Market Trends

Growth, risk and the rise of "hidden" business accounts As inflation remains elevated and early signs of labor market cooling emerge, the credit card landscape is entering its next phase. Over the past few weeks, policy actions and discussions around potential interest-rate caps have driven increased uncertainty across the credit card industry and broader global markets. Lenders face a careful balancing act: capturing growth opportunities while maintaining disciplined risk oversight. Our second annual State of Credit Cards Report explores the macroeconomic forces influencing the market, key shifts in originations and delinquency trends, and lender mix. New this year, the report also digs into an often‑overlooked segment: business accounts hidden inside consumer credit card portfolios. Additionally, the report offers actionable strategies to help lenders segment risk and drive disciplined growth more effectively. Key insights include: 30+ DPD delinquency rates remained above pre-pandemic levels in 2025, underscoring the need for disciplined asset‑quality monitoring. Fintechs continue to gain ground, posting a 71% YOY increase in account originations. Business accounts masked in the consumer credit card universe represent roughly 14% of balances and are more than 50% larger than the business card universe — a material segment with distinct risk and profitability dynamics that many lenders are not explicitly managing today. The report also outlines practical strategies to: Identify and segment business behavior within consumer portfolios. Align underwriting and account management with actual usage patterns. Capture targeted growth while protecting long‑term portfolio performance. Ready to dive deeper? Download the full 2026 State of Credit Cards Report to uncover insights that can help your organization manage risk more precisely and grow with confidence. Download report

The mortgage industry stands at a turning point. As acquisition costs climb and regulatory changes reshape long-held practices like mortgage trigger leads, lenders must rethink how they identify and engage qualified borrowers. What’s emerging is a smarter, more strategic approach—one that begins long before a credit application is submitted and leverages alternative data to illuminate borrower readiness, income, and risk. Traditional lead generation methods, often reliant on credit pulls and costly verification, are becoming less sustainable. Instead, forward-thinking lenders are embracing a layered data strategy—one that aligns each stage of the mortgage funnel with the right type of data at the right time. Rental History as a Window into Readiness A consumer’s rental history is far more than a record of where they’ve lived. It’s a powerful signal of their financial behavior, stability, and capacity to take on a mortgage. By analyzing verified rental payment data through sources like Experian RentBureau—the largest such database in North America—lenders can uncover early indicators of income, affordability, and risk. For instance, rental payments are highly correlated with income, typically showing a 3:1 ratio. This allows lenders to estimate income at the top of the funnel without relying on more expensive, verified income and employment data. It’s a practical way to reduce cost while preserving accuracy in segmentation. Alternative Data: From Insight to Action In today’s mortgage market, it’s not just about what data you have—it’s about when and how you use it. A tiered approach to data usage allows lenders to optimize both performance and spend: Prospecting and Segmentation: Observed data and rental history provide an affordable way to predict income and flag early risk signals without triggering compliance thresholds. Prequalification: Lightweight verification products help validate consumer-reported income and employment for prequal decisions at a lower cost. Decisioning: At the underwriting stage, verified income and employment data from trusted sources become critical to ensure compliance and close quality loans. This progressive framework improves lead quality, reduces fallout, and allows marketing and lending teams to focus their efforts on high-potential borrowers. Behavioral Indicators That Predict Mortgage Success Certain data points consistently emerge as predictors of mortgage readiness: Employment Tenure: Borrowers with more than six months in a verified job are twice as likely to apply for a mortgage. Rental Payment Behavior: Renters with more than two late payments are four times more likely to become delinquent on their mortgage. Affordability Thresholds: Consumers tend to feel comfortable with mortgage payments that are 25% to 75% higher than their rent—a range that correlates with lower delinquency and higher satisfaction. These insights allow lenders to flag risk and readiness early—reducing reliance on one-size-fits-all targeting and creating more meaningful, data-driven engagement. Preparing for a Post-Trigger Lead Environment With the elimination of mortgage trigger leads looming, lenders will need to replace reactive lead generation tactics with proactive, insight-driven strategies. Alternative data provides the foundation for this shift. Rather than waiting for a credit inquiry to act, lenders can use rent data, employment patterns, and observed financial behaviors to predict who is most likely to engage—and succeed—on the path to homeownership. Tools like Experian’s RentBureau and Observed Data platforms enable this transformation by providing access to decision-grade behavioral data earlier in the funnel. These tools not only reduce acquisition costs but also offer a better experience for the consumer—less invasive, more personalized, and more aligned with their financial journey. Modernizing the Mortgage Funnel The modern borrower expects a digital-first, seamless experience. For lenders, meeting this expectation requires more than a responsive website or fast application—it requires a reimagined data strategy. The key is precision. Mortgage lenders that align the right data with the right decision point—from prequal to close—will outperform in efficiency, risk management, and consumer satisfaction. By layering alternative and verified data sources, they can build a funnel that is not only cost-effective but also calibrated to real indicators of borrower success. Looking Ahead The future of mortgage lending will be defined by agility, intelligence, and inclusivity. As the market moves away from legacy lead gen tactics and toward data-informed decisioning, the role of alternative data will only grow. Lenders who adopt this shift early will be positioned to say yes to more borrowers, reduce costs, and deliver a better customer experience. Those who cling to traditional models risk falling behind as the industry evolves. Now is the time to rethink the mortgage lead strategy. Not just to reduce cost—but to build a better, smarter path to homeownership for the next generation of buyers. For a deeper dive into how alternative data is transforming mortgage lead generation, watch the recent HousingWire and Experian webinar: “Rethinking Mortgage Lead Strategy: How Alternative Data Sources Can Predict Income, Risk, and Readiness.” Learn how to apply these insights across your funnel—from prospecting to prequalification—and hear directly from Experian product leaders on practical strategies to boost efficiency and performance. Watch the full webinar on demand here.

