How Do Lenders View Your Credit?

Credit checks are common when you apply for loans or credit cards, but you may wonder what a credit check actually reveals about you. When lenders run credit checks, they're trying to assess what kind of borrower you'll be, and going over your credit score and report can help them understand how you've historically managed credit. Late payments, maxed-out credit cards and accounts in collections may paint you as an unreliable borrower. On the other hand, having a long track record of timely payments, low credit balances and paid-off accounts tends to work in your favor.

Here's how your credit report, credit score and other credit application information help lenders decide whether to lend to you.

What Lenders Look at on Your Credit Report

Your credit report provides a detailed record of how you manage credit. For lenders who are just getting to know you, a credit report tells a lot about your experience with various kinds of credit. The best way to visualize what your credit report says is to check it yourself. You can access your credit report for free from all three credit bureaus at AnnualCreditReport.com or get a free Experian credit report anytime. You can also read up on what a typical Experian credit report contains. A few highlights:

- Personal information, including any names associated with your credit, current and past addresses and date of birth

- Current and past employers that have been listed on past credit applications

- Open loans and revolving credit accounts with credit limits, dates of late payments and current status

- Collection accounts, both open and resolved

- Bankruptcies, which are the only public record listed on your credit report

- Credit inquiries, including those from prospective lenders and credit card issuers

Lenders don't necessarily expect to see a flawless credit report. But a history of late payments, accounts in collections or a flurry of recent credit inquiries can raise red flags, lower credit scores, and may disqualify you from getting the best rates and terms or from being approved at all.

What Is Considered a Good Credit Score?

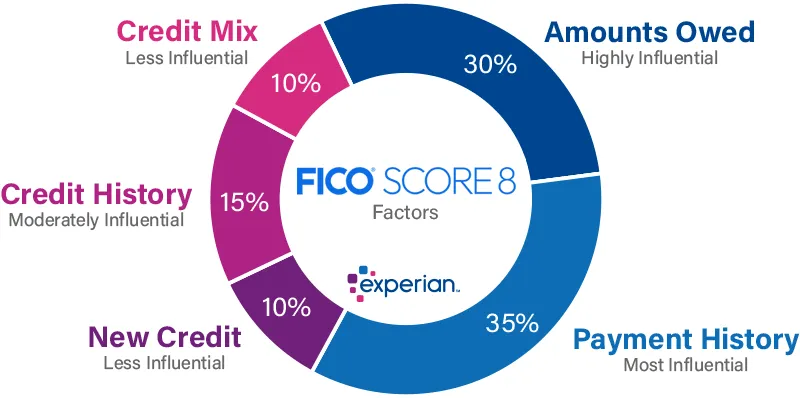

Your credit report provides a detailed credit history, while your credit score gives a quick read on how well you manage credit. Using data from your credit report, credit scoring models create numerical scores ranging from 300 to 850. The exact algorithms used to calculate these scores are not public knowledge, but the factors that affect your credit score are widely known. FICO, whose scores are used in most consumer lending decisions, breaks down the factors as follows:

- Payment history: Paying on time every time creates a solid base for your credit score.

- Amounts owed: The less of your available revolving credit you're using, the better. Progress on paying off loans is also considered in this factor.

- Length of credit history: Having long-standing accounts shows stability.

- Credit mix: A diverse mix of revolving credit cards and installment loans shows you can manage multiple types of credit.

- New credit: While opening new credit isn't bad per se, frequent credit applications can make you appear as more of a credit risk.

How does your credit score stack up? Here are FICO credit score ranges and how they might play out when you're applying for credit:

| How Your FICO® ScoresΘ Stack Up With Lenders | |

|---|---|

| 800 - 850

Exceptional |

|

| 740 - 799

Very good |

|

| 670 - 739

Good |

|

| 580 - 669

Fair |

|

| 300 - 579

Poor |

|

Although scores of 670 and above are considered "good," when you're applying for credit, there's no one credit score that's universally considered "good enough" for all lenders and all types of credit. For instance, the score you'll need to qualify for a benefits-rich rewards card with a hefty credit line is going to be significantly higher than what you'll need to get a more basic credit card. With a higher credit score, you'll often be able to access better rates and terms. If your score is less than stellar, however, your options are to accept the rates and terms you qualify for now, or wait and try to raise your score significantly.

