Latest Posts

Colorado has a great deal to offer first-time homebuyers (FTHBs). While the Denver area attracts many people with its combination of outdoor recreation, culture, and economic opportunities, other parts of Colorado are worthy of attention as well. Take Colorado Springs for example – it ranks third among best places to live in the U.S. when considering lifestyle, the job market, and overall popularity.1 Overview of the Colorado FTHB market Colorado accounts for 2.15% of all U.S. first-time homebuyers, according to Experian Housing’s recent first-time homebuyer report. This figure puts Colorado in the top 20 of all states across the country. Colorado's charm holds a special appeal for younger generations. Known for its wealth of enriching experiences, Colorado naturally attracts adventure-seekers. With an array of outdoor activities like hiking and skiing, it's no wonder that Generation Y and Generation Z make up 75% of all first-time homebuyers in the state, surpassing the national average of ~70%. Affordability With three-quarters of all FTHBs in the younger market segments, affordability is a key consideration in buying a home as housing costs are a significant part of an individual or family’s overall cost of living.2 What determines affordability? Affordability can be assessed through various metrics. For the purposes of this study, Experian Housing defined affordability by calculating the rent-to-mortgage ratio (RTM). This involves comparing monthly rent payments to monthly mortgage payments. A higher rent-to-mortgage ratio suggests renters may find mortgage payments more feasible, potentially making home buying a more appealing option. Comparison of rent costs to mortgage costs What we observed: Based on the RTM ratio, home buying is most affordable in Colorado Springs, Pueblo, and Castle Rock, while renting may look more attractive in Lakewood, Fort Collins, and Arvada. Additional measures to consider: Other realities play a key role in determining what is affordable. A prospective homebuyer’s income, monthly expenses, downpayment funds available, and the cost of the rent or mortgage payment as an added expense against income, factor heavily in final decision-making. In this regard, Experian Housing examined other metrics for assessing affordability. Debt-to-income What we observed: Down payments Sample of CO data observations: (High, mid, low down payments) Sale prices and income What we observed: Experian Housing examined the median sales prices and median incomes across the U.S. This metric is useful to see how much of one’s income typically is going to housing costs in a given area, which again, impacts overall cost of living. Comparison is essential because while sales prices may be higher in a given area, correlation with income helps determine affordability. A closer look at Colorado Springs Colorado Springs ranks #1 in affordability based on Experian’s research, and its status of best affordable place to live considering overall living costs, jobs, and livability is solid.4 The younger generation is the fastest growing population in Colorado Springs. Colorado Springs is expected to be the largest city in the state by 2050 given its current rate of growth and expansion.5 In addition to its five military installations, with a huge U.S. Air Force presence, key job sectors include the larger defense industry, education, technology, and manufacturing. Affordability coupled with opportunity and lifestyle suggest Colorado Springs deserves a closer look and area mortgage lenders have a lot to tout. Experian’s data system offers unique value to lenders given the ability to take a more comprehensive look at a borrower’s financial behavior. Experian uses credit, property, rental, and other alternative data sources to capture the borrower profile. Access to such data also gives Experian a unique ability to conduct research for reports like this one, and the recent reports on Texas and Florida. For more information about the lending possibilities for first-time homebuyers, download our white paper and visit us online. Download white paper Learn more 1 US News & World Report: Best Places to Live in the US 2024-2025 https://realestate.usnews.com/places/rankings/best-places-to-live 2 https://www.experian.com/blogs/insights/top-destinations-for-first-time-homebuyers/ 3 Arvada, Lakewood and Castle Rock, part of the Denver Metro Area and what is popularly known as the Front Range Urban Corridor, also have price to income ratios of 2.8%. 4 https://www.sofi.com/best-affordable-places-to-live-in-colorado/ 5 Colorado Springs Chamber & EDC, coloradospringschamberedc

Call center fraud is a growing threat, and it’s crucial for businesses to take steps to protect their operations and their consumers.

Check out September's report for a deep dive into the latest market trends, including those around job creation and retail sales.