A Realignment is underway The U.S. housing market is no longer waiting on the sidelines. After enduring over two years of historically high mortgage rates, the Federal Reserve began implementing rate cuts in fall 2025, with additional reductions forecast for early 2026. For lenders, this marks more than a turning point—it’s a call to action. Whether you’re targeting first-time buyers, tracking refinance-ready loans, or watching affordability trends, today’s environment demands rapid, strategic adjustments. Rate cuts are fueling renewed demand Mortgage rates, which hovered around 7% for much of the past year, have begun to ease. Even a modest drop has the potential to unlock substantial borrower interest—particularly among the 4.4 million U.S. mortgages now “ripe” for refinance. Expect a spike in both rate-and-term refinances and cash-out activity, as homeowners look to lower payments or access equity. Lenders must scale up quickly, especially around digital capacity, prescreen targeting, and streamlined closings. Affordability is still a roadblock—Especially for younger renters Despite improving borrowing conditions, affordability remains a systemic challenge. The national rent-to-income (RTI) ratio stands at 46.8%, up 7.7% since early 2023. In high-cost states like California and Massachusetts, it exceeds 56%. Experian data reveals that 62% of renters fall into the low-to-moderate income category, spending over half their income on rent. Over 50% now fall into Near Prime or Subprime credit tiers, making alternative credit data—like rental payment history—vital for inclusive underwriting. Refinance isn't the only opportunity—Target first-time buyers strategically Gen Z is now the largest segment of the rental population, and many are financially strained yet aspirational. A major opportunity exists in helping these renters transition to homeownership using expanded credit models and customized offerings. With Federal Housing Finance Agency (FHFA)-approved models like VantageScore 4.0 and FICO 10T on the horizon, lenders should explore how newer scoring frameworks and rent payment reporting can increase access to mortgage credit. Region-specific strategies are more important than ever From Miami to Minneapolis, market conditions vary drastically. Some metros, like Kansas City (+16.7%) and Louisville (+14.2%), are experiencing double-digit rent growth, while cities like Atlanta and Jacksonville are seeing declines. Lenders must tailor outreach based on local affordability trends, migration patterns, and housing supply constraints. Dynamic analytics tools—like Experian’s Ascend or Mortgage Insights Dashboard—can guide regional strategy at scale. The supply side may not keep pace Even with rate cuts stimulating demand, housing supply could remain a bottleneck. Multifamily completions are outpacing starts 1.5 to 1, and single-family construction, though recovering, remains cautious. In markets with tight supply, reduced borrowing costs may drive up prices faster than inventory can absorb, exacerbating affordability for first-time buyers. What lenders should prioritize now: Build Refinance Infrastructure: Prepare for increased volume with instant income verification tools like Experian Verify to streamline processes. Target First-Time Buyers: Use rental history, cashflow scores, and rent-to-income metrics to assess nontraditional credit applicants fairly. Get Granular with Geography: Align product offerings with local affordability, vacancy rates, and rent growth. Leverage Self-Service Prescreen Tools: Act on opportunities quickly using Experian’s agile targeting platforms. Model with New Credit Scores: Take advantage of the Experian Score Choice Bundle to test VantageScore 4.0 and FICO 2 side by side. Final Thought: The market is not rebounding—It is realigning The current housing shift is not a return to old norms—it’s the start of a redefined landscape. Lenders who act decisively, invest in technology, and prioritize inclusivity will lead the next chapter in mortgage growth. Experian is here to support you—with data, insights, and tools designed for this very moment.