How to Improve Your Credit Before Applying

Before applying with a lender, start by checking your credit score and report. This will give you a better idea of what types of loans and credit cards you might qualify for. You can access your Experian FICO® Score and credit report for free at any time, or sign up for free credit monitoring with alerts that let you know when changes have been made to your credit file.

Unless your credit score is already top-tier, there's always room for improvement. And moving from "good" to "very good" credit, for example, may open the doors to lower interest rates, more favorable terms or simply a better chance of approval. Although there's no quick fix for your credit, there are steps you can take to bring your credit score up. Here are a handful of tips to consider:

- Review your credit scoring risk factors. These are shown with your Experian credit report and score, and are a great starting point when trying to bring your score up.

- Practice good credit habits. Pay every bill on time, keep your credit card balances low and don't apply for credit unnecessarily.

- Check out Experian Boost®ø. Adding on-time utility, phone and streaming service payments to your credit file with Experian Boost may help you bump up your scores.

- Give yourself time. The longer your history of making on-time payments, the more beneficial those payments will be. If you have negative marks on your credit, the passage of time will reduce the impact they have on your scores and eventually they'll be removed entirely. If you've recently paid down card balances to reduce your credit utilization, it may take a few billing cycles for your score to fully reflect that change. Bottom line: If you want to raise your credit score to improve your loan or credit card options, there's no better time to start than now.

The same advice holds if you don't have much of a credit history—or your credit file is "thin" (with fewer than five credit accounts). It may take time to build the credit score you aspire to, so start working on it now. Building good credit from scratch may take multiple steps. You may want to begin with a secured credit card or consider a credit-builder loan. Over time, as long as you manage your credit responsibly and continue to make all payments on time, your positive credit history will populate your credit report and help build up your score. Make sure your lender reports your payment activity to all three credit bureaus.

Instantly raise your credit scoresø

Add any bank accounts you use to pay your bills. Your information remains private.

We’ll detect bills with on-time payments, and you can add them to your Experian credit file.

You’ll find out right away if your credit scores increased and by how many points.

What Else Do Lenders Look at in Your Credit Application?

Together, your credit score and report provide quite a bit of insight into how you manage credit. But most lenders also want to know more about you and your finances. This information is not included in your credit report, and they'll typically ask you to provide this information yourself or provide documentation to back it up.

Income: Lenders want to know about your employment and monthly income so they know you can afford to pay back your debt. They'll also use this information to calculate your debt-to-income ratio to make sure your total debts aren't eating up too much of your monthly income.

Capital: Lenders want to know that you'll be able to make your payments even if you run into a bit of financial trouble. Having emergency savings or an investment account shows you have the financial backup to carry on through choppy waters.

Collateral: Two common examples of collateralized—or secured—loans are mortgages and car loans. If you default on either of these types of loans, the lender will seize your property and sell it to recoup their money. Credit cards are generally unsecured, though applicants who are building credit may consider secured credit cards, which require you provide a cash deposit equal to your credit line as collateral. If your collateral is property, you'll likely need to prove its value and that you own it.

Lenders may also look at factors that don't seem to relate directly to credit. For example, if you've been at your job for many years or have lived in the same place for a long time, that's seen as a sign of stability.

Put Your Best Foot Forward

Securing credit often involves a lot of scrutiny. For lenders, though, checking your credit isn't about being invasive or judgmental: They just want to reduce their financial risk by verifying that your credit history and finances match up with requirements for the loan or credit card they're offering. Understanding what lenders are looking for, then checking your credit score and credit report and looking for ways to put your best foot forward can help you secure the loan you want—and maybe help you breathe a little easier during the approval process.

What’s on your credit report?

Stay up to date with your latest credit information—and get your FICO® Score for free.

Get your free reportNo credit card required

About the author

Gayle Sato

Gayle Sato writes about financial services and personal financial wellness, with a special focus on how digital transformation is changing our relationship with money. As a business and health writer for more than two decades, she has covered the shift from traditional money management to a world of instant, invisible payments and on-the-fly mobile security apps.

Read more from Gayle