Tag: consumer credit behavior

In the dynamic consumer credit landscape, understanding emerging trends is paramount for fintechs to thrive. Experian's latest fintech trends report provides deep insights into the evolving market, shedding light on crucial areas such as origination volumes, average loan balances, and delinquency trends. Let's delve into some key findings and their implications for fintech lenders. Fintech lending origination volume trends The report reveals intriguing shifts in origination volumes for unsecured personal loans and credit cards. While overall origination amounts dipped, fintechs experienced a notable decrease, signaling potential challenges in funding availability and economic uncertainties. Despite this, the total origination volume for fintechs remains robust, underlining their continued significance in the market. Fintech market share versus traditional lenders Fintechs, known for their agility and digital prowess, witnessed fluctuations in market share, particularly in the unsecured personal loan segment. While digital loans continue to drive a significant portion of originations, there's a discernible shift in market dynamics, urging fintech lenders to explore diversification strategies, including expanding into credit card offerings. Fintech lending average loan balance trends Amidst changing economic landscapes, average loan balances for both unsecured personal loans and credit cards exhibited intriguing patterns. Fintech lenders, although maintaining a competitive edge in average balances, face the challenge of balancing risk and profitability, especially amidst rising delinquency levels. Fintech lending delinquency trends One of the most critical aspects highlighted in the report is the uptick in delinquency levels for unsecured personal loans and credit cards. While fintechs navigate through economic uncertainties, there's a growing imperative to enhance risk management strategies and focus on prime and above credit tiers to mitigate potential risks. Understanding the digital borrower As digital borrowing continues to gain prominence, it's essential for fintechs to grasp the nuances of the digital borrower. With millennials emerging as key players in the digital lending landscape, fintechs must tailor their offerings to cater to the unique preferences and behaviors of this demographic segment. Looking ahead to 2024 for fintech lenders As we look to the future, data-driven decision-making and strategic portfolio management are more important than ever for fintechs. With economic uncertainties still in the mix, fintechs must leverage data and analytics to fuel growth while safeguarding against potential risks. Experian's fintech trends report serves as a guiding beacon, equipping fintechs with the knowledge and strategies needed to navigate through uncertainties and unlock opportunities for sustainable growth. The report offers actionable insights, including the imperative to conduct periodic portfolio reviews, retool data analytics and models, and remodel lending criteria to stay ahead in the competitive landscape. Learn more about our fintech solutions and how we can work together to drive profitable growth for your company. Learn more Download the report About the report: Experian's Fintech Trends Report 2024 offers a comprehensive analysis of credit trends, leveraging data from January 2019 to November 2023. The report provides valuable insights into the evolving landscape of unsecured personal loans and credit cards, empowering fintechs with actionable intelligence to thrive in a competitive market environment.

BNPL is a misunderstood form of credit. In fact, many consumers are unaware that it is credit at all and view it simply as a mode of payment. This guide debunks common BNPL myths to explain what BNPL data will mean for lenders and consumers. In the past year, Experian collected more than 130 million buy now, pay later (BNPL) records from four major BNPL fintech lenders and conducted the most comprehensive analysis of BNPL data available today. The results provided valuable insights on: Who are the consumers using BNPL loans? What is the nature of their current mainstream credit relationships? What do their current BNPL behaviors look like? BNPL myth-busting: Who’s using it, how much are they spending and how risky are BNPL loans? Since BNPL launched in the United States in the 2010s, BNPL has exploded into the consciousness of online shoppers, especially during the COVID-19 pandemic. According to Forrester, Millennials are the biggest adopters of BNPL at 18%, followed by their younger counterparts in Gen Z at 11%.1 But looking at statistics like these without additional analysis could be problematic. The dramatic growth of leading BNPL fintechs such as Klarna, Affirm and Afterpay has demonstrated how strongly these services resonate with consumers and retailers. The growth of BNPL has attracted the attention of established lenders interested in capitalizing on the popularity of these services (while also looking to minimize its impact on their existing services, such as credit cards or personal loans). Meanwhile, the Consumer Financial Protection Bureau (CFPB) has urged caution about potential risks, calling for more consistent consumer protections market-wide and transparency into consumer debt accumulation and overextension across lenders. The underlying assumptions debated are that BNPL is used: Predominantly by young people with limited incomes and credit history To pay for frequent, low-value purchases using a cheap and readily available source of credit As a result, it is often seen as a riskier form of lending. But are these assumptions correct? Using data from more than 130 million BNPL transactions from four leading BNPL fintech lenders, we’ve obtained a more detailed and comprehensive understanding of BNPL users and their defining features. Our findings look somewhat different to the popular stereotypes. Myth 1: BNPL is used only for low-value purchases According to our analysis, most BNPL purchases, 95 percent are for items costing $300 or less.2 Some of it is low-value, but not all. In fact, we found that the average purchase using BNPL was similar to that of a credit card, at $132.Average transaction sizes have increased 10 percent year-over-year, and we now see BNPL purchases for goods costing well over $1,000. We also see that consumers take out an average of 5 BNPL loans in a year and 23 percent of them have loans with more than one BNPL provider at a time. Myth 2: BNPL is simply an easier payment method Consumers see BNPL as a simple, quick and convenient way to pay. But, as shoppers receive goods for which payment is deferred, it’s also a form of credit. However, unlike short-term high-interest loans, BNPL credit comes at zero cost to the borrower, with some, but not all BNPL fintech providers charging late payment fees – fueling many borrowers’ sense that it’s an easy way to pay, rather than a loan. Myth 3: Only Gen Z shoppers aged 25 and below are using BNPL Younger shoppers are slightly more represented in the data transactions, but our analysis shows consumers of all ages use BNPL. BNPL is going mainstream, and its appeal is widening. The average age of BNPL consumers is 36 years old, with an average credit history of 9 years.2 The ease of use of these services at the checkout means they have a broad appeal. Over half of U.S. adults have reported using a BNPL service at least once. Despite Millennials and Gen Z having used BNPL financing the most, Gen Xers are not too far behind in usage, with 52% having used it.2 We anticipate that in the use of BNPL will continue to grow as more customers become more familiar with the benefits, and the diversification of products continues. Understanding the opportunities this growth presents to both consumers and lenders is critical to protecting their interests. And helping to facilitate access to credit, enabling responsible spending, while also limiting risks and providing services that consumers can afford is also critical. Download the full guide for additional myths we’re exposing We will take a deep dive into what our early data analysis suggests about the market and the BNPL myths our analysis is exposing. Additionally, we will examine: Why BNPL data matters to providers and lenders How BNPL data can improve visibility of consumers’ creditworthiness Ways in which transparency of BNPL data could benefit consumers 1The Buy Now, Pay Later (BNPL) Opportunity,” Forrester Report, April 29, 2022.2Experian data and analytics derived from 130M+ BNPL transactions

