Latest Posts

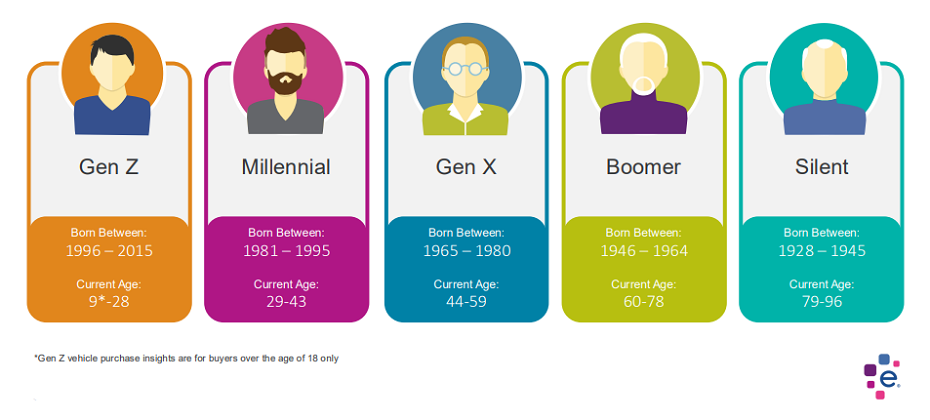

Quick Answer: New research on generational buying habits can help the auto industry better understand target audiences and improve marketing. The automotive industry is undergoing a rapid transformation, driven by technological advancements, changing consumer preferences, and a diverse marketplace. To navigate this complex landscape, understanding your target audience is key. This is where generational insights are indispensable. Why Generations Matter Each generation brings unique values, preferences, and buying behaviors to the table. Ignoring these differences can lead to ineffective marketing campaigns and missed opportunities. Different Needs and Priorities: Baby Boomers, Gen X, Millennials, and Gen Z have distinct needs and priorities when it comes to vehicles. For example, Baby Boomers may purchase more luxury vehicles, while Gen Z purchases a higher percentage of non-luxury vehicles. Communication Styles: Each generation responds differently to marketing messages. Traditional advertising might resonate with Baby Boomers, while social media and influencer marketing could be more effective for younger generations. Purchasing Behavior: The way people research and purchase cars has evolved significantly across generations. Understanding these differences can help you optimize your sales process. Leveraging Generational Insights To effectively leverage generational insights, consider the following: Conduct In-Depth Research: Gain a deep understanding of each generation's values, preferences, and buying habits. Use data analytics, surveys, and focus groups to gather insights. Create Targeted Messaging: Develop tailored messaging that resonates with each generation. Highlight the features and benefits that matter most to them. Choose the Right Channels: Select the most effective marketing channels for each generation. For example, television advertising might be less effective for Gen Z compared to social media. Personalize the Customer Experience: Offer personalized experiences that cater to the specific needs and preferences of each generation. Embrace Technology: Utilize technology to reach and engage different generations. For example, virtual showrooms or augmented reality experiences can appeal to younger consumers. Special Report: Generational Insights We've conducted in-depth research on generational buying habits for new and used vehicles. These insights can revolutionize your automotive marketing and sales strategies. Gain a competitive edge with our Automotive Consumer Trends Special Report: Generation Insights. Discover how to tailor your approach for maximum impact. Conclusion In today's competitive automotive market, understanding your target audience is essential for success. By incorporating generational insights into your marketing strategy, you can create more effective campaigns, build stronger customer relationships, and drive sales growth. Remember, a one-size-fits-all approach is unlikely to work. Embrace the diversity of your audience and tailor your message accordingly. Experian Automotive is here to help you with your marketing needs. If you’d like to learn more about our solutions and how we can support you, contact us below.

Dealerships can avoid purchasing flood-damaged vehicles with Experian AutoCheck's Free Flood Risk Check.

In this report, we explore how the evolving fraud landscape is impacting identity verification, customer experience, and business priorities for the future.

To authenticate identities and combat fraud within the Gen Z population, financial organizations need to implement comprehensive strategies.

AI fraud detection helps organizations enhance their security measures, reduce fraud losses, authenticate identity, and improve customer experience.

