Welcome to the Experian Thought Leadership Hub

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

Gain insights into the fast-changing world of consumer and business data through our extensive library of resources.

84 resultsPage 1

Report

Report

As the credit card landscape evolves, understanding how consumers and businesses are adapting has never been more important.

Our second annual State of Credit Cards Report provides a timely update on key market dynamics and dives into an often-overlooked segment within credit card portfolios: business accounts.

Key takeaways:

The Regional Economic Health Tracker examines consumer health across the four U.S. census regions. It highlights how regional dynamics, from data center growth to housing costs and credit conditions, are shaping household finances today.

White Paper

White Paper

ITIN holders are active, responsible participants in the U.S. credit economy — yet many remain overlooked by traditional lending models.

Our white paper takes a closer look at this financially active and resilient population, revealing key insights into their credit performance and long-term growth potential.

Some findings include:

Read the full white paper for more insights.

Tip Sheet

Tip Sheet

This summary outlines important research findings that help lenders drive a more inclusive environment for customers, while mitigating risk.

A few takeaways:

Report

Report

Gain actionable insights from Experian’s 2026 State of the U.S. Housing Market Report:

Report

Report

Despite tariff headwinds in 2025, the U.S. economy exceeded expectations and is positioned for continued growth. Improving credit dynamics point to a stronger lending environment in 2026.

White Paper

White Paper

Read the latest findings about "Closing the credit gap" white paper, and what they mean for financial inclusion and risk management.

Key insights:

Webinar

Webinar

As we step closer to 2026, all eyes remain on the economic outlook, the labor market and consumer health. Experian’s Chief Economist Joseph Mayans, Director of Fintech Gavin Harding and Solution Insights Director Amanda Roth, will provide a look into:

Video

Video

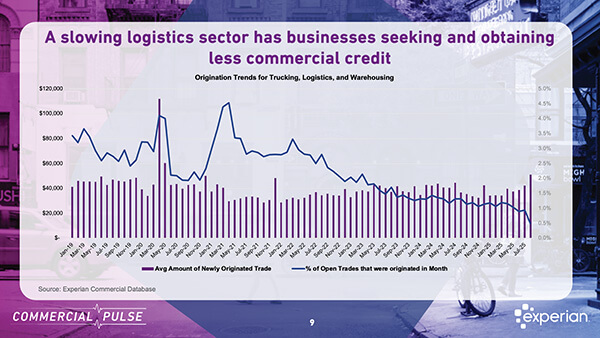

As the U.S. economy continues to recalibrate post-pandemic, the transportation and warehousing segments of the logistics sector are signaling caution. While the broader logistics industry has remained in expansion mode, Experian’s latest Commercial Pulse Report reveals that delinquencies are rising—an early warning of growing risk in two of the economy’s most critical subsectors.

Check out the full report to see how these trends could impact your strategy!

The latest insights, tips, and trends on all things related to commercial risk by the Experian Business Information Services team.

Experian Employer Services’ HR, payroll and tax experts share news, insights and best practices for employer compliance topics and challenges.

Experian's Global News Blog is your go-to source for the latest news, insights and trends in the world of data and analytics.

Experian Health’s blog features the latest trends and insights shaping the future of healthcare.

Helping businesses make faster, smarter, and more inclusive decisions with the power of data, analytics, and technology.

Marketing insights and solutions to help you drive more meaningful interactions so your consumers can connect, engage, and thrive.

Small business advice and credit education, news, and trends.