Believe it or not, 2023 is underway, and the new year could prove to be a challenging one for apartment operators in certain ways. In 2021 and into the beginning of 2022, demand for apartment rentals approached record levels, which shrunk vacancy rates and increased monthly rents. The rest of the year remained stagnant while other regions saw some decline, but inflation and other economic factors have many apartment communities confronted with labor shortages, and other challenges which can certainly make leasing and operating properties difficult. Against that backdrop, here are some of the technologies and solutions operators should consider for optimizing their success and efficiencies in 2023 and beyond. Tools that allow prospective residents to have a fully digital and contactless leasing experience — During the pandemic, many operators rushed to implement virtual tours, onsite self-guided tours and other solutions that allowed prospects to apply for and finalize their leases remotely. Prospective renters have undoubtedly grown fond of navigating the leasing process from their homes and taking self-guided tours when onsite, and the demand for digital solutions will surely continue even after COVID distancing is no longer a factor. Therefore, apartment owners and operators should think of these capabilities as long-term investments and always seek ways to optimize the digital leasing experience they provide. Along those lines, forward-thinking operators are employing solutions that allow them to embed credit functionality into their websites and mobile apps using modern, RESTful APIs like the Experian ConnectSM API. Not only does it enhance the information included in a lease application with credit report data, but it also allows prospective renters to easily apply for more than one property at once, enhancing their experience at the same time. Automated lease application form fill — By using information entered by a lease applicant (such as first name, last name, postal code and the last four digits of a Social Security number), this technology uses information from credit files to automatically fill other data fields in a lease application. This tool reduces the effort required by prospective renters to complete the application process, resulting in a better user experience, faster completions, greater accuracy and reduced application abandonment. Automated verification of income, assets, and employment — These solutions eliminate the need for associates to manually verify these components of a lease application. Manual verification is both time-consuming and prone to human error. In addition, automated tools eliminate the opportunity for applicants to supply falsified supporting documentation. The best part about verification is the variety of options available; leasing managers can pick and choose verification options that meet their needs. Renter Risk Score™ and custom-built scores and models applying RentBureau data — These options offer a score designed expressly to predict the likelihood that an applicant will pay rent. Renter risk score can be purchased with preset score logic, or for high-volume decisions, a model can be built calibrated for your specific leasing decisioning needs. A rental payment history report — The RentBureau Consumer Profile tool can provide detailed insight into a lease applicant's history of meeting their lease obligations, which is invaluable information during the lease application process. Having a tool to report rental payment histories to credit bureaus can be a powerful financial amenity. By reporting these payments, operators can help residents build credit histories and improve financial well-being. Such an amenity can attract and retain residents and provide them with a powerful incentive to pay rent on time and in full. In the end, tools that seek to manage risk and create improved experiences for prospective renters have a multitude of benefits. They create meaningful efficiencies for onsite staff by greatly reducing the time, resources and paperwork required to process applications and verify applicant information. This gives overextended associates more time to handle their many other responsibilities. Beyond just efficiency savings, these technologies and solutions also can help operators avoid the complications and loss of income that result from evictions. In fact, the National Association of Realtors estimates that average eviction costs $7,685. Managing risk and providing the best possible customer experience should always be top of mind for rental housing operators. And with the solutions outlined above, they can effectively accomplish those goals in 2023 and beyond.