The Quiet But Real Shift in Mortgage Marketing Despite the media’s focus on digital advertising, the mailbox is quietly becoming a major battleground again for mortgage and home equity lenders. The environment is ripe for this: interest rates are stabilizing near 7 % (which opens up refinance & home equity demand), and consumer credit profiles remain robust yet tightening in certain segments. For lenders, precision outreach is now a key differentiator. Why Direct Mail Still Works — and Why It Matters Now According to a 2025 industry study, direct‑mail marketing continues to deliver the strongest ROI: for example, direct mail’s ROI is cited at ~$58 for every dollar spent, compared with ~$19 for PPC and ~$7 for email. PostGrid A separate piece notes that physical mail pieces still command attention: “Consumers are more likely to trust physical mail than digital ads … response rates can range from 2% to over 5% depending on targeting and message quality.” KYC Data+2Highnote+2 But the most important reason mail is working now: data + personalization. Lenders who combine accurate consumer/credit/property insight with mail campaigns are seeing better alignment of offers and borrowers. A recent article emphasizes that “when backed by high‑quality data sources and AI‑driven triggers, mortgage direct mail can outperform digital‑only campaigns.” Megaleads For mortgage & home‑equity marketers specifically, Experian’s data shows direct mail and refined segmentation remain growth levers in a market where originations are modest, but competition for good borrowers is intense. Experian+1 Why this matters now, for lenders: With rates comparatively high, many borrowers are choosing to postpone purchases or full refinances—but still open to tapping equity. That makes mail‑based offers (especially those tailored with relevant property/equity/credit data) very timely. Digital advertising is crowded, algorithmic, and increasingly expensive — mail provides a differentiated channel. The exit or pull‑back of certain large players in home equity creates opportunity gaps. The Data Speaks: From ITA to Prescreen — and What’s Changing Here’s a breakdown of key shifts: In May 2025, for mortgage and home‑equity offers: Mortgage ITA (Invitation to Apply) volume: ~29.2 million Home Equity ITA volume: ~25.8 million Mortgage Prescreen volume: ~15.6 million Home Equity Prescreen volume: ~19.0 million Experian Further, recent trends report that home equity direct mail offers have now surpassed first‑mortgage offers in some segments — driven by aggressive marketing and AVM‑based personalization. Experian The latest data from the ICE Mortgage Technology November 2025 Mortgage Monitor shows that falling mortgage rates have expanded the pool of homeowners who can reduce monthly payments via refinance or access home equity, which in turn supports more targeted direct‑mail outreach. Mortgage Tech What this means for campaign strategy: Prescreen (where the lender sends offers to pre‑qualified or high‑propensity segments) is edging into prominence over broad ITA campaigns — because it enables targeted, efficient spend and stronger conversion. Lenders can use property and credit data (e.g., equity levels, credit score, loan‑to‑value, tenure) to craft mail offers that align with actual borrower situations (not just “Dear Homeowner”). The gap left by large players exiting or backing off in home equity means agile lenders can expand mail volume and capture incremental market share. Market Movers: Who’s Winning — and Why In the direct mail and home-equity space, a mix of established players and newer entrants is reshaping the competitive landscape. Overall mortgage mail volume is being driven by institutions that lean heavily on prescreen strategies and sophisticated, data-driven segmentation. At the same time, leadership in ITA mail offers is shifting away from traditional incumbents toward organizations using more agile marketing approaches and refined offer logic. Notably, several non-traditional and alternative-model providers now rank among the top mailers in the home-equity category, signaling growing consumer interest in options such as shared equity or sale-leaseback structures. Fintech and digitally native lenders, in particular, are accelerating home-equity prescreen activity; their speed, experimentation, and product innovation are raising expectations for both relevance and simplicity in borrower outreach. Meanwhile, pullbacks and exits by some large financial institutions have opened meaningful white space in the home-equity market, creating opportunities for others to capture unmet demand. For lenders looking to compete, the playbook is becoming clearer: rapid testing and iteration, tight coordination between direct mail and digital follow-up, a strong focus on homeowner equity, and precise, data-driven targeting. The most effective campaigns align product design to well-defined segments – for example, borrowers with substantial equity, strong credit profiles, and