Latest Posts

Offering identity theft protection is an effective way to maintain strong customer relationships and deliver an engaging experience.

Cris Ryan, Go to Market Lead for Experian Identity and Fraud, shares his thoughts on demand deposit account fraud and how to combat it.

Future-proof your business and safeguard your customers with fraud detection leveraging machine learning solutions.

Learn how expanded data, AI-driven models, and increased automation can help you enhance your credit risk management strategies.

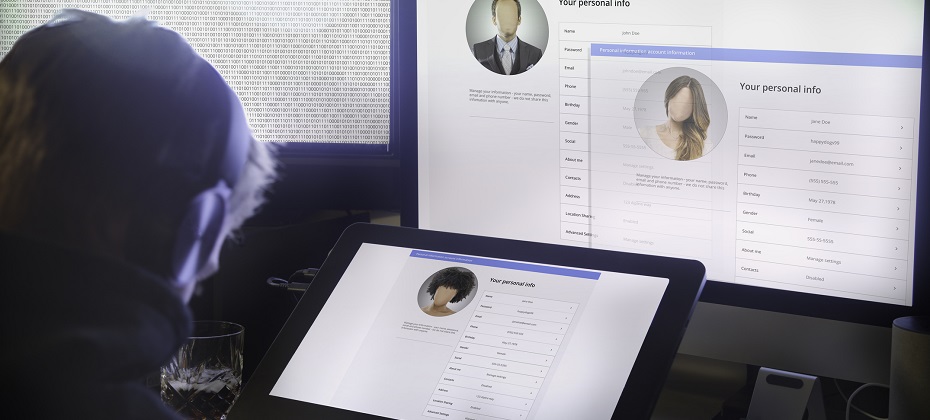

Sometimes logging into an account feels a bit like playing 20 questions. Security is vital for a positive customer experience, and engaging the right identity verification strategies is essential to proactive fraud prevention. For financial institutions and businesses, secure authentication is more important than ever. It is imperative for customer safety – which drives retention and loyalty – and your bottom line – as fraud has determinantal effects on and off the balance sheet. Information sharing has proliferated, as has the number of times consumers are prompted to provide access to sensitive information. While today’s consumer has grown accustomed to providing such information, there’s also a heightened demand for security. According to Experian’s 2023 U.S. Identity and Fraud Report, nearly two-thirds (64%) of consumers say they’re very or somewhat concerned with online safety, listing identity theft, stolen card information and online privacy as top concerns. Customers want to know who they are providing access to and whether that entity will have their safety in mind. From a business perspective, one way to ensure that only the right people can get in is by using (KBA). KBA takes traditional authentication methods, like passwords and Personal Identification Numbers (PINs), one step further by creating an additional layer of security through collecting private facts from each user. In this post, we'll look at how KBA works, what its benefits are as a form of identity verification, and how it can improve customer trust. Introducing Knowledge Based Authentication (KBA): What it is and how it works Knowledge Based Authentication can be part of a multifactor authentication solution and is one way to stay on top of privacy and security for your customers – existing and new. KBA is a feature designed to protect online accounts by verifying the account holder’s identity. It involves answering a series of personal questions, such as mother's maiden name or first pet's name, that only the account holder should know. This system has become increasingly popular due to its effectiveness in preventing fraud and identity theft. With KBA, businesses and individuals can have peace of mind that their information is protected by a reliable authentication system that is difficult for unauthorized users to breach. Benefits of implementing KBA and a multifactor authentication strategy By implementing KBA into your business, customers experience an additional layer of security by verifying the identity of users through personalized questions. This reduces the risk of fraud and enhances customer trust and confidence. Secondly, it improves the customer experience by making the authentication process faster and user-friendly. Lastly, KBA reduces costs by automating the authentication process and reducing the need for manual intervention. However, KBA is just one facet of an ideal strategy. Multifactor authentication provides confidence while reducing friction. Risk-based authentication tools allow organizations to assess risk to apply the appropriate level of security. Factors to consider adding to your authentication processes include: Generating unique one-time passwords (OTPs): By creating a new OTP for each transaction, you can increase the level of security. Confirm device ownership: A multifactored approach applies device intelligence checks to increase confidence that the message is reaching the correct user. Maintain low friction with secondary options: If the OTP fails or can’t be attempted by the user, working with a provider who allows an automatic default to another authentication service, such as a knowledge-based authentication solution, decreases end-user friction. Identifying