Alternative credit scoring has become mainstream. Lenders that use alternative credit scores can find opportunities to expand their lending universe without taking on additional risk and more accurately assess the credit risk of traditionally scoreable consumers. Obtaining a more holistic consumer view can help lenders improve automation and efficiency throughout the customer lifecycle. What is alternative credit scoring? Alternative credit scoring models incorporate alternative credit data* that isn't typically found on consumer credit reports. These scores aren't necessarily trying to predict alternative outcomes. The goal is the same — to understand the likelihood that a borrower will miss payments in the future. What's different is the information (and sometimes the analytical techniques) that inform these predictions.Traditional credit scoring models solely consider information found in consumer credit reports. There's a lot of information there — Experian's consumer credit database has data on over 245 million consumers. But although traditional consumer data can be insightful, it doesn't necessarily give lenders a complete picture of consumers' creditworthiness. Alternative credit scores draw from additional data sources, including: Alternative financial services: Credit data from alternative financial services (AFS) can tell you about consumers' experiences with small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Buy Now Pay Later: Buy Now Pay Later (BNPL) borrowing is popular with consumers across the scoring spectrum, and lenders can use access to open BNPL loans to better assess consumers' current capacity. Rental payments: Landlords, property managers, collection companies, rent payment services and consumer-permissioned data can give lenders access to consumers' rent payment history. Full-file public records: Credit reports generally only include bankruptcy records from the previous seven to ten years. However, lenders with access to full-file public records can also learn about consumers' property deeds, address history, and professional and occupational licenses. READ: Take a deep dive into Experian's State of Alternative Credit Data report to learn more about the different types of alternative credit data and uses across the loan lifecycle. With open banking, consumers can now easily and securely share access to their banking and brokerage account data — and they're increasingly comfortable doing so. In fact, 70% would likely share their banking data for better loan rates, financial tools or personalized spending insights.Tools like Experian Boost allow consumers to add certain types of positive payment information to their Experian credit reports, including rent, utility and select streaming service payments. Some traditional scores consider these additional data points, and users have seen their FICO Score 8 from Experian boosted by an average of 13 points.1 Experian Go also allows credit invisible consumers to establish a credit report with consumer-permissioned alternative data. The benefits of using alternative credit data The primary benefit for lenders is access to new borrowers. Alternative credit scores help lenders accurately score more consumers — identifying creditworthy borrowers who might otherwise be automatically denied because they don't qualify for traditional credit scores. The increased access to credit may also align with lenders' financial inclusion goals.Lenders may additionally benefit from a more precise understanding of consumers who are scoreable. When integrated into a credit decisioning platform, the alternative scores could allow lenders to increase automation (and consumers' experiences) without taking on more credit risk. The future of alternative credit scoring Alternative credit scoring might not be an alternative for much longer, and the future looks bright for lenders who can take advantage of increased access to data, advanced analytics and computing power.Continued investment in alternative data sources and machine learning could help bring more consumers into the credit system — breaking barriers and decreasing the cost of basic lending products for millions. At the same time, lenders can further customize offers and automate their operations throughout the customer lifecycle. Partnering with Experian Small and medium-sized lenders may lack the budget or expertise to unlock the potential of alternative data on their own. Instead, lenders can turn to off-the-shelf alternative models that can offer immediate performance lifts without a heavy IT investment.Experian's Lift PlusTM score draws on industry- leading mainstream credit data and FCRA-regulated alternative credit data to provide additional consumer behavior insights. It can score 49% of mainstream credit-invisible consumers and for thin file consumers with a new trade, a 29% lift in scoreable accounts. Learn more about our alternative credit data scoring solutions. Learn more * When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions as regulated by the Fair Credit Reporting Act (FCRA). Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.1Experian (2023). Experian Boost

Whether your goal is to gain new business or create cross-sell opportunities, being proactive in your credit marketing approach can help drive higher response rates and more meaningful customer experiences. But without knowing when your ideal customers are actively seeking credit, you may risk losing business to lenders who have already engaged. So, how can you identify new opportunities when they occur? Given that 91% of consumers say they’re more likely to shop with brands that provide relevant offers, you’ll need to reach the right consumers at the right moment to increase response rates and stay ahead of competitors. Event-based credit triggers can help you identify new tradelines, inquiries and certain loans nearing term to locate highly responsive, credit-active individuals. By receiving updates on consumers’ recent credit activities, you can make firm credit offers immediately so you never miss an opportunity. Case Study: Deliver timely offers with credit trigger leads Vantage West Credit Union serves over 170,000 members across Arizona. With their members looking elsewhere for their mortgage needs, Vantage West aimed to drive as many of these members back to the credit union as possible. To do this, they looked for a solution that could help them identify and target members who are in the market for a new mortgage. By augmenting their prescreen process with Experian’s Prospect Triggers for mortgages, the credit union was able to quickly pinpoint consumers that not only met their credit criteria but were also likely to respond to their credit offers. Within two years of implementing Prospect Triggers, Vantage West funded an additional $18 million in mortgages and is continuing to grow by making timely offers to credit-active prospects. Prospect Triggers is available for banks, credit card issuers, mortgage lenders, retailers and automotive lenders. To learn how Experian can help bring precision and profitability to your credit marketing campaigns, read the full case study or visit us. Download the case study Visit us