established tenure – ensuring offers are both timely and highly relevant. Prescreen vs. ITA: Why Targeting Wins The shift from broad ITA to prescreen‑based campaigns might seem nuanced, but its implications are strategic: Prescreen advantages: Better alignment with borrower creditworthiness and property profile — because you are sending offers to those who meet risk and propensity criteria. Improved conversion and campaign efficiency — by reducing wasted mailings to low‑probability recipients. Lower marketing spend per funded loan — because you spend less to reach the right audience. Faster speed‑to‑market — thanks to platforms that allow weekly refreshed data and custom lists. For example, Experian’s self‑service prescreen platform offers weekly data updates and FCRA‑compliant targeting. Regulatory and operational clarity — prescreen infrastructure has matured, with aligned credit data, reason‑codes, and compliance built in. ITA (Invitation to Apply) still has use cases: When you want to cast a wider net (e.g., first‑time homebuyers, large volume builds) When brand awareness is a goal rather than immediate action When the product is straightforward and broader, not highly segmented But the winning strategy in 2025 and beyond is data‑driven prescreen + targeted direct mail, especially in home equity. As one blog post notes, direct mail campaigns that are personalized can deliver up to ~44% stronger conversions compared with less personalized campaigns. Megaleads Strategic Opportunities for Lenders & Marketing Teams Based on the data and competitive shifts, here are actionable recommendations: Expand Home Equity Prescreen Offers: With home equity direct mail offers now pushing ahead of first‑mortgage offers in volume (and with tappable equity reaching trillions), this channel is ripe. For instance, a recent BCG report estimates ~$18.3 trillion in tappable equity in the U.S. system. BCG Media Publications+1 Leverage the Player Exits: Large institutions reducing or exiting HELOC/home‑equity lines provide space for nimble lenders to increase direct‑mail volume and connect with households previously under‑targeted. Integrate Multi‑Channel Touchpoints: While mail is the vehicle, the journey often involves digital follow‑up, landing pages, and timely calls. Studies show layering direct mail with digital channels improves results. Highnote+1 Use Data for Targeting, Not Just Volume: Utilize property, credit, income, and behavioral data (from providers like Experian) to identify segments like: homeowners with >30% equity, 5–10 years of tenure, credit score 700+, and interest in renovations or cash‑out use cases. Speed Matters: Campaigns should be nimble. Weekly data refreshes, agile list creation, rapid mail deployment, and timely follow‑up matter in a competitive environment. Measure & Optimize: Track response, conversion, ROI per piece. For example, what are funded loans per 1,000 mail pieces? Which segments convert better? Optimize creative, offer, timing. Stay Compliant & Transparent: Prescreen offers must follow FCRA rules; mail pieces must clearly disclose terms. Consumers and regulators are increasingly sensitive to over‑targeting or over-personalization — balance personalization with respect and transparency.* Megaleads Putting It All Together: Rethinking Your Direct‑Mail Strategy If your marketing playbook still treats direct mail as a “safe‑bet, high‑volume fallback”, it’s time for an upgrade. Today’s borrowers expect relevance, personalization, and fast follow‑through. They are homeowners — not just buyers — and many are seeking home‑equity options rather than traditional purchase refis. Lenders that find success in this space are likely to: Use data and analytics (credit + property + behavior) to identify the right audience. Deploy prescreen‑based campaigns rather than generic blanket offers. Combine direct mail + digital + phone as an orchestrated funnel. Monitor performance in near real‑time and iterate quickly. Offer products aligned with what the borrower wants (e.g., interest‑only draw period HELOCs, fixed‑conversion options, etc). Operate with speed, precision, and compliance. As the market shifts, the channel is shifting too. Direct mail isn’t dead — it’s evolving, and those who invest in the right mix of data, targeting, creative, and execution stand to win. Call to Action Ready to elevate your direct‑mail and prescreen strategy? Contact Experian’s Mortgage & Housing solutions team to explore how our platform enables: Weekly refreshed, bureau‑grade credit + property data Self‑service prescreen campaign build and list generation Custom segmentation using credit, equity, tenure, and product propensity Compliance‑ready reason codes and targeting workflows* Visit: experian.com/mortgage or speak with your Experian account executive today. Next in the Series Blog Post 3 – “Beyond the HELOC: Why the Future of Home Equity Might Not Involve Loans at All” *Clients are responsible for ensuring their own compliance with FCRA requirements.

