How To Maximize Receivables as Delinquencies Rise

Sip and Solve™ 15-Minute Webinar

Sip and Solve™ 15-Minute Webinar

Webinar Overview

Managing receivables has never been more important or more challenging. Traditional approaches may no longer apply. In this 15-minute Sip and Solve session, we discuss some solutions for effectively and efficiently handling the increase in receivables many companies are facing.

After watching this talk you will learn three key takeaways:

What follows is a lightly edited transcription of this Sip and Solve talk.

[John]: Welcome to another Sip and Solve. My name's John Krickus. I'm a Senior Product Manager with Experian Business Information Services. I'm responsible for our business scores, and I work with clients to utilize our scores. I worked for nearly a decade in managing both first and third-party receivable collections. Today, we'll be walking you through how you can use analytics, scores, and data to improve collections in these challenging times. With me today is Andrew Moore.

[Andrew]: Hello, everyone. My name is Andrew Moore. I am a Senior Consultant within our Commercial Data Sciences group, and I support Experian's commercial credit accounts, and I am excited to be joining you today.

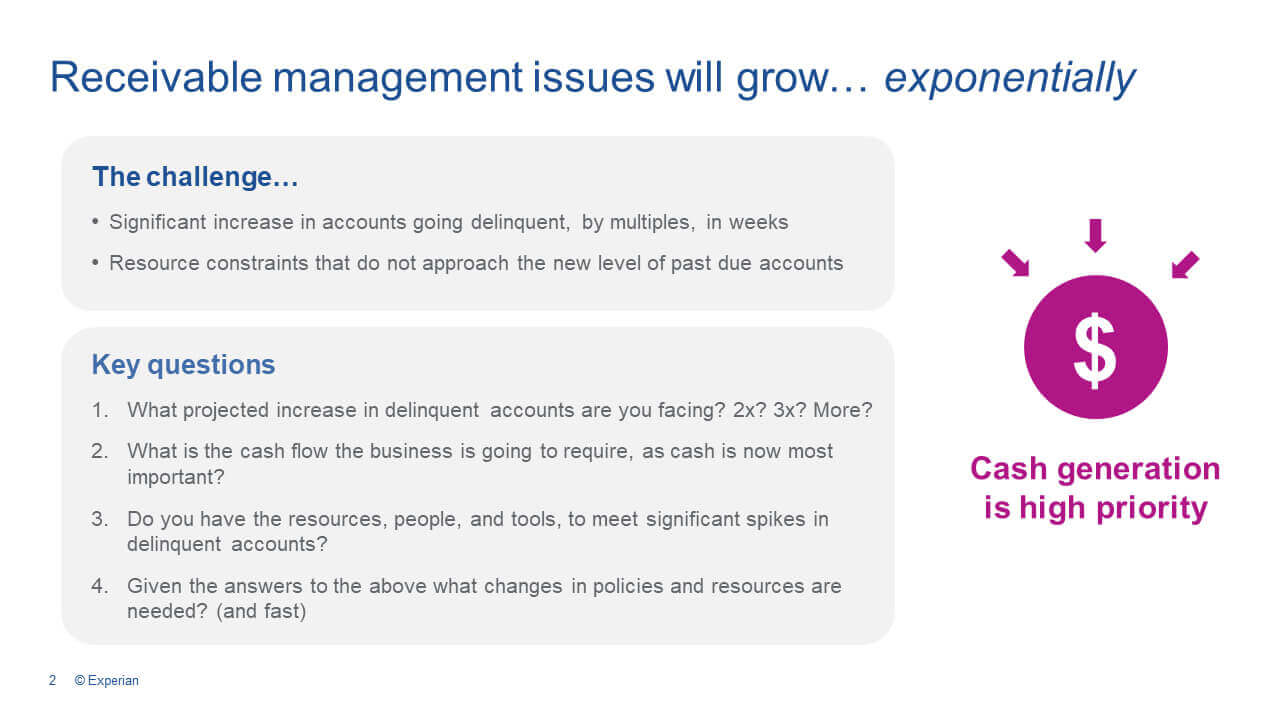

[John]: So our topic today is about how to maximize receivables in these very challenging times because, as we've seen from our clients, delinquent receivables are starting to grow, and they're starting to grow at a significant rate. And in this atmosphere, many of you probably have the same resources. You're not getting additional resources to deal with this new level of past due accounts. So we're here to talk about some ideas on how to resolve this