What Is a Credit Card CVV Number?

Quick Answer

A CVV is a three- or four-digit code printed on your credit card that helps verify you have the physical card when you make online or phone purchases, adding a layer of protection against fraud.

When you buy something online or over the phone, you're often asked to enter a short security code along with your card number and expiration date. That code is your CVV, and it plays a key role in protecting you from fraud. Here's what the CVV on your credit card does, where to find it and how to keep it safe.

What Is a CVV on a Credit Card?

A CVV is a three- or four-digit security code printed on your credit card that helps verify you have the physical card in your possession. CVV stands for card verification value, and it's designed to add a layer of protection against fraud when your card isn't physically present at checkout.

Different card networks use different names for this code, but they all serve the same purpose. Depending on the type of card you have, it may also be referred to as a CVV2, CVC2, card security code (CSC) or card identification number (CID). Regardless of the name, merchants use it to confirm a purchase is likely being made by the legitimate cardholder.

Learn more: Pros and Cons of Virtual Credit Cards

Where to Find Your CVV

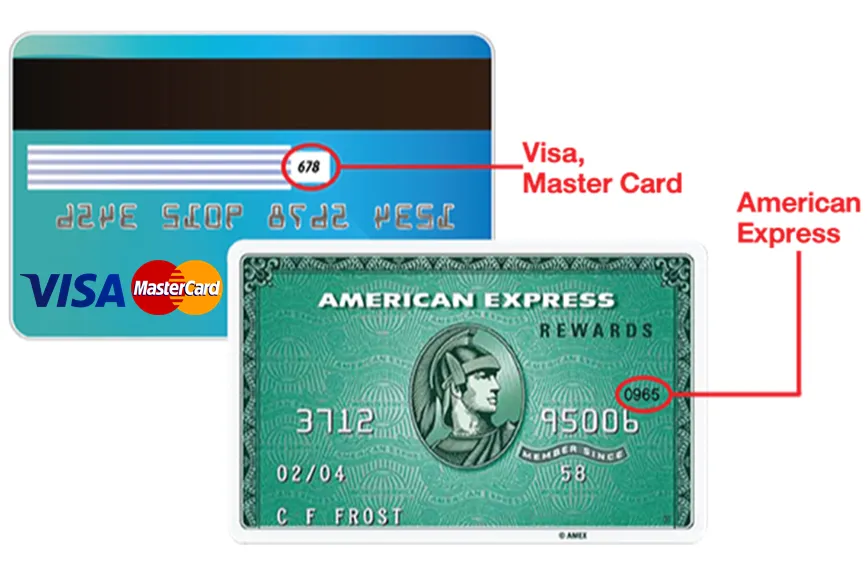

The location of your CVV depends on which card network issued your card. For Visa, Mastercard and Discover, the three-digit code is printed on the back of the card, typically to the right of where the signature panel is or was.

For American Express cards, the four-digit CID is printed on the front of the card, above and to the right of the card number.

What's the Purpose of a CVV?

The main purpose of a CVV is to prove you have the physical card during transactions where a merchant can't see or swipe it. These are known as card-not-present transactions, and they're one of the most common targets for fraud.

You'll typically be asked to enter your CVV in the following situations:

- Online purchases: Most e-commerce sites require a CVV at checkout, especially for first-time purchases.

- Phone orders: A customer service rep will often ask for your CVV when you place an order by phone.

- Adding a card to an app or digital wallet: Services like Apple Pay, PayPal and subscription apps often request a CVV when you first link a card.

- Some recurring billing setups: You may be asked for your CVV during the initial setup, though merchants can't store it for future charges.

You generally won't need your CVV for in-person transactions. When you tap, insert or swipe your card at a payment terminal, the terminal reads the chip or magnetic stripe to verify the card, so the CVV isn't required.

How Your CVV Protects You From Identity Theft

CVVs add an extra layer of defense against identity theft and unauthorized transactions. Under the Payment Card Industry Data Security Standard (PCI DSS), merchants and service providers are prohibited from storing your CVV after a transaction is authorized, even if you give them permission.

So even if a thief hacks into a merchant's database and steals stored card numbers and expiration dates, they shouldn't walk away with your CVV. Without it, many online and phone merchants will reject a transaction, which limits what a thief can do with the stolen information.