Rental affordability in the U.S. isn’t just about rising prices—it’s about where those increases are happening. Some cities and states are becoming increasingly unaffordable compared to others, and renters are feeling the financial pressure differently across the country. Not all rent increases are equal National rent prices have increased by about 16% in two years, but where you live plays a huge role in how much of your paycheck goes toward housing. In places like California and Massachusetts, the average renter now spends over 56% of their income on rent. That’s nearly double the “affordable” threshold of 30%. But even traditionally affordable states are feeling the heat. Oklahoma, Kentucky, and Louisiana all saw rent hikes between 6% and 10%—with Oklahoma topping out at 9.7%. These increases are hitting renters in places that used to be considered “safe” from housing inflation. Regional breakdown: Here’s how the rent-to-income ratio compares across regions: West: Rent-to-income ratio of 46.4% Northeast: 48.1% South: 43% (but fastest-growing burden) Midwest: 37.7% (still below the national average, but climbing fast) Florida, for example, saw its rent-to-income ratio jump by 12.1% since 2023. Arizona isn’t far behind, with an 11.7% increase. These changes are tied to migration patterns—many people moved to these states during the pandemic, and now demand is far outpacing supply. City-level surprises Some of the biggest rent increases are happening in cities you might not expect: Miami, FL: Up 21.1% YOY Kansas City, MO: Up 16.7% Louisville, KY: Up 14.2% Chicago, OH: Up 13% On the flip side, a few cities have seen rent drops: Jacksonville, FL: Down 3% Atlanta, GA: Down 2.2% Austin, TX: Essentially flat These shifts show how local economic factors and population trends can quickly change a market’s affordability. More renters are moving—and struggling to settle Another sign of pressure: renters are on the move. The percentage of renters with more than one lease has jumped since 2023, especially among Gen X and older millennials. People are relocating more often—sometimes chasing affordability, sometimes being priced out. At the same time, vacancy rates are rising—from 6.6% to 7.1% nationally. That may sound good for renters, but it’s often a sign of mismatch: more units are being built, but not always where people can afford them. The bottom line If you’re a landlord or investor, these geographic insights matter. Rent pressure isn’t universal—but knowing where it’s concentrated can help you adjust screening, pricing, and retention strategies. For renters, this means being more informed and prepared before moving or signing a lease. In our final post, we’ll explore the macro trends shaping the future—like mortgage rates, construction slowdowns, fraud risks, and how better data is helping landlords and lenders keep up.