dilemma. Some key questions as you look at the situation are what is going on with your delinquent accounts? How much are they increasing? Some businesses may not be experiencing as dire circumstances as others. So what's the cash flow needs of your business? And notably, as you match up the needs, the increase in delinquency, what type of resources do you have? And how are we going use existing resources in order to maximize our receivables and our collections?

[John]: Andrew, I know you work with clients every week. Could you touch on a couple of the events that you're seeing out there right now?

[Andrew]: Yeah, so, they go very much in line with what you just said. I think the key theme is what I was doing a year ago isn't necessarily the same thing that I should be doing today. Obviously, we know that the economic landscape has changed, and so a lot of the conversations I have is around what resources do I have at my disposal? How do I effectively and efficiently deploy those resources in the current economic environment? And then also, from a sales support standpoint, what solutions does Experian have to compliment what I'm doing today? From a frequency standpoint, I have these conversations weekly with clients.

[John]: So, as we look at this, the situation we're facing, we're going to talk about a traditional prioritization of receivable management. We'll call that the base strategy, but now we're going to want to assess that strategy, given the tough circumstances that we're all in with the economic and health crisis. So we're going to identify two areas for adjustment to help us out in this situation. And then finally, to act upon that plan. All of this is meant to maximize cash flow to maximize collections.

