Latest Posts

Winning with Purpose: My Experience at the FHFA 2024 TechSprint and the Road to ADA Compliance

Apply FSD TagAt Experian, we believe in fostering innovation and collaboration to solve complex challenges. Recently, Ivan Ahmed, one of our talented product management leaders at Experian Housing, had the opportunity to participate in the FHFA 2024 TechSprint, where his team won the award for the best Risk Management and Compliance idea. In this article, we share Ivan's experience as he reflects on the TechSprint, the inspiration behind his team's project, and the valuable lessons learned. Can you share your experience participating in the FHFA 2024 TechSprint? What was the atmosphere like, and how did it feel to be recognized for the best Risk Management and Compliance idea? Let me start by explaining what a TechSprint is. It is a fast-paced, high-energy collaborative workshop where diverse experts and stakeholders come together to design technological solutions to complex problems. Each team is given a high-level problem and use case. From there, stakeholders and domain experts must develop a proof of concept within 3 days to best address the problem. On the last and final day, called the “Demo Day,” teams must showcase their solution in front of a panel of judges. It’s a fun, high-energy, challenging, and rewarding experience. A TechSprint is a convergence of everything I love – technology, business, and design and I think FHFA did a wonderful job orchestrating the event. Each team consisted of representatives from different functions in the housing ecosystem, including lenders, technologists, product managers, and regulators. We were given access to a room, whiteboards, and, most importantly, delicious snacks. We were also given access to industry subject matter experts outside our teams, including representatives from Fannie Mae and Freddie Mac, FHFA, and leaders from top companies. What I found the most impactful was the ability to pressure test our ideas and solutions against these industry subject matter experts. Ideating in a vacuum can be challenging, so being able to stress test things rapidly with these experts allowed us to change course quickly as new information was introduced. Winning the best Risk Management and Compliance idea award was rewarding, especially as we were able to ideate a solution to such a critical accessibility issue. Ultimately, our goal was to help create a fairer, more equitable, and inclusive housing finance system. A big shoutout to my teammates, Wemimo Abbey, Joseph Karbowski, Will Regenauer, and Eddy Atkins. What inspired Team Arsenal to focus on identifying potential gaps in ADA compliance within multifamily buildings, and what were some of the key challenges your team faced during the process? My mother has suffered from several disabilities most of her life. With age, she has become more wheelchair-dependent, and traveling has become a major challenge. On a recent family trip, the entry to our hotel building wasn’t ADA-compliant, and I had to carry her up a flight of stairs. It was frustrating to deal with. I later went down a rabbit hole around ADA compliance and, much to my surprise, learned that only 0.15% of all homes in the U.S. are wheelchair accessible! As we explored the problem space further as a team, we learned how difficult it is to ensure that new and existing rental homes are ADA-compliant. We hypothesized that a solution is needed to establish incentives for borrowers, lenders, and GSEs to meet compliance. A technological solution could more easily enable multi-family lenders and builders to identify rental units that are non-ADA compliant and could provide ways to address the gaps. We noticed two primary challenges: an enforcement gap and an incentive gap. We learned that agency loans (Fannie Mae and Freddie Mac) account for most multi-family home loan originations. If we could tackle the enforcement challenge at the GSE level, we could set up the proper incentives for all players in the multi-family lending process. By providing tools to both the borrower and the GSE’s, we could help foster a more inclusive and accessible rental housing market. How do you envision your AI-driven solution impacting the rental housing market and improving ADA compliance for multifamily buildings? We wanted to ensure that we leveraged the true power of Generative AI, which meant that our solution could take multimodal inputs and produce multimodal outputs. For example, we could train the Generative AI model on photos of interior multi-family rental units and structured or unstructured text like building sketches, site layouts, and local building codes. We could then incorporate ADA design requirements and analyze discrepancies. The result would be a compliance report or tool outlining the adherence level to ADA design requirements and providing tips and recommendations on remediation. The solution could be delivered as a free tool by the GSEs, who could incentivize its usage by offering price concessions to borrowers. Developers could also use the tool to evaluate whether new or existing builds were ADA-compliant. How did your background and experience with Experian contribute to developing your team's winning idea at the FHFA TechSprint? Much of my role at Experian has involved exploring ways to leverage proprietary and public record property data for marketing, account review, and analytical use cases. I work very closely with property data at Experian, so I was very familiar with the types of input fields of property data that would be the most relevant to improving a generative AI model output. Specifically, in our use case, we wanted to train the model to better identify homes and features that were non-compliant with ADA and provide clear remediation steps. We knew that public record property information was available from various sources and could be leveraged as additional third-party input data to improve our model accuracy. What advice would you give to other teams or individuals looking to participate in future TechSprint events, especially those aiming to tackle complex issues like risk management and compliance? It’s important to remember that an ideal solution is both impactful and practical. Practicality is achieved when the solution has both business and technical viability. Therefore, it’s crucial to carefully vet problems and solutions by understanding their viability. Working as a team to solve the problem means leveraging the expertise of subject matter experts around you. Each team member should draw on their strengths, making the collective effort stronger than individual contribution. Most importantly, fairness, inclusivity, and accessibility matter. An effective solution should strive to have a positive social impact in addition to other considerations. Winning with purpose Ivan’s journey through the FHFA 2024 TechSprint exemplifies the innovative and collaborative spirit that drives our team at Experian. His reflections highlight the impact of well-designed technological solutions on critical issues like ADA-compliance in multifamily housing. We hope Ivan’s experience inspires others to explore their potential in solving complex problems and to participate in future TechSprints, where innovative thinking and a commitment to social good can lead to meaningful change.

