Latest Posts

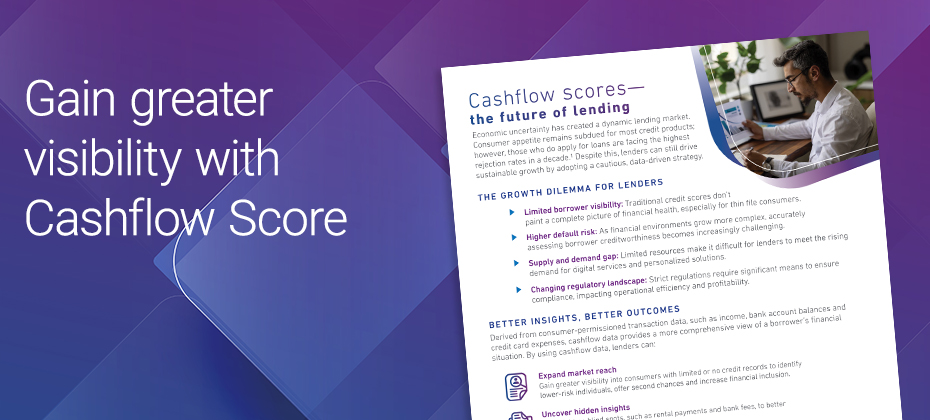

Discover how cashflow data empowers lenders to unlock new growth opportunities and manage risk more effectively.

While many industry pundits are assessing how macroeconomic changes may impact the future of the automotive market, recent data suggests consumers tend to stick to specific fuel types. According to Experian’s Automotive Market Trends Report: Q4 2024, over the last 12 months, 77.5% of electric vehicle (EV) owners replaced their EV with another one, with 15.6% returning to gas-powered vehicles. Meanwhile, 82.2% of gas vehicle owners replaced it with the same fuel type, while only 4.7% made the switch to electric. It’s important for professionals to recognize that most consumers tend to replace their vehicles with the same fuel type. Additionally, knowing who is making these purchases and the types of vehicles being registered allows better anticipation for consumer needs and ultimately enhances the buying experience while fostering consumer loyalty. Breaking down fuel types by generation Through Q4 2024, Baby Boomers predominantly registered new gasoline vehicles, accounting for 74.7% of their choices, while 15.9% opted for hybrids and 6.6% chose EVs. Millennials showed a similar trend, with 69.2% registering gas vehicles, followed by 15.1% selecting hybrids and 12.5% choosing EVs. Gen Z also favored gasoline vehicles at 74.0%, with hybrids making up 14.3% and EVs at 9.1% of their registrations. Although gasoline vehicles account for the majority of new registrations, EVs and hybrids are steadily gaining ground, particularly among the younger generations who are drawn to advanced features that align with their preferences. This will likely play a role in shaping the future of vehicle registrations as more gas alternative models hit the market and consumers make the switch. To learn more about vehicle market trends, view the full Automotive Market Trends Report: Q4 2024 presentation on demand.

While federal funding is being scaled back for community-based financial institutions, we are scaling up to support CDFIs and credit unions.

In this episode of "The Chrisman Commentary" podcast, Ken Tromer and Ted Wentzel discuss how Experian Verify ensures price transparency.

While CUVs and SUVs continue to dominate the market, sedans remain a popular choice among consumers. According to Experian’s Automotive Consumer Trends Report: Q4 2024, sedans accounted for 18.4% of new retail registrations and 36.9% of used. Comparatively, CUVs/SUVs came in at 59.3% for new and 38.6% for used. For retail sedan registrations, the Toyota Camry made up the most market share for both new and used in the last 12 months, coming in at 10.5% and 6.0%, respectively. Meanwhile, the Honda Civic came in a close second for new sedan registrations at 10.1% and the Honda Accord followed closely for used at 5.9%. Knowing which sedan models are leading in registrations is important for professionals as it helps them understand evolving consumer preferences, enhance marketing strategies, and make informed inventory decisions. Understanding the key generations fueling the sedan segment When examining generational interest in this vehicle segment, data found Gen Z and Millennials over-indexed in new retail sedan registrations. In the past 12 months, Gen Z represented 12.4% of new retail sedan registrations, while their total new retail registration was 8.2%. Millennials had 27.3% of sedan registrations out of 27% total registrations. Understanding who is purchasing and what models they’re gravitating towards can unlock valuable insights as professionals craft their next move and position themselves one step ahead in a competitive market. To learn more about sedan insights, view the full Automotive Consumer Trends Report: Q4 2024 presentation.

