What Is Net Worth?

Quick Answer

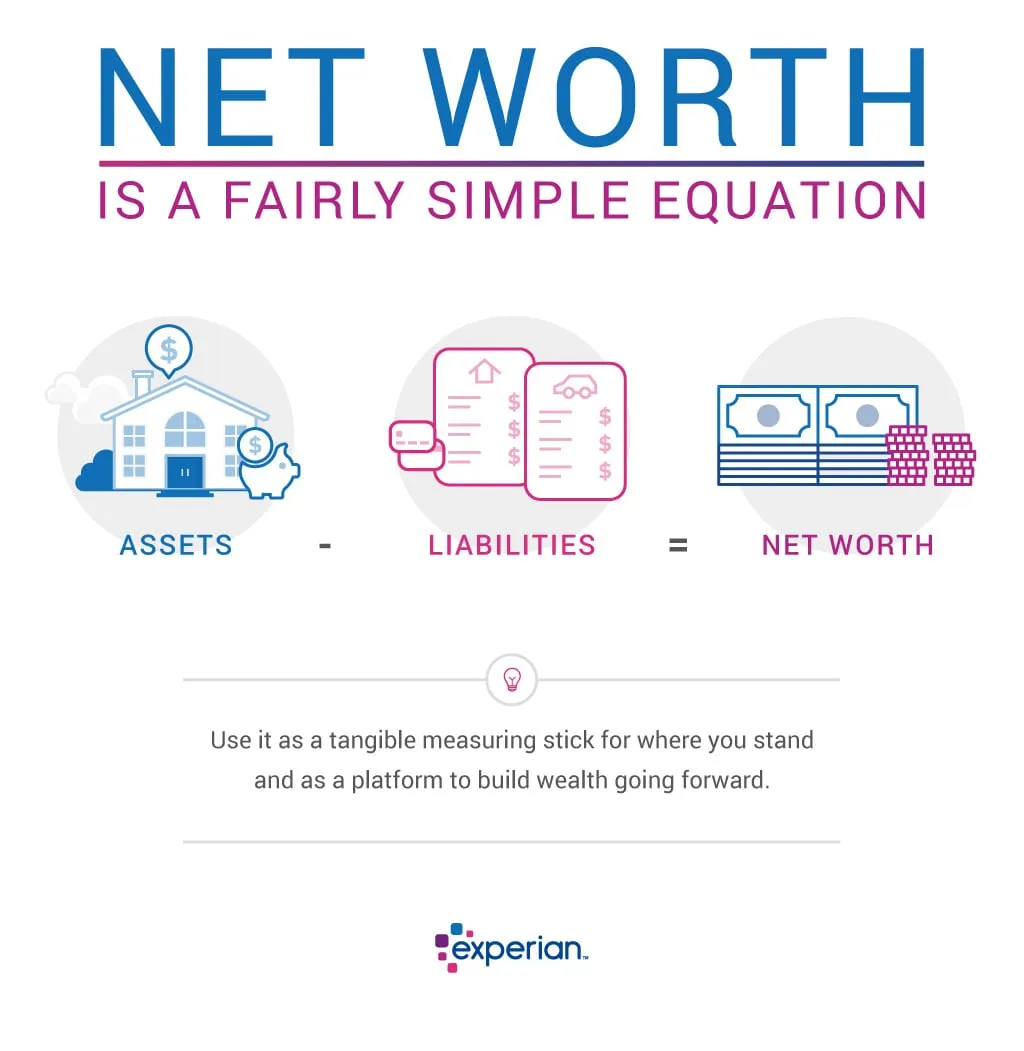

Net worth is equal to the difference between your assets and liabilities. It tells you whether you owe more than you own, or vice versa. Over time, net worth can show your progress toward financial goals—or point out a need to correct course.

Net worth is the total value of your assets minus your liabilities. Net worth gives you a snapshot of your finances that can help you size up your financial health and measure your progress toward financial goals.

Here's more about what net worth is, how to calculate it and how to use it to better understand your financial position.

What Is Net Worth?

Net worth is the difference between your total assets and total liabilities. One way to think about it: Net worth is what would be left over if you cashed out all your assets and paid off your debts.

