Can You Pay Utilities With a Credit Card?

Quick Answer

You can pay your utility bill with a credit card, but you may pay convenience fees. However, it could also help you earn rewards and ensure your bills get paid even when your checking account is empty.

When life gets busy, you can easily forget to pay a bill or two. But fail to pay your utility bill and you could end up without essential services like electricity or water. To ensure your utility bills are covered every month, you can pay utility bills with a credit card, but there may be a convenience fee and other factors to consider. Here are some pros and cons to understand before paying a utility bill with your credit card.

What Utilities Can You Pay With a Credit Card?

While payment options may vary depending on your utility provider, you can usually pay the following utility bills with a credit card:

- Phone or cellphone bill

- Internet bill

- Cable bill

- Water bill

- Electric bill

- Gas bill

Best credit cards of 2026

Compare cards from our partners with intro bonuses, cash back or points offers, and annual fees as low as $0.

Offers from our partners

Citi Double Cash® Card

Intro APR:0% for 18 months on Balance Transfers

Ongoing APR:17.49% - 27.49% (Variable)

Rewards:2% (cash back)

Annual Fee:$0

Blue Cash Everyday® Card from American Express

Intro bonus:As High As $200 Cash Back. Find Out Your Offer.

Intro APR:0% on Purchases and Balance Transfers for 15 months

Ongoing APR:19.49%-28.49% Variable

Rewards:1% - 3% (cash back)

Annual Fee:$0

Wells Fargo Reflect® Card

Intro APR:0% intro APR for 21 months from account opening on purchases and qualifying balance transfers

Ongoing APR:17.49%, 23.99%, or 28.24% Variable APR

Rewards:N/A*

Annual Fee:$0

American Express Platinum Card®

Intro bonus:As high as 175,000 points. Find out your offer.

Ongoing APR:See Pay Over Time APR

Rewards:1x - 5x (Points per dollar)

Annual Fee:$895

Wells Fargo Active Cash® Card

Intro bonus:$200

Intro APR:0% intro APR for 12 months from account opening on purchases and qualifying balance transfers

Ongoing APR:18.49%, 24.49%, or 28.49% Variable APR

Rewards:2% (Cash Rewards)

Annual Fee:$0

Discover it® Cash Back

Intro bonus:Cashback Match™

Intro APR:0% intro APR for 15 months on Purchases and Balance Transfers

Ongoing APR:17.49% - 26.49% Variable APR

Rewards:1% - 5% (cash back)

Annual Fee:$0

FIT™ Platinum Mastercard® - $400 Credit Limit

Ongoing APR:35.90% Fixed

Rewards:N/A*

Annual Fee:$99 first year; $125 thereafter

Avant® Cashback Rewards Mastercard®

Ongoing APR:29.99%*

Rewards:2% (cash back)

Annual Fee:$0*

The opensky® Secured Visa® Credit Card

Ongoing APR:23.89% Variable

Rewards:10% (cash back)

Annual Fee:$35

Credit One Bank American Express® Card for Rebuilding Credit

Ongoing APR:29.74% Variable

Rewards:1% (cash back)

Annual Fee:$75 First year. $99 thereafter, billed monthly at $8.25

Blue Cash Preferred® Card from American Express

Intro bonus:As High As $300 Cash Back. Find Out Your Offer.

Intro APR:0% on Purchases and Balance Transfers for 12 months

Ongoing APR:19.49%-28.49% Variable

Rewards:1% - 6% (cash back)

Annual Fee:$0 intro annual fee for the first year, then $95.

American Airlines AAdvantage® MileUp® Card

Intro APR:0% for 15 months on Balance Transfers

Ongoing APR:19.49% - 29.49% (Variable)

Rewards:2x (Miles per dollar)

Annual Fee:$0

Costco Anywhere Visa® Card by Citi

Ongoing APR:18.74% - 26.74% (Variable)

Rewards:1% - 5% (cash back)

Annual Fee:$0

American Express® Gold Card

Intro bonus:As high as 100,000 points. Find out your offer.