Fake IDs have been around for decades, but today’s fraudsters aren’t just printing counterfeit driver’s licenses — they’re using artificial intelligence (AI) to create synthetic identities. These AI fake IDs bypass traditional security checks, making it harder for businesses to distinguish real customers from fraudsters. To stay ahead, organizations need to rethink their fraud prevention solutions and invest in advanced tools to stop bad actors before they gain access. The growing threat of AI Fake IDs AI-generated IDs aren’t just a problem for bars and nightclubs; they’re a serious risk across industries. Fraudsters use AI to generate high-quality fake government-issued IDs, complete with real-looking holograms and barcodes. These fake IDs can be used to commit financial fraud, apply for loans or even launder money. Emerging services like OnlyFake are making AI-generated fake IDs accessible. For $15, users can generate realistic government-issued IDs that can bypass identity verification checks, including Know Your Customer (KYC) processes on major cryptocurrency exchanges.1 Who’s at risk? AI-driven identity fraud is a growing problem for: Financial services – Fraudsters use AI-generated IDs to open bank accounts, apply for loans and commit credit card fraud. Without strong identity verification and fraud detection, banks may unknowingly approve fraudulent applications. E-commerce and retail – Fake accounts enable fraudsters to make unauthorized purchases, exploit return policies and commit chargeback fraud. Businesses relying on outdated identity verification methods are especially vulnerable. Healthcare and insurance – Fraudsters use fake identities to access medical services, prescription drugs or insurance benefits, creating both financial and compliance risks. The rise of synthetic ID fraud Fraudsters don’t just stop at creating fake IDs — they take it a step further by combining real and fake information to create entirely new identities. This is known as synthetic ID fraud, a rapidly growing threat in the digital economy. Unlike traditional identity theft, where a criminal steals an existing person’s information, synthetic identity fraud involves fabricating an identity that has no real-world counterpart. This makes detection more difficult, as there’s no individual to report fraudulent activity. Without strong synthetic fraud detection measures in place, businesses may unknowingly approve loans, credit cards or accounts for these fake identities. The deepfake threat AI-powered fraud isn’t limited to generating fake physical IDs. Fraudsters are also using deepfake technology to impersonate real people. With advanced AI, they can create hyper-realistic photos, videos and voice recordings to bypass facial recognition and biometric verification. For businesses relying on ID document scans and video verification, this can be a serious problem. Fraudsters can: Use AI-generated faces to create entirely fake identities that appear legitimate Manipulate real customer videos to pass live identity checks Clone voices to trick call centers and voice authentication systems As deepfake technology improves, businesses need fraud prevention solutions that go beyond traditional ID verification. AI-powered synthetic fraud detection can analyze biometric inconsistencies, detect signs of image manipulation and flag suspicious behavior. How businesses can combat AI fake ID fraud Stopping AI-powered fraud requires more than just traditional ID checks. Businesses need to upgrade their fraud defenses with identity solutions that use multidimensional data, advanced analytics and machine learning to verify identities in real time. Here’s how: Leverage AI-powered fraud detection – The same AI capabilities that fraudsters use can also be used against them. Identity verification systems powered by machine learning can detect anomalies in ID documents, biometrics and user behavior. Implement robust KYC solutions – KYC protocols help businesses verify customer identities more accurately. Enhanced KYC solutions use multi-layered authentication methods to detect fraudulent applications before they’re approved. Adopt real-time fraud prevention solutions – Businesses should invest in fraud prevention solutions that analyze transaction patterns and device intelligence to flag suspicious activity. Strengthen synthetic identity fraud detection – Detecting synthetic identities requires a combination of behavioral analytics, document verification and cross-industry data matching. Advanced synthetic fraud detection tools can help businesses identify and block synthetic identities. Stay ahead of AI fraudsters AI-generated fake IDs and synthetic identities are evolving, but businesses don’t have to be caught off guard. By investing in identity solutions that leverage AI-driven fraud detection, businesses can protect themselves from costly fraud schemes while ensuring a seamless experience for legitimate customers. At Experian, we combine cutting-edge fraud prevention, KYC and authentication solutions to help businesses detect and prevent AI-generated fake ID and synthetic ID fraud before they cause damage. Our advanced analytics, machine learning models and real-time data insights provide the intelligence businesses need to outsmart fraudsters. Learn more *This article includes content created by an AI language model and is intended to provide general information. 1 https://www.404media.co/inside-the-underground-site-where-ai-neural-networks-churns-out-fake-ids-onlyfake/