From awarding bonus points on food delivery purchases to incorporating social media into their marketing efforts, credit card issuers have leveled up their acquisition strategies to attract and resonate with today’s consumers. But as appealing as these rewards may seem, many consumers are choosing not to own a credit card because of their inability to qualify for one. As card issuers go head-to-head in the battle to reach and connect with new consumers, they must implement more inclusive lending strategies to not only extend credit to underserved communities, but also grow their customer base. Here’s how card issuers can stay ahead: Reach: Look beyond the traditional credit scoring system With limited or no credit history, credit invisibles are often overlooked by lenders who rely solely on traditional credit information to determine applicants’ creditworthiness. This makes it difficult for credit invisibles to obtain financial products and services such as a credit card. However, not all credit invisibles are high-risk consumers and not every activity that could demonstrate their financial stability is captured by traditional data and scores. To better evaluate an applicant’s creditworthiness, lenders can leverage expanded data sources, such as an individual’s cash flow or bank account activity, as an additional lens into their financial health. With deeper insights into consumers’ banking behaviors, card issuers can more accurately assess their ability to pay and help historically disadvantaged populations increase their chances of approval. Not only will this empower underserved consumers to achieve their financial goals, but it provides card issuers with an opportunity to expand their customer base and improve profitability. Connect: Become a financial educator and advocate Credit card issuers looking to build lifelong relationships with new-to-credit consumers can do so by becoming their financial educator and mentor. Many new-to-credit consumers, such as Generation Z, are anxious about their finances but are interested in becoming financially literate. To help increase their credit understanding, card issuers can provide consumers with credit education tools and resources, such as infographics or ‘how-to’ guides, in their marketing campaigns. By learning about the basics and importance of credit, including what a credit score is and how to improve it, consumers can make smarter financial decisions, boost their creditworthiness, and stay loyal to the brand as they navigate their financial journeys. Accessing credit is a huge obstacle for consumers with limited or no credit history, but it doesn’t have to be. By leveraging expanded data sources and offering credit education to consumers, credit card issuers can approve more creditworthy applicants and unlock barriers to financial well-being. Visit us to learn about how Experian is helping businesses grow their portfolios and drive financial inclusion. Visit us

Millions of consumers are excluded from the credit economy, whether it’s because they have limited credit history, dated information within their credit file, or are a part of a historically disadvantaged group. Without credit, it can be difficult for consumers to access the tools and services they need to achieve their financial goals. This February, Experian surveyed over 1,000 consumers across census demographics, including income, ethnicity, and age, to understand the perceptions, needs, and barriers underserved communities face along their credit journey. Our research found that: 75% of consumers with an average household income of less than $50,000 have less than $1,000 in savings. 1 in 5 consumers with an average household income of less than $35,000 say they’re confident in getting approved for credit. 80% of respondents who are not or slightly confident in getting approved for credit were women. When asked why they believed they would not get approved for credit, participants shared common responses, such as having poor payment history, a low credit score, and insufficient income. Given these findings, what can lenders provide to help underserved consumers strengthen their financial profiles and gain access to the credit they need and deserve? The power of credit education While only 20% of respondents were familiar with credit education tools, the majority expressed interest in these offerings. With Experian, lenders can develop and implement credit education programs, tools, and solutions to help consumers understand their credit and the impact certain choices can have on their credit scores. From interactive tools like Score Simulator and Score Planner to real-time alerts from Credit Monitoring, consumers can actively assess their financial health, take steps to improve their creditworthiness, and ultimately become better candidates for credit offers. In turn, consumers can feel more confident and empowered to achieve their financial goals. Credit education tools not only help consumers increase their credit literacy, confidence, and chances of approval, but they also create opportunities for lenders to build lasting customer relationships. Consumers recognize that healthy credit plays an important role in their financial lives, and by helping them navigate the credit landscape, lenders can increase engagement, build loyalty, and enhance their brand’s reputation as an organization that cares about their customers. Empowering consumers with credit education is also a way for lenders to unlock new revenue streams. By learning to borrow, save, and spend responsibly, consumers can improve their creditworthiness and be in a better position to accept extended credit offerings, driving more cross-sell and upsell opportunities for lenders. More ways experian can help Experian is deeply committed to helping marginalized and low-income communities access the financial resources they need. In addition to our credit education tools, here are a few of our other offerings: Our expanded data helps lenders make better lending decisions by providing greater visibility and transparency around a consumer’s inquiry and payment behaviors. With a holistic view of their current and prospective customers, lenders can more accurately identify creditworthy applicants, uncover new growth opportunities, and expand access to credit for underserved consumers. Experian GoTM is a free, first-of-its-kind program to help credit invisibles and those with limited credit histories begin building credit on their own terms. After authenticating their identities and obtaining an Experian credit report, users will receive ongoing education about how credit works and recommendations to further build their credit history. To learn more about building profitable customer relationships with credit education, check out our credit education solutions and watch our Three Ways to Uncover Financial Growth Opportunities that Benefit Underserved Communities webinar. Learn more Watch webinar