The Growing Appetite for Leasing: Understanding the Shift in Consumer Preference

Apply Automotive TagDriven by a range of appealing factors including lower monthly payments and a wider array of models—due to the continuous rise in new vehicle inventory—leasing has reappeared as an optimal choice for consumers who are in the market for a vehicle. According to Experian’s State of the Automotive Finance Market Report: Q2 2024, leasing increased to 25.35%, up from 21.14% in Q2 2023 and 19.30% the year prior. While the average monthly payment and interest rate for a new loan modestly increased year-over-year, leasing is increasingly becoming a more attractive option for those leaning towards flexibility and affordability. For example, the average monthly payment on a leased vehicle was $148 less than a loan this quarter. What’s more, it seems consumers are leaning towards larger vehicles. For instance, the Honda CR-V (2.98%) continued to lead the top leased models in Q2 2024, and it was followed closely by the Tesla Model Y (2.61%). Rounding out the top five were the Honda Civic (2.29%), Ford F-150 (2.02%), and Chevrolet Silverado 1500 (1.86%). Prime financing grows and lease payments decline across all segments When looking at risk distribution trends in Q2 2024, prime consumers accounted for nearly 70% of the total finance market—with prime coming in at 37.82%, down from 39.84% last year and super prime increasing from 28.98% to 31.59% year-over-year. Subprime also saw a slight increase, going from 13% to 13.06% during the same period. It’s notable that all risk segments experienced a decrease in average monthly payments for leased vehicles, as super prime went from $601 in Q2 2023 to $586 in Q2 2024, prime declined to $583 this quarter, from $596 last year, and subprime was at $597, from $611. With the average monthly payments declining year-over-year for majority of shoppers, it can potentially create a more competitive market and drive more consumers towards this finance option—something automotive professionals should keep a close eye on. New and used vehicle finance market overview Data in Q2 2024 found that new vehicle loan amounts increased slightly, reaching $40,927, up from $40,743 last year, and the average interest rate went from 6.78% to 6.84% year-over-year. Despite the increases, the average monthly payment for a new vehicle only experienced a $1 growth to $734 this quarter. On the used side, the average loan amount declined from $27,316 Q2 2023 to $26,248 in Q2 2024, and the average rate grew from 11.47% to 12.01% in the same time frame. Though, the average monthly payment declined to $525 this quarter, from $536 last year. As the automotive industry continues to adapt to the changing market conditions and consumer preferences, it’s important for professionals to leverage the most current data—this will allow them to effectively assist consumers by meeting their financial needs with the available options. To learn more about automotive finance trends, view the full State of the Automotive Finance Market: Q2 2024 presentation on demand.