potential security risks associated with KBA KBA relies on personal information that may easily be discovered via social media and other public records, which makes it vulnerable to fraud and identity theft. This highlights the need for a multilayered fraud and identity solution. The landscape of digital security is constantly changing, leveraging an arsenal of fraud and identity prevention strategies, like document verification, one-time passcode, and various identity authentication and verification measures, is critical for keeping your customers and business safe. Commonly used technologies for enhancing KBA security With the rising need for secure authentication, KBA systems have become increasingly popular. However, cyberthreats evolve at an alarming rate, making it imperative to stay current with the latest fraud schemes and how to enhance and supplement your security. Biometrics, like facial recognition and fingerprint scans, as a tactic is gaining traction, as evidenced by “85% of consumers report physical biometrics as the most trusted and secure authentication method they have recently encountered,” according to Experian’s 2023 U.S. Identity and Fraud Report. Additionally, machine learning algorithms detect patterns and anomalies in user behavior and flag any potential security breaches. Multi-factor authentication is another tool that adds an extra layer of security by requiring users to provide multiple forms of identification before logging in. Keeping up with these and other technological advancements can help ensure your KBA system stays one step ahead of potential cyberattacks. Interestingly, there’s a disconnect between the technologies consumers feel safe with and/or are prepared to use versus the technologies and strategies that organizations implement. According to the U.S. Identity and Fraud Report, biometrics are only currently used by 33% of businesses to detect and protect against fraud. An opportunity for business differentiation and driving customer loyalty through a better customer experience may be tapping into some of these lesser used – but sought after – technologies. Compliance with industry standards regarding KBA Ensuring that your system complies with industry standards regarding KBA is crucial for protecting sensitive information from unauthorized access. By implementing the following tips, you can stay ahead of the game and safeguard your organization's data. Analyze your system's current authentication methods and evaluate if they meet industry standards. Additionally, follow standard guidelines for data storage and encryption, limit access to only authorized personnel, and y current with regulations. Lastly, conduct frequent security audits and perform vulnerability tests to identify and address any potential threats. Knowledge-based authentication offers a robust security solution for businesses of all sizes, and incorporating KBA as part of a multifactor authentication strategy is a winning course of action. It provides an added layer of protection for personal data, encourages user accountability, and safeguards against unauthorized access. By leveraging appropriate KBA technologies and maintaining compliance with industry standards, it is possible to create a secure system for customers that gives you peace of mind for your business and bottom line. Experian can help you with knowledge-based authentication offerings, a multifactor authentication strategy and everything in between to enhance your existing authentication process without causing user fatigue. Increase your pass rates, confirm device ownership and add security to risky or high-value transactions, all while executing identity verification and fraud detection to protect your business from risk. The most important step is getting started. Learn more

According to Experian’s State of the Automotive Finance Market Report: Q3 2023, the average new vehicle loan amount decreased to $40,184, from $41,543 in Q3 2022 and the average used vehicle loan amount went from $28,684 to $27,167 year-over-year.

Learn how a well-designed underwriting strategy can help you drive growth and create more value out of your member relationships.

Learn about travel, hospitality and hotel fraud and how you can best detect and combat it. Read more here!

