Tag: alternative lending

Our State of Alternative Data Report provides insight into the alternative lending market, new data sources and growth opportunities.

Learn how you can grow your portfolio and minimize risk by leveraging industry-leading alternative credit scoring models. Read more!

A move toward inclusive finance, including incorporating alternative data in credit scoring models, is a crucial step towards promoting financial inclusion.

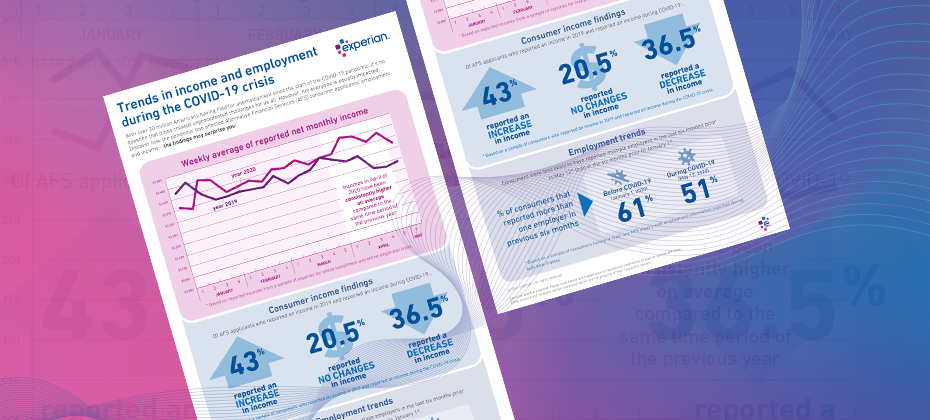

COVID-19 has had far-reaching economic consequences. When it comes to your consumers' finances, are you seeing the full picture?

Since the end of the recession, customer loyalty has been a focus for lenders, given that there are more options for AFS borrowers. Read more!

How are fintechs faring against traditional FIs? Our latest infographic uncovers industry trends and key metrics in unsecured personal installment loans.

It’s important for lenders to get a comprehensive view to find the most qualified candidates. Using alternative credit data can expand your choices.

Four Ways Fintech Has Changed the Lending Process and How Other Financial Institutions Can Keep Up

Apply CIS TagLearn four ways fintech has changed the lending process and how traditional financial institutions and lenders can keep up. Read more!

Break Out of Decision Paralysis: Three Data Points About Alternative Financial Services Data

Apply CIS TagAlternative financial services data gives lenders access to powerful and predictive supplemental credit data that better detect risk and benefits consumers.

Whether it is an online marketplace lender offering to refinance the student loan debt of a recent college graduate or an online small-business lender providing an entrepreneur with a loan when no one else will, there is no doubt innovation in the online lending sector is changing how Americans gain access to credit. This expanding market segment takes great pride in using “next-generation” underwriting and credit scoring risk models. In particular, many online lenders are incorporating noncredit information such as income, education history (i.e., type of degree and college), professional licenses and consumer-supplied information in an effort to strike the right balance between properly assessing credit risk and serving consumers typically shunned by traditional lenders because of a thin credit history. Regulatory concerns The exponential growth of the online lending sector has caught the attention of regulators — such as the U.S. Treasury Department, the Federal Deposit Insurance Corporation, Congress and the California Business Development Office — who are interested in learning more about how online marketplace lenders are assessing the credit risk of consumers and small businesses. At least one official, Antonio Weiss, a counselor to the Treasury secretary, has publicly raised concerns about the use of so-called nontraditional data in the underwriting process, particularly data gleaned from social media accounts. Weiss said that “just because a credit decision is made by an algorithm, doesn’t mean it is fair,” citing the need for lenders to be aware of compliance with fair lending obligations when integrating nontraditional credit data. Innovative and “tried and true” are not mutually exclusive Some have suggested the only way to assuage regulatory concerns and control risk is by using tried-and-true legacy credit risk models. The fact is, however, online marketplace lenders can — and should — continue to push the envelope on innovative underwriting and business models, so long as these models properly gauge credit risk and ensure compliance with fair lending rules. It’s not a simple either-or scenario. Lenders always must ensure their scoring analytics are based upon predictive and accurate data. That’s why lenders historically have relied on credit history, which is based upon data consumers can dispute using their rights under the Fair Credit Reporting Act. Statistically sound and validated scores protect consumers from discrimination and lenders from disparate impact claims under the Equal Credit Opportunity Act. The Office of the Comptroller of the Currency guidance on model risk management is an example of regulators’ focus on holding responsible the entities they oversee for the validation, testing and accuracy of their models. Marketplace lenders who want to push the limit can look to credit scoring models now being used in the marketplace without negatively impacting credit quality or raising fair lending risk. For example, VantageScore® allows for the scoring of 30 million to 35 million more people who currently are unscoreable under legacy credit score models. The VantageScore® credit score does this by using a broader, deeper set of credit file data and more advanced modeling techniques. This allows the VantageScore® credit score model to capture unique consumer behaviors more accurately. In conclusion, online marketplace lenders should continue innovating with their own “secret sauce” and custom decisioning systems that may include a mix of noncredit factors. But they also can stay ahead of the curve by relying on innovative “tried-and-true” credit score models like the VantageScore® credit score model. These models incorporate the best of both worlds by leaning on innovative scoring analytics that are more inclusive, while providing marketplace lenders with assurances the decisioning is both statistically sound and compliant with fair lending laws. VantageScore® is a registered trademark of VantageScore Solutions, LLC.