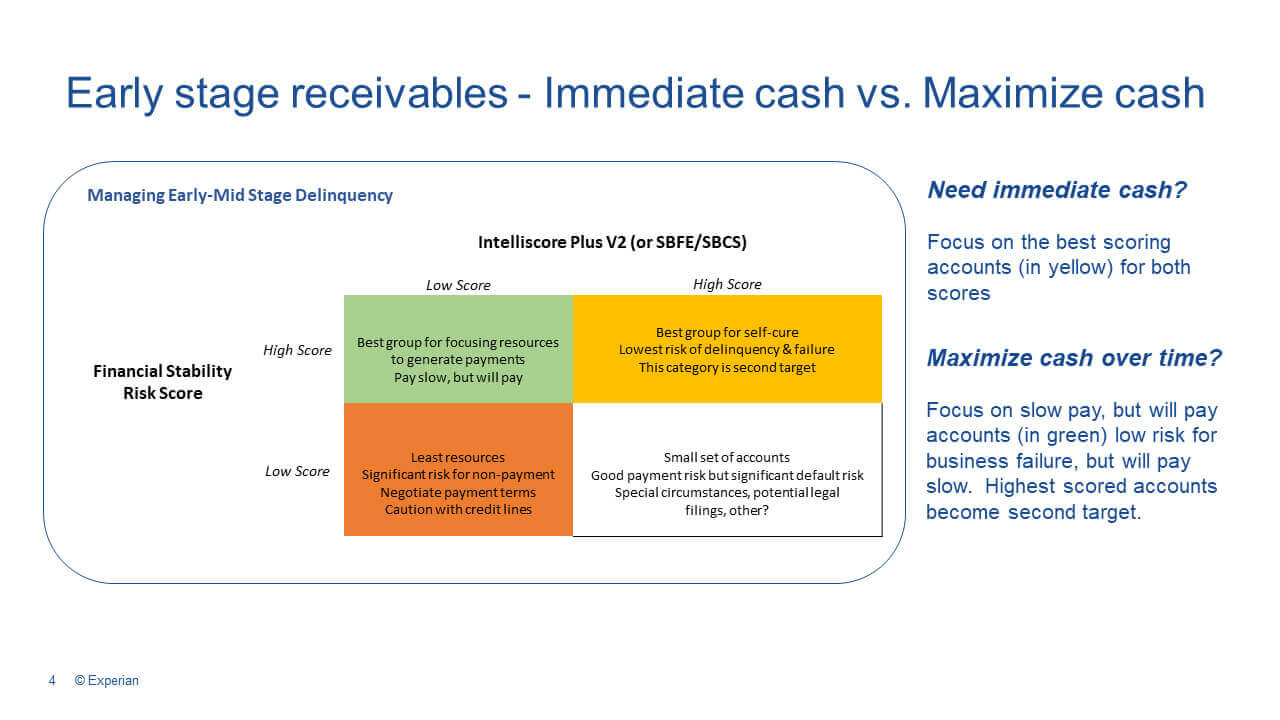

[John] Let's talk about a traditional plan, but then you see to the right, we have a question for you. Are you able to follow this traditional plan, which has meant to maximize cash over time or do you need to be cash? So what we've done here is if we were to take a look at a receivable portfolio, we would suggest using two score measures.

So now we're going to use intelligence and analytics in order to help prioritize our limited resources. Across the top, you see our credit score, Intelliscore Plus. We also have Small Business Financial Exchange (SBFE), Small Business Credit Share (SBCS). Those are consortium scores. They're all predicting delinquency. A high score means they're at low risk of delinquency. A low score means they're at a much higher risk of paying in the delinquent manner. We're going to add to that our Financial Stability Risk Score. This is a score that's predicting business failure.

Again, a low score means that there's a real high risk of that business failing compared to the high scored accounts. So when we put those grids together. We've grouped accounts into four buckets. Now, traditionally, we might focus on the green bucket. They're going to pay slow. They have a low score for Intelliscore Plus, but have a high score for their Financial Stability Risk so have a very low likelihood of failure. So if traditionally you're trying to maximize cash over time, you might focus your limited resources on accounts that are paying slow, but will pay.

If you need immediate cash, the focus may need to be on the yellow or gold group, generally the best group for self-cure. If a large part of your portfolio is with businesses in travel, entertainment and restaurants, all industries heavily affected by the current crisis, you may now need to go after the high scoring accounts in both areas. Those are the businesses that will have the best chance of producing results. So that's where, depending upon the answer to your questions that we laid out, you need that immediate cash. You're going to go after the high scores, both areas to generate collection results.