If you’re a manager at a business that lends to consumers or otherwise extends credit, you certainly are aware that 10-15% of your current customers and prospective future customers are among the approximately 27 million consumers who are now – or will soon be -- fitting another bill into their monthly budgets. Early in the COVID-19 pandemic, the government issued a pause on federal student loan payments and interest. Now that the payment pause has expired, millions of Americans face a new bill averaging more than $200. Will they pay you first? If this is your concern, you aren’t alone: Experian recently held a webinar that discussed how the end of the student loan pause might affect businesses. When we surveyed the webinar attendees, nearly 3 out of 4 responses included Risk Management as a main concerns now. Another top concern is about credit scores. Lenders and investors use credit scores – bureau scores such FICO® or VantageScore® credit score or custom credit scores proprietary to their institution – to predict credit default risk. The risk managers at those companies want to know to what extent they can continue to rely on those scores as Federal student loan payments come due and consumers experience payment shock. I’ve analyzed a large and statistically meaningful sample (10% of the US consumer population in Experian’s Ascend Sandbox) to shed some light on that question. As background information, the average consumer with student loans had lower scores before the pandemic than the average of the general population. One of my Experian colleagues has explored some of the reasons at https://www.experian.com/blogs/ask-experian/research/average-student-loan-payments). Here are some of the things we can learn from comparing the credit data of the two groups of people. I looked at a period from 2019 and from 2023 to see how things have changed: Average credit scores increased during the pandemic, continuing a long-term trend during which more Americans have been willing and able to meet all their obligations. During the COVID Public Health Emergency, consumers with student loans brought up their scores by an average of 25 points; that was 7 points more than consumers without student loans. Another way to look at it: in 2019, consumers with student loans had credit scores 23 points lower than consumers without. By 2023, that difference had shrunk to 16 points. Experian research shows that there will be little immediate impact on credit scores when the new bills come due. Time will tell whether these increased credit scores accurately reflect a reduction in the risk that consumers will default on other bills such as auto loans or bankcards soon, even as some people fit student loan bills into their budgets. It is well-known that many people saved money during the public health emergency. Since then, the personal savings rate has fallen from a pandemic high of 32% to levels between 3% and 5% this year – lower than at any point since the 2009 recession. In an October 2023 Experian survey, only 36% of borrowers said they either set aside funds or they planned using other financial strategies specifically for the resumption of their student loan payments. Additional findings from that study can be found here. Furthermore, there are changes in the way your customers have used their credit cards over the last four years: Consumers’ credit card balances have increased over the last four years. Consumers with student loans have balances that are on average $282 (4%) more now than in 2019. That is a significantly smaller increase than for consumers without student loans, whose total credit card debt increased by an average of $1,932 (26%). Although their balances increased, the ratio of consumers’ total revolving debt balances to their credit limits (utilization) changed by less than 1% for both consumers with student loans and consumers without. In 2019, the utilization ratio was 9.8 percentage points lower for consumers with student loans than consumers without. Four years later, the difference is nearly the same (9.6 points). We can conclude that many student loan borrowers have been very responsible with credit during the Public Health Emergency. They may have been more mindful of their credit situation, and some may have planned for the day when their student loan payments will be due. As the student loan pause come to an end, there are a few things that lenders and other businesses should be doing to be ready: Even if you are not a student loan lender, it is important to stay on top of the rapidly evolving student loan environment. It affects many of your customers, and your business with them needs to adapt. Anticipate that fraudsters and abusers of credit will be creative now: periods of change create opportunities for them and you should be one step ahead. Build optimized strategies in marketing, account opening, and servicing. Consider using machine learning to make more accurate predictions. Those strategies should reflect trends in payments, balances, and utilization; older credit scores look at a single point in time. Continually refresh data about your customers—including their credit scores and important attributes related to payments, balances, and utilization patterns. Look for alternative data that will give you a leg up on the competition. In the coming weeks and months, Experian’s data scientists will monitor measures of performance of the scores and attributes that you depend on in your data-driven strategies — particularly focusing on the Kolmogorov-Smirnov (KS) statistics that will show changes in the predictive power of each score and attribute. (If you are a data-driven business, your data science team or a trusted partner should be doing the same thing with a more specific look at your customer base and business strategies.) In future reports and blog posts, we’ll shed light on the impact student loans are having on your customers and on your business. In the meantime, for more information about how to use data and advanced analytics to grow while controlling costs and risks, all while staying in compliance and providing a good customer experience, visit our website.

Our State of Alternative Data Report provides insight into the alternative lending market, new data sources and growth opportunities.

Lemon vehicle history is a serious issue that can have a significant impact on the automotive industry. Buying a vehicle that is branded as a lemon may harm a dealership or the OEM's reputation. Customers may be less likely to buy automobiles from that manufacturer or dealership in the future if they learn the vehicle they bought was branded a lemon. Used vehicles with lemon vehicle history has implications Furthermore, automakers may incur higher costs as the expense of buying back and fixing lemon vehicles is frequently the responsibility of the auto manufacturers. Finally, the used automobile market may be impacted by a vehicle's lemon history. Used cars with lemon vehicle history events are frequently worth less than equivalent autos without such activity. New lemon-reported events analysis infographic available View our most recent Vehicle Insights Infographic Report: Lemon Reported Events Data Analysis. You’ll learn more about lemon-reported activity for vehicles, what percentage of owners repurchase a different vehicle after the initial reported activity, and how many vehicles with the lemon event history are still on the road. We have a series of vehicle insight infographic reports you may also be interested in: Water and Flood Reported Events Vehicle Accident and Damage Insights

