Market Trends

In Q1 2020, 30-day delinquencies decreased from 1.98 percent in Q1 2019 to 1.93 percent, while 60-day delinquencies dropped from 0.68 percent to 0.67.

Today, Experian and Oliver Wyman launched the Ascend Portfolio Loss ForecasterTM, a solution built to help lenders make better decisions – during COVID-19 and beyond – with customized forecasts and macroeconomic data. Phrases like “the new normal,” “unprecedented times,” and “extreme economic volatility” have flooded not only media for the last few months, but also financial institutions’ strategic discussions regarding plans to move forward. What has largely been crisis response is quickly shifting to an urgent need to answer the many questions around “Will we survive this crisis?,” let alone “What’s next?” And arguably, we’ve entered a new era of loss forecasting. After the longest period of economic growth in post-war U.S. history, previously built models are not sufficient for the unprecedented and sudden changes in economic conditions due to COVID-19. Lenders need instant insights to assess impact and losses to their portfolios. The Ascend Portfolio Loss Forecaster combines advanced modeling from Oliver Wyman, pandemic-specific insights and macroeconomic scenarios from Oxford Economics, and Experian’s quality data to analyze and produce accurate loan loss forecasts. Additionally, all of the data, including the forecasts and models, are regularly updated as macroeconomic conditions change. “Experian’s agility and innovative technologies allow us to help lenders make informed decisions in real time to mitigate future risk,” said Greg Wright, chief product officer of Experian’s Consumer Information Services, in a recent press release. “We’re proud to work with our partners, Oxford Economics and Oliver Wyman, to bring lenders a product powered by machine learning, comprehensive data and macroeconomic forecast scenarios.” Built using advanced modeling and expert scenarios, the web-based application maximizes the more than 15 years of Experian’s loan-level data, including VantageScore® credit score, bankruptcy scores and customer-level attributes. Financial institutions can gauge loan portfolio performance under various scenarios. “It is important that the banks take into account the evolving credit behaviors due to the COVID-19 pandemic, in addition to the robust modeling technique for their loss forecasting and strategic decisioning,” said Anshul Verma, senior director of products at Oliver Wyman, also in the release. “With the Ascend Portfolio Loss Forecaster, lenders get robust models that work in the current conditions and take into account evolving consumer behaviors,” Verma said. To watch Experian’s webinar on portfolio loss forecasting, please click here and to learn more about the Ascend Portfolio Loss Forecaster, click the button below. Learn More

The COVID-19 pandemic and resulting rush to transition to a remote lifestyle made it clear that many businesses need a refreshed digital authentication and fraud prevention strategy that includes an investment in technology and provides consumer assurance. This is particularly important when it comes to identity, as many of the standard in-person verification methods and tools are currently unavailable. The meaning of identity is growing and shifting Technology trends are intersecting with social trends to create heightened awareness, and a whole new public conversation has emerged around customer trust and privacy. Attitudes and ideas are changing—even to the point of what we mean by “identity.” An identity is no longer just a name, date of birth, and SSN. Now, there are digital manifestations everywhere you look: screen names, email addresses, mobile phone numbers, device identifiers, and the other “exhaust” we leave behind as we travel the internet. This leads to concerns about what an identity is, who owns it, and who manages and protects it. Businesses have to be able to prove to their ability to protect their customers’ identities through investment in technology and a robust fraud strategy. Consumer attitudes are changing Several years ago, consumers were excited by all the new digital capabilities and the speed, ease, and convenience they provided. Last year, Experian found that consumers still wanted those things, with 70% willing to provide more information to businesses if there was a perceived benefit. However, they also wanted more security in the balance. In Experian’s most recent Global Identity and Fraud Report, we found that 74% of consumers say that security is the most important factor when deciding to engage with a business. Consumers are particularly more tolerant of friction during the enrollment process—as a means of building trust. But, when they return to the app or website, they want to be recognized. This means achieving a balance by using layered technologies, some of which are active and visible to the consumer, and some of which are invisibly working in the background to confirm the identity of returning consumers. Consumer attitudes vs. regulatory pressure The drivers behind the business changes are twofold: shifting consumer attitudes and regulatory changes. While regulations are becoming stricter on a national and global level, they’re not keeping pace with technology and social change. The digital world is evolving at a rapid pace, opening up more new ways for companies to collect information about consumers and use it to identify and verify, and also to target goods and services. With all of this data available, it’s important for businesses to use the tools in the market to help protect identity information. Next steps in technology The bottom line is, businesses can’t wait for regulations to dictate how best to protect information. Instead, they should be looking to technologies like physical and behavioral biometrics to help provide identity authentication and protection – layering those solutions with information from the user and from third parties to give a holistic consumer view. Businesses should adopt a platform approach for identity and fraud in order to be able to adapt quickly, whether to incorporate new kinds of technology or to prevent emerging types of fraud. By investing in technology now, even in the midst of the COVID-19 pandemic, businesses can build the flexibility needed to respond to future crises and help offset future fraud losses. In turn, those fraud-loss savings can then be used to help grow the business in the future. Learn more about Experian’s commitment to helping businesses maximize their investment in technology to safeguard against fraud. Learn more