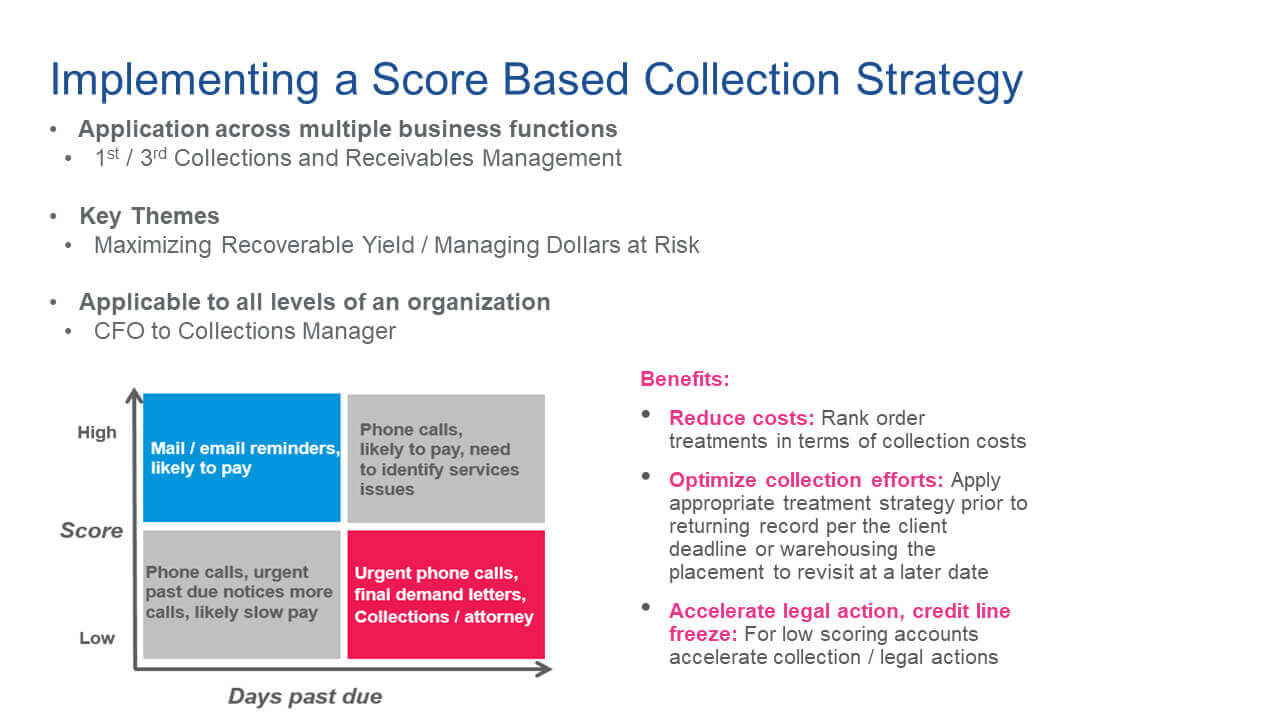

[Andrew]: When we talk about implementing a score based strategy, there are three key themes, and for this audience, I'm hoping that these three resonate because I do think the implementation of a strategy is applicable across multiple business functions. So whether you're in first-party, or third-party collections, or receivable management, I think the key themes that resonate are Maximize Recoverable Yield, or how do I get the money that is owed to me most efficiently and effectively? Then, how do I manage my dollars at risk? If I'm looking at this from a portfolio level, where does my risk lie? And then what action, what strategy do I deploy to protect those dollars? Lastly, I think it applies to all levels of the organization. From the highest level, if you're thinking about this from a P&L standpoint, or looking across your portfolio to figure out where does our risk lie? From a portfolio standpoint to a collection manager on the front lines pulling the lever allocating the resources. How do I go after the dollars that are owed to us to maximize my recoverable yield? These are three key themes. So having said that, John, do you want to touch on the benefits of implementing a strategy?

[John]: Yes, we talked earlier about the dilemma of having significantly increased workload, and in all likelihood, you have the thinning resources, and I've been there. I've worked for about a decade in receivable management, both in first-party and third-party, and the whole part of a receivable management effort. Given the huge volume of accounts you're dealing with, you want a lot of those accounts to self-cure. Well, given the situation we're in, as you assess your portfolio as to how much you have to depart from a traditional strategy, you may need to optimize your collection accounts. For example, accounts that have a low likelihood of payment or and are in a high probability of failure; you may want to accelerate out to legal action or out to credit line freezes. Or take other steps to reduce your costs in dealing with them. So you can optimize your collection efforts by focusing on the clients who can pay to generate that cash flow. That is one of the adjustments that we would need to make in this environment. And another one involves our COVID capabilities.

[Andrew]: One of the things that I think is a compliment to any score based strategy or one of the solutions that can complement a score based approach is the evaluation or the overlay of our COVID-19 risk index. Experian's COVID-19 Risk index is a combination of the geographical case load across the United States in combination with industry risk. So think Construction, that was deemed an essential function versus Restaurants and Retail. So, through this Risk Index, we can provide a severity level from high impact to low impact, which allows you to even further segment, within score bands, your portfolio, and just give you an even a deeper, granular view of your receivables management collection strategy.