The gig economy — also called the sharing economy or access economy — is an activity where people earn income by providing on-demand work, services, or goods. Often, it is through a digital platform like an application (app) or website. The gig economy seamlessly connects individuals with a diverse range of services, whether it be a skilled handyman for those long-awaited office shelves, or an experienced chauffeur to quickly drive you to the airport to not miss your flight. However, there are instances when these arrangements fall short of expectations. The hired handyman may send a substitute who’s ill-equipped for the task, or the experienced driver takes the wrong shortcut leaving you scrambling to make your flight on time. On the flip side, there are numerous risks faced by those working in the gig/sharing economy, from irritable customers to dangerous situations. In such cases, trust takes a hit. The gig economy has witnessed a surge in recent years, as individuals gravitate towards flexible, freelance, and contract work instead of traditional full-time employment. This shift has unlocked a multitude of opportunities for both workers and businesses. Nevertheless, it has also ushered in challenges pertaining to security and trust. One such challenge revolves around the escalating significance of digital identity verification within the gig economy. Digital identity verification and the gig economy Digital identity verification encompasses validating a person's identity through digital means, such as biometric data, facial recognition, or document verification. Within the gig economy, this process has high importance, as it establishes trust between businesses and their pool of freelance or contract workers. With the escalating number of remote workers and the proliferation of online platforms connecting businesses with gig workers, verifying the identities of these individuals has become more vital than ever before. Protecting gig users and improving the customer experience One primary rationale behind the mounting importance of digital identity verification in the gig economy is its role in curbing fraud. As the gig economy gains traction, the risk of individuals misrepresenting themselves or their qualifications to secure work burgeons. This scenario can lead businesses to hire unqualified or even fraudulent workers, thereby posing severe repercussions for both the company and its customers. By adopting digital identity verification processes, businesses can ensure the legitimacy and competence of their workforce, subsequently decreasing the risk of fraudulent activities. In the digital age, trust and safety are crucial for businesses to succeed. Consumers prioritize brands they can trust, and broken trust can lead to loss of customers.According to Experian's 2023 Fraud and Identity Report, over 52% of US consumers feel they’re more of a target for online fraud than they were a year ago. As such, online security continues to be a real concern for most consumers. Nearly 64% of consumers say that they are very or somewhat concerned with online security, with 32% saying they are very concerned. Establishing trust and safety measures not only protects your brand but also enhances the user experience, fosters loyalty, and boosts your business. Role of a dedicated Trust and safety team Trust and safety are the set of business practices for online platforms to follow to reduce the risk of users being exposed to harm, fraud, or other behaviors outside community guidelines. This is becoming an increasingly important function as online platforms look to protect their users while improving customer acquisition, engagement, and retention. That team also safeguards organizations from security threats and scams. They verify customers' identities, evaluate actions and intentions, and ensure a safe environment for all platform users. This enables both organizations and customers to trust each other and have confidence in the platform. Their role has evolved from fraud prevention to encompass broader areas, such as user-generated content and the metaverse. With the rise of user-generated content, platforms face challenges like fake accounts, imitations, malicious links, and inappropriate content. As a result, trust and safety teams have expanded their focus and are involved in product engineering and customer journey design. Another noteworthy factor contributing to the growing emphasis on digital identity verification for trust and safety teams stems from the necessity to adhere to diverse regulations and laws. Many countries have implemented stringent regulations to safeguard workers and ensure the legal and ethical operations of businesses. In the United States, for instance, businesses must verify the identities and work eligibility of all employees, including freelancers and contractors, as part of the Form I-9 process. By leveraging digital identity verification tools, businesses can streamline these procedures and guarantee compliance with prevailing regulations. Mitigating risk in online marketplaces To mitigate risks in online marketplaces, businesses can take several steps, including creating a clear set of user guidelines, implementing identity verification during onboarding, enforcing multi-factor authentication for all accounts, leveraging reverification during high-risk moments, performing link analysis on the user base, and applying automation. Online identity verification plays a pivotal role in safeguarding gig workers themselves. With the surge of online platforms connecting businesses with freelancers and contractors, there comes an augmented risk of workers falling prey to scams or identity theft. By mandating digital identity verification as an integral part of the onboarding process, these platforms can shield workers and ensure they only engage with bona fide businesses. While automation can be a powerful tool for fraud detection and mitigation, it is not a cure-all solution. Automated identity verification has its strengths, but it also has its weaknesses. While automation can spot risk signals that a human might miss, a human might spot risk signals that automation would have skipped. Therefore, for many companies, the goal should not be full automation but achieving the right ratio of automation to manual review. Manual review takes time, but it's necessary to ensure that all potential risks are identified and addressed. The more efficient these processes can be, the better, as it allows for a quicker response to potential threats. As the number of individuals embracing freelance and contract work surges, and businesses increasingly rely on these workers to carry out vital responsibilities, ensuring the security and trustworthiness of these individuals becomes paramount. By integrating digital identity verification processes, businesses can shield themselves against fraud, comply with regulations, and cultivate trust with their gig workers. Finding the right partner While trust and safety are concerns for all online marketplaces, there’s no universal solution that will apply to all businesses and in all cases. Your trust and safety policies need to be tailored to the realities of your business. The industries you serve, regions you operate in, regulations you are subject to, and expectations of your users should all inform your processes. Experian’s comprehensive suite of customizable identity verification solutions can help you solve the problem of trust and safety once and for all. Learn more *This article leverages/includes content created by an AI language model and is intended to provide general information.

