Data & Analytics

Learn how to accurately and consistently report on consumers' credit while complying with regulatory guidance during the COVID-19 pandemic.

Learn the benefits of leveraging alternative credit data to better assess risk at the onset of the loan decisioning process. Read more.

Experian’s Commitment to Helping Consumers Protect Their Financial Health During the COVID-19 Pandemic

Data & AnalyticsAt Experian, we are here to help consumers understand how the credit reporting system and personal finance overall will move forward during the pandemic.

Experian Boost™ Wins Consumer Lending Innovation Award in Prestigious Fintech Competition

Data & AnalyticsWe are excited to announce that Experian has been selected as a Fintech Breakthrough Awards winner in the Consumer Lending Innovation category.

Learn more about the terminology around artificial intelligence and machine learning and discover what they mean for your financial institution.

We surveyed more than 6,500 consumers and 650 businesses worldwide about their identity and fraud priorities for our 2020 Global Identity and Fraud Report

If you're looking for a competitive edge in 2020, Vision is your ticket into differentiating your organization with the latest insights and innovation.

With shrinking budgets and increased demand for customized messaging, financial marketing teams have numerous challenges. Learn how the best find success.

Leverage the strength of today's economy to solve your most complex problems. Recession readiness means proactively managing your portfolio today.

Exploring some of the top trends for the financial services industry going into the new decade from data and decisioning to fraud and customer experience.

According to Experian’s Q3 2019 State of the Automotive Finance Market report, used vehicle financing increased across all credit tiers.

Electric Vehicles in Operation: Share Still Low as OEMs Make Bets on How to Time the Market

Data & AnalyticsElectric vehicles have 2.08 percent of total VIO share through September 30, 2019

Financial firms are turning to customer acquisition engines to help them build, test and optimize custom targeting strategies faster than ever before.

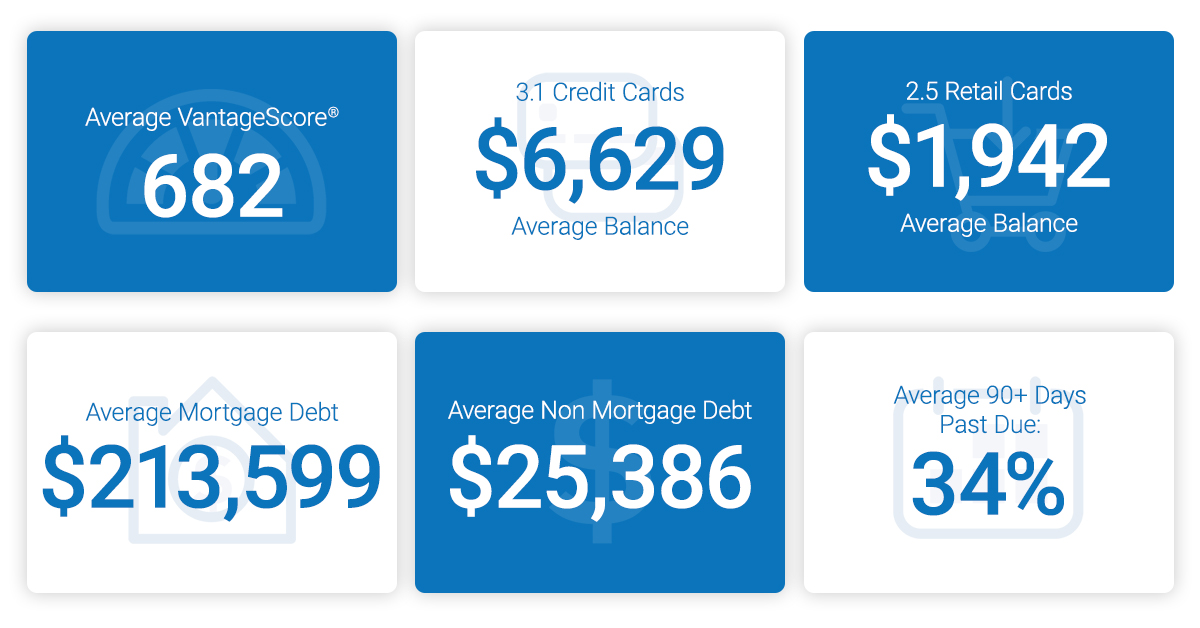

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.

What if you could increase your market engagement rate from 5% to 10%? Getting strategic about your segmentation makes all the difference.