Rays of hope are beginning to shine in the economy that suggest the U.S. may have moved beyond the most acute phase of the economic crisis. The housing sector, in particular, looks poised to regain momentum and perhaps lead the path towards stabilization in the second half of 2020. A “V-Shaped” rebound in mortgage applications Despite record levels of unemployment and widespread economic uncertainty, homebuyers have returned to the market with conviction. After shelter-in-place restrictions curtailed open-house visits and crimped buyer demand in early April, applications to purchase a home have risen for six consecutive weeks, according to the Mortgage Bankers Association. The latest data for the week of May 22nd, indicate that purchase applications were 9% higher than during the same period in 2019. If this trend continues, it will show that significant pent-up demand exists in the housing market that may be able to offset some of the lost spring buying season. April new home sales far exceed expectations After declining by 13.7% in March, new home sales rose a modest 0.6% in April. While this was only a slight gain, it was considerably above economists’ projections of a fall of 20% and may mark the turning point in the downtrend. Since the recording of new home sales data occurs when the purchase contract is signed or a deposit is accepted – and is typically for a house that hasn’t been built yet or is currently under construction – it provides a gauge of how buyers feel about their future economic prospects. Building a home also requires hiring new construction workers, buying building supplies, and supporting a host of ancillary industries, thus making it an indicator of further economic activity. Some of the increase in demand for new homes may have been driven by coronavirus quirks. The number of existing homes on the market is at record lows and many people may have been reluctant to put their home up for sale and have buyers tour as health concerns remain. Buyers, as well, may have preferred to steer clear of occupied homes or were unable to make in-person visits due to shelter-in-place restrictions. This lack of options for home buyers, coupled with record-low mortgage rates, likely drove sales of new homes higher. However, for the same reasons why new home sales rose, pending sales for existing homes fell sharply. In April, the National Association of Realtors reported that sales declined by 21.8%, which is the largest drop in ten years. Home prices continue to gain ground Even with shelter-in-place restrictions dampening buyer demand in early April, home values have continued to rise. This is because the supply of homes on the market also contracted, resulting in a simultaneous drop of demand and supply. According to Zillow Research, the total inventory of homes for sale is down roughly 20% from this time last year. With fewer competing homes on the market, sellers have been reluctant to slash prices and are betting that the lack of options and low mortgage rates will keep buyers on the hook. In April, U.S. home values rose 4.3% from the year before. The states with the strongest growth were Idaho (9.8%), Arizona (8.5%), Maine (7.6%), and Washington (7.4%). It will be interesting to see if this pattern of growth changes as newly implemented work from home policies may shift where people prefer to live and work. Why it matters The housing market has an outsized influence on the overall direction of the U.S. economy. Housing is not only is a big contributor to economic growth, but many owners have a large portion of their wealth tied up in their home. If the housing market can find its footing in the second half of 2020, then it could set the stage for an eventual economic recovery. Learn more