That said, the CVV isn't a silver bullet. Thieves can still get your full card information through the following:

- Phishing scams: Fraudsters may send fake emails or texts that trick you into entering your full card details on a spoofed website.

- Malware: Malicious software on a merchant's systems or your own device can capture card data, including the CVV, as you enter it.

- Physical theft: If someone steals your actual card, they have the CVV printed right on it.

Best credit cards of 2026

Compare cards from our partners with intro bonuses, cash back or points offers, and annual fees as low as $0.

Offers from our partners

Citi Double Cash® Card

Intro APR:0% for 18 months on Balance Transfers

Ongoing APR:17.49% - 27.49% (Variable)

Rewards:2% (cash back)

Annual Fee:$0

Revel® Platinum Mastercard®

Ongoing APR:35.90% Fixed

Rewards:N/A*

Annual Fee:$75 - $125

Citi® Diamond Preferred® Card

Intro APR:0% for 21 months on Balance Transfers and 12 months on Purchases

Ongoing APR:16.49% - 27.24% (Variable)

Rewards:N/A*

Annual Fee:$0

Wells Fargo Active Cash® Card

Intro bonus:$200

Intro APR:0% intro APR for 12 months from account opening on purchases and qualifying balance transfers

Ongoing APR:18.49%, 24.49%, or 28.49% Variable APR

Rewards:2% (Cash Rewards)

Annual Fee:$0

Avant® Cashback Rewards Mastercard®

Ongoing APR:29.99%*

Rewards:2% (cash back)

Annual Fee:$0*

The opensky® Secured Visa® Credit Card

Ongoing APR:23.89% Variable

Rewards:10% (cash back)

Annual Fee:$35

Credit One Bank® American Express® for Rebuilding Credit

Ongoing APR:29.74% Variable

Rewards:1% (cash back)

Annual Fee:$75 First year. $99 thereafter, billed monthly at $8.25

Reflex® Platinum Mastercard®

Ongoing APR:35.90% Fixed

Rewards:N/A*

Annual Fee:$75 - $125

Citi Strata Premier® Card

Intro bonus:60,000 Points

Ongoing APR:19.49% - 27.49% (Variable)

Rewards:1x - 10x (Points per dollar)

Annual Fee:$95

First Latitude Secured Mastercard® Cash Back Rewards

Ongoing APR:27.49% Variable

Rewards:1% - 10% (cash back)

Annual Fee:$0

Citi® / AAdvantage® Platinum Select® World Elite Mastercard®

Ongoing APR:19.49% - 29.49% (Variable)

Rewards:2x (Miles per dollar)

Annual Fee:$99, waived for first 12 months

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$75*

Citi® / AAdvantage® Globe™ Mastercard®

Ongoing APR:19.49% - 29.49% (Variable)

Rewards:1x - 6x (Miles per dollar)

Annual Fee:$350

AT&T Points Plus® Card from Citi

Intro bonus:$200

Ongoing APR:19.49% - 27.49% (Variable)

Rewards:1x - 3x (Points per dollar)

Annual Fee:$0

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$75 first year; then $99/year

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$39*

First Progress Select Secured Mastercard® Cash Back Rewards

Ongoing APR:17.49% Variable

Rewards:1% - 10% (cash back)

Annual Fee:$39

Credit One Bank® Platinum Rewards Visa® Card

Ongoing APR:29.74% Variable

Rewards:1% (cash back)

Annual Fee:$39

Delta SkyMiles® Gold American Express Card

Intro bonus:As High As 80,000 Bonus Miles. Find Out Your Offer.

Ongoing APR:19.49%-28.49% Variable

Rewards:1x - 2x (Miles per dollar)

Annual Fee:$0 introductory annual fee for the first year, then $150.

Credit One Bank® Premier American Express® Unlimited Rewards Card

Ongoing APR:29.74% Variable

Rewards:1% (cash back)

Annual Fee:$0

Hilton Honors American Express Surpass® Card

Intro bonus:130,000 Points

Ongoing APR:19.49%-28.49% Variable

Rewards:3x - 12x (Points per dollar)

Annual Fee:$0 introductory annual fee, then $150.