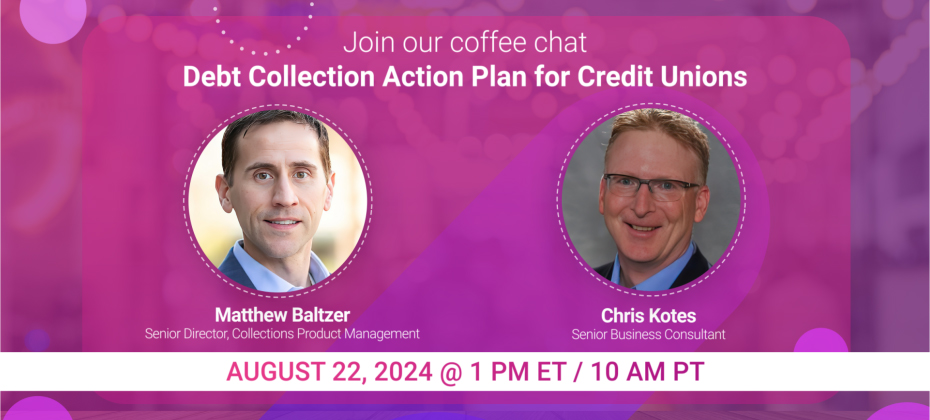

Grab a cup of coffee and join our experts for a conversation on credit union collection trends and successful account management strategies.

In this article...Recent trends in credit card debtThe rising tide of delinquenciesWhat is credit limit optimization?Benefits of credit limit optimizationEconomic indicators and CLO ImpactEnhanced profitability and risk mitigation This post was originally published on our Global Insights Blog. As credit card issuers grow, the size of their customer base expands, bringing both opportunities and challenges. One of the most critical challenges is managing growth while controlling default rates. Credit limit optimization (CLO) has emerged as a vital tool for banks and credit lenders to achieve this balance. By leveraging machine learning models and mathematical optimization, CLO enables lenders to tailor credit limits to individual customers, enhancing profitability while mitigating risk. Recent trends in credit card debt To understand the significance of CLO, it is essential to consider the current economic landscape. The first quarter of 2024 saw total household debt in the U.S. rise by $184 billion, reaching $17.69 trillion. While credit card balances declined slightly (a reflection of seasonal factors and consumer spending patterns), they remain a substantial component of household liabilities, with total credit card debt standing at approximately $1.26 trillion in early 2024. On average, American households hold around $10,479 in credit card debt, which is down from previous years but still significant. The average APR for credit cards in the first quarter of 2024 was 21.59%.* The rising tide of delinquencies In the first quarter of 2024, about 8.9% (annualized) of credit card balances transitioned into delinquency. This trend underscores the need for credit card issuers to adopt more sophisticated methods to assess credit risk and adjust credit limits accordingly. The rising rate of credit card delinquencies is a key driver behind the adoption of CLO strategies. What is credit limit optimization? Credit limit optimization uses advanced analytics to assess individual customers’ creditworthiness. By analyzing various data points, including payment history, income levels, spending patterns, and economic indicators, these tools can recommend optimal credit limits that maximize customer spending potential while minimizing the risk of default, all within the constraints set by the business in terms of its appetite for risk and capacity. For instance, a customer with a strong payment history and stable income might receive a higher credit limit, encouraging more spending and enhancing the lender’s revenue through interest and interchange fees. Conversely, customers showing signs of financial stress might see their credit limit reduced to prevent them from accumulating unmanageable debt. Benefits of credit limit optimization Improved profitability – By setting credit limits reflecting customers’ credit risk and spending potential, lenders can increase their revenue through higher interest and fee income. Reduced default rates – Lenders can significantly reduce the incidence of bad debt by identifying customers at risk of default and adjusting their credit limits accordingly. Improved customer satisfaction – Personalized credit limits can improve customer satisfaction, as customers are more likely to receive credit that matches their needs and financial situation. Regulatory compliance – CLO can help lenders comply with regulatory requirements by ensuring that credit limits are set based on objective, data-driven criteria. Economic indicators and CLO Impact Several economic indicators provide context for the importance of CLO in the current market. For instance, the Federal Reserve reported that in 2023, fewer than half of adult credit cardholders carried a balance on their cards, down from previous years. This indicates a more cautious approach to credit use among consumers, likely influenced by economic uncertainty and rising interest rates. Moreover, the disparity in credit card debt across different states highlights the varying economic conditions and the need for tailored credit strategies. States like New Jersey have some of the highest average credit card debts, while states like Mississippi have the lowest. This regional variation underscores lenders’ need to adopt flexible, data-driven approaches to credit limit setting. Enhanced profitability and risk mitigation Credit limit optimization is critical for credit card issuers aiming to balance growth and risk management. As economic conditions evolve and consumer behaviors shift, the ability to set personalized credit limits will become increasingly important. By leveraging advanced analytics and machine learning, CLO enhances profitability and contributes to a more stable and resilient financial system. One such solution is Experian’s Ascend Intelligence Services™ Limit, which provides an optimized strategy designed to enhance the precision and effectiveness of credit limit assignments. Ascend Intelligence Services™ Limit combines best-in-class bureau data with machine learning to simulate the impact of different credit limits in real time. This capability allows lenders to quickly test and refine their credit limit strategies without the lengthy trial-and-error period traditionally required. Ascend Intelligence Services Limit enables lenders to set credit limits that align with their business objectives and risk tolerance. By providing insights into the likelihood of default and potential revenue for each credit limit scenario, Ascend Intelligence Services Limit helps design optimal limit strategies. This not only maximizes revenue but also minimizes the risk of defaults by ensuring credit limits are appropriate for each customer’s financial situation. In a landscape marked by rising delinquencies and varying regional debt levels, the strategic use of CLO like Ascend Intelligence Services Limit represents a forward-thinking approach to credit management, benefiting both lenders and consumers. Learn More * HOUSEHOLD DEBT AND CREDIT REPORT (Q1 2024) – Federal Reserve Bank of New York