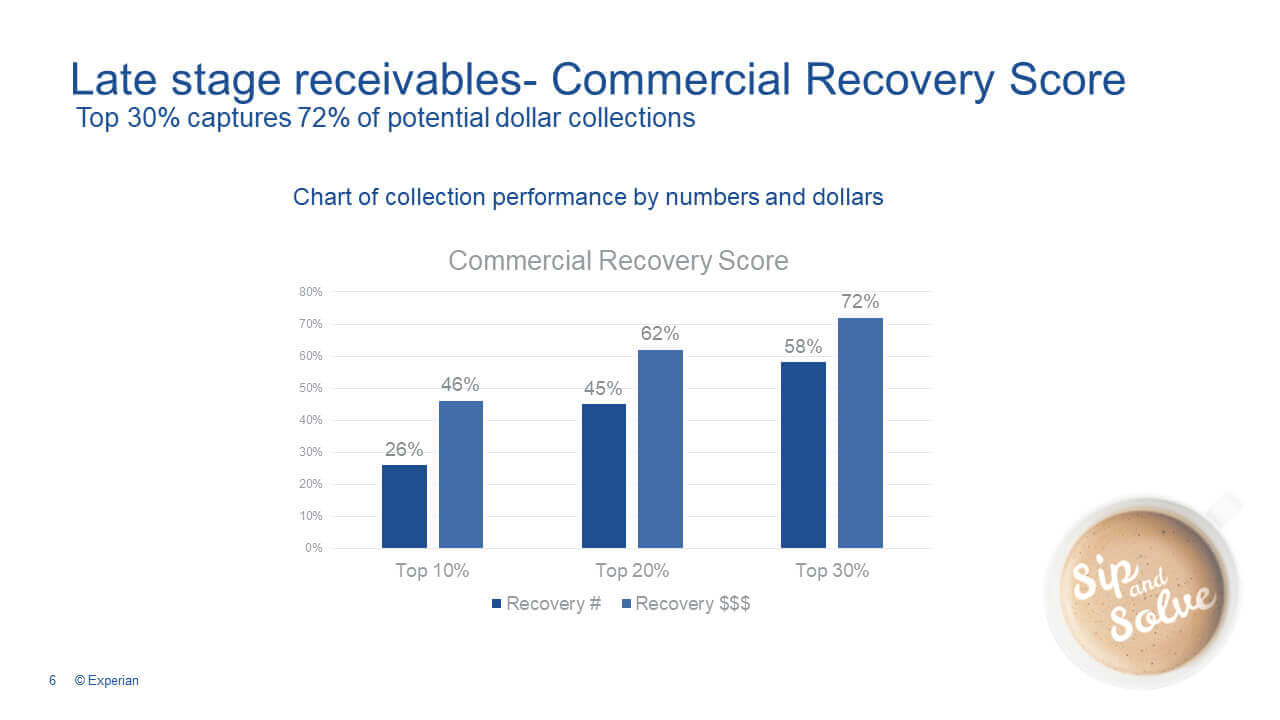

[John]: The other product that we have for these delinquent receivables is our Commercial Recovery Score. It was just launched last year, and normally with scores, we talk about the bad accounts at the bottom end of the score scale. So in the bottom 20% of scores, how many of the bads were we able to exclude? You can have an 80% approval rate and get rid of 50% of all the potential bad accounts with the commercial recovery score. We're trying to help you out with severely delinquent accounts. Here we're looking at the Good score. So the good scores as you see in this chart, these were very severely delinquent receivables. We were able to collect 72% of the potential dollars in the top 30% of scores. So at the bottom end you would really save a lot of your efforts. Andrew can you talk about what our commercial recovery score capabilities can do?

[Andrew]: In Commercial Data Sciences, I am a big supporter of the Commercial Recovery Score and the associated analytics. What you're seeing here is, a highly summarized view of output on a client portfolio. And what I like to say here is this is where we quantify the concept.

We've been talking a lot about the application of a strategy. Here's where we get into the numbers and the statistics to quantify how you apply that.