By powering your deposit growth strategy with fresh consumer insights, you can find the best customers and members to engage.

With great risk comes great reward, as the saying goes. But when it comes to business, there's huge value in reducing and managing that risk as much as possible to maximize benefits — and profits. In today's high-tech strategic landscape, financial institutions and other organizations are increasingly using risk modeling to map out potential scenarios and gain a clearer understanding of where various paths may lead. What is a risk model? A risk model is a representation of a particular situation that's created specifically for the purpose of assessing risk. That risk model is then used to evaluate the potential impacts of different decisions, paths and events. From assigning interest rates and amortization terms to deciding whether to begin operating in a new market, risk models are a safe way to analyze data, test assumptions and visualize potential scenarios. Risk models are particularly valuable in the credit industry. Credit risk models and credit risk analytics allow lenders to evaluate the pluses and minuses of lending to clients in specific ways. They are able to consider the larger economic environment, as well as relevant factors on a micro level. By integrating risk models into their decision-making process, lenders can refine credit offerings to fit the assessed risk of a particular situation. It goes like this: a team of risk management experts builds a model that brings together comprehensive datasets and risk modeling tools that incorporate mathematics, statistics and machine learning. This predictive modeling tool uses advanced algorithmic techniques to analyze data, identify patterns and make forecasts about future outcomes. Think of it as a crystal ball, but with science behind it. Your team can then use this risk model for a wide range of applications: refining marketing targets, reworking product offerings or reshaping business strategies. How can risk models be implemented? Risk models consolidate and utilize a wide variety of data sets, historical benchmarks and qualitative inputs to model risk and allow business leaders to test assumptions and visualize the potential results of various decisions and events. Implementing risk modeling means creating models of systems that allow you to adjust variables to imitate real-world situations and see what the results might be. A mortgage lender, for example, needs to be able to predict the effects of external and internal policies and decisions. By creating a risk model, they can test how scenarios such as falling interest rates, rising unemployment or a shift in loan acceptance rates might affect their business, and make moves to adjust their strategies accordingly. One aspect of risk modeling that can't be underestimated is the importance of good data, both quantitative and qualitative. Efforts to implement or expand risk modeling should begin with refining your data governance strategy. Maximizing the full potential of your data also requires integrating data quality solutions into your operations in order to ensure that the building blocks of your risk model are as accurate and thorough as possible. It's also important to ensure your organization has sufficient model risk governance in place. No model is perfect, and each comes with its own risks. But these risks can be mitigated with the right set of policies and procedures, some of which are part of regulatory compliance. With a comprehensive model risk management strategy, including processes like back testing, benchmarking, sensitivity analysis and stress testing, you can ensure your risk models are working for your organization — not opening you up to more risk. How can risk modeling be used in the credit industry? Risk modeling isn't just for making credit decisions. For instance, you might model the risk of opening or expanding operations in an underserved country or the costs and benefits of an existing one that is underperforming. In information technology, a critical branch of virtually every modern organization, risk modeling helps security teams evaluate the risk of malicious attacks.Banking and financial services is one industry for which understanding and planning for risk is key, not only for business reasons but to align with relevant regulations. The mortgage lender mentioned above, for example, might use credit risk models to better predict risk, enhance the customer journey and ensure transparency and compliance.It's important to highlight that risk modeling is a guide, not a prophecy. Datasets can contain flaws or gaps, and human error can happen at any stage. It's also possible to rely too heavily on historical information, and while they say history repeats itself, they don't mean it repeats