Latest Posts

The holidays can be a stressful time of year for consumers, and also an important time for lenders to anticipate the aftermath of big credit card spend.

It's the holiday season - you've been breached. Fraudsters and other criminals can make one of the busiest shopping times of the year, a miserable one.

How healthy is the auto loan industry? Q3 data show lenders reduce loans to subprime consumers and increase loans to prime consumers

Apply Automotive TagThis quarter’s State of the Automotive Finance Market report provides a stark reality check for anyone making doomsday predictions about a subprime bubble in the auto industry. While delinquent payments are slightly on the rise, data from the report show that the auto lending industry has responded by reining in loans to subprime consumers. Results found that newly originated loans to prime borrowers jumped two percent to encompass nearly 60 percent of auto loans financed in Q3 2016. Moreover, loans extended to consumers in the subprime tier fell 4.5 percent from the previous year, and loans to deep-subprime consumers dropped 2.8 percent to the lowest level on record since 2008. When considering delinquent payments, there’s no extreme cause for concern either as overall 30-day delinquencies remained flat from the previous quarter, and overall 60-day delinquencies showed a slight uptick to 0.74 percent in Q3 2016 (0.67 percent in Q3 2015). The move in Q3 to more prime and super prime customers pushed the average loan scores higher for the first time in four years. For new vehicle loans, the average credit score climbed two points to 712 in Q3 2016, marking the first time average credit scores for new vehicle loans rose since hitting a record high of 723 in Q2 2012. For used-vehicle loans, the average credit score jumped five points from 650 in Q3 2015 to 655 in Q 2016. More notable news in the auto loan market – there was a slight increase in interest rates. Interest rates for the average new vehicle loan went from 4.63 percent in Q3 2015 to 4.69 percent in Q3 2016. This increase played a key role in driving more market share to the credit unions. Credit unions grew their share of the total automotive loan market from 17.6 percent in Q3 2015 to 19.6 percent in Q3 2016. For new vehicle loans specifically, credit unions grew their share by 22 percent, going from 9.9 percent in Q3 2015 to 12 percent in Q3 2016. Other key findings from the Q3 2016 report: Total open automotive loan balances reached a record high of $1.055 billion. Used vehicle loan amounts reached a record high of $19,227, up by $361. The average new vehicle loan amount jumped to $30,022 from $28,936. Share of new vehicle leasing jumped to 29.49 percent from 26.93 percent. The average monthly payment for a new vehicle loan was $495, up from $482. The average new vehicle lease payment was $405, up from $398. The average monthly payment for a used vehicle loan was $362, up from $360. The average loan term for a new vehicle was 68 months. To see the full report results, or to download the webinar and presentation, visit https://www.experian.com/automotive/auto-data.html

let’s look at the increasingly popular smart voice/AI assistant. Here are some insights on how consumers are using Amazon ECHO