As more consumers apply for credit and increase their spending1, lenders and financial institutions have an opportunity to expand their portfolios and improve profitability. The challenge is ensuring they’re extending credit responsibly and inclusively. Millions of Americans, many of whom are creditworthy, lack access to mainstream credit options. This may be because they have limited or no credit history, negative information within their credit file, or are a part of a historically disadvantaged group. To say “yes” to consumers they otherwise couldn’t or wouldn’t lend to, lenders must gain a deeper understanding of an individual’s stability, ability and willingness to pay. That’s where expanded FCRA-regulated and trended data come in. While traditional credit data has long been the primary means of gauging creditworthiness, it doesn’t tell the full story of a consumer’s financial situation. Let’s explore how differentiated data can help lenders make more informed credit decisions. Using differentiated data for deeper lending Expanded FCRA-regulated data provides supplemental credit data to help lenders gain a more holistic view of their current and prospective customers. Some examples of expanded FCRA-regulated data include alternative financial services data from nontraditional lenders, consumer-permissioned account data, rental payments and full-file public records. Because this data drives greater visibility and transparency around inquiry and payment behaviors, lenders can more accurately determine a consumer’s ability to pay and distinguish between reliable and high-risk applicants. In turn, lenders can approve more creditworthy consumers, grow their portfolios and increase financial opportunities for underserved communities, all while preventing and mitigating risk. 89% of lenders agree that expanded FCRA-regulated data allows them to extend credit to more consumers. Trended data empowers lenders with predictive insights into consumers by providing key balance and payment data for the previous 24 months. This is important as lenders can determine if a consumer’s credit behavior has improved or deteriorated over time. In turn, lenders can: Identify creditworthy customers: Establish if a consumer has a demonstrated ability to pay, is consistently paying more than the minimum payment, or shows no signs of payment stress. Increase response rates: Match the right products with the right prospects. Determine upsell and cross-sell opportunities: Present relevant offers based on anticipated needs and behaviors. Limit loss exposure: Understand the direction and velocity of payment performance to effectively manage risk exposure. Trended data helps lenders better predict future behavior, manage portfolio risk and design the best marketing offers. Turning insights into action Together, trended and expanded FCRA-regulated data benefit lenders and consumers alike. With a more holistic view of their customers, lenders gain powerful insights to lend deeper, ultimately helping them to expand their portfolios and drive greater access to credit for underserved communities. Learn more 1 The Recovery of Credit Applications to Pre-Pandemic Levels, Consumer Financial Protection Bureau, 2021.

As industry experts are still unsure when the economy will fully recover, re-entry into marketing preapproved credit offers seems like a far-off proposal. However, several of the top credit card issuers are already mailing prescreen offers, with many other lenders following suit. When the time comes for organizations to resume, or even expand this type of targeting, odds are that the marketing budget will be tighter than in the past. To make the most of the limited available marketing spend, lenders will need to be more prescriptive with their selection process to increase response rates on fewer delivered offers. Choosing the best candidates to receive these offers, from a credit risk perspective, will be critical. With delinquencies being suppressed due to CARES Act reporting guidelines, identifying consumers with the ability to repay will require additional assessment of recent credit behavior metrics, such as actual payment amounts and balance migration. Along with the presence of explicit indicators of accommodated trades (trades affected by natural disaster, trades with a balance but no scheduled payment amount) on a prospect’s credit file, their recent trends in payments and balance shifts can be integral in determining whether a prospect has been adversely impacted by today’s economic environment. Once risk criteria have been developed using a mix of bureau scores (like the VantageScore® credit score), traditional credit attributes and trended attributes measuring recent activity, additional targeting will be critical for selecting a population that’s most likely to open the relevant trade type. For credit cards and personal installment loans, response performance can be greatly improved by aligning product offers with prospects based on their propensity to revolve, pay in full each month or consolidate balances. Additionally, the process to select final prospects should integrate a propensity to open/respond assessment for the specific offering. While many lenders have custom models developed on previous internal response performance, off-the-shelf propensity to open models are also available to provide an assessment of a prospect’s likelihood to open a particular type of trade in the coming months. These models can act as a fast-start for lenders that intend to develop internal custom models, but don’t have the response performance within a particular product/geography/risk profile. They are also commonly used as a long-term solution for lenders without an internal model development team or budget for an outsourced model. Prescreen selection best practices Identify geography and traditional credit risk assessment of the prospect universe. Overlay attributes measuring accommodated trades and recent payment/balance trends to identify prospects with indications of ability to pay. Segment the prospect universe by recent credit usage to determine products that would resonate. Make final selections using propensity to open model scores to increase response rates by only making offers to consumers who are likely looking for new credit offers. While the best practices listed above don’t represent a risk-free approach in these uncertain times, they do provide a framework for identifying prospects with mitigated repayment risk and insights into the appropriate credit offer to make and when to make it. Learn about in the market models Learn about trended attributes VantageScore® is a registered trademark of VantageScore Solutions, LLC.