In this article...What is credit card fraud?Types of credit card fraudWhat is credit card fraud prevention and detection?How Experian® can help with card fraud prevention and detection With debit and credit card transactions becoming more prevalent than cash payments in today’s digital-first world, card fraud has become a significant concern for organizations. Widespread usage has created ample opportunities for cybercriminals to engage in credit card fraud. As a result, millions of Americans fall victim to credit card fraud annually, with 52 million cases reported last year alone.1 Preventing and detecting credit card fraud can save organizations from costly losses and protect their customers and reputations. This article provides an overview of credit card fraud detection, focusing on the current trends, types of fraud, and detection and prevention solutions. What is credit card fraud? Credit card fraud involves the unauthorized use of a credit card to obtain goods, services or funds. It's a crime that affects individuals and businesses alike, leading to financial losses and compromised personal information. Understanding the various forms of credit card fraud is essential for developing effective prevention strategies. Types of credit card fraud Understanding the different types of credit card fraud can help in developing targeted prevention strategies. Common types of credit card fraud include: Card not present fraud occurs when the physical card is not present during the transaction, commonly seen in online or over-the-phone purchases. In 2023, card not present fraud was estimated to account for $9.49 billion in losses.2 Account takeover fraud involves fraudsters gaining access to a victim's account to make unauthorized transactions. In 2023, account takeover attacks increased 354% year-over-year, resulting in almost $13 billion in losses.3,4 Card skimming, which is estimated to cost consumers and financial institutions over $1 billion per year, occurs when fraudsters use devices to capture card information from ATMs or point-of-sale terminals.5 Phishing scams trick victims into providing their card information through fake emails, texts or websites. What is credit card fraud prevention and detection? To combat the rise in credit card fraud effectively, organizations must implement credit card fraud prevention strategies that involve a combination of solutions and technologies designed to identify and stop fraudulent activities. Effective fraud prevention solutions can help businesses minimize losses and protect their customers' information. Common credit card fraud prevention and detection methods include: Fraud monitoring systems: Banks and financial institutions employ sophisticated algorithms and artificial intelligence to monitor transactions in real time. These systems analyze spending patterns, locations, transaction amounts, and other variables to detect suspicious activity. EMV chip technology: EMV (Europay, Mastercard, and Visa) chip cards contain embedded microchips that generate unique transaction codes for each purchase. This makes it more difficult for fraudsters to create counterfeit cards. Tokenization: Tokenization replaces sensitive card information with a unique identifier or token. This token can be used for transactions without exposing actual card details, reducing the risk of fraud if data is intercepted. Multifactor authentication (MFA): Adding an extra layer of security beyond the card number and PIN, MFA requires additional verification such as a one-time code sent to a mobile device, knowledge-based authentication or biometric/document confirmation. Transaction alerts: Many banks offer alerts via SMS or email for every credit card transaction. This allows cardholders to spot unauthorized transactions quickly and report them to their bank. Card verification value (CVV): CVV codes, typically three-digit numbers printed on the back of cards (four digits for American Express), are used to verify that the person making an online or telephone purchase physically possesses the card. Machine learning and AI: Advanced algorithms can analyze large datasets to detect unusual patterns that may indicate fraud, such as sudden large transactions or purchases made in different geographic locations within a short time frame. Advanced algorithms can analyze large datasets to detect unusual patterns that may indicate fraud, such as sudden large transactions or purchases made in different geographic locations within a short time frame. Behavioral analytics: Monitoring user behavior to detect anomalies that may indicate fraud. Education and awareness: Educating consumers about phishing scams, identity theft, and safe online shopping practices can help reduce the likelihood of falling victim to credit card fraud. Fraud investigation units: Financial institutions have teams dedicated to investigating suspicious transactions reported by customers. These units work to confirm fraud, mitigate losses, and prevent future incidents. How Experian® can help with card fraud prevention and detection Credit card fraud detection is essential for protecting businesses and customers. By implementing advanced detection technologies, businesses can create a robust defense against fraudsters. Experian® offers advanced fraud management solutions that leverage identity protection, machine learning, and advanced analytics. Partnering with Experian can provide your business with: Comprehensive fraud management solutions: Experian’s fraud management solutions provide a robust suite of tools to prevent, detect and manage fraud risk and identity verification effectively. Account takeover prevention: Experian uses sophisticated analytics and enhanced decision-making capabilities to help businesses drive successful transactions by monitoring identity and flagging unusual activities. Identifying card not present fraud: Experian offers tools specifically designed to detect and prevent card not present fraud, ensuring secure online transactions. Take your fraud prevention strategies to the next level with Experian's comprehensive solutions. Explore more about how Experian can help. Learn More Sources 1 https://www.security.org/digital-safety/credit-card-fraud-report/ 2 https://www.emarketer.com/chart/258923/us-total-card-not-present-cnp-fraud-loss-2019-2024-billions-change-of-total-card-payment-fraud-loss 3 https://pages.sift.com/rs/526-PCC-974/images/Sift-2023-Q3-Index-Report_ATO.pdf 4 https://www.aarp.org/money/scams-fraud/info-2024/identity-fraud-report.html 5 https://www.fbi.gov/how-we-can-help-you/scams-and-safety/common-scams-and-crimes/skimming This article includes content created by an AI language model and is intended to provide general information.