The U.S. housing market is no longer waiting on the sidelines. After enduring over two years of historically high mortgage rates, the Federal Reserve began implementing rate cuts in fall 2025, with additional reductions forecast for early 2026. For lenders, this marks more than a turning point—it’s a call to action. Whether you’re targeting first-time buyers, tracking refinance-ready loans, or watching affordability trends, today’s environment demands rapid, strategic adjustments. Rate cuts are fueling renewed demand Mortgage rates, which hovered around 7% for much of the past year, have begun to ease. Even a modest drop has the potential to unlock substantial borrower interest—particularly among the 4.4 million U.S. mortgages now “ripe” for refinance. Expect a spike in both rate-and-term refinances and cash-out activity, as homeowners look to lower payments or access equity. Lenders must scale up quickly, especially around digital capacity, prescreen targeting, and streamlined closings. Affordability is still a roadblock—Especially for younger renters Despite improving borrowing conditions, affordability remains a systemic challenge. The national rent-to-income (RTI) ratio stands at 46.8%, up 7.7% since early 2023. In high-cost states like California and Massachusetts, it exceeds 56%. Experian data reveals that 62% of renters fall into the low-to-moderate income category, spending over half their income on rent. Over 50% now fall into Near Prime or Subprime credit tiers, making alternative credit data—like rental payment history—vital for inclusive underwriting. Refinance isn't the only opportunity—Target first-time buyers strategically Gen Z is now the largest segment of the rental population, and many are financially strained yet aspirational. A major opportunity exists in helping these renters transition to homeownership using expanded credit models and customized offerings. With Federal Housing Finance Agency (FHFA)-approved models like VantageScore 4.0 and FICO 10T on the horizon, lenders should explore how newer scoring frameworks and rent payment reporting can increase access to mortgage credit. Region-specific strategies are more important than ever From Miami to Minneapolis, market conditions vary drastically. Some metros, like Kansas City (+16.7%) and Louisville (+14.2%), are experiencing double-digit rent growth, while cities like Atlanta and Jacksonville are seeing declines. Lenders must tailor outreach based on local affordability trends, migration patterns, and housing supply constraints. Dynamic analytics tools—like Experian’s Ascend or Mortgage Insights Dashboard—can guide regional strategy at scale. The supply side may not keep pace Even with rate cuts stimulating demand, housing supply could remain a bottleneck. Multifamily completions are outpacing starts 1.5 to 1, and single-family construction, though recovering, remains cautious. In markets with tight supply, reduced borrowing costs may drive up prices faster than inventory can absorb, exacerbating affordability for first-time buyers. What lenders should prioritize now • Build Refinance Infrastructure: Prepare for increased volume with instant income verification tools like Experian Verify to streamline processes. • Target First-Time Buyers: Use rental history, cashflow scores, and rent-to-income metrics to assess nontraditional credit applicants fairly. • Get Granular with Geography: Align product offerings with local affordability, vacancy rates, and rent growth. • Leverage Self-Service Prescreen Tools: Act on opportunities quickly using Experian’s agile targeting platforms. • Model with New Credit Scores: Take advantage of the Experian Score Choice Bundle to test VantageScore 4.0 and FICO 2 side by side. Final Thought: The market is not rebounding—It is realigning The current housing shift is not a return to old norms—it’s the start of a redefined landscape. Lenders who act decisively, invest in technology, and prioritize inclusivity will lead the next chapter in mortgage growth. Experian is here to support you—with data, insights, and tools designed for this very moment.