Ongoing APR:See Pay Over Time APR

Rewards:1x - 4x (Points per dollar)

Annual Fee:$325

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$75*

Citi® / AAdvantage® Globe™ Mastercard®

Ongoing APR:19.49% - 29.49% (Variable)

Rewards:1x - 6x (Miles per dollar)

Annual Fee:$350

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$39*

First Progress Select Secured Mastercard® Cash Back Rewards

Ongoing APR:17.49% Variable

Rewards:1% - 10% (cash back)

Annual Fee:$39

Credit One Bank® Platinum Visa®

Ongoing APR:29.74% Variable

Rewards:1% (cash back)

Annual Fee:$39

Credit One Bank® Wander® American Express® with Dining, Gas & Travel Rewards

Ongoing APR:29.74% Variable

Rewards:1% - 10% (cash back)

Annual Fee:$95

Hilton Honors American Express Card

Intro bonus:70,000 Points

Ongoing APR:19.49%-28.49% Variable

Rewards:3x - 7x (Points per dollar)

Annual Fee:$0

Marriott Bonvoy Brilliant® American Express® Card

Intro bonus:200,000 Points

Ongoing APR:19.49%-28.49% Variable

Rewards:2x - 6x (Points per dollar)

Annual Fee:$650

Discover it® Miles

Intro bonus:Discover Match®

Intro APR:0% intro APR for 15 months on Purchases and Balance Transfers

Ongoing APR:17.49% - 26.49% Variable APR

Rewards:1.5x (Miles per dollar)

Annual Fee:$0

Delta SkyMiles® Reserve American Express Card

Intro bonus:As High As 100,000 Bonus Miles. Find Out Your Offer.

Ongoing APR:19.49%-28.49% Variable

Rewards:1x - 3x (Miles per dollar)

Annual Fee:$650

Delta SkyMiles® Gold American Express Card

Intro bonus:As High As 80,000 Bonus Miles. Find Out Your Offer.

Ongoing APR:19.49%-28.49% Variable

Rewards:1x - 2x (Miles per dollar)

Annual Fee:$0 introductory annual fee for the first year, then $150.

Delta SkyMiles® Blue American Express Card

Intro bonus:10,000 Miles

Ongoing APR:19.49%-28.49% Variable

Rewards:1x - 2x (Miles per dollar)

Annual Fee:$0

PREMIER Bankcard® Mastercard® Credit Card

Ongoing APR:See Rates & Fees

Rewards:N/A*

Annual Fee:See Rates & Fees

One Key™ Card

Intro bonus:$300

Ongoing APR:18.49%, 23.49%, or 28.49% Variable APR

Rewards:1.5x - 3x (Points per dollar)

Annual Fee:$0

One Key+™ Card

Intro bonus:$350

Ongoing APR:18.49%, 23.49%, or 28.49% Variable APR

Rewards:2x - 3x (Points per dollar)

Annual Fee:$99

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$0*

See all our best credit cards for 2026.

Pros and Cons of Paying Utility Bills With a Credit Card

When considering paying utility bills with a credit card, evaluate the pros and cons first.

Pros of Paying Utilities With a Credit Card

- You could earn credit card rewards. Using a credit card that earns rewards to pay your utility bills can help you garner more perks such as points, miles or cash back.

- You might benefit from purchase protection. While not all credit cards have this feature, some cards provide purchase protection for items you use the card to pay for. You may be able to get protection for damage or theft to your cellphone, for example, with certain cards if you pay your bills with that card.

- It can help you qualify for a welcome bonus. Some credit cards give new cardholders a welcome bonus or introductory bonus if they spend a certain dollar figure within a short time after opening the account. Using such a card to pay your utility bill could push your spending over the limit you need to earn the bonus.

- It ensures your payments go through. When you set up automatic bill payments from your checking account, you'll have to make sure your account has sufficient funds to cover the bill on the due date. If your account balance tends to fluctuate and you forget to check it before a bill comes due, your payment might not go through. That might mean late fees from the utility company, an interruption in service or an overdraft fee from your bank. Using a credit card for your autopayments can give you peace of mind that your payments will be made on schedule.

- It can simplify disputing charges. Should a questionable charge appear on your utility bill, paying with a credit card can help you get your money back. Once you dispute a credit card charge, you don't have to pay the disputed amount or any interest it accrues until the dispute has been reviewed. If your automated payment was made with a checking account, however, you must wait for the review to be completed before you'll get your money back.

- It could help boost your credit score. Are you new to using credit? Paying credit card bills on time can help you build a solid credit history. Even something as small as regularly paying a streaming service subscription with a credit card can demonstrate your responsible credit usage, or keep active a card you no longer use for everyday purchases.

Cons of Paying Utilities With a Credit Card

- There may be a convenience fee. Some utility providers charge a convenience fee for paying your bill with a credit card. While the fee may only be a few dollars, you'll pay it every month, which adds up over the year. Often, these convenience fees total more than the credit card rewards you can earn by paying the bill. Before opting to pay with a credit card to earn rewards, carefully weigh the potential rewards against any fees. On the flip side, some utility companies give you a discount if you pay directly from your checking account. Ask if yours does.