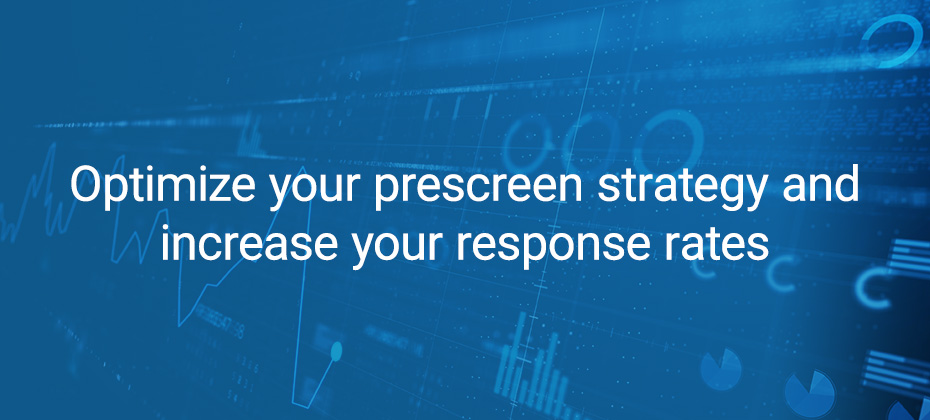

Ascend Intelligence Services™ Target leverages custom response models and optimized prescreen strategies to enhance response rates.

The electric vehicle (EV) market continues to see remarkable growth as both new and used registrations rise year-over-year. For the first time, new EVs accounted for 9.2% of all retail vehicle registrations across the U.S. in 2024, according to Experian’s 2024 EV Year in Review Report, and used EV registrations climbed to just over 1%, from 0.7% the year prior. As we dove into the data, we found that Tesla remains the dominant player in both new and used sectors; however, the shift in consumer preferences is extending across various manufacturers with more models hitting the market. For instance, Tesla accounted for 50.7% of new retail registrations in 2024, from 60.6% in 2023. Meanwhile, Ford increased from 4.7% to 6.2% year-over-year and Hyundai went from 4.2% to 5.4%. On the used side, Tesla made up 59% of retail registrations, from 60% in 2023, while Chevrolet grew from 7.1% to 9% and Nissan was at 5.4%, from 8.3%. As the EV market continues to grow, it’s not just the various manufacturers making waves; geographical trends are also coming into play in shaping how these vehicles are being embraced nationwide. While EV adoption is expanding well beyond the traditional EV strongholds, California still holds the highest number of registrations, with Los Angeles accounting for more than 180,000 new retail EV registrations, followed by San Francisco at 91,000+ and San Diego with more than 31,000. Hartford and New Haven, Connecticut experienced the highest growth in new retail EV registrations over the last five years, reaching 110.5% in 2024. Close behind were El Paso, Texas (with a 99% increase), and Colorado Springs, Colorado (with an 85.7% spike). These shifts highlight the rapid expansion of EV adoption across the country as we see more consumers in diverse areas opting for the fuel type. Analyzing and leveraging the broader range of registrations will help automotive professionals as they identify emerging markets to effectively tailor their strategies. To learn more about EV insights, visit Experian Automotive’s EV Resource Center.