As a mortgage lender, understanding the intricacies of the New York housing market is crucial, especially when dealing with first-time homebuyers (FTHBs). While the housing market fluctuates nationwide, New York presents unique challenges and opportunities that require a nuanced approach. Distinguishing NYC from the rest of New York New York City's housing market, along with its suburbs, stands distinct from the rest of the state. With a high cost of living and unique lifestyle, NYC demands a tailored mortgage marketing strategy. This article will highlight key factors affecting affordability in New York, providing valuable insights for mortgage lenders working in this market. Overview of the New York FTHB market According to Experian Housing’s recent report on first-time homebuyers, the state of New York accounts for nearly 4.9% of all first-time homebuyers nationwide.1 More than half of first-time homebuyers are from Generation Y. When combined with Gen Z, these younger buyers make up just over 67% of the state's FTHBs, a figure slightly below the national average of 69%. Affordability metrics: The rent-to-mortgage ratio For many Americans, homeownership represents stability, security, and the future for family, community, and life. However, the decision to buy versus rent often hinges on affordability. Mortgage lenders must understand this dynamic to better assist their clients. Affordability can be defined in various ways. For the purposes of this study, Experian Housing defined affordability by comparing rental and mortgage payments, known as the rent-to-mortgage ratio (RTM ratio). A higher ratio indicates that buying a home is more economically attractive. Again, this metric does not consider incomes and debt levels, but simply housing rental prices and mortgage costs. Based solely on the RTM ratio, the transition from renting to homeownership may be more attractive in New York City, Syracuse, and Oyster Bay, while the transition may be more difficult in Cheektowaga, Amherst, and Hempstead. For mortgage lenders, understanding local markets and buyer profiles is essential. Building trust through personalized service, such as educating buyers on relevant loan programs and showcasing geographic expertise, can set you apart. With this knowledge, you can help buyers make informed decisions about affordability, whether they prefer living in the city or the suburbs. In some areas, the suburbs may offer more affordable options, while in others, the city center might be more cost-effective. Additional factors: Income, debt, and down payments Affordability extends beyond just rent and mortgage payments. Prospective homebuyers must consider their income, monthly expenses, and access to funds for a down payment. Mortgage lenders need to account for these factors when advising first-time homebuyers. Debt-to-income Average DTI across the 14 cities observed was 25.6%. The chart below highlights those at the higher and lower end of the spectrum. Down payments Down payments varied greatly, but the median across the cities observed was 16.5%. The chart below highlights an example at the high, mid, and low point. Sale prices and income Experian Housing analyzed median sales prices and incomes across the U.S., with New York serving as a prime example of the importance of this comparison in assessing affordability. This correlation is crucial; while sales prices may be high, understanding how they align with local incomes helps lenders accurately gauge market dynamics and guide buyers more effectively. In conclusion, having a deep understanding of the New York housing market is invaluable for mortgage lenders aiming to support first-time homebuyers. By leveraging insights into market dynamics, affordability metrics, and borrower profiles, lenders can offer tailored advice that meets the specific needs of their clients. This not only helps buyers navigate the complexities of homeownership but also builds lasting trust and loyalty. Equipped with these insights, you, as a lender, can play a pivotal role in making the dream of homeownership a reality for first-time buyers in New York. Let's continue to empower our clients with the knowledge and guidance they need to make informed and confident decisions in their homebuying journey. For more insights, check out our recent studies on the Florida and Texas markets and download our first-time homebuyer whitepaper. Download white paper Learn more

Here’s a step-by-step guide on how to create an effective credit union collection strategy. Read on to learn more.

Fraud-as-a-Service (FaaS) represents an emerging and increasingly sophisticated business model within cybercrime. Read more.

Reject inferencing techniques unlock a more comprehensive view of your applicant pool for more informed underwriting decisions.