exactly. That's especially true in the face of novel challenges, such as the rise of artificial intelligence. Making the best use of risk modeling tools involves not just optimizing software and data but using expert insight to interpret predictions and recommendations so that decision-making comes from a place of breadth and depth. Why are risk models important for banks and financial institutions? In the world of credit, optimizing risk assessment has clear ramifications when meeting overall business objectives. By using risk modeling to better understand your current and potential clients, you are positioned to offer the right credit products to the right audience and take action to mitigate risk. When it comes to portfolio risk management, having adequate risk models in place is paramount to meet targets. And not only does implementing quality portfolio risk analytics help maximize sales opportunities, but it can also help you identify risk proactively to avoid costly mistakes down the road. Risk mitigation tools are a key component of any risk modeling strategy and can help you maintain compliance, expose potential fraud, maximize the value of your portfolio and create a better overall customer experience. Advanced risk modeling techniques In the realm of risk modeling, the integration of advanced techniques like machine learning (ML) and artificial intelligence (AI) is revolutionizing how financial institutions assess and manage risk. These technologies enhance the predictive power of risk models by allowing for more complex data processing and pattern recognition than traditional statistical methods.Machine learning in risk modeling: ML algorithms can process vast amounts of unstructured data – such as market trends, consumer behavior and economic indicators — to identify patterns that may not be visible to human analysts. For instance, ML can be used to model credit risk by analyzing a borrower’s transaction history, social media activities and other digital footprints to predict their likelihood of default beyond traditional credit scoring methods.Artificial intelligence in decisioning: AI can automate the decisioning process in risk management by providing real-time predictions and risk assessments. AI systems can be trained to make decisions based on historical data and adjust them as they learn from new data. This capability is particularly useful in credit underwriting where AI algorithms can make rapid decisions based on market conditions.Financial institutions looking to leverage these advanced techniques must invest in robust data infrastructure, skilled personnel who can bridge the gap between data science and financial expertise, and continuous monitoring systems to ensure the models perform as expected while adhering to regulatory standards. Challenges in risk model validation Validating risk models is crucial for ensuring they function appropriately and comply with regulatory standards. Validation involves verifying both the theoretical foundations of a model and its practical implementation. Key challenges in model validation Model complexity: As risk models become more complex, incorporating elements like ML and AI, they become harder to validate. Complex models can behave in unpredictable ways, making it difficult to understand why they are making certain decisions (the so-called "black box" issue).Data quality and availability: Effective validation requires high-quality, relevant data. Issues with data completeness, accuracy or relevance can lead to incorrect model validations. Best practices in model validation Regulatory compliance: With regulations continually evolving, maintaining compliance with risk models can be challenging. Different jurisdictions may have varying requirements, further complicating validation processes.Regular reviews: Continuous monitoring and periodic reviews help ensure that models remain accurate over time and adapt to changing market conditions.Third-party audits: Independent reviews by external experts can provide an unbiased assessment of the risk model’s performance and compliance.These practices help institutions maintain the reliability and integrity of their risk models, ensuring that they continue to function as intended and comply with regulatory requirements. How Experian can help Risk is inherent to business, and there's no avoiding it entirely. But integrating credit risk modeling into your operations can ensure stability and profitability in a rapidly evolving business landscape. Start with Experian's credit modeling services, which use expansive data, analytical expertise and the latest credit risk modeling methodologies to better predict risk and accelerate growth. Learn more

Automated debt collection can help you save time and money while increasing customer satisfaction and long-term values.