Net worth is separate from income, and it's a good complement for measuring your financial health. Use net worth to understand the relationship between what you owe and what you own. It can tell you whether you're overextended on debt—or heading in that direction. It can also show your progress toward financial goals. Together with your budget, debt-to-income ratio and credit score, your net worth is a valuable indicator of how you're doing financially.

How to Calculate Net Worth

To calculate your net worth, add up your assets and subtract your liabilities. You can start with a blank sheet of paper, an online net worth calculator or a spreadsheet. Here are the basic steps you'll follow:

1. Total Your Assets

Make a list of your assets, including bank account balances, retirement funds, investments and major assets like your home, cars, valuables and life insurance. Using the template below, estimate the value of each asset, then total up your assets on the last line.

| Asset Category | Examples | How to Estimate Value | Your Amount |

|---|---|---|---|

| Cash | Savings, checking and money market accounts | Check your online account or statement | |

| Retirement | 401(k)s, IRAs | Check your online account or statement | |

| Taxable investments | Brokerage accounts, cryptocurrency | Check your online account or statement | |

| Home value | What your home is worth | Use a home value estimator or home appraisal | |

| Vehicles (owned or financed, not leased) | What your cars are worth | Use a car valuation site | |

| Other major assets | Health savings accounts, cash value life insurance, real estate, collectibles, art, jewelry, boats, RVs | Check your online account or use an online marketplace or online valuation tool to estimate value |

2. Add Up Your Liabilities

Make a list of your outstanding debts. Check your accounts to get your most recent loan balance or payoff amount, then total your debts on the final line of the template below.

| Asset Category | Examples | How to Estimate Value | Your Amount |

|---|---|---|---|

| Mortgage | Primary mortgage, home equity loan or home equity line of credit | Most recent statement balance or payoff amount | |

| Auto loans | Car loans | Most recent statement balance or payoff amount | |

| Student loans | Student loans | Most recent statement balance or payoff amount | |

| Credit cards | Credit cards | Most recent statement balance or payoff amount | |

| Personal loans | Secured or unsecured personal loans | Most recent statement balance or payoff amount | |

| Other debts | Unpaid taxes, loans from friends or family, 401(k) loans | Most recent statement balance or current amount owed |

Learn more: How Do I Find All My Debt?

3. Subtract Your Liabilities From Your Assets

Subtract your total debts from your total assets to find your net worth.

- A positive net worth means you own more than you owe.

- A negative net worth means your liabilities are greater than your assets.

Learn more: How Do You Calculate Net Worth?

Example of Net Worth

Here's how you might calculate net worth for Madeline, a woman who owns the following assets:

- $25,000 in checking and savings accounts

- $50,000 in a 401(k) account

- Car worth $35,000, currently being financed

- Condo valued at $300,000

$25,000 + $50,000 + $35,000 + $300,000 = $410,000 in assets

Along with her $410,000 in assets, Madeline has the following liabilities, totaling $235,000:

- $10,000 in credit card debt

- $200,000 remaining mortgage balance

- $25,000 car loan

$10,000 + $200,000 + $25,000 = $235,000 in debts

Madeline's net worth is her total assets ($410,000) minus her total liabilities ($235,000), or $175,000. Madeline's $175,000 positive net worth shows that she has more assets than debt.

$410,000 ᠆ $235,000 = $175,000

Example of Negative Net Worth

On the flip side, say James has a negative net worth. His assets include:

- $200 in a bank account

- Car valued at $20,000, owned outright

- Home valued at $250,000

$200 + $20,000 + $250,000 = $270,000 in assets

James has the following debts:

- $40,000 in student loans

- $15,000 on a credit card

- $225,000 remaining mortgage balance

- $5,000 on a personal loan

$30,000 + $10,000 + $200,000 + $2,000 = $285,000 in debts

So, James has a negative net worth of $15,000. If he were to cash in all his assets, he still would not have enough to pay for all his outstanding debts.

$270,000 ᠆ $285,000 = -$15,000

How to Increase Your Net Worth

You can improve your net worth by saving money, increasing assets and paying off debt. Here are seven tips to help you move in the right direction.