Voter registration lists are the backbone of our democratic process. However, maintaining accurate and up-to-date lists is a challenge that election agencies constantly face. With several regulations related to voting and election integrity that have been enacted or proposed in the last two years, maintaining a quality voter list is more important now than ever before. Election officials now have a powerful tool at their disposal: commercially available data to enhance voter list maintenance and boost voter confidence. The importance of maintaining voter lists Audit teams within election agencies are tasked with ensuring election integrity through voter list maintenance. These teams need reliable tools to: Verify and correct voter registration data Identify and update contact information Provide a cost-effective method for record updates Reduce election costs for taxpayers Success stories in voter list management Case study: West Virginia Secretary of State The West Virginia Secretary of State (WVSOS) uses Experian’s TrueTrace™ solution to enhance voter roll maintenance. Traditionally a skip-tracing solution for debt collectors, TrueTrace leverages unique data sources to ensure voters receive correct information, reducing wasted resources and improving election efficiency. WVSOS was challenged with enhancing their existing processes to a more robust 50-state comparison for cross-state movers. After WVSOS’s first data pull using TrueTrace, nearly 16,000 individuals were identified with a potential new "best" address that were also not flagged by other data comparison programs used by the state. The results? Of the almost 16,000 mailings sent, about 25% returned were undeliverable, confirming those individuals had moved. Access the full case study to discover best practices for maintaining voter rolls and conducting cost-effective elections. Webinar: El Paso County Clerk & Recorder's Office The El Paso County Clerk & Recorder’s Office was looking to bring transparency, efficiency, and increased voter confidence to the elections in El Paso County, Texas. To achieve this, they required verified enriched data for registered voters. By partnering with Experian, voter data was enriched using our TrueTrace solution. This partnership has enabled the Office to verify and append the most up-to-date voter address, leading to significant improvements in list maintenance. To date, the El Paso County Clerk & Recorder’s Office has seen a reduction of more than $39,860 in undeliverable ballot costs. Their ROI to date is a positive $4,537 back to the citizens of El Paso County. Listen to our on-demand webinar to hear more about this collaboration. Visit us online to learn more about our public sector solutions. Learn more

Learn about the state of housing affordability in Florida and how you can attract first-time homebuyers here.

Check out August's report for a deep dive into the latest market trends, including those around originations and the new housing market.

Cashflow underwriting is a modern approach to evaluating creditworthiness, giving lenders a greater view into one's financial situation.