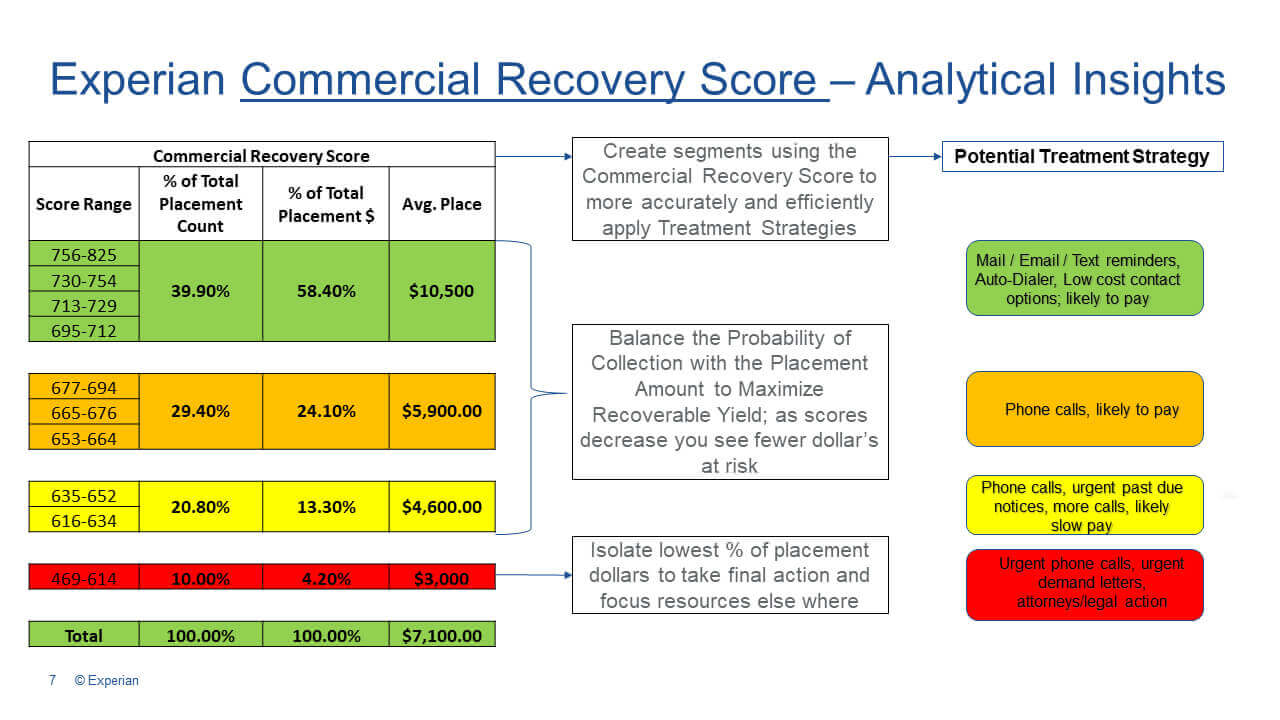

There's three key themes — utilizing a score, ie; the Commercial Recovery Score. We want to create segments that, more accurately and efficiently identify and apply treatment strategies.