Last December, American Banker named online marketplace lending its innovation of the year as a result of the “industry’s rapid growth and evolution.” Meanwhile, in 2015, millennials scored headlines in nearly every publication imaginable – industries, politicians and academics all trying to understand and articulate how the now largest-living generation will influence how we work, live and lead. So perhaps it’s no surprise the two hot topics have collided this year. Gen Y is tech-dependent and Internet-enabled. They have increasingly grown to expect the tools and services they use to be available online, including anything and everything in the financial services space. Marketplace lenders are ever-so eager to sweep in and serve. Online and mobile solutions are certainly one thing, but Experian’s latest research reveals this generation is also very receptive to “non-bank” lenders for the ease, speed and accessibility they provide. 47 percent of millennials said they are likely to use alternative finance sources in the near future 57 percent reported they are willing to use alternative companies and services that innovate to meet their needs 13 percent said they’ve already taken out a loan from an alternate or non-bank lender As they come of age, hitting those big milestones – college graduations, marriage, starting families, making home purchases – Gen Y is wading through its financial options. Research and logic suggest millennials will without a doubt have a greater openness toward nontraditional banking, representing a huge market for online marketplace lenders. For the millennial entrepreneurs especially, marketplace lending is proving to be a good fit. “They are on the earlier curve of their small business ownership and entrepreneurial paths,” David Solis, sales performance manager at Bank of America, told CNN Money. “It makes sense they’re going to be pursuing alternative forms of lending.” Affluent millennials are another segment open to alternative financial services. A 2015 LinkedIn study on this specific target stated affluent millennials are particularly likely to envision a cashless, sharing-based economy in the future, where banks no longer serve as their primary financial institutions. Nearly seven out of 10 affluent millennials are likely to consider such offerings outside of the traditional financial services space, compared to just 47 percent of affluent Gen X’ers. The millennial generation may not fully understand all products traditional banks offer, since they rarely set foot in “brick-and-mortar” establishments, but they are a prime market for online investing and lending services. They’re more experimental, more digital, less loyal. In short, they are looking for financial services that are as tech-savvy as they are; those who don’t keep up may get left behind, and online marketplace lenders are certainly positioning themselves to win over this generation. To be most successful in capturing this highly sought-after generation, online marketplace lenders will need to continue to innovate both in terms of differentiating their product offerings and getting more sophisticated in their targeted marketing approach. As the online marketplace continues to expand with more players, heating up with increased competition, segmentation strategies will be key in finding the right borrowers and matching them with the right offer. As we head into 2016, there is no doubt many will continue to monitor the financial services trends emerging. Chances are online marketplace lenders and millennials will likely be attached to many of the headlines. For more information, visit www.experian.com/marketplacelending.