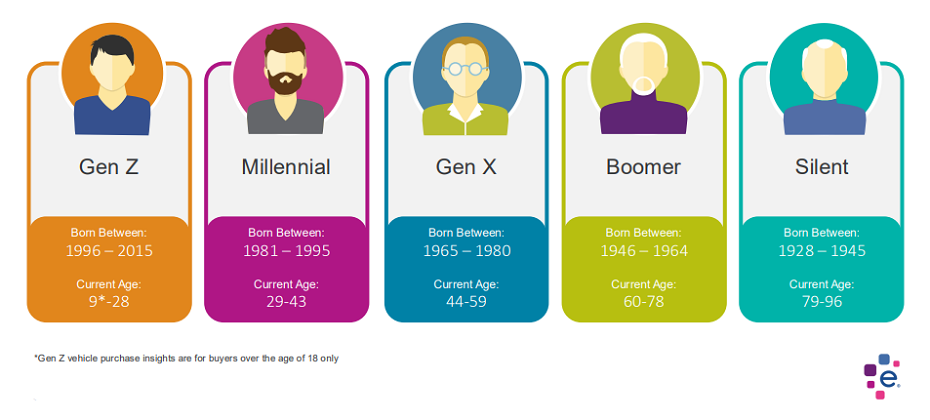

Quick Answer: New research on generational buying habits can help the auto industry better understand target audiences and improve marketing. The automotive industry is undergoing a rapid transformation, driven by technological advancements, changing consumer preferences, and a diverse marketplace. To navigate this complex landscape, understanding your target audience is key. This is where generational insights are indispensable. Why Generations Matter Each generation brings unique values, preferences, and buying behaviors to the table. Ignoring these differences can lead to ineffective marketing campaigns and missed opportunities. Different Needs and Priorities: Baby Boomers, Gen X, Millennials, and Gen Z have distinct needs and priorities when it comes to vehicles. For example, Baby Boomers may purchase more luxury vehicles, while Gen Z purchases a higher percentage of non-luxury vehicles. Communication Styles: Each generation responds differently to marketing messages. Traditional advertising might resonate with Baby Boomers, while social media and influencer marketing could be more effective for younger generations. Purchasing Behavior: The way people research and purchase cars has evolved significantly across generations. Understanding these differences can help you optimize your sales process. Leveraging Generational Insights To effectively leverage generational insights, consider the following: Conduct In-Depth Research: Gain a deep understanding of each generation's values, preferences, and buying habits. Use data analytics, surveys, and focus groups to gather insights. Create Targeted Messaging: Develop tailored messaging that resonates with each generation. Highlight the features and benefits that matter most to them. Choose the Right Channels: Select the most effective marketing channels for each generation. For example, television advertising might be less effective for Gen Z compared to social media. Personalize the Customer Experience: Offer personalized experiences that cater to the specific needs and preferences of each generation. Embrace Technology: Utilize technology to reach and engage different generations. For example, virtual showrooms or augmented reality experiences can appeal to younger consumers. Special Report: Generational Insights We've conducted in-depth research on generational buying habits for new and used vehicles. These insights can revolutionize your automotive marketing and sales strategies. Gain a competitive edge with our Automotive Consumer Trends Special Report: Generation Insights. Discover how to tailor your approach for maximum impact. Conclusion In today's competitive automotive market, understanding your target audience is essential for success. By incorporating generational insights into your marketing strategy, you can create more effective campaigns, build stronger customer relationships, and drive sales growth. Remember, a one-size-fits-all approach is unlikely to work. Embrace the diversity of your audience and tailor your message accordingly. Experian Automotive is here to help you with your marketing needs. If you’d like to learn more about our solutions and how we can support you, contact us below.

Dealerships can avoid purchasing flood-damaged vehicles with Experian AutoCheck's Free Flood Risk Check.

In this report, we explore how the evolving fraud landscape is impacting identity verification, customer experience, and business priorities for the future.

To authenticate identities and combat fraud within the Gen Z population, financial organizations need to implement comprehensive strategies.

AI fraud detection helps organizations enhance their security measures, reduce fraud losses, authenticate identity, and improve customer experience.

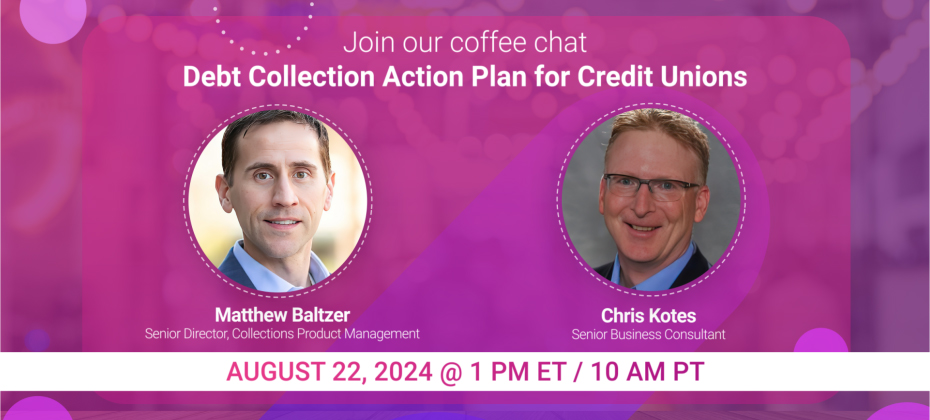

Grab a cup of coffee and join our experts for a conversation on credit union collection trends and successful account management strategies.