In 2025, home equity lending has re-emerged as a central theme in the American financial landscape—an evolution not driven by hype, but by hard data, economic realities, and consumer behavior. As homeowners grapple with inflation, rising consumer debt, and a persistent affordability crisis in housing, the home equity line of credit (HELOC) is gaining traction as a practical, flexible, and often misunderstood financial solution.

Now in its tenth year, Experian’s U.S. Identity and Fraud Report continues to uncover the shifting tides of fraud threats and how consumers and businesses are adapting. Our latest edition sheds light on a decade of change and unveils what remains consistent: trust is still the cornerstone of digital interactions. This year’s report draws on insights from over 2,000 U.S. consumers and 200 businesses to explore how identity, fraud and trust are evolving in a world increasingly shaped by generative artificial intelligence (GenAI) and other emerging technologies. Highlights: Over a third of companies are using AI, including generative AI, to combat fraud. 72% of business leaders anticipate AI-generated fraud and deepfakes as major challenges by 2026. Nearly 60% of companies report rising fraud losses, with identity theft and payment fraud as top concerns. Digital anxiety persists with 57% of consumers worried about doing things online. Ready to go deeper? Explore the full findings and discover how your organization can lead with confidence in an evolving fraud landscape. Download report Watch on-demand webinar Read press release

First mortgage delinquencies and foreclosures are increasing, particularly in later stages of delinquency. Home equity delinquencies remain low, signaling stability in that segment. Mortgage originations are up, with refinances beginning to recover. HELOC direct mail offers have surpassed first mortgage offers, driven by aggressive marketing and AVM-based personalization. Lenders using property data in marketing outperform peers relying on volume alone. Strategic focus for lenders: tighten risk analytics, integrate data into marketing, and adopt AVM-based personalization.

Understanding generational trends and preferences is more crucial than ever, especially for the financial services industry.

Market volatility, evolving regulations, and shifting consumer expectations are a catalyst to make energy providers to rethink how they operate. Rising energy costs, grid reliability concerns, and the push for sustainable energy sources add layers of complexity to an already challenging landscape. In this environment, data analytics in utilities has become a strategic imperative, enabling companies to optimize operations, mitigate risks, and enhance customer experiences. With a wealth of data at their disposal, utilities must harness the power of utility analytics to transform raw information into actionable intelligence. This is where Experian’s energy and utilities solutions come into play. With an unmatched data reach of more than 1.5 billion consumers and 201 million businesses, we are uniquely positioned to help energy and utility providers unlock greater potential within their organizations, whether that’s by boosting customer engagement, preventing fraud and verifying identities, or optimizing collections. Market Challenges Facing the Utilities Sector Utilities today face a series of economic, regulatory, and operational hurdles that demand innovative solutions. Regulatory and Compliance Pressures: Governments and regulatory bodies are tightening rules around emissions, sustainability, and grid reliability. Utilities must balance compliance with the need for cost efficiency. New carbon reduction mandates and reporting requirements force energy providers to adopt predictive modeling solutions that assess future demand and optimize energy distribution. Economic Uncertainty and Rising Costs: Inflation, fuel price fluctuations, and supply chain disruptions are impacting the cost of delivering energy. Utilities must find ways to improve financial forecasting and reduce inefficiencies—tasks well suited for advanced analytics solutions that optimize asset management and detect cost-saving opportunities. Grid Modernization and Infrastructure Investments: Aging infrastructure and increased energy demand require significant investments in modernization. Data-driven insights help utilities prioritize infrastructure upgrades, preventing costly failures and ensuring reliability. Predictive analytics models play a crucial role in identifying patterns that signal potential grid failures before they occur. Customer Expectations and Energy Transition: Consumers are more engaged than ever, demanding personalized service, real-time billing insights, and renewable energy options. Utilities must leverage advanced analytics to segment customer data, predict energy usage, and offer tailored solutions that align with shifting consumer preferences. Rising Fraud: Account takeover fraud, a form of identity theft where cybercriminals obtain credentials to online accounts, is on the rise in the utility sector. Pacific Gas and Electric Company reported over 26,000 reports of scam attempts in 2024 and has received over 1,700 reports of attempted scams in January 2025 alone. Utility and energy providers must leverage advanced fraud detection and identity verification tools to protect their customers and also their business. How Data Analytics Is Transforming the Utilities Industry Optimizing Revenue and Reducing Fraud Fraud and revenue leakage remain significant challenges. Utilities can use data and modeling to detect anomalies in energy usage, identify fraudulent accounts, and minimize losses. Experian’s predictive modeling solutions enable proactive fraud detection, ensuring financial stability for providers. Enhancing Demand Forecasting and Load Balancing With renewable energy sources fluctuating daily, accurate demand forecasting is critical. By leveraging utility analytics, providers can predict peak demand periods, optimize energy distribution, and reduce waste. Improving Credit Risk and Payment Management Economic uncertainty increases the risk of late or unpaid bills. Experian’s energy and utilities solutions help providers assess creditworthiness and develop more flexible payment plans, reducing bad debt while improving customer satisfaction. Why Experian? The Power of Data-Driven Decision Making Only Experian delivers a comprehensive suite of advanced analytics solutions that help utilities make smarter, faster, and more informed decisions. With more than 25 years of experience in the energy and utility industry, we are your partner of choice. Our predictive analytics models provide real-time risk assessment, fraud detection, and customer insights, ensuring utilities can confidently navigate today’s economic and regulatory challenges. In an industry defined by complexity and change, utilities that fail to leverage data analytics in utilities risk falling behind. From optimizing operations to enhancing customer engagement, the power of utility analytics is undeniable. Now is the time to act. Explore how Experian’s energy and utilities solutions can help your organization harness the power of advanced analytics to navigate market challenges and drive long-term success. Learn more Partner with our team