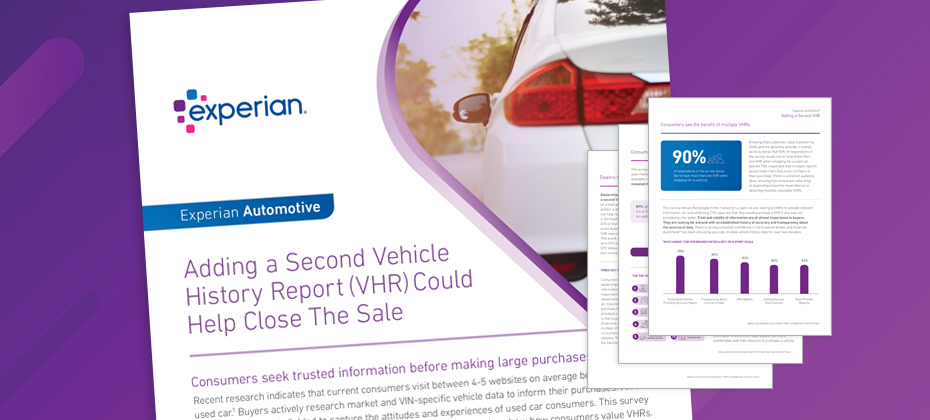

Quick Answer: A new consumer survey reveals that 90% of survey respondents would like to have more than one Vehicle History Report when shopping for a used car. Offering an Experian AutoCheck® VHR as a second Vehicle History Report is a smart, simple strategy to help you close more deals. In today’s used car market, standing out from the crowd is more important than ever. As buyers become savvier and more informed, dealerships need to find new ways to build trust and close sales. One simple yet effective strategy? Offering a second Vehicle History Report (VHR) to your customers. Why VHRs Matter So Much Let’s face it—buying a car is a big deal. Most people don’t just walk onto a lot and pick the first car they see. They do their homework, and a big part of that research involves Vehicle History Reports. In fact, a recent survey found that 70% of people used a VHR the last time they bought a car. And it’s not just a one-time thing—83% of buyers say they’ll use a VHR for their next purchase too. Why? Because these reports provide crucial details like accident history, mileage accuracy, and service records that give buyers confidence in their decisions. The Case for Offering Multiple VHRs Here’s something that might surprise you: 90% of surveyed car buyers said they’d like to see more than one VHR when shopping for a used car. Think about that for a second. People want that extra layer of reassurance that only comes from cross-checking information. This is especially true for those who prefer buying from dealerships—these customers expect comprehensive, reliable data before they make a decision. How Multiple VHRs Can Give Your Dealership an Edge So, what’s the big deal about offering more than one VHR? It’s all about trust and transparency. Just like banks look at multiple credit reports before approving a loan, offering multiple VHRs can help you provide a fuller, more accurate picture of a vehicle’s history. This can reduce your liability and protect your dealership’s reputation. We have done some digging into this, and the results are eye-opening. For instance, in one case study, a dealership found additional damage events through an Experian AutoCheck® VHR that weren’t picked up by other VHRs. This kind of discrepancy shows just how valuable it can be to provide that second report—it helps ensure that all the facts are on the table, which protects both you and your customers. Meeting and Exceeding Customer Expectations Here’s something else to keep in mind: people expect dealerships to go the extra mile. The survey found that 86% of used car buyers believe VHRs should be provided for free by the dealership. By offering multiple reports at no additional cost, you’re not just meeting their expectations—you’re exceeding them. And that’s a surefire way to boost customer confidence, satisfaction, and, ultimately, your sales. What You Can Do Today Offering a second Vehicle History Report is a smart, simple strategy to help you close more deals. It shows your customers that you’re committed to transparency and that you care about providing them with all the information they need to make a confident decision. In a competitive market, it’s the little things like this that can make a big difference. Your customers—and your bottom line—will thank you. Experian Automotive is here to help you with your vehicle history data needs. If you’d like to learn more about our AutoCheck solution and how we can support you, click below to have someone from our team contact you.

Replay attacks are network-based security hacks attackers use to fraudulently gain access to a network or system. Learn more.

Winning with Purpose: My Experience at the FHFA 2024 TechSprint and the Road to ADA Compliance