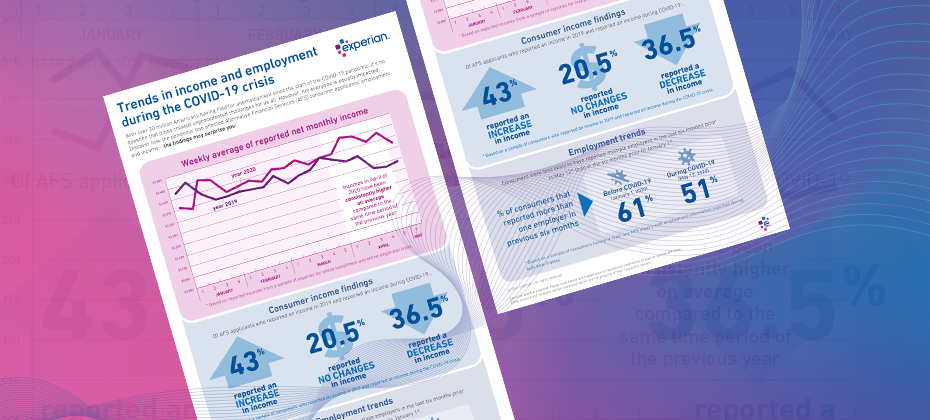

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

Including vehicle history reports in online vehicle listings create a more complete picture of the vehicle a consumer is looking at online.

The economic impact of the COVID-19 health crisis is ever-evolving and requires great flexibility and planning from lenders. Shannon Lois, Experian’s Senior Vice President, Analytics, Consulting and Operations, discusses what lenders can expect and next steps to take. Q: Though COVID-19 is catalyzing a sharp economic slowdown, many experts expect it to be temporary and liken it more to a global natural disaster than the prior financial crisis. What are your reactions? SL: There is still debate as to whether we will have a U-shaped or a V-shaped recession and its probable severity and longevity. Regardless, we are in a recession caused by a health pandemic with uncertainty of what it will mean for our global economy and without a clear view as to when it will end. The sooner we can contain the virus the more it will help to curtail the size of the recession. The unemployment rates and the consumer lack of confidence in the future will continue to contract spending which in turn will continue to propagate the recession. Our ability to limit COVID-19 over the coming months will have a direct impact in the economy, although the effects will probably linger on for six or more months. Q: From an economic perspective, what are the current trends we’re seeing? SL: Unemployment has skyrocketed and every business sector has been impacted although with different degrees of severity. In particular, tourism/hospitality, airlines, automotive, consumer products and retail have suffered. Consumers’ financial status varies and will continue to fluctuate, and credit conditions tighten while welfare payments increase. The government programs that have started will help, but they’re not enough to counter a prolonged recession. As some states seek to reopen and others extend their shelter in place orders, we will continue to see economic changes, with different sectors bouncing back or dipping further depending on their geographic location. Q: How does the economic slowdown compare to what we may have expected previously? SL: This recession is different than anything we have encountered previously not only because of the health concerns and implication of our population but because of the uncertainty of it all. As an example, social distancing has significantly and immediately impacted consumer demand but overall it is their low confidence in the future that will cause a continuous drop in discretionary and non-discretionary spending. Not only do we have challenges on the demand side, we also are seeing the same on the supply side with no automotive manufacturing occurring in the USA, and international oil flooding the market causing negative impact on domestic oil and the broad energy market. Q: How do the unemployment and liquidity challenges come into play? SL: The unemployment rate has already jumped to a record high. Most consumers are facing liquidity and affordability challenges and businesses do not have enough cash reserves to sustain them. Consumer activity has shifted drastically across all channels while lenders are exercising more caution. If this is a V-shaped recession (and hopefully it will be), then most activity is bound to spring back quickly in Q3. With companies safeguarding some jobs and the help of governments’ supplemental programs, businesses will restore supply and consumer demand will get a kick start. Q: What is the smartest next play for financial institutions? SL: The path forward requires several steps. First, understand your customers, existing and new. Refine your policies with the right information around your customers’ financial situations and extend programs (forbearance and loan payment forgiveness) as needed under the right guidelines. It’s also important to use refreshed data to lend to consumers and businesses who need it now more than ever, with the proper policies and fraud checks in place. Finally, increase your agility to operate effectively and dynamically with automation, interactive communication and self-serving digital tools. Experian is committed to helping lenders throughout these uncertain times. For more resources, visit our Look Ahead 2020 Resource Hub. Learn more About Our Expert Shannon Lois, Senior Vice President, Analytics, Consulting and Operations, Decision Analytics Shannon and her team of analysts, scientists, credit, fraud and marketing risk management experts provide results-driven consulting services and state-of-the-art advanced analytics, science and data products to clients in a wide range of businesses, including banking, auto, credit, utility, marketing and finance. Prior to her current role, she founded the Advisory Services practice at Experian, driving to actionable and proven solutions for our clients’ most pressing business problems.