Marriott Bonvoy Bevy® American Express® Card

Intro bonus:85,000 Points

Ongoing APR:19.49%-28.49% Variable

Rewards:2x - 6x (Points per dollar)

Annual Fee:$250

PREMIER Bankcard® Mastercard® Credit Card

Ongoing APR:See Rates & Fees

Rewards:N/A*

Annual Fee:See Rates & Fees

Credit One Bank® Platinum X5 Visa Signature® Card

Ongoing APR:29.74% Variable

Rewards:1% - 5% (cash back)

Annual Fee:$95

Citi Simplicity® Card

Intro APR:0% intro APR for 18 months from account opening on purchases and qualifying balance transfers

Ongoing APR:17.49% - 28.24% (Variable)

Rewards:N/A*

Annual Fee:$0

Avant® Cashback Rewards Mastercard® - $500 Credit Limit

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$125 first year; then $125.04/year ($10.42/mo)

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$0*

Avant® Cashback Rewards Mastercard®

Ongoing APR:35.99%*

Rewards:1% (cash back)

Annual Fee:$75*

Bank of America® Customized Cash Rewards credit card

Intro bonus:$200

Intro APR:0% Intro APR on purchases and qualifying balance transfers for 15 billing cycles

Ongoing APR:17.49% - 27.49% Variable

Rewards:1% - 6% (cash back)

Annual Fee:$0

Bank of America® Unlimited Cash Rewards credit card

Intro bonus:$200

Intro APR:0% Intro APR on purchases and qualifying balance transfers for 15 billing cycles

Ongoing APR:17.49% - 27.49% Variable

Rewards:1.5% - 2% (cash back)

Annual Fee:$0

See all our best credit cards for 2026.

Is It Safe to Share Your CVV?

It's safe to share your CVV with a legitimate merchant during a purchase, but only then. The CVV exists to be used at checkout, so entering it on a trusted retailer's secure website or giving it to a reputable company over the phone is generally fine.

But, you should never provide it in response to an unsolicited email, text or phone call, even if the sender claims to be from your bank or a company you use. This is also true for websites you land on by clicking a link in a suspicious message or anyone offering to "verify" your account or confirm a suspicious charge.

Be aware: Your card issuer will never call or email you out of the blue and ask for your CVV. If someone does, assume it's a scam.

Learn more: The Latest Scams You Need to Be Aware Of

Tips to Keep Your Credit Card Information Safe

A CVV is just one layer of protection. The following habits can help keep your full card information out of the wrong hands:

- Shop on secure sites. Look for "https" and a padlock icon in the address bar before entering card details. Avoid entering card information over public Wi-Fi without a virtual private network.

- Use digital wallets when possible. Services like Apple Pay and Google Pay use tokenization, which replaces your card number with a unique code for each transaction.

- Set up transaction alerts. Most issuers let you get a text or push notification for every purchase, which helps you spot fraud quickly.

- Avoid saving cards on unfamiliar sites. The fewer places your card is stored, the smaller your exposure if a retailer is breached.

- Watch out for skimmers. Inspect card readers at gas pumps and ATMs for loose parts or unusual attachments before inserting your card. Card skimmers can pull your card information.

- Keep your card in view at restaurants. Alternatively, you can pay with a contactless method so your card never leaves your hand.

- Monitor your accounts. Check your credit card and bank statements often for charges you don't recognize.

Tip: Many card issuers offer a virtual card number feature, which lets you generate a temporary card number and CVV for online shopping. If the number is stolen, the thief can't use it elsewhere or for long.

Frequently Asked Questions

The Bottom Line

A CVV is a simple but effective tool that helps keep your credit card secure during online and phone purchases. Still, no single security feature can stop every threat, so it's smart to back it up with good habits like monitoring your accounts, avoiding suspicious links and shopping only on trusted sites.

You can also keep a closer eye on your personal and financial information with free credit monitoring from Experian. You'll get alerts about key changes to your Experian credit report, so you can act quickly if something looks off.

Don’t apply blindly

Apply for credit cards confidently with personalized offers based on your credit profile. Get started with your FICO® Score for free.

See your offersAbout the author

Ben Luthi

Ben Luthi has worked in financial planning, banking and auto finance, and writes about all aspects of money. His work has appeared in Time, Success, USA Today, Credit Karma, NerdWallet, Wirecutter and more.

Read more from Ben