Avoid the Shamrock Swindle: How Financial Institutions Can Help Clients Steer Clear of Lottery Scams

Apply Identity Protection page tagFinancial institutions can help protect clients by educating them on the warning signs of fraudulent lottery scams.

Leveraging Analytics in Utilities: Navigating Market Challenges with Data-Driven Insights

Data & AnalyticsDiscover how data analytics in utilities helps energy providers navigate regulatory, economic, and operational challenges. Learn how utility analytics and advanced analytics solutions from Experian can optimize operations and enhance customer engagement.

Quick Summary: Leasing continues to increase in the electric vehicle (EV) market. EVs accounted for nearly 20% of all new vehicle leases in Q4 2024, up from only 2.11% of new vehicle leases four years ago in Q4 2020. With consumers looking for flexibility—both in monthly payment and model availability—we’re seeing leasing continue to surge in the electric vehicle (EV) market. According to Experian’s State of the Automotive Finance Market Report: Q4 2024, EVs accounted for 19.5% of all new vehicle leases this quarter, up from 11.7% last year and a substantial increase from 2.1% in Q4 2020. Diving a bit deeper, data found EVs accounted for 9.3% of all new purchases in Q4 2024. Of those EVs, 50.1% were leased, while 38.9% were financed through loans. With lease payments for EVs ultimately being more affordable compared to loans and the excitement of driving the latest models packed with advanced technology, it’s no surprise we’re seeing leasing grow in popularity. Top leased EVs: How do lease and loan payments compare? As more consumers transition to EVs and manufacturers introduce new options to their lineup, certain models have become top choices for those opting to lease. Tesla accounted for the top two leased EVs in Q4 2024, with Tesla Model 3 coming in at 12.2% and Tesla Model Y at 9.1%. However, the Honda Prologue followed closely at 8.8% this quarter. Rounding out the top five were Hyundai IONIQ 5 (6.9%) and Chevrolet Equinox EV (5.9%). It’s notable that leasing has traditionally been a value-driven option for consumers, and the same holds true in the EV market. Leasing continues to offer lower monthly payments, making the finance option stand out for those looking to test an EV before purchasing or simply wanting the latest model on the lot. In Q4 2024, the average payment difference between a loan and a lease was $175. Though, the average monthly payment to lease a non-luxury EV was $504 this quarter, noting a $205 difference compared to the $709 loan payment. By comparison, the average monthly payment between a loan and leased luxury EV was $98—coming in at $842 for a lease and $940 for a loan. As more consumers choose to lease EVs, automotive professionals in both new and used markets have a chance to capitalize on this trend. By leveraging this data, those in the new retail market can effectively reach the right audience, while those in the used market can stay ahead of the curve and prepare for the influx of off-lease models in the coming years. To learn more about automotive finance trends, view the full State of the Automotive Finance Market: Q4 2024 presentation on demand.

By providing an employee financial wellness program to empower your workforce, you can create a more engaged, motivated, and stable team.

