Boost®ø. Experian Boost is a free feature that gives you credit for on-time payments to rent, utility, cellphone and certain streaming service accounts on your Experian credit report. Signing up for Experian Boost could give you an immediate lift to your credit scores powered by Experian data.

- Consider applying for a credit-builder loan. Credit-builder loans are specialized loans designed to help people build credit. The money you borrow is held in a savings account while you make payments, and those payments are reported to the credit bureaus. Just make sure the lender reports to all three credit bureaus for the best results.

How Long Does It Take to Build Credit?

The time it takes to build credit depends on your starting point and the actions you take. If you're building credit from scratch with no credit history, you can typically generate a FICO® Score after six months of opening your first credit account, as long as that account is being reported to the credit bureaus. It's just a single month for VantageScore® credit scores.

However, building good credit—not just establishing a credit score—takes longer. Achieving and maintaining a score in the "good" range (generally 670 or higher on the FICO® Score scale) often requires several years of responsible credit use.

If you're rebuilding credit after negative events like missed payments or collections, the process can take longer. Negative items remain on your credit reports for seven years in most cases, though their impact on your scores diminishes over time as you add positive history.

Whatever you do, know that there are no shortcuts to building solid credit—it requires patience and consistent financial responsibility.

Tip: If you're brand new to credit and want to learn more about how credit works and why it's important, the Experian Credit Course: A Complete Guide to Credit can help you get up to speed.

Frequently Asked Questions

The Bottom Line

Building credit is a fundamental step toward financial wellness and independence. The benefits extend throughout your financial life, from securing better loan terms to accessing premium credit cards and rental housing.

Start with simple steps: Open a credit account appropriate for your situation, make all payments on time and keep your balances low. Monitor your progress by checking your credit reports regularly and consider using free tools to track your credit score over time. If you don't yet have a credit report, you can also use Experian Go™ to establish a report and get tips on how to build credit.

As you work to establish your good credit habits, Experian's free credit monitoring tool allows you to see how your credit-building efforts are paying off. With patience and responsible financial habits, you can establish strong credit that serves you well for years to come.

Instantly raise your FICO® Score for free

Use Experian Boost® to get credit for the bills you already pay like utilities, mobile phone, video streaming services and now rent.

No credit card required

About the author

Ben Luthi

Ben Luthi has worked in financial planning, banking and auto finance, and writes about all aspects of money. His work has appeared in Time, Success, USA Today, Credit Karma, NerdWallet, Wirecutter and more.

Read more from Ben