With jobs losses mounting and the prospects for a quick economic rebound fading, some segments of the financial markets are beginning to bet that the Federal Reserve will take interest rates negative for the first time in U.S. history. If that happens, it could have a profound impact on the U.S. economy, and more specifically, on financial institutions. While other nations such as Denmark, Japan, Sweden, and Switzerland have experimented with negative rates over the years, the U.S. has shied away – both for political and economic reasons. Instead, when interest rates are near zero, the Fed prefers to use a mix of large-scale asset purchases and forward guidance to support the economy. In the current crisis, the Fed has also launched several new emergency lending programs to ensure the smooth functioning of the financial system. The question remains, however, if these tools will be enough to keep the U.S. out of a deep recession, especially if Congress fatigues on further fiscal support. The Fed is independent but keep an eye on the markets In his May 13th remarks to the Peterson Institute for International Economics, Fed Chairman Jerome Powell said that he and the rest of the rate-setting committee unanimously shared the same view on negative rates: “For now, it is not something we are considering”. While some market watchers looked for clues in the “for now” phrasing, it was clear from the rest of his remarks that the bar for enacting negative rates was set very, very high. However, despite the Fed having independence in its policy-making decisions, financial markets and to some extent, politics, still have influence. And there is precedent for markets exerting pressure on the Fed and perhaps even getting their way. In 2013, when then-Fed Chairman Ben Bernanke made a surprise announcement that the Fed would reduce the level of asset purchases, global financial markets went into a frenzy. That period, now known as the “Taper Tantrum”, altered the way the Fed signals its policy actions. More recently, the big declines in equity markets in late 2018 were seen by many as a primary driver in the Fed’s sudden U-turn from raising rates four times that year to lowering them three times in 2019. Now, with equity markets wanting more stimulus and traders in fed fund futures appearing to anticipate negative rates from the central bank in early 2021, there is concern that the markets are trying to bully their way again. And with the president’s renewed call for the Fed to take rates negative, there is some reason to believe that “not now” could become “now” sooner than many expect. Concerns for financial institutions While several central banks have resorted to negative interest rate policy for years, the efficacy of its use is unclear. But what is clear, is that financial institutions bear the greatest burden in implementing the policy. Currently in the U.S., banks earn interest on excess reserves held at the Fed. Negative rates would essentially flip the script and penalize this practice, forcing banks either to pay the Fed interest or do something else with the money. The hope is that this will encourage banks to make more loans and stimulate the economy. However, as Fed Chair Powell said in his remarks, he believes that negative rates could have the opposite effect and curtail lending. Since negative rates would put a downward pressure on interest rates across the board, the net interest margin – the spread banks make between what they pay depositors and what they charge for loans – would be compressed and profitability would sink. If banks and other financial institutions are struggling, credit availability could decline when it is needed the most. Why it matters Financial institutions cannot ignore the possibility of negative interest rates in the U.S. as it would have wide-ranging effects and potentially significant consequences. And while Fed officials have said they are not considering negative rates, the notion is not totally off the table. As the famous economist, Stanley Fischer, advised his fellow central bankers in his well-known piece “Central Bank Lessons from the Global Crisis”: “In a crisis, central bankers (and no doubt other policymakers) will often find themselves deciding to implement policy actions that they never thought they would have to undertake – and these are frequently policy actions that they would prefer not to have to undertake. Hence, a few final words of advice for central bankers: Never say never.”