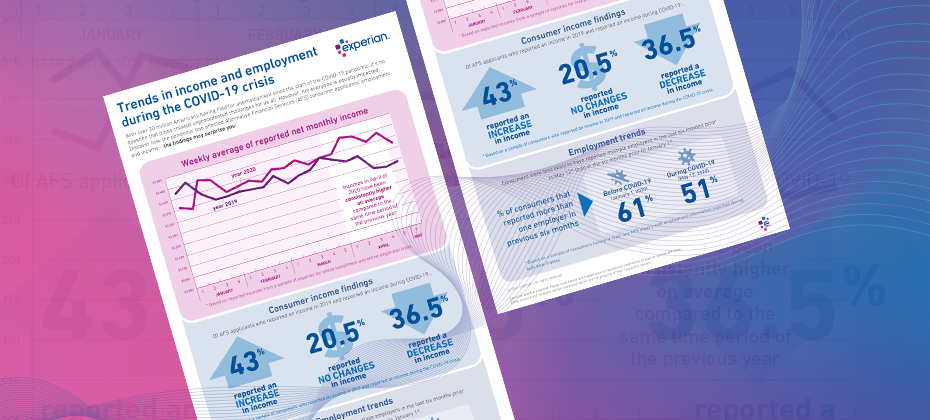

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

In the face of severe financial stress, such as that brought about by an economic downturn, lenders seeking to reduce their credit risk exposure often resort to tactics executed at the portfolio level, such as raising credit score cut-offs for new loans or reducing credit limits on existing accounts. What if lenders could tune their portfolio throughout economic cycles so they don’t have to rely on abrupt measures when faced with current or future economic disruptions? Now they can. The impact of economic downturns on financial institutions Historically, economic hardships have directly impacted loan performance due to differences in demand, supply or a combination of both. For example, let’s explore the Great Recession of 2008, which challenged financial institutions with credit losses, declines in the value of investments and reductions in new business revenues. Over the short term, the financial crisis of 2008 affected the lending market by causing financial institutions to lose money on mortgage defaults and credit to consumers and businesses to dry up. For the much longer term, loan growth at commercial banks decreased substantially and remained negative for almost four years after the financial crisis. Additionally, lending from banks to small businesses decreased by 18 percent between 2008-2011. And – it was no walk in the park for consumers. Already faced with a rise in unemployment and a decline in stock values, they suddenly found it harder to qualify for an extension of credit, as lenders tightened their standards for both businesses and consumers. Are you prepared to navigate and successfully respond to the current environment? Those who prove adaptable to harsh economic conditions will be the ones most poised to lead when the economy picks up again. Introducing the FICO® Resilience Index The FICO® Resilience Index provides an additional way to evaluate the quality of portfolios at any point in an economic cycle. This allows financial institutions to discover and manage potential latent risk within groups of consumers bearing similar FICO® Scores, without cutting off access to credit for resilient consumers. By incorporating the FICO® Resilience Index into your lending strategies, you can gain deeper insight into consumer sensitivity for more precise credit decisioning. What are the benefits? The FICO® Resilience Index is designed to assess consumers with respect to their resilience or sensitivity to an economic downturn and provides insight into which consumers are more likely to default during periods of economic stress. It can be used by lenders as another input in credit decisions and account strategies across the credit lifecycle and can be delivered with a credit file, along with the FICO® Score. No matter what factors lead to an economic correction, downturns can result in unexpected stressors, affecting consumers’ ability or willingness to repay. The FICO® Resilience Index can easily be added to your current FICO® Score processes to become a key part of your resilience-building strategies. Learn more