With the advent of AI and ML, optimizing credit prescreen campaigns has never been easier or more efficient.

Check out July's report for a deep dive into the latest market trends, including those around job openings and bankcard delinquency rates.

For car dealers, the holy grail isn't a flashy sports car or a top-selling SUV. It's a simple whisper: "I'm thinking about getting a new car." Imagine if you could hear that murmur from every potential customer walking through your doors, online, or even driving down the street. That's the power of knowing who's in the market for a new car, and it's a game-changer for dealerships. Go beyond the cookie and website tracking and leverage the power of psychographic data and predictive analytics to know who is coming into the market in the next 30, 60, 90 days with the Experian Marketing Engine’s Affinity AutoAudiences. Boost Efficiency and ROI: Targeted Sales: No more shotgun blasts of marketing campaigns! Precisely target consumers considering a new car with personalized offers and incentives. Imagine tailoring financing proposals based on their budget and desired features, not guesswork. Inventory Optimization: Say goodbye to dusty lots filled with unsold models. Knowing market trends and individual preferences allows you to stock in-demand vehicles, maximizing sales and minimizing depreciation costs. Streamlined Sales Process: When a customer walks in already open to buying, the entire process becomes smoother. Focus on addressing their specific needs and preferences, leading to quicker deals and happier customers. Build Stronger Customer Relationships: Proactive Engagement: Instead of waiting for leads, reach out at the perfect moment. A friendly call or email during their research phase demonstrates attentiveness and builds trust, setting you apart from the competition. Personalized Recommendations: Forget one-size-fits-all pitches. Recommend models based on their lifestyle, budget, and driving habits. This shows genuine interest and builds rapport, increasing the likelihood of conversion. Enhanced Customer Experience: Cater to their specific needs before they even step onto the lot. Offer virtual test drives, online financing options, and even home delivery – all tailored to their preferences. This level of personalized service fosters loyalty and repeat business. Leverage the Power of Data: Knowing when a consumer is in the market for a new car isn't just about a head start, it's about building trust, offering convenience, and tailoring the entire experience to their needs. In a competitive market, this inside knowledge is the key to unlocking increased sales, stronger customer relationships, and ultimately, a thriving dealership. So, what are you waiting for? Start listening and turn those whispers into deals! Or

In this blog post, we'll explore skip-tracing best practices, offering valuable insights and practical tips and tools. Read more!

Open Banking use cases are extensive and will continue to expand as access to permissioned data becomes more common. Learn more.

Explore the essentials of identity authentication, its importance for financial institutions, and what effective solutions look like.

Hybrid Registrations Grow Year-Over-Year, Signaling a Shift in Fuel Type Preference

Apply Automotive TagAccording to Experian’s Automotive Market Trends Report: Q1 2024, hybrids accounted for 11.8% of new vehicle registrations, an increase from 8.8% last year.