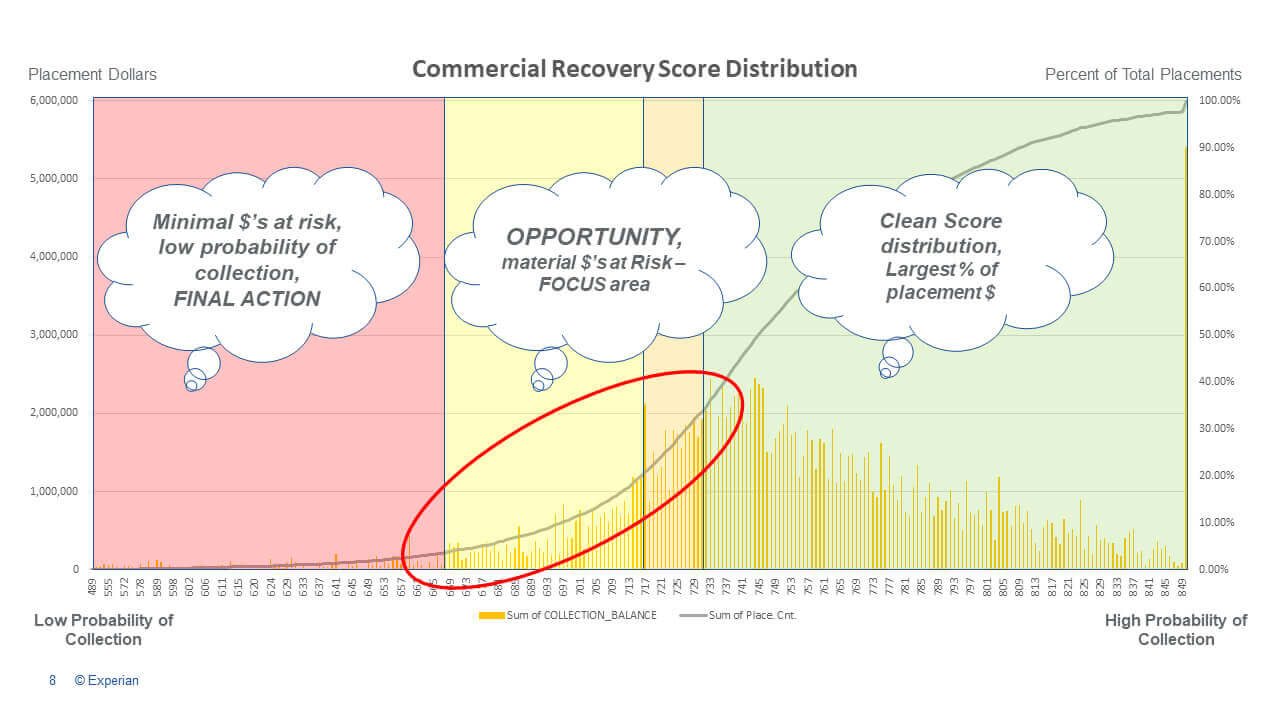

Secondly, we want to balance the probability of collection. Looking at the credit file, we want to balance the probability of collection with the placement amount to optimize the dollars that we recover. I'm going to show you a visualization about that in a moment, but to John's point, you know, 40% of my placements, I'm recovering 60% of my dollars. So we want to create that balance. And then lastly, we want to isolate the lowest percentage of placement dollars to take some final action. Because on that bottom 10%, would you be better served by focusing your resources elsewhere? Take that bottom 10%, take some final action and then focus the resources elsewhere to go after other dollars.

[Andrew]: This is one of the things I like to show. I think this is a really good slide for a number of reasons. It’s a depiction of what you saw on the previous slide, but this gives you a visualization of where your opportunity lies. So again, utilizing the Commercial Recovery Score, the whole bowl is, I like to call it, is to identify the opportunity on the margin. On the right hand side, you see a very clean distribution, the largest percent of your payments or placements, a very clean line is identified in the gray, clean score curve. Those are the commercial accounts that have a high probability of paying. That's your low-cost effort — an email, autodialer, etcetera. I think the opportunity lies on the margin in the orange and the yellow. You can still see some high scores. There are still some high dollars at risk. So take the commercial recovery score as a compliment to your other tools, identify those statistically, you can quantify the dollars, and allocate resources strategically in a score based strategy to go after them. That's where you can move the needle and advance your recoveries or or protect your receivables. That provides a very clear line of sight to implementing a strategy.

[Andrew]: Lastly, in the red section, you can see very low score range, very low dollar, or very, very low score distribution. Very low dollars as identified in the orange columns. Focus your resources there. Would you be better served by focusing your resources elsewhere to achieve optimized results? In terms of commercial data, science being able to provide something and utilization of the Commercial Recovery Score, I think this slide makes a compelling argument for utilization of a score based collection strategy or receivable management strategy.