1. Track Your Net Worth

Start by calculating your net worth and tracking it over time. Whether you choose to check it yearly, quarterly, monthly or even weekly, you'll see your progress toward saving money and accumulating wealth. You may also uncover rising debt or a decline in the value of your home or investments.

2. Find More Ways to Save

Saving money increases your assets and may help you avoid (or at least minimize) debt when confronted with a large expense.

- Work on a budget. If you haven't already created a plan for managing your income and expenses, start now.

- Reduce your expenses. That includes the money you pay to make and manage your money: investment fees, credit card interest, bank charges and so on.

- Build an emergency fund. Having cash on hand will help you avoid using your credit cards to cover unexpected expenses.

Earn Money Faster

Compare high-yield savings accounts

Find a high-yield savings account with today’s APY. Compare current APY and offers to find the best savings account for you.

3. Pay Down Debt

Paying off high-interest credit card debt can reduce your liabilities and save you money in interest charges. Also, don't overlook the opportunity to pay down other types of debt:

- Make a bigger mortgage payment every month

- Pay off your car loan faster

- Accelerate student loan repayment

4. Grow Your Retirement

Set goals for funding your retirement and stick to them. Contributing to your employer's 401(k) plan and opening an individual retirement account (IRA) are two good places to start. Investing in a tax-advantaged retirement account may also save you money on taxes, which can help you stash away even more money or avoid additional debt.

Learn more: Ways to Save More for Retirement

5. Build Home Equity

Home equity is the market value of your home minus your mortgage. When you get a new home, your mortgage adds a significant amount of debt to your portfolio. As you pay your mortgage off and your home's value appreciates, however, your home equity grows. You can help the process along by making extra mortgage payments or improving your home's value with a renovation or addition.

Learn more: How to Pay Off Your Mortgage Early

6. Increase Your Income

While raising your income won't automatically increase your net worth, more income gives you more money to save and invest. Consider taking on outside work or looking for passive income opportunities. Also, take a closer look at your savings account: You may be able to boost interest income by choosing a high-yield savings account.

7. Invest

Grow your assets by investing in stocks, bonds, mutual funds and other investments. A higher rate of return helps you increase your assets and, in turn, your net worth. If you're not sure how to invest, consider working with an investment advisor. Or, look for a brokerage that offers investment advice or robo-advisors at a low cost.

Learn more: How to Start Investing

What Is the Average Net Worth by Age?

The median family net worth for all age groups is $192,900, according to the Federal Reserve's 2023 Survey of Consumer Finances (SCF). Generally speaking, net worth tends to rise with age as savings accumulate and assets appreciate in value. The following table shows median household net worth based on most recent Federal Reserve data, collected in 2022.

| Age | Median Net Worth |

|---|---|

| 34 and younger | $39,000 |

| 35-44 | $135,600 |

| 45-54 | $247,200 |

| 55-64 | $364,500 |

| 65-74 | $409,900 |

| 75 and older | $335,600 |

Source: Federal Reserve, 2023 Survey of Consumer Finances

Frequently Asked Questions

The Bottom Line

Measuring your net worth can help you gauge how the assets you're accumulating stack up against the debts you carry—and how your finances are (or aren't) progressing toward long-term goals. Ideally, a lifetime of good habits like saving, investing and paying off debt will lead to higher and higher net worth.

Along the way, keep an eye on your net worth to help you identify potential problems and course-correct if necessary. Together with strategies for budgeting, investing, career development and monitoring credit, tracking your net worth helps you evaluate—and hopefully celebrate—your financial progress.

What makes a good FICO® Score?

Learn what it takes to achieve a good credit score. Review your FICO® Score for free and see what’s helping and hurting your score.

Get your FICO® ScoreNo credit card required

About the author

Gayle Sato

Gayle Sato writes about financial services and personal financial wellness, with a special focus on how digital transformation is changing our relationship with money. As a business and health writer for more than two decades, she has covered the shift from traditional money management to a world of instant, invisible payments and on-the-fly mobile security apps.

Read more from Gayle