The days of managing credit risk, fraud prevention, and compliance in silos are over. As fraud threats evolve, regulatory scrutiny increases, and economic uncertainty persists, businesses need a more unified risk strategy to stay ahead. Our latest e-book, Navigating the intersection of credit, fraud, and compliance, explores why 94% of forward-looking companies expect credit, fraud, and compliance to converge within the next three years — and what that means for your business.1 Key insights include: The line between fraud and credit risk is blurring. Many organizations classify first-party fraud losses as credit losses, distorting the true risk picture. Fear of fraud is costing businesses growth. 68% of organizations say they’re denying too many good customers due to fraud concerns. A unified approach is the future. Integrating risk decisioning across credit, fraud, and compliance leads to stronger fraud detection, smarter credit risk assessments, and improved compliance. Read the full e-book to explore how an integrated risk approach can protect your business and fuel growth. Download e-book 1Research conducted by InsightAvenue on behalf of Experian

The financial services industry faces increasing pressure to innovate in today's fluctuating interest rate environment. For regional banks and credit unions, effective deposit growth strategies involve more than just offering attractive rates. Leveraging data and analytics is key to enhancing deposit portfolios, improving customer engagement, and fostering financial wellness. By prioritizing consumer-focused solutions, institutions can achieve dual benefits: driving organizational growth while meeting customer needs. For a deeper dive into this subject, check out our on-demand webinar “Growing Beyond Interest Rates: The Opportunity for Demand Deposit Accounts.” The current state of interest rates and market dynamics As interest rates change, financial institutions encounter shrinking margins and heightened competition. The stakes are high: 54% of consumers plan to leave their banks within the next year1, often citing unmet expectations for personalized services and financial guidance2. This competitive environment requires innovative strategies to retain customers and attract new ones without solely relying on interest rates. Key challenges: Shrinking margins due to rate volatility. Increased competition from fintechs and alternative providers. Rising consumer expectations for personalized, proactive services. Leveraging data and analytics in your deposit growth strategies Regional banks and credit unions can distinguish themselves by investing in advanced data analytics and personalized engagement tools. These strategies help create value for customers while improving the institution’s operational efficiency and revenue potential. 1. Personalization through financial insights According to Experian data, more than half of consumers expect their financial provider to actively support their financial wellness2. However, one-third feel that current efforts fall short3. Offering tools like spending trackers, budgeting resources, and personalized credit score improvement plans can help close this gap. 2. Engagement-driven solutions Consumers are more likely to stay loyal to institutions that provide actionable insights. Experian’s partners have seen a 5% lift in 12-month retention rates among customers enrolled in credit and identity programs according to data reported by partners2. Alerts for credit monitoring and financial updates not only keep customers informed but also help drive monthly logins, enhancing cross-sell opportunities. 3. Identity and data protection as value-added services With the increasing threat of identity theft, proactive identity monitoring and restoration services are becoming critical. Banks offering these features—branded under their name—can boost customer satisfaction and loyalty. Practical steps for regional banks and credit unions To capitalize on these opportunities, financial institutions should consider the following steps: Step 1: Develop a customer-centric engagement program Tailor programs to different demographic groups. Millennials and Gen Z are particularly drawn to tech-savvy solutions that integrate seamlessly with their financial lives. By consolidating financial management tools within one portal, banks can help simplify customers’ lives and enhance engagement. Step 2: Focus on retention and cross-sell opportunities Consumers engaged with financial tools, such as credit score trackers or budgeting aids, exhibit stronger loyalty and are more likely to adopt additional products. Use insights from these tools to offer personalized product recommendations that align with their financial journey. Step 3: Offer premium tiers Institutions can create tiered service packages, starting with free offerings (e.g., basic credit monitoring) and progressing to paid premium packages that include advanced identity protection or financial management analytics. Step 4: Utilize advanced analytics for targeting By analyzing anonymized customer data, banks can identify high-value segments and tailor marketing efforts to their specific needs. This targeted approach fosters more meaningful relationships and improves ROI on acquisition campaigns. Case for Action: Why consumer engagement matters A customer engagement program does more than enhance loyalty, it helps drive measurable outcomes: Retention rates: Over 98% for free services and 91% for paid programs.4 Improved credit scores: Subprime consumers enrolled in credit-building tools see an average credit score increase of 32 points.5 Higher satisfaction scores: Some institutions offering comprehensive financial tools report a lift in Net Promoter Scores (NPS). Conclusion The path forward for regional banks and credit unions lies in moving beyond rate-based competition and looking to multipronged deposit growth strategies. By leveraging data, analytics, and consumer-focused programs, financial institutions can enhance their deposit portfolios and deepen customer relationships. Now is the time to transform engagement into a growth engine, ensuring long-term success in a dynamic market. Ready to elevate your deposit portfolio with our tailored solutions? Click below to learn more or contact us to schedule a consultation and design a program that meets your organization’s goals. Learn more Watch the webinar 1 Retail Bank Customer Satisfaction Holds Steady but Trust Declines, J.D. Power Finds, 2024 2 Experian internal analysis, 2024 3 MX, What Influences Where Consumers Choose to Bank, June 2023 4 Experian Core metrics analysis, October 2023 5 Experian Data, Credit Score Rates with subprime consumers, June 2022 – June 2023

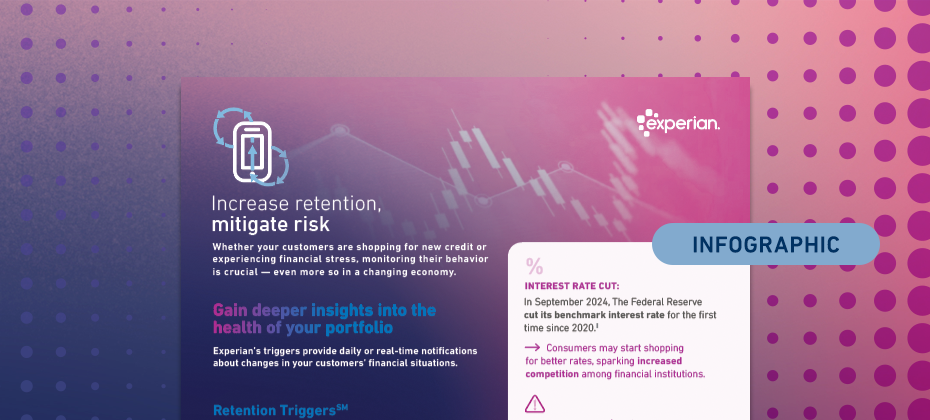

Whether consumers are shopping for new credit or experiencing financial stress, monitoring their behavior is crucial — even more so in an ever-changing economy. Our latest infographic explores economic trends impacting consumers’ financial behaviors and how Experian’s Risk and Retention TriggersSM enable lenders to detect early signs of risk or churn. Key highlights include: Credit card balances climbed to $1.17 trillion in Q3 2024. As prices of goods and services remain elevated, consumers may continue to experience financial stress, potentially leading to higher delinquency rates. Increasing customer retention rates by 5% can boost profits by 25% to 95%. View the infographic to learn how Risk and Retention Triggers can help you advance your portfolio management strategy. Access infographic

The credit card market is rapidly evolving, driven by technological advancements, economic volatility, and changing consumer behaviors. Our new 2025 State of Credit Card Report provides an in-depth analysis of the credit card landscape and strategy considerations for financial institutions. Findings include: Credit card debt reached an all-time high of $1.17 trillion in Q3 2024. About 19 million U.S. households were considered underbanked in 2023. Bot-led fraud attacks doubled from January to June 2024. Read the full report for critical insights and strategies to navigate a shifting market. Access report