In this article...Recent trends in credit card debtThe rising tide of delinquenciesWhat is credit limit optimization?Benefits of credit limit optimizationEconomic indicators and CLO ImpactEnhanced profitability and risk mitigation This post was originally published on our Global Insights Blog. As credit card issuers grow, the size of their customer base expands, bringing both opportunities and challenges. One of the most critical challenges is managing growth while controlling default rates. Credit limit optimization (CLO) has emerged as a vital tool for banks and credit lenders to achieve this balance. By leveraging machine learning models and mathematical optimization, CLO enables lenders to tailor credit limits to individual customers, enhancing profitability while mitigating risk. Recent trends in credit card debt To understand the significance of CLO, it is essential to consider the current economic landscape. The first quarter of 2024 saw total household debt in the U.S. rise by $184 billion, reaching $17.69 trillion. While credit card balances declined slightly (a reflection of seasonal factors and consumer spending patterns), they remain a substantial component of household liabilities, with total credit card debt standing at approximately $1.26 trillion in early 2024. On average, American households hold around $10,479 in credit card debt, which is down from previous years but still significant. The average APR for credit cards in the first quarter of 2024 was 21.59%.* The rising tide of delinquencies In the first quarter of 2024, about 8.9% (annualized) of credit card balances transitioned into delinquency. This trend underscores the need for credit card issuers to adopt more sophisticated methods to assess credit risk and adjust credit limits accordingly. The rising rate of credit card delinquencies is a key driver behind the adoption of CLO strategies. What is credit limit optimization? Credit limit optimization uses advanced analytics to assess individual customers’ creditworthiness. By analyzing various data points, including payment history, income levels, spending patterns, and economic indicators, these tools can recommend optimal credit limits that maximize customer spending potential while minimizing the risk of default, all within the constraints set by the business in terms of its appetite for risk and capacity. For instance, a customer with a strong payment history and stable income might receive a higher credit limit, encouraging more spending and enhancing the lender’s revenue through interest and interchange fees. Conversely, customers showing signs of financial stress might see their credit limit reduced to prevent them from accumulating unmanageable debt. Benefits of credit limit optimization Improved profitability – By setting credit limits reflecting customers’ credit risk and spending potential, lenders can increase their revenue through higher interest and fee income. Reduced default rates – Lenders can significantly reduce the incidence of bad debt by identifying customers at risk of default and adjusting their credit limits accordingly. Improved customer satisfaction – Personalized credit limits can improve customer satisfaction, as customers are more likely to receive credit that matches their needs and financial situation. Regulatory compliance – CLO can help lenders comply with regulatory requirements by ensuring that credit limits are set based on objective, data-driven criteria. Economic indicators and CLO Impact Several economic indicators provide context for the importance of CLO in the current market. For instance, the Federal Reserve reported that in 2023, fewer than half of adult credit cardholders carried a balance on their cards, down from previous years. This indicates a more cautious approach to credit use among consumers, likely influenced by economic uncertainty and rising interest rates. Moreover, the disparity in credit card debt across different states highlights the varying economic conditions and the need for tailored credit strategies. States like New Jersey have some of the highest average credit card debts, while states like Mississippi have the lowest. This regional variation underscores lenders’ need to adopt flexible, data-driven approaches to credit limit setting. Enhanced profitability and risk mitigation Credit limit optimization is critical for credit card issuers aiming to balance growth and risk management. As economic conditions evolve and consumer behaviors shift, the ability to set personalized credit limits will become increasingly important. By leveraging advanced analytics and machine learning, CLO enhances profitability and contributes to a more stable and resilient financial system. One such solution is Experian’s Ascend Intelligence Services™ Limit, which provides an optimized strategy designed to enhance the precision and effectiveness of credit limit assignments. Ascend Intelligence Services™ Limit combines best-in-class bureau data with machine learning to simulate the impact of different credit limits in real time. This capability allows lenders to quickly test and refine their credit limit strategies without the lengthy trial-and-error period traditionally required. Ascend Intelligence Services Limit enables lenders to set credit limits that align with their business objectives and risk tolerance. By providing insights into the likelihood of default and potential revenue for each credit limit scenario, Ascend Intelligence Services Limit helps design optimal limit strategies. This not only maximizes revenue but also minimizes the risk of defaults by ensuring credit limits are appropriate for each customer’s financial situation. In a landscape marked by rising delinquencies and varying regional debt levels, the strategic use of CLO like Ascend Intelligence Services Limit represents a forward-thinking approach to credit management, benefiting both lenders and consumers. Learn More * HOUSEHOLD DEBT AND CREDIT REPORT (Q1 2024) – Federal Reserve Bank of New York