When running a credit report on a new applicant, you must ensure Fair Credit Reporting Act (FCRA) compliance before accessing, using and sharing the collected data. The Coronavirus Aid, Relief, and Economic Security (CARES) Act has impacted credit reporting under the FCRA, as has new guidance from the Consumer Financial Protection Bureau (CFPB). Recent updates include: The CARES Act amended the FCRA to require furnishers who agree to an “accommodation,”1 to report the account as current, although it is permitted to continue to report the account as delinquent if the account was delinquent before the accommodation was made. Although not legally obligated, data furnishers should continue furnishing information to the credit reporting agencies (CRAs) during the COVID-19 crisis, and make sure that information reported is complete and accurate. Below is a brief FCRA-related compliance overview2 covering various FCRA requirements3 when requesting and using consumer credit reports for an extension of credit permissible purpose. For more information regarding your responsibilities under the FCRA as a user of consumer reports, please consult your Legal Counsel and the Notice to Users of Consumer Reports: Obligations of Users Under the FCRA handbook located on our website. Before obtaining a consumer report you have… Reviewed your federal and state regulations and laws related to consumer reports, scores, decisions, etc. Made sure you have a valid permissible purpose for pulling the consumer report. Certified compliance to the CRA from which you are getting the consumer report. You have certified that you complied with all the federal and state requirements. After you take an adverse action based on a consumer report you… Provide the consumer with an oral, written or electronic notice of the adverse action. Provide written or electronic disclosure of the numerical credit score used to take the adverse action, or when providing a “risk-based pricing” notice. Provide the consumer with an oral, written or electronic notice, which includes the below information: Name, address and telephone number of CRA that supplied the report, if nationwide. A statement that the CRA did not make the adverse decision and therefore can’t explain why the decision was made. Notice of the consumer’s right to a free copy of their report from the CRA, if requested within 60 days. Notice of the consumer’s right to dispute with the CRA the accuracy or completeness of any information in a consumer report provided by the CRA. Provide the consumer with a “risk-based pricing” notice if credit was granted but on less favorable terms based on information in their consumer report. We understand how challenging it is to understand and meet all your obligations as a data furnisher – we’re here to make it a little easier. Click below to speak with a representative and gain more insight on how the CARES Act impacts FCRA reporting. Download overview Speak with a representative 1An “accommodation” is defined as “an agreement to defer one or more payments, make a partial payment, forbear any delinquent amounts, modify a loan or contract, or any other assistance or relief” granted to a consumer affected by COVID-19 during the covered period. 2This FCRA overview is not legal guidance and does not enumerate all your requirements under the FCRA as a user of consumer reports. Additionally, this FCRA Overview is not intended to provide legal advice or counsel you regarding your obligations under the FCRA or any other federal or state law or regulation. Should you have any questions about your institution’s specific obligations under the FCRA or any other federal or state law or regulation, you should consult with your Legal Counsel. 3This FCRA overview is intended to be used solely by financial service providers when extending credit to consumers and does not include all FCRA regulatory obligations. You are responsible for regulatory compliance when requesting and using consumer reports, which includes adhering to all applicable federal and state statutes and regulations and ensuring that you have the correct policies and procedures in place.

There is no doubt that there will be many headlines published about the latest Bureau of Labor Statistics (BLS) jobs report. The official unemployment rate spiked to 14.7%, the highest level since the Great Depression, and employers shed an unprecedented 20.5 million jobs. However, given the scale and pace that businesses around the country are adjusting their workforces, these headline numbers – especially the official unemployment rate – fall short in capturing the nuances and internal dynamics of the crisis. To get a better picture of labor market health in the coming months, there are three other components reported in BLS’s employment release that require close attention: the underemployment rate, the labor force participation rate, and the employment-population ratio. Tracking underemployment The BLS reports six unemployment figures in its monthly employment release, U1 – U6. The most cited is the “official” unemployment rate, which is U3. However, in the current crisis, the more salient measure of unemployment is U6, which is often known as the “underemployment” rate. This is because the underemployment (U6) rate takes the unemployed and adds on part-time workers who want a full-time job (BLS calls this segment “part time for economic reasons”), plus marginally attached and discouraged workers (those who don’t think they can find work). Viewing the employment landscape through this lens provides greater insight into the pain points within the labor market. In April, the underemployment rose from 8.7% to 22.8% - the largest jump on record. A large contributor to the rise was a doubling of the number of part-time workers that wanted a full-time job. Mirroring what happened in previous downturns, the rise in this segment was caused by employers downshifting workers into part-time roles. The official unemployment rate will miss this insight as it classifies everyone who is working as “employed”, regardless if they worked one hour or 100 hours. Trends in the underemployment rate will be especially important to watch as the recovery gets underway. If employers are doubtful of a strong rebound, they may keep employees on as part time and forgo filling any full-time positions. Who’s in and who’s out of the labor force The labor force participation rate is the percentage of the working-age population (aged 16+) that is employed or searching for a job. A decline in the labor force participation rate means that people are leaving the workforce and are no longer looking for employment. April’s employment report showed labor force participation declining from 62.7% to 60.2%. Teenage participation was especially hard hit, dropping from 35.5% to 30.8% - the lowest level since the government started collecting the data in 1948. During the recovery phase, tracking what happens with labor force participation will provide insight into how potential workers perceive their chances of landing a job and if it is safe to return. A healthy (or improving) labor market will bring people off the sidelines in search of work, while a weak labor market will do the opposite. Get a clearer view with the employment-population ratio In the current environment where people are bouncing rapidly between employed, unemployed, underemployed, and out of the labor force, tracking the employment-population ratio provides a more stable baseline to view the economic environment. The latest data shows that the employment-population ratio dropped to the lowest level on record of 51.3% in April. This means that only half of people who are of working age in the U.S. are currently employed in some form. Unlike the unemployment rate, which is calculated by dividing the number of unemployed workers by the labor force and thus subject to more variation as people start and stop looking for work, the employment to population ratio is the percentage of the total working-age population that is currently employed. By having a more stable baseline, it is easier to locate trends and see through the market gyrations. And finally, why it matters The labor market is the backbone of the economy and is the engine that powers the US consumer. But the ongoing crisis and rapid reallocation of the workforce has made it difficult to get a clear picture on what is happening at the ground level. By going beyond the headlines, businesses and financial institutions can glean nuanced insights that provide a better view of where the opportunities lie and how the recovery is likely to unfold. Learn more