- Your credit score could suffer. Depending on your utility charges, how many utilities you pay with the same card and your credit limit, it's possible that paying utility bills with a credit card could push your credit utilization ratio too high. Using more than 30% of your available revolving credit can negatively affect your credit score. For example, if you have a credit card with a $1,000 limit and you put $400 worth of utility bills on it every month, you're using 40% of your available credit. To avoid this risk, estimate your monthly utility bills and, if necessary, spread them across multiple credit cards to avoid overloading any one card.

- You could end up paying interest. If you use a credit card to pay your utility bills and don't pay the balance in full when it's due, your balance will begin to accrue interest. Credit card interest is generally compounded daily. With current credit card annual percentage rates (APRs) topping 20%, interest can quickly snowball, making it harder to pay off your balance.

How to Pay Utilities With a Credit Card

You can typically set up automatic payments for your utility bills on the utility provider's website or by calling the company. Some providers accept credit card payments directly, while others require you to go through a third-party processor, such as Plastiq.

Third-party companies generally charge fees; these may be in addition to fees charged by the utility company. Before setting up automatic credit card payments, make sure you clearly understand all the fees involved.

How On-Time Utility Payments Can Improve Your Credit

Utility providers don't report your payments to the three major credit bureaus (Experian, TransUnion and Equifax). As a result, utility payments traditionally don't help—or hurt—your credit score. (One exception: If your payments are so late that your debt is sent to collections or charged off, it shows up on your credit report and can lower your credit score.)

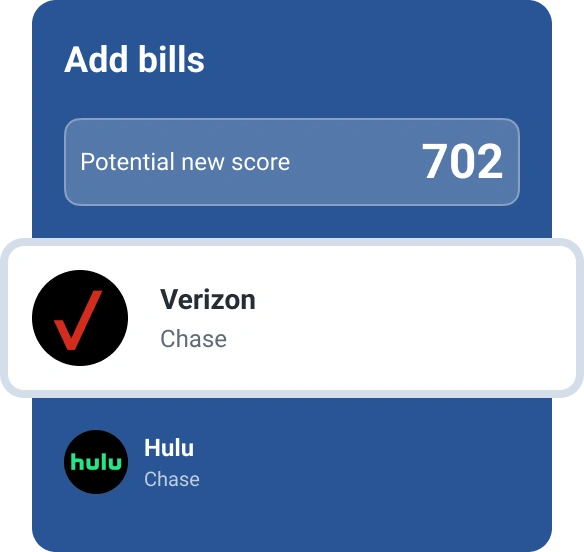

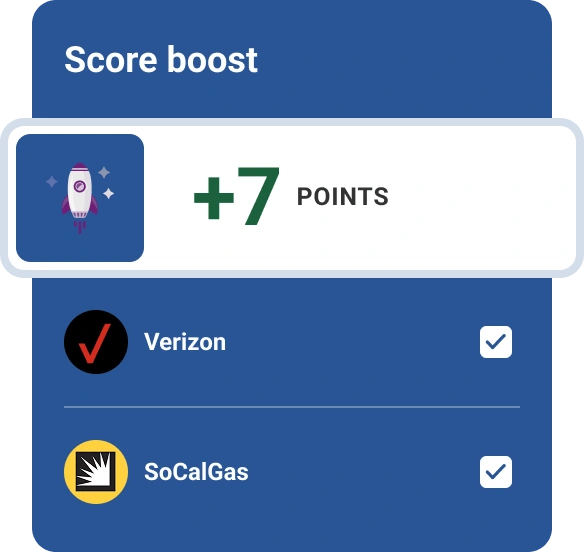

However, there is a way to use on-time utility payments to help improve your credit score. Experian Boost®ø is a free feature that lets you add utility accounts to your Experian credit report and potentially boost your credit score. You can select which accounts to add, including utilities, cable, cellphone and many streaming services. Since Experian Boost only reports on-time payments, you can rest easy that a late payment won't hurt your credit score.

Instantly raise your credit scoresø

Add any bank accounts you use to pay your bills. Your information remains private.

We’ll detect bills with on-time payments, and you can add them to your Experian credit file.

You’ll find out right away if your credit scores increased and by how many points.

The Bottom Line

Planning to pay utilities with a credit card? Be sure to keep an eye on your credit card balances so an unexpectedly high electric bill doesn't push your credit utilization too high. Experian's free credit monitoring service sends you real-time alerts of important changes in your credit report. It also includes access to your FICO® ScoreΘ and Experian credit report, so you can be sure paying utility bills with credit cards isn't hurting your credit score.

Don’t apply blindly

Apply for credit cards confidently with personalized offers based on your credit profile. Get started with your FICO® Score for free.

See your offersAbout the author

Karen Axelton

Karen Axelton is Experian’s in-house senior personal finance writer. She has over 20 years of experience as a journalist and has written or ghostwritten content for a variety of financial services companies.

Read more from Karen