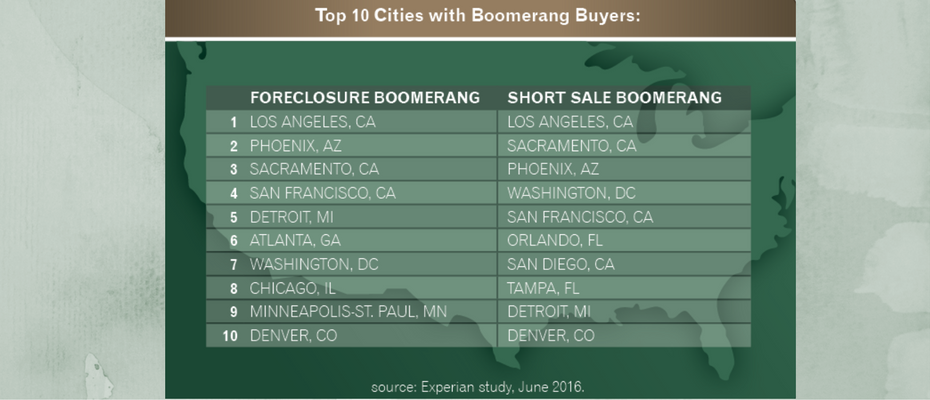

Which part of the country has bragging rights when it comes to sporting the best consumer credit scores? Drum roll please … Honors go to the Midwest. In fact, eight of the 10 cities with the highest consumer credit scores heralded from Minnesota and Wisconsin. Mankato, Minn., earned the highest ranking with an average credit score of 708 and Greenwood, Miss., placed last with an average credit score of 622. Even better news is that the nation’s average credit score is up four points; 669 to 673 from last year and is only six points away from the 2007 average of 679, which is a promising sign as the economy continues to rebound. Experian’s annual study ranks American cities by credit score and reveals which cities are the best and worst at managing their credit, along with a glimpse at how the nation and each generation is faring. “All credit indicators suggest consumers are not as ‘credit stressed’ — credit card balances and average debt are up while utilization rates remained consistent at 30 percent,” said Michele Raneri, vice president of analytics and new business development at Experian. As for the generational victors, the Silents have an average 730, Boomers come in with 700, Gen X with 655 and Gen Y with 634. We’re also starting to see Gen Z emerge for the first time in the credit ranks with an average score of 631. Couple this news with other favorable economic indicators and it appears the country is humming along in a positive direction. The stock market reached record highs post-election. Bankcard originations and balances continue to grow, dominated by the prime borrower. And the housing market is healthy with boomerang borrowers re-emerging. An estimated 2.5 million Americans will see a foreclosure fall of their credit report between June 2016 and June 2017, creating a new pool of potential buyers with improved credit profiles. More than 12 percent who foreclosed back in the Great Recession have already boomeranged to become homeowners again, while 29 percent who experienced a short sale during that same time have also recently taken on a mortgage. “We are seeing the positive effects of economic recovery with the rise in income and low unemployment reflected in how Americans are managing their credit,” said Raneri. Which means all is good in the world of credit. Of course there is always room for improvement, but this year’s 7th annual state of credit reveals there is much to be thankful for in 2016.

Experian Data Breach Resolution releases its fourth annual Data Breach Industry Forecast report with five key predictions on the 2017 data breach landscape

During Thanksgiving 2015, 736 million pounds of turkey were consumed in the United States.

FinCEN and email-compromise fraud sheds additional light on the threats of Email Account Compromise and Business Email Compromise.

personalized subject lines have a 27% higher unique click rate, an 11% higher CTO and more than double the transaction of other promotional mailings

Panel discussion on Reinventing Identity for the Digital Age at Electronic Signature & Records Association (ESRA) conference

Under the updated requirements for Customer Due Diligence, financial institutions must expand programs.

More lenders are turning to VantageScore® to help achieve their goals and reduce risk

For members of the U.S. military, relocating often, returning home following a lengthy deployment and living with uncertainty isn’t easy. It can take an emotional and financial toll, and many are unprepared for their economic reality after they separate from the military. As we honor those who have served our country this Veterans Day, we are highlighting some of the special financial benefits and safeguards available to help veterans. Housing Help One of the best benefits offered to service members is the Veteran’s Administration (VA) home-loan program. Loan rates are competitive, and the VA guarantees up to 25 percent of the payment on the loan, making it one of the only ways available to buy a home with no down payment and no private mortgage insurance. Debt Relief Having a VA loan qualifies military members for a Military Debt Consolidation Loan (MDCL) that can help with overcoming financial difficulties. The MDCL is similar to a debt consolidation loan: take out one loan to pay off all unsecured debts, such as credit cards, medical bills and payday loans, and make a single payment to one lender. The advantage of a MDCL? Paying a lower interest rate and closing costs than civilians and far less interest than paying the same bills with credit cards. These refinancing loans can be spread out over 10, 15 and sometimes 30 years. Education Benefits The GI Bill is arguably the best benefit for veterans and members of the armed forces. It helps service members pay for higher education for themselves and their dependents, and is one of the top reasons people enlist. Eligible service members receive up to 36 months of education benefits, based on the type of training, length of service, college fund availability and whether he or she contributed to a buy-up program while on active duty. Benefits last up to 10 years, but the time limit may be extended. Saving & Investing Money According to the Department of Defense’s annual Demographics Report, 87 percent of military families contribute to a retirement account. Service members who participated in the Thrift Savings Plan, however, are often unaware of their options after they separate from service, and many don’t realize the advantages of rolling their plans into an IRA or retirement plan of a new employer. Safeguarding Identity Everyone is a potential identity theft target, but military personnel and veterans are particularly vulnerable. Routinely reviewing a credit report is one way to detect a breach. The Attorney General's Office provides general information about what steps to take to recover from identify theft or fraud. Today is a great time to consider ways to support your veteran and active military consumers. They are deserving of our support and recognition not just today but continuously. Learn more about services for veterans and active military to understand the varying protections, and how financial institutions can best support military credit consumers and their families.

Experian is recognized as a leading security solution provider for fraud and identity solutions in order to protect customers and financial institutions

Experian analysis shows that 2.5M consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017