Welcome to the Experian Thought Leadership Hub

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

44 resultsPage 1

Infographic

Infographic

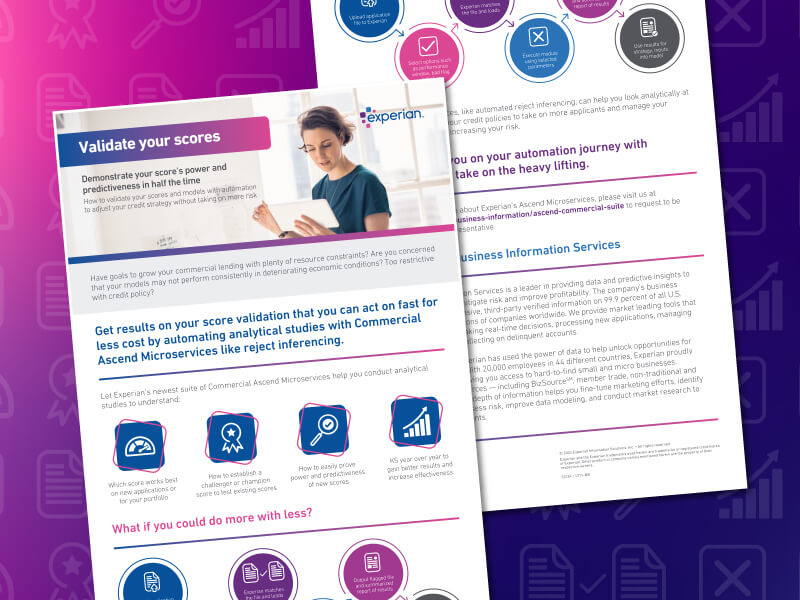

A concise guide to simplifying business credit modeling with automation. Learn how microservices streamline validation, testing, and analysis to help relationship managers, credit analysts, and adjudicators reduce manual effort, improve risk visibility, and make faster, more confident lending decisions.

Infographic

Infographic

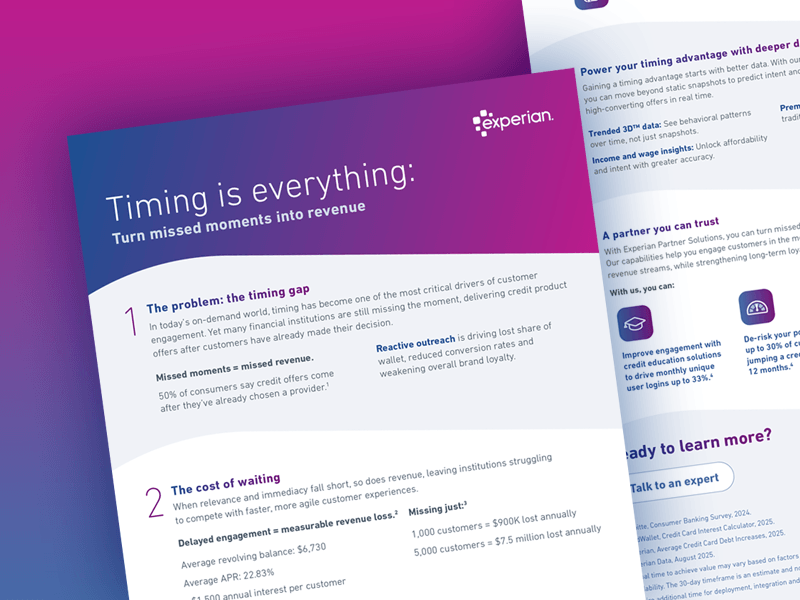

View our infographic to learn how to capture high-intent moments and turn them into lasting revenue. Discover:

Infographic

Infographic

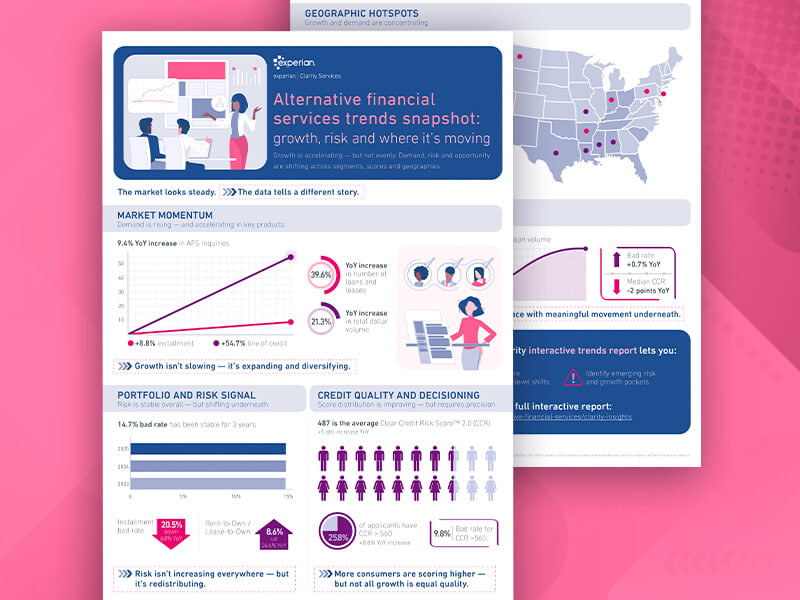

Download the latest Alternative Financial Services Trend Report to reveal new insights on growth and risk, including:

Infographic

Infographic

Discover a faster, more efficient way to bring financial wellness and privacy solutions to market. Learn how to:

Infographic

Infographic

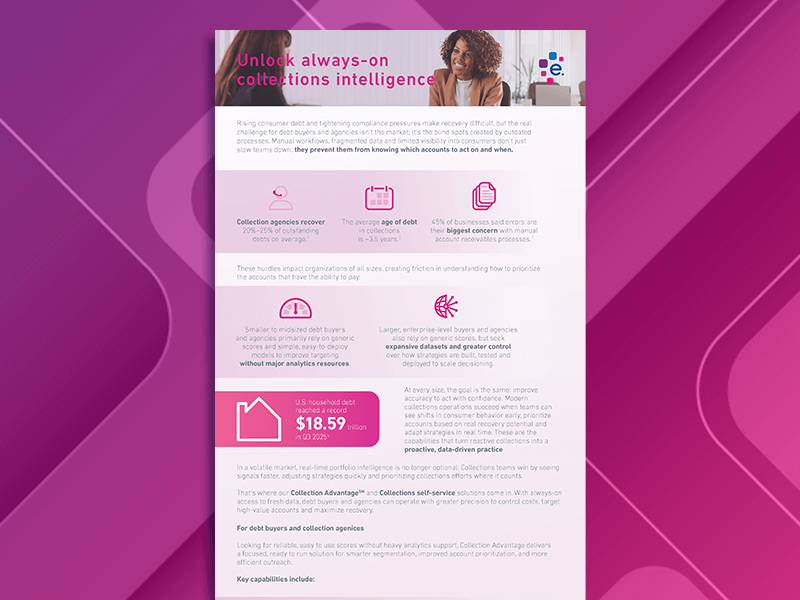

Recoveries hinge on knowing who can pay, not just who owes. This infographic explores how debt buyers and collections agencies can better identify signals of true payment capacity.

Did you know?

Read the infographic for more insights and strategies to drive smarter recoveries.

1Household Debt and Credit report, Q3 2025, Federal Reserve Bank of New York.

2Debt Collection Industry Statistics, zipdo.

3Collections Industry Statistics, Gitnux.

Infographic

Infographic

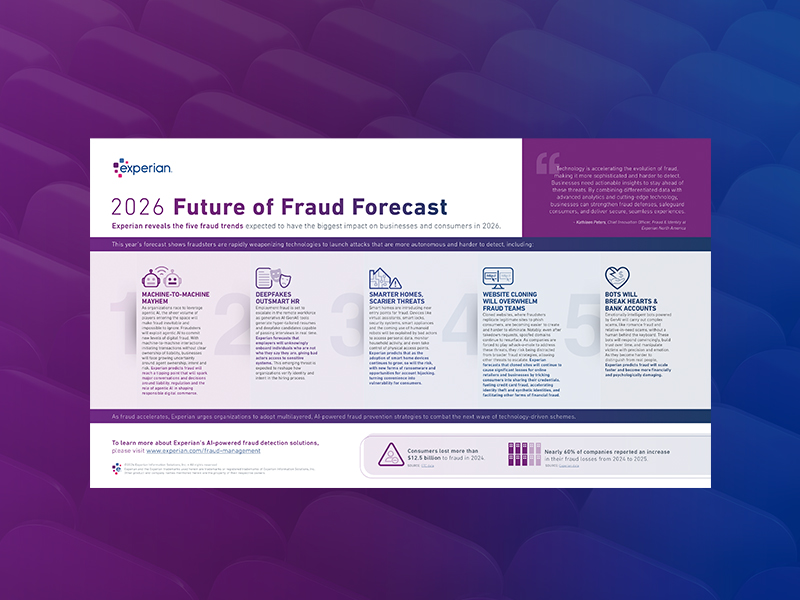

Download Experian’s 2026 Future of Fraud Forecast to explore five fraud trends expected to have the biggest impact on businesses and consumers in the coming year, including:

Infographic

Infographic

As market conditions shift, collections success depends on continuous, high-quality consumer data. This checklist highlights how always-on collections intelligence can help debt buyers and agencies:

Infographic

Infographic

Changes in consumer behavior and advancements in data and technology mean that traditional collection methods may no longer produce the best results.

Download our checklist for four key signs that your strategy needs updating and how modern solutions can help:

Infographic

Infographic

Home equity lending is shifting fast and hidden risks could be costing you.

The latest insights, tips, and trends on all things related to commercial risk by the Experian Business Information Services team.

Experian Employer Services’ HR, payroll and tax experts share news, insights and best practices for employer compliance topics and challenges.

Experian's Global News Blog is your go-to source for the latest news, insights and trends in the world of data and analytics.

Experian Health’s blog features the latest trends and insights shaping the future of healthcare.

Helping businesses make faster, smarter, and more inclusive decisions with the power of data, analytics, and technology.

Marketing insights and solutions to help you drive more meaningful interactions so your consumers can connect, engage, and thrive.

Small business advice and credit education, news, and trends.