Article written by Alex Lintner, Experian's Group President of Consumer Information Services and Sandy Anderson, Experian's Senior Vice President of Client and Sales Operations Many consumers are facing financial stress due to unemployment and other hardships related to the COVID-19 pandemic. Not surprisingly, data scientists at Experian are looking into how consumers’ credit scores may be impacted during the COVID-19 national emergency period as financial institutions and credit bureaus follow guidance from financial regulators and law established in Section 4021 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). In a nutshell, Experian finds that if consumers contact their lenders and are granted an accommodation, such as a payment holiday or forbearance, and lenders report the accommodation accordingly, consumer scores will not be materially affected negatively. It’s not just Experian’s findings, but also those of the major credit scoring companies, FICO® and VantageScore®. FICO has reported that if a lender provides an accommodation and payments are reported on time consistent with the CARES Act, consumers will not be negatively impacted by late payments related to COVID-19. VantageScore® has also addressed this issue and stated that its models are designed to mitigate the impact of missed payments from COVID-19. At the same time, if as predicted, lenders tighten underwriting standards following 11 consecutive years of economic growth, access to credit for some consumers may be curtailed notwithstanding their score because their ability to repay the loan may be diminished. Regulatory guidance and law provide a robust response Recently, the Federal Reserve, along with the federal and state banking regulators, issued a statement encouraging mortgage servicers to work with struggling homeowners affected by the COVID-19 national emergency by allowing borrowers to defer mortgage payments up to 180-days or longer. The Federal Deposit Insurance Corporation stated that financial institutions should “take prudent steps to assist customers and communities affected by COVID-19.” The Office of the Comptroller of the Currency, which regulates nationally chartered banks, encouraged banks to offer consumers payment accommodations to avoid delinquencies and negative credit bureau reporting. This regulatory guidance was backed by Congress in passing the CARES Act, which requires any payment accommodations to be reported to a credit bureau as “current.” The Consumer Financial Protection Bureau, which has oversight of all financial service providers, reinforced the regulatory obligation in the CARES Act. In a statement, the Bureau said “the continuation of reporting such accurate payment information produces substantial benefits for consumers, users of consumer reports and the economy as a whole.” Moreover, the consumer reporting industry has a history of successful coordination during emergency circumstances, like COVID-19, and we’ve provided the support necessary for lenders to report accurately and consistent with regulatory guidance. For example, when a consumer faces hardship, a lender can add a code that indicates a customer or borrower has been “affected by natural or declared disaster.” If a lender uses this or a similar code, a notification about the disaster or other event will appear in the credit report with the trade line for the customer’s account and will remain on the trade line until the lender removes it. As a result, the presence of the code will not negatively impact the consumer credit score. However, other factors may impact a consumer’s score, such as an increase in a consumer’s utilization of their credit lines, which is a likely scenario during a period of financial stress. Suppression or Deletion of late payments will hurt, not help, credit scores In response to the nationwide impact of COVID-19, some lawmakers have suggested that lenders should not report missed payments or that credit bureaus should delete them. The presumption is that these actions would hold consumers harmless during the crisis caused by this pandemic. However, these good intentions end up having a detrimental impact on the whole credit ecosystem as consumer credit information is no longer accurately reflecting consumers’ specific situation. This makes it difficult for lenders to assess risk and for consumers to obtain appropriately priced credit. Ultimately, the best way to help is a consumer-specific solution, meaning one in which a lender reaches an accommodation with each affected individual, and accurately reflects that person’s unique situation when reporting to credit bureaus. When a consumer misses a payment, the information doesn’t end up on a credit report immediately. Most payments are monthly, so a consumer’s payment history with a financial institution is updated on a similar timeline. If, for example, a lender was required to suppress reporting for three months during the COVID-19 national emergency, the result would be no data flowing onto a credit report for three months. A credit report would therefore show monthly payments and then three months of no updates. The same would be true if a credit reporting agency were required to suppress or delete payment information. The lack of data, due to suppression or deletion, means that lenders would be blinded when making credit decisions, for example to increase a credit limit to an existing customer or to grant a new line of credit to a prospective customer. When faced with a blind spot, and unable to assess the real risk of a consumer’s credit history, the prudential tendency would be to raise the cost of credit, or to decrease the availability of credit, to cover the risk that cannot be measured. This could effectively end granting of credit to new customers, further stifling economic recovery and consumer financial health at a time when it’s needed most. Beyond the direct impact on consumers, suppression or deletion of credit information could directly affect the safety and soundness of the nation’s consumer and small business lending system. With missing data, lenders and their regulators would be flying blind as to the accurate information about a consumer’s risk and could result in unknowingly holding loan portfolios with heightened risk for loss. Too many unexpected losses threaten the balance of the financial system and could further seize credit markets. Experian is committed to helping consumers manage their credit and working with lenders on how best to report consumer-specific solutions. To learn more about what consumers can do to manage credit during the COVID-19 national emergency, we’ve provided resources on our website. For individuals looking to explore options their lenders may offer, we’ve included links to many of the companies and update them continuously. With good public policy and consumer-specific solutions, consumers can continue to build credit and help our economy grow.

In today’s rapidly changing economic environment, the looming question of how to reduce portfolio volatility while still meeting consumers' needs is on every lender’s mind. So, how can you better asses risk for unbanked consumers and prime borrowers? Look no further than alternative credit data. In the face of severe financial stress, when borrowers are increasingly being shut out of traditional credit offerings, the adoption of alternative credit data allows lenders to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure without unnecessarily impacting insensitive or more “resilient” consumers. What is alternative credit data? Millions of consumers lack credit history or have difficulty obtaining credit from mainstream financial institutions. To ease access to credit for “invisible” and subprime consumers, financial institutions have sought ways to both extend and improve the methods by which they evaluate borrowers’ risk. This initiative to effectively score more consumers has involved the use of alternative credit data.1 Alternative credit data is FCRA-regulated data that is typically not included in a traditional credit report and helps lenders paint a fuller picture of a consumer, so borrowers can get better access to the financial services they need and deserve. How can it help during a downturn? The economic environment impacts consumers’ financial behavior. And with more than 100 million consumers already restricted by the traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By pulling in alternative credit data, such as consumer-permissioned data, rental payments and full-file public records, lenders can gain a holistic view of current and future customers. These insights help them expand their credit universe, identify potential fraud and determine an applicant’s ability to pay all while mitigating risk. Plus, many consumers are happy to share additional financial information. According to Experian research, 58% say that having the ability to contribute positive payment history to their credit files makes them feel more empowered. Likewise, many lenders are already expanding their sources for insights, with 65% using information beyond traditional credit report data in their current lending processes to make better decisions. By better assessing risk at the onset of the loan decisioning process, lenders can minimize credit losses while driving greater access to credit for consumers. Learn more 1When we refer to “Alternative Credit Data,” this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.