The effects of the COVID-19 pandemic has created extreme volatility in the US markets. While the high unemployment rate and impact on the stock market can be attributed to the pandemic, there were signs that the economy was already headed for a downturn. In a recent webinar, Mohammed Chaudhri, Experian’s UK Chief Economist, stated, “Even in the absence of COVID-19, […] the consensus was that the US was going into a period of a slowdown. Talks of a recession were building and financial indicators all pointed to an inverse yield curve.” With a global recession on the horizon, economists are using different scenarios to forecast potential outcomes. Chaudhri and his team of Experian economists mapped out four macroeconomic scenarios for economic recovery: V-shape scenario: A scenario in which the U.S. is able to recover losses and is able to recover quickly – possibly within 3 months. The impacts of strict lockdowns and social distancing may allow for a V-shape recovery. This V-shape follows previous pandemics and is the most likely outcome. Delayed V-shape scenario: A scenario in which the economy bounces back (albeit much slower than a regular V-shape). This may occur as various states slowly lift their lockdown guidelines and return to business as usual. This delay can be caused by regulations and guidelines that vary from state to state. U-shape scenario: A scenario in which the U.S. is unable to return to pre-COVID-19. W-shape scenario: A scenario that is much more serious than a U-shape and has the greatest impact on the economy. This can occur if the state lockdowns are lifted too early and a reemergence of the virus occurs. In our latest on-demand webinar, our experts discuss current trends which are indicative of emerging patterns and highlight economic forecasts that show some immediate concentrations of risk and exposure and the implications for your organization. Take a deeper dive into the latest data insights relating to the credit economy, and specifically, the impact brought by COVID-19. Explore the macroeconomic outlook, including: The immediate and near-term economic impact Views on how a downturn could impact consumers’ affordability and emerging signs of vulnerability Views on what KPIs you should focus on Watch the webinar