Apply CIS TagAt Experian, we believe in fostering innovation and collaboration to solve complex challenges. Recently, Ivan Ahmed, one of our talented product management leaders at Experian Housing, had the opportunity to participate in the FHFA 2024 TechSprint, where his team won the award for the best Risk Management and Compliance idea. In this article, we share Ivan's experience as he reflects on the TechSprint, the inspiration behind his team's project, and the valuable lessons learned. Can you share your experience participating in the FHFA 2024 TechSprint? What was the atmosphere like, and how did it feel to be recognized for the best Risk Management and Compliance idea? Let me start by explaining what a TechSprint is. It is a fast-paced, high-energy collaborative workshop where diverse experts and stakeholders come together to design technological solutions to complex problems. Each team is given a high-level problem and use case. From there, stakeholders and domain experts must develop a proof of concept within 3 days to best address the problem. On the last and final day, called the “Demo Day,” teams must showcase their solution in front of a panel of judges. It’s a fun, high-energy, challenging, and rewarding experience. A TechSprint is a convergence of everything I love – technology, business, and design and I think FHFA did a wonderful job orchestrating the event. Each team consisted of representatives from different functions in the housing ecosystem, including lenders, technologists, product managers, and regulators. We were given access to a room, whiteboards, and, most importantly, delicious snacks. We were also given access to industry subject matter experts outside our teams, including representatives from Fannie Mae and Freddie Mac, FHFA, and leaders from top companies. What I found the most impactful was the ability to pressure test our ideas and solutions against these industry subject matter experts. Ideating in a vacuum can be challenging, so being able to stress test things rapidly with these experts allowed us to change course quickly as new information was introduced. Winning the best Risk Management and Compliance idea award was rewarding, especially as we were able to ideate a solution to such a critical accessibility issue. Ultimately, our goal was to help create a fairer, more equitable, and inclusive housing finance system. A big shoutout to my teammates, Wemimo Abbey, Joseph Karbowski, Will Regenauer, and Eddy Atkins. What inspired Team Arsenal to focus on identifying potential gaps in ADA compliance within multifamily buildings, and what were some of the key challenges your team faced during the process? My mother has suffered from several disabilities most of her life. With age, she has become more wheelchair-dependent, and traveling has become a major challenge. On a recent family trip, the entry to our hotel building wasn’t ADA-compliant, and I had to carry her up a flight of stairs. It was frustrating to deal with. I later went down a rabbit hole around ADA compliance and, much to my surprise, learned that only 0.15% of all homes in the U.S. are wheelchair accessible! As we explored the problem space further as a team, we learned how difficult it is to ensure that new and existing rental homes are ADA-compliant. We hypothesized that a solution is needed to establish incentives for borrowers, lenders, and GSEs to meet compliance. A technological solution could more easily enable multi-family lenders and builders to identify rental units that are non-ADA compliant and could provide ways to address the gaps. We noticed two primary challenges: an enforcement gap and an incentive gap. We learned that agency loans (Fannie Mae and Freddie Mac) account for most multi-family home loan originations. If we could tackle the enforcement challenge at the GSE level, we could set up the proper incentives for all players in the multi-family lending process. By providing tools to both the borrower and the GSE’s, we could help foster a more inclusive and accessible rental housing market. How do you envision your AI-driven solution impacting the rental housing market and improving ADA compliance for multifamily buildings? We wanted to ensure that we leveraged the true power of Generative AI, which meant that our solution could take multimodal inputs and produce multimodal outputs. For example, we could train the Generative AI model on photos of interior multi-family rental units and structured or unstructured text like building sketches, site layouts, and local building codes. We could then incorporate ADA design requirements and analyze discrepancies. The result would be a compliance report or tool outlining the adherence level to ADA design requirements and providing tips and recommendations on remediation. The solution could be delivered as a free tool by the GSEs, who could incentivize its usage by offering price concessions to borrowers. Developers could also use the tool to evaluate whether new or existing builds were ADA-compliant. How did your background and experience with Experian contribute to developing your team's winning idea at the FHFA TechSprint? Much of my role at Experian has involved exploring ways to leverage proprietary and public record property data for marketing, account review, and analytical use cases. I work very closely with property data at Experian, so I was very familiar with the types of input fields of property data that would be the most relevant to improving a generative AI model output. Specifically, in our use case, we wanted to train the model to better identify homes and features that were non-compliant with ADA and provide clear remediation steps. We knew that public record property information was available from various sources and could be leveraged as additional third-party input data to improve our model accuracy. What advice would you give to other teams or individuals looking to participate in future TechSprint events, especially those aiming to tackle complex issues like risk management and compliance? It’s important to remember that an ideal solution is both impactful and practical. Practicality is achieved when the solution has both business and technical viability. Therefore, it’s crucial to carefully vet problems and solutions by understanding their viability. Working as a team to solve the problem means leveraging the expertise of subject matter experts around you. Each team member should draw on their strengths, making the collective effort stronger than individual contribution. Most importantly, fairness, inclusivity, and accessibility matter. An effective solution should strive to have a positive social impact in addition to other considerations. Winning with purpose Ivan’s journey through the FHFA 2024 TechSprint exemplifies the innovative and collaborative spirit that drives our team at Experian. His reflections highlight the impact of well-designed technological solutions on critical issues like ADA-compliance in multifamily housing. We hope Ivan’s experience inspires others to explore their potential in solving complex problems and to participate in future TechSprints, where innovative thinking and a commitment to social good can lead to meaningful change.