Fraud rings cause an estimated $5 trillion in financial damages every year, making them one of the most dangerous threats facing today’s businesses. They’re organized, sophisticated and only growing more powerful with the advent of Generative AI (GenAI). Armed with advanced tools and an array of tried-and-true attack strategies, fraud rings have perfected the art of flying under the radar and circumventing traditional fraud detection tools. Their ability to adapt and innovate means they can identify and exploit vulnerabilities in businesses' fraud stacks; if you don’t know how fraud rings work and the right signs to look for, you may not be able to catch a fraud ring attack until it’s too late. What is a fraud ring? A fraud ring is an organized group of cybercriminals who collaborate to execute large-scale, coordinated attacks on one or more targets. These highly sophisticated groups leverage advanced techniques and technologies to breach fraud defenses and exploit vulnerabilities. In the past, they were primarily humans working scripts at scale; but with GenAI they’re increasingly mobilizing highly sophisticated bots as part of (or the entirety of) the attack. Fraud ring attacks are rarely isolated incidents. Typically, these groups will target the same victim multiple times, leveraging insights gained from previous attack attempts to refine and enhance their strategies. This iterative approach enables them to adapt to new controls and increase their impact with each subsequent attack. The impacts of fraud ring attacks far exceed those of an individual fraudster, incurring significant financial losses, interrupting operations and compromising sensitive data. Understanding the keys to spotting fraud rings is crucial for crafting effective defenses to stop them. Uncovering fraud rings There’s no single tell-tale sign of a fraud ring. These groups are too agile and adaptive to be defined by one trait. However, all fraud rings — whether it be an identity fraud ring, coordinated scam effort, or large-scale ATO fraud scheme — share common traits that produce warning signs of imminent attacks. First and foremost, fraud rings are focused on efficiency. They work quickly, aiming to cause as much damage as possible. If the fraud ring’s goal is to open fraudulent accounts, you won’t see a fraud ring member taking their time to input stolen data on an application; instead, they’ll likely copy and paste data from a spreadsheet or rely on fraud bots to execute the task. Typically, the larger the fraud ring attack, the more complex it is. The biggest fraud rings leverage a variety of tools and strategies to keep fraud teams on their heels and bypass traditional fraud defenses. Fraud rings often test strategies before launching a full-scale attack. This can look like a small “probe” preceding a larger attack, or a mass drop-off after fraudsters have gathered the information they needed from their testing phase. Fraud ring detection with behavioral analytics Behavioral analytics in fraud detection uncovers third-party fraud, from large-scale fraud ring operations and sophisticated bot attacks to individualized scams. By analyzing user behavior, organizations can effectively detect and mitigate these threats. With behavioral analytics, businesses have a new layer of fraud ring detection that doesn’t exist elsewhere in their fraud stack. At a crowd level, behavioral analytics reveals spikes in risky behavior, including fraud ring testing probes, that may indicate a forthcoming fraud ring attack, but would typically be hidden by sheer volume or disregarded as normal traffic. Behavioral analytics also identifies the high-efficiency techniques that fraud rings use, including copy/paste or “chunking” behaviors, or the use of advanced fraud bots designed to mimic human behavior. Learn more about our behavioral analytics solutions and their fraud ring detection capabilities. Learn more

Fraud never sleeps, and neither do the experts working to stop it. That’s why we’re thrilled to introduce Meet the Maker, our new video series spotlighting the brilliant minds behind Experian’s cutting-edge fraud solutions. In our first episode, Matt Ehrlich, Senior Director of Identity and Fraud Product Management, and Andrea Nighswander, Senior Director of Global Solution Strategy, share how they use data, advanced analytics, and deep industry expertise to stay ahead of fraudsters. With 35+ years of combined experience, these fraud-fighting veterans know exactly what it takes to keep bad actors at bay. Watch now for an exclusive look at the minds shaping the future of fraud prevention. Stay tuned for more episodes featuring the visionaries driving fraud innovation.

Why Credit Risk, Fraud, and Compliance Are Converging — and Why It Matters for Your Risk Strategy

Apply DA TagThe days of managing credit risk, fraud prevention, and compliance in silos are over. As fraud threats evolve, regulatory scrutiny increases, and economic uncertainty persists, businesses need a more unified risk strategy to stay ahead. Our latest e-book, Navigating the intersection of credit, fraud, and compliance, explores why 94% of forward-looking companies expect credit, fraud, and compliance to converge within the next three years — and what that means for your business.1 Key insights include: The line between fraud and credit risk is blurring. Many organizations classify first-party fraud losses as credit losses, distorting the true risk picture. Fear of fraud is costing businesses growth. 68% of organizations say they’re denying too many good customers due to fraud concerns. A unified approach is the future. Integrating risk decisioning across credit, fraud, and compliance leads to stronger fraud detection, smarter credit risk assessments, and improved compliance. Read the full e-book to explore how an integrated risk approach can protect your business and fuel growth. Download e-book 1Research conducted by InsightAvenue on behalf of Experian