After two consecutive emergency meetings in March and numerous stimulus announcements, the Federal Open Market Committee (FOMC) finally got back on track and wrapped up their standard two-day meeting on April 29th. While Fed officials did not make any changes to the federal funds rate – which is currently sitting near zero - or to the level of purchases of treasuries and mortgage-backed securities, they did provide a glimpse into how long rates are likely to remain at their current levels. Hint: It is going to be a while. Understanding the Fed’s statement In order to get a clearer picture of what the Fed is thinking, skip the headlines and go straight to the source – the post-meeting press release. Here is the most important paragraph from their statement (with the key components underlined): “The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term. In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” Just by taking the statement at face value, it is clear the Fed is going to keep rates where they are for some time, but for how long? That depends on how the key phrases are interpreted. The first, “over the medium term”, seems simple but requires some detective work. What does “medium term” mean? In the post-meeting press conference, the Fed Chairman was asked this question and he alluded that it likely means a year or more. So, there is part 1 - the Fed expects to keep rates near zero for at least a year. That is not all that surprising, but it does provide a floor: a minimum timeframe. Key phrase 2, however, requires a bit more effort but is where the real story lives. The dual mandate is no longer a balancing act “The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.” There is a lot of economics in that sentence. The Fed has been mandated by Congress to achieve two primary goals – maximum employment and price stability (inflation near 2%). These two goals, or the “dual mandate” as they are often referred to, seem simple but have historically been at odds. The thinking went that if the Fed kept interest rates low to support employment, then inflation would rise. And if the Fed increased interest rates to control inflation, then employment would decline. A delicate balance - at least it was thought. Somewhere in the last couple of years Fed officials have realized that even after a decade of near-zero interest rates following the financial crisis and very-low levels of unemployment, inflation has remained persistently below their 2% target. Something has broken in the relationship. This is key, because it means that the Fed now feels free to keep interest rates exceptionally low in order to get employment back on track, without having to worry about inflation; and may in fact need to keep rates lower for longer in order to boost inflation. Both sides of the dual mandate now appear to require low rates. Chasing “maximum employment” With inflation no longer a priority for Fed officials at the moment, their sights are set squarely on achieving the maximum employment portion of the mandate. But what does it mean to achieve “maximum employment”? Well, it is an elusive target, but in general, it is the point at which rising wages leads to higher inflation – the result of businesses increasing pay to compete for a shrinking supply of workers. What is known is that even when the unemployment rate was at a 50-year low of 3.5% in early 2020, wages were not rising much. Which indicates that the economy may have been near maximum employment but was not quite there yet. So, to achieve maximum employment, unemployment needs to be somewhere near 3.5% and that could take some time, a long time. Current range estimates show the unemployment rate rising to anywhere between 12 – 30% in the coming months. And a recent report out of the Congressional Budget Office projected that unemployment will still be around 9.5% at the end of 2021. The last time the unemployment rate was at 9.5% was right after the financial crisis, and from that point it took nearly a decade for the rate to fall to 3.5%. And while it is not expected that the current crisis will be as prolonged as the previous one, it still provides a reference point as to how long it can take to recover job losses. So how long does the Fed expect to keep rates near zero? One year at the very minimum, easily two years, and perhaps up to a decade.

Essential personnel and organizations are working tirelessly to deliver food and other resources, not to mention, protecting the health and safety of those around us. These vehicles still require proper maintenance and care to ensure they run smoothly. That’s where the automotive industry can help.

The coronavirus (COVID-19) outbreak is causing widespread concern and economic hardship for consumers and businesses across the globe – including financial institutions, who have had to refine their lending and downturn response strategies while keeping up with compliance regulations and market changes. As part of our recently launched Q&A perspective series, Shannon Lois, Experian’s Head of DA Analytics and Consulting and Bryan Collins, Senior Product Manager, tackled some of the tough questions for lenders. Here’s what they had to say: Q: What trends and triggers should lenders be prepared to react to? BC: Lenders are still trying to figure out how to assess risk between the broader, longer-term impacts of the pandemic and the near-term Coronavirus Aid, Relief, and Economic Security (CARES) Act that extends relief funds and deferment to consumers and small businesses. Traditional lending processes are not possible, lenders will have to adjust underwriting strategies and workflows as they deploy hardship programs while complying with the Act. From a utilization perspective, lenders need to look for near-term trends on payments, balances and skipped payments. From an extension standpoint, they should review limits extended or reduced by other lenders. Critical trends to look for would be missed or late auto payments, non-traditional credit shopping and rental payment delinquencies. Q: What should lenders be doing to plan for an uptick in delinquencies? SL: First, lenders should make sure they have a complete picture of how credit risk and losses are evolving, as well as any changes to their consumers’ affordability status. This will allow a pointed refinement of their customer management strategies (I.e. payment holidays, changing customer to cheaper product, offering additional services, re-pricing, term amendment and forbearance management.) Second, given the increased stress on collection processes and regulations guidelines, they should ensure proper and prepared staffing to handle increased call volumes and that agency outsourcing and automation is enabled. Additionally, lenders should migrate to self-service and interactive communication channels whenever possible while adopting new segmentation schemas/scores/attributes based on fresh data triggers to queue lower risk accounts entering collections. Q: How can lenders best help their customers? SL: Lenders should understand customers’ profiles with vulnerability and affordability metrics allowing changes in both treatment and payment. Payment Holidays are common in credit card management, consider offering payment freezes on different types of credit like mortgage and secured loans, as well as short term workout programs with lower interest rates and fee suppression. Additionally, lenders should offer self-service and FAQ portals with information about programs that can help customers in times of need. BC: Lenders can help by complying with aspects of the CARES Act guidance; they must understand how to deploy payment relief and hardship programs effectively and efficiently. Data integrity and accuracy of loan reporting will be critical. Financial institutions should adjust their collection and risk strategies and processes. Additionally, lenders must determine a way to address the unbanked population with relief checks. We understand how challenging it is to navigate the changing economic tides and will continue to offer support to both businesses and consumers alike. Our advanced data and analytics can help you refine your lending processes and better understand regulatory changes. Learn more About Our Experts: Shannon Lois, Head of DA Analytics and Consulting, Experian Data Analytics, North America Shannon and her team of analysts, scientists, credit, fraud and marketing risk management experts provide results-driven consulting services and state-of-the-art advanced analytics, science and data products to clients in a wide range of businesses, including banking, auto, credit, utility, marketing and finance. Shannon has been a presenter at many credit scoring and risk management conferences and is currently leading the Experian Decision Analytics advisory board. Bryan Collins, Senior Product Manager, Experian Consumer Information Services, North America Bryan is a member of Experian's CIS product management team, focusing on the Acquisitions suite and our evolving Ascend Identity Services Platform. With more than 20 years of experience in the financial services and credit industries, Bryan has established strong partnerships and a thorough understanding of client needs. He was instrumental in the launch of CIS's segmentation suite and led product management for lender and credit-related initiatives in Auto. Prior to joining Experian, Bryan held marketing and consumer experience roles in consumer finance, business lending and card services.