In this article...What is credit card fraud?Types of credit card fraudWhat is credit card fraud prevention and detection?How Experian® can help with card fraud prevention and detection With debit and credit card transactions becoming more prevalent than cash payments in today’s digital-first world, card fraud has become a significant concern for organizations. Widespread usage has created ample opportunities for cybercriminals to engage in credit card fraud. As a result, millions of Americans fall victim to credit card fraud annually, with 52 million cases reported last year alone.1 Preventing and detecting credit card fraud can save organizations from costly losses and protect their customers and reputations. This article provides an overview of credit card fraud detection, focusing on the current trends, types of fraud, and detection and prevention solutions. What is credit card fraud? Credit card fraud involves the unauthorized use of a credit card to obtain goods, services or funds. It's a crime that affects individuals and businesses alike, leading to financial losses and compromised personal information. Understanding the various forms of credit card fraud is essential for developing effective prevention strategies. Types of credit card fraud Understanding the different types of credit card fraud can help in developing targeted prevention strategies. Common types of credit card fraud include: Card not present fraud occurs when the physical card is not present during the transaction, commonly seen in online or over-the-phone purchases. In 2023, card not present fraud was estimated to account for $9.49 billion in losses.2 Account takeover fraud involves fraudsters gaining access to a victim's account to make unauthorized transactions. In 2023, account takeover attacks increased 354% year-over-year, resulting in almost $13 billion in losses.3,4 Card skimming, which is estimated to cost consumers and financial institutions over $1 billion per year, occurs when fraudsters use devices to capture card information from ATMs or point-of-sale terminals.5 Phishing scams trick victims into providing their card information through fake emails, texts or websites. What is credit card fraud prevention and detection? To combat the rise in credit card fraud effectively, organizations must implement credit card fraud prevention strategies that involve a combination of solutions and technologies designed to identify and stop fraudulent activities. Effective fraud prevention solutions can help businesses minimize losses and protect their customers' information. Common credit card fraud prevention and detection methods include: Fraud monitoring systems: Banks and financial institutions employ sophisticated algorithms and artificial intelligence to monitor transactions in real time. These systems analyze spending patterns, locations, transaction amounts, and other variables to detect suspicious activity. EMV chip technology: EMV (Europay, Mastercard, and Visa) chip cards contain embedded microchips that generate unique transaction codes for each purchase. This makes it more difficult for fraudsters to create counterfeit cards. Tokenization: Tokenization replaces sensitive card information with a unique identifier or token. This token can be used for transactions without exposing actual card details, reducing the risk of fraud if data is intercepted. Multifactor authentication (MFA): Adding an extra layer of security beyond the card number and PIN, MFA requires additional verification such as a one-time code sent to a mobile device, knowledge-based authentication or biometric/document confirmation. Transaction alerts: Many banks offer alerts via SMS or email for every credit card transaction. This allows cardholders to spot unauthorized transactions quickly and report them to their bank. Card verification value (CVV): CVV codes, typically three-digit numbers printed on the back of cards (four digits for American Express), are used to verify that the person making an online or telephone purchase physically possesses the card. Machine learning and AI: Advanced algorithms can analyze large datasets to detect unusual patterns that may indicate fraud, such as sudden large transactions or purchases made in different geographic locations within a short time frame. Advanced algorithms can analyze large datasets to detect unusual patterns that may indicate fraud, such as sudden large transactions or purchases made in different geographic locations within a short time frame. Behavioral analytics: Monitoring user behavior to detect anomalies that may indicate fraud. Education and awareness: Educating consumers about phishing scams, identity theft, and safe online shopping practices can help reduce the likelihood of falling victim to credit card fraud. Fraud investigation units: Financial institutions have teams dedicated to investigating suspicious transactions reported by customers. These units work to confirm fraud, mitigate losses, and prevent future incidents. How Experian® can help with card fraud prevention and detection Credit card fraud detection is essential for protecting businesses and customers. By implementing advanced detection technologies, businesses can create a robust defense against fraudsters. Experian® offers advanced fraud management solutions that leverage identity protection, machine learning, and advanced analytics. Partnering with Experian can provide your business with: Comprehensive fraud management solutions: Experian’s fraud management solutions provide a robust suite of tools to prevent, detect and manage fraud risk and identity verification effectively. Account takeover prevention: Experian uses sophisticated analytics and enhanced decision-making capabilities to help businesses drive successful transactions by monitoring identity and flagging unusual activities. Identifying card not present fraud: Experian offers tools specifically designed to detect and prevent card not present fraud, ensuring secure online transactions. Take your fraud prevention strategies to the next level with Experian's comprehensive solutions. Explore more about how Experian can help. Learn More Sources 1 https://www.security.org/digital-safety/credit-card-fraud-report/ 2 https://www.emarketer.com/chart/258923/us-total-card-not-present-cnp-fraud-loss-2019-2024-billions-change-of-total-card-payment-fraud-loss 3 https://pages.sift.com/rs/526-PCC-974/images/Sift-2023-Q3-Index-Report_ATO.pdf 4 https://www.aarp.org/money/scams-fraud/info-2024/identity-fraud-report.html 5 https://www.fbi.gov/how-we-can-help-you/scams-and-safety/common-scams-and-crimes/skimming This article includes content created by an AI language model and is intended to provide general information.

With the advent of AI and ML, optimizing credit prescreen campaigns has never been easier or more efficient.