The Growing Appetite for Leasing: Understanding the Shift in Consumer Preference

Apply Automotive TagDriven by a range of appealing factors including lower monthly payments and a wider array of models—due to the continuous rise in new vehicle inventory—leasing has reappeared as an optimal choice for consumers who are in the market for a vehicle. According to Experian’s State of the Automotive Finance Market Report: Q2 2024, leasing increased to 25.35%, up from 21.14% in Q2 2023 and 19.30% the year prior. While the average monthly payment and interest rate for a new loan modestly increased year-over-year, leasing is increasingly becoming a more attractive option for those leaning towards flexibility and affordability. For example, the average monthly payment on a leased vehicle was $148 less than a loan this quarter. What’s more, it seems consumers are leaning towards larger vehicles. For instance, the Honda CR-V (2.98%) continued to lead the top leased models in Q2 2024, and it was followed closely by the Tesla Model Y (2.61%). Rounding out the top five were the Honda Civic (2.29%), Ford F-150 (2.02%), and Chevrolet Silverado 1500 (1.86%). Prime financing grows and lease payments decline across all segments When looking at risk distribution trends in Q2 2024, prime consumers accounted for nearly 70% of the total finance market—with prime coming in at 37.82%, down from 39.84% last year and super prime increasing from 28.98% to 31.59% year-over-year. Subprime also saw a slight increase, going from 13% to 13.06% during the same period. It’s notable that all risk segments experienced a decrease in average monthly payments for leased vehicles, as super prime went from $601 in Q2 2023 to $586 in Q2 2024, prime declined to $583 this quarter, from $596 last year, and subprime was at $597, from $611. With the average monthly payments declining year-over-year for majority of shoppers, it can potentially create a more competitive market and drive more consumers towards this finance option—something automotive professionals should keep a close eye on. New and used vehicle finance market overview Data in Q2 2024 found that new vehicle loan amounts increased slightly, reaching $40,927, up from $40,743 last year, and the average interest rate went from 6.78% to 6.84% year-over-year. Despite the increases, the average monthly payment for a new vehicle only experienced a $1 growth to $734 this quarter. On the used side, the average loan amount declined from $27,316 Q2 2023 to $26,248 in Q2 2024, and the average rate grew from 11.47% to 12.01% in the same time frame. Though, the average monthly payment declined to $525 this quarter, from $536 last year. As the automotive industry continues to adapt to the changing market conditions and consumer preferences, it’s important for professionals to leverage the most current data—this will allow them to effectively assist consumers by meeting their financial needs with the available options. To learn more about automotive finance trends, view the full State of the Automotive Finance Market: Q2 2024 presentation on demand.

Voter registration lists are the backbone of our democratic process. However, maintaining accurate and up-to-date lists is a challenge that election agencies constantly face. With several regulations related to voting and election integrity that have been enacted or proposed in the last two years, maintaining a quality voter list is more important now than ever before. Election officials now have a powerful tool at their disposal: commercially available data to enhance voter list maintenance and boost voter confidence. The importance of maintaining voter lists Audit teams within election agencies are tasked with ensuring election integrity through voter list maintenance. These teams need reliable tools to: Verify and correct voter registration data Identify and update contact information Provide a cost-effective method for record updates Reduce election costs for taxpayers Success stories in voter list management Case study: West Virginia Secretary of State The West Virginia Secretary of State (WVSOS) uses Experian’s TrueTrace™ solution to enhance voter roll maintenance. Traditionally a skip-tracing solution for debt collectors, TrueTrace leverages unique data sources to ensure voters receive correct information, reducing wasted resources and improving election efficiency. WVSOS was challenged with enhancing their existing processes to a more robust 50-state comparison for cross-state movers. After WVSOS’s first data pull using TrueTrace, nearly 16,000 individuals were identified with a potential new "best" address that were also not flagged by other data comparison programs used by the state. The results? Of the almost 16,000 mailings sent, about 25% returned were undeliverable, confirming those individuals had moved. Access the full case study to discover best practices for maintaining voter rolls and conducting cost-effective elections. Webinar: El Paso County Clerk & Recorder's Office The El Paso County Clerk & Recorder’s Office was looking to bring transparency, efficiency, and increased voter confidence to the elections in El Paso County, Texas. To achieve this, they required verified enriched data for registered voters. By partnering with Experian, voter data was enriched using our TrueTrace solution. This partnership has enabled the Office to verify and append the most up-to-date voter address, leading to significant improvements in list maintenance. To date, the El Paso County Clerk & Recorder’s Office has seen a reduction of more than $39,860 in undeliverable ballot costs. Their ROI to date is a positive $4,537 back to the citizens of El Paso County. Listen to our on-demand webinar to hear more about this collaboration. Visit us online to learn more about our public sector solutions. Learn more

Learn about the state of housing affordability in Florida and how you can attract first-time homebuyers here.

Check out August's report for a deep dive into the latest market trends, including those around originations and the new housing market.

Cashflow underwriting is a modern approach to evaluating creditworthiness, giving lenders a greater view into one's financial situation.