Many small businesses in the hardest-hit states missed out on the first round of federal relief through the recently created Paycheck Protection Program (PPP). The Coronavirus Aid, Relief, and Economic Security (CARES) Act established the PPP in order to disburse $349 billion in forgivable loans to small businesses hurt by the COVID-19 outbreak. However, the program’s funding limit and first-come, first-serve method for accepting loan applications put an immense strain on the financial institutions tasked with getting the money out the door. This resulted in many small businesses unable to get their applications submitted, approved, and funded before the program ran out of money after only two weeks. Where did the money go? The latest data from the Small Business Administration shows that the most populous states received the largest number of PPP loans. This is unsurprising, as states with higher populations tend to have a greater number of small businesses. One way to get a better picture of the impact of PPP loans on communities is to examine what percentage of a state’s small businesses received PPP loans (Figure 1). When viewed through this lens, the results are a quite striking - many of the coastal areas and larger markets missed out, while the rural, north-central states won out. Less than 4% of small businesses in California, Florida, and New York – three of the top five largest markets – were approved for PPP loans. While more than 12% of small businesses in North Dakota, Nebraska, and South Dakota received support. What happened? There are several factors that could have played a part in the uneven distribution of PPP loans. One explanation may be that some financial institutions in highly populated urban areas did not have the capacity to process such a large volume of loan applications in such a short amount of time. There may also be an urban-rural divide to how relationship banking occurs. Rural communities and small businesses with close-knit ties to area financial institutions may have had easier access to getting their PPP applications submitted and approved. In line with this, Figure 2 shows the top five and bottom five states in terms of financial institutions (banks and credit unions) per 100,000 people. The states with the highest prevalence of financial institutions were also the top states for PPP small business loan share. While the states with the lowest prevalence of financial institutions were the states with the smallest share. Another factor may have been the extent that shelter-in-place rules were being enforced. North Dakota, Nebraska, and South Dakota – the three top states for loan share – are part of the handful of states that still do not have statewide lockdowns. California, on the other hand, was the first state in the country to issue shelter-in-place measures. Why it matters The first round of stimulus through the Paycheck Protection Program provided relief for many small businesses around the country. However, the first-come, first-serve method of distributing loans may have resulted in some small business communities having easier access to the program than others. Insights as to why these differences occurred and why small businesses in the larger markets received a lower share of PPP loans can inform future stimulus efforts and ensure that recovery among the states is as even and broad as possible. Figure 1 Sources: Small Business Administration Paycheck Protection Program Report 4/16/2020, Census Bureau SUSB and NES Statistics. Author’s calculations. Figure 2 Sources: Experian data on financial institutions, Census Bureau population estimates. Author's calculations.