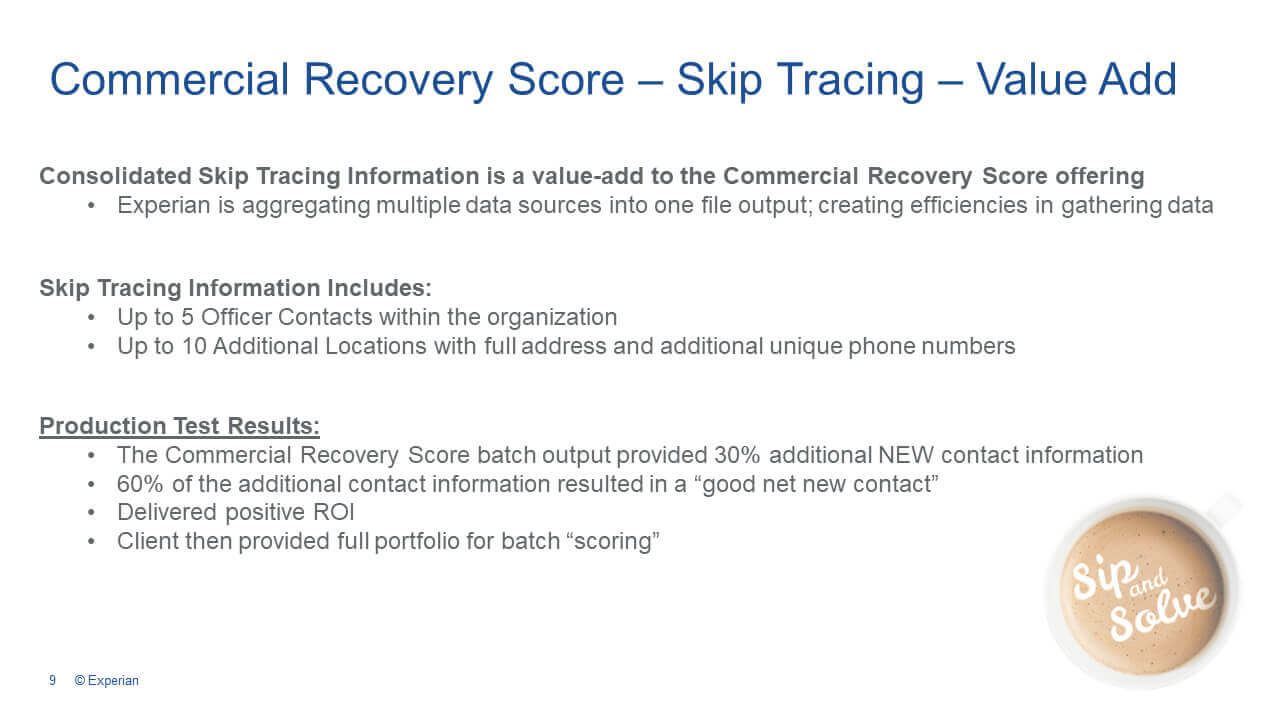

[Andrew]: The Commercial Recovery Score is much more than just a score. One additional value is the skip tracing information that Experian has been able to append to this offering. We have consolidated all of the data within Experian's robust database and providing that to you in one output. So not only are you getting scores, you're getting all the additional information that we have related to your commercial accounts. Within that we're including up to five officer contacts, as well as 10 additional location contacts with address and unique phone numbers.

So on a client validation that I performed, we provided 30% net new contact information, of which 60% of the 30% resulted in a net new contact. That in and of itself, just the robustness of the data was enough to deliver a positive ROI, which resulted in a full book of clients and doing a subsequent match. I think this creates immense efficiencies in terms of self-sourcing of your own data, from three to five different sources. Think of the Commercial Recovery Score, not only as a score, but an overarching solution to help you implement a strategy to achieve your results.

[John]: Well, that's all we have for you today. Thanks for spending your coffee break with Andrew and me. Hopefully, we gave you some ideas on how to improve your receivable management and collections. If you have any questions or want to learn more about what we talked about today, especially assistance from our decision science and analytics area. You can email us a commercialdatasciencerequests@experian.com.

Andrew Moore is an Analytical Consultant within the Commercial Data Science team at Experian. He provides strategic analytical support across all business verticals. In his role Andrew supports custom engagements for commercial acquisition models and credit risk mitigation, commercial underwriting, commercial marketing, etc.

Prior to joining Experian Andrew worked as a Sr. Consultant for Equifax for 6 years. He has experience in the automotive credit as well as consumer payments. He graduated with an MBA from Louisiana Tech University.

John Krickus is a Senior Product Manager responsible for business scoring solutions. Prior to joining Experian, John worked for Receivable Management Services, deploying scoring and other business data to increase the effectiveness of both first- and third-party collections. John started his career in finance and earned his CPA in the state of New Jersey.

We will be scheduling more Sip and Solve sessions. Sign up below to be notified.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.