Originally posted by Experian Global News blog At Experian, we have an unwavering commitment to helping consumers and clients manage through this unprecedented period. We are actively working with consumers, lenders, lawmakers and regulators to help mitigate the potential impact on credit scores during times of financial hardship. In response to the urgent and rapid changes associated with COVID-19, we are accelerating and enhancing our financial education programming to help consumers maintain good credit and gain access to the financial services they need. This is in addition to processes and tools the industry has in place to help lenders accommodate situations where consumers are affected by circumstances beyond their control. These processes will be extended to those experiencing financial hardship as a result of COVID-19. As the Consumer’s Credit Bureau, our commitment at Experian is to inform, guide and protect our consumers and customers during uncertain times. With expected delays in bill payments, unprecedented layoffs, hiring freezes and related hardships, we are here to help consumers in understanding how the credit reporting system and personal finance overall will move forward in this landscape. One way we’re doing this is inviting everyone to join our special eight-week series of #CreditChat conversations surrounding COVID-19 on Wednesdays at 3 p.m. ET on Twitter. Our weekly #CreditChat program started in 2012 to help the community learn about credit and important personal finance topics (e.g. saving money, paying down debt, improving credit scores). The next several #CreditChats will be dedicated to discussing ways to manage finances and credit during the pandemic. Topics of these #CreditChats will include methods and strategies for bill repayment, paying down debt, emergency financial assistance and preparing for retirement during COVID-19. “As the consumer’s credit bureau, we are committed to working with consumers, lenders and the financial community during and following the impacts of COVID-19,” says Craig Boundy, Chief Executive Officer of Experian North America. “As part of our nation’s new reality, we are planning for options to help mitigate the potential impact on credit scores due to financial hardships seen nationwide. Our #CreditChat series and supporting resources serve as one of several informational touchpoints with consumers moving forward.” Being fully committed to helping consumers and lenders during this unprecedented period, we’ve created a dedicated blog page, “COVID-19 and Your Credit Report,” with ongoing and updated information on how COVID-19 may impact consumers’ creditworthiness and – ultimately – what people should do to preserve it. The blog will be updated with relevant news as we announce new solutions and tactics. Additionally, our “Ask Experian” blog invites consumers to explore immediate and evolving resources on our COVID-19 Updates page. In addition to this guidance, and with consumer confidence in the economy expected to decline, we will be listening closely to the expert voices in our Consumer Council, a group of leaders from organizations committed to helping consumers on their financial journey. We established a Consumer Council in 2009 to strengthen our relationships and to initiate a dialogue among Experian and consumer advocacy groups, industry experts, academics and other key stakeholders. This is in addition to ongoing collaboration with our regulators. Additionally, our Experian Education Ambassador program enables hundreds of employee volunteers to serve as ambassadors sharing helpful information with consumers, community groups and others. The goal is to help the communities we serve across North America, providing the knowledge consumers need to better manage their credit, protect themselves from fraud and identity theft and lead more successful, financially healthy lives. COVID-19 has impacted all industries and individuals from all walks of life. We want our community to know we are right there with you. Learn more about our weekly #CreditChat and upcoming schedule here. Learn more

There are more than 100 million people in the United States who don’t have a fair chance at access to credit. These people are forced to rely on high-interest credit cards and loans for things most of us take for granted, like financing a family car or getting an apartment. At Experian, we have a fundamental mission to be a champion for the consumer. Our commitment to increasing financial inclusion and helping consumers gain access to the financial services they need is one of the reasons we have been selected as a Fintech Breakthrough Award winner for the third consecutive year. The Fintech Breakthrough Awards is the premier awards program founded to recognize the fintech innovators, leaders and visionaries from around the world. The 2020 Fintech Breakthrough Award program attracted more than 3,750 nominations from across the globe. Last year, Experian took home the award for Best Overall Analytics Platform for our Ascend Analytical Sandbox™, a first-to-market analytics environment that promised to move companies beyond just business intelligence and data visualization to data insights and answers they could use. The year prior, Experian won the Consumer Lending Innovation Award for our Text for Credit™ solution, a powerful tool for providing consumers the convenience to securely bypass the standard-length ‘pen & paper’ or keystroke intensive credit application process while helping lenders make smart, fraud protected lending decisions. This year, we are excited to announce that Experian has been selected once again as a winner in the Consumer Lending Innovation category for Experian Boost™. Experian Boost – with direct, active consumer consent – scans eligible accounts for ‘boostable’ positive payment data (e.g., utility and telecom payments) and provides the means for consumers to add that data to their Experian credit reports. Now, for the very first time, millions of consumers benefit from payments they’ve been making for years but were never reflected on their credit reports. Since launching in March 2019, cumulatively, more than 18 million points have been added to FICO® Scores via Experian Boost. Two-thirds of consumers who completed the Experian Boost process increased their FICO Score and among these, the average score increase has been more than 13 points, and 12% have moved up in credit score category. “Like many fintechs, our goal is to help more consumers gain access to the financial services they need,” said Alex Lintner, Group President of Experian Consumer Information Services. “Experian Boost is an example of our mission brought to life. It is the first and only service to truly put consumers in control of their credit. We’re proud of this recognition from Fintech Breakthrough and the momentum we’ve seen with Experian Boost to date.” Contributing consumer payment history to an Experian credit file allows fintech lenders to make more informed decisions when examining prospective borrowers. Only positive payment histories are aggregated through the platform and consumers can remove the new data at any time. There is no limit to how many times one can use Experian Boost to contribute new data. For more information, visit Experian.com/Boost.