Apply DA Tag

Shri Santhanam, Executive Vice President and General Manager of Global Analytics and Artificial Intelligence (AI) was recently featured on Lendit’s ‘Fintech One-on-One’ podcast. Shri and podcast creator, Peter Renton, discussed advanced analytics and AI’s role in lending and how Experian is helping lenders during what he calls the ‘digital lending revolution.’ Digital lending revolution “Over the last decade and a half, the notion of digital tools, decisioning, analytics and underwriting has come into play. The COVID-19 pandemic has dramatically accelerated that, and we’re seeing three big trends shake up the financial services industry,” said Shri. A shift in consumer expectations More than ever before, there is a deep focus on the customer experience. Five or six years ago, consumers and businesses were more accepting of waiting several days, sometimes even weeks, for loan approvals and decisions. However, the expectation has dramatically changed. In today’s digital world, consumers expect lending institutions to make quick approvals and real-time decisions. Fintechs being quick to act Fintech lenders have been disrupting the traditional financial services space in ways that positively impacts consumers. They’ve made it easier for borrowers to access credit – particularly those who have been traditional excluded or denied – and are quick to identify, develop and distribute market solutions. An increased adoption of machine learning, advanced analytics and AI Fintechs and financial institutions of all sizes are further exploring using AI-powered solutions to unlock growth and improve operational efficiencies. AI-driven strategies, which were once a ‘nice-to-have,’ have become a necessity. To help organizations reduce the resources and costs associated with building in-house models, Experian has launched Ascend Intelligence Services™, an analytics solution delivered on a modern tech AI platform. Ascend Intelligence Services helps streamline model builds and increases decision automation and approval rates. The future of lending: will all lending be done via AI, and what will it take to get there? According to Shri, lending in AI is inevitable. The biggest challenge the lending industry may face is trust in advanced analytics and AI decisioning to ensure lending is fair and transparent. Can AI-based lending help solve for biases in credit decisioning? We believe so, with the right frameworks and rules in place. Want to learn more? Explore our fintech solutions or click below. Listen to Podcast Learn more about Ascend Intelligence Services

Experian recently announced that it has made the IDC 2021 Fintech Rankings Top 100, highlighting the best global providers of financial technology. Experian is ranked number 11, rising 33 places from its 2020 ranking. IDC also refers to Experian as a ‘rising star.’ The robust data assets of Experian, combined with best-in-class modeling, decisioning and technology are powering new and innovative solutions. Experian has invested heavily in new technologies and infrastructures to deliver the freshest insights at the right time, to make the best decision. For example, Experian's Ascend Intelligence Services™ provides data, analytics, strategy, and performance monitoring, delivered on a modern-tech AI platform. With the investment in Ascend Intelligence Services, Experian has been able to streamline the delivery speed of analytical solutions to clients, improve decision automation rates and increase approval rates, in some cases by double digits. “Recognition in the top 20 of IDC FinTech Rankings demonstrates Experian’s commitment to the success of its financial clients,” said Marc DeCastro, research director at IDC Financial Insights. “We congratulate Experian for being ranked 11th in the 2021 IDC FinTech Rankings Top 100 list.” View the IDC Fintech Rankings list in its entirety here. Focus on Data, Advanced Analytics and Decisioning Creates Winning Strategy for Experian Experian’s focus on data, advanced analytics and decisioning has continued to gain recognition from various notable programs that acknowledge Fintech industry leaders and breakthrough technologies worldwide. Beyond the IDC Fintech Rankings Top 100, Experian won honors from the 2021 FinTech Breakthrough Awards, the 2021 CIO 100 Awards and was most recently shortlisted in the CeFPro Global Fintech Leaders List for 2022 in the categories of advanced analytics, anti-fraud, credit risk and core banking/back-end system technologies. “At Experian, we are committed to supporting the Fintech community. It’s great to see our continued efforts and investments driving positive impacts for our clients and their consumers. We will continue to invest and innovate to help our clients solve problems, create opportunities and support their customer-first missions,” said Jon Bailey, Vice President for Fintech at Experian. Learn more about how Experian can help advance your business goals with our Fintech Solutions and Ascend Intelligence Services. Explore fintech solutions Learn more about AIS

Artificial intelligence is here to stay, and businesses who are adopting the newest AI technology are ahead of the game. From targeting the right prospects to designing effective collections efforts, AI-driven strategies across the entire customer lifecycle are no longer a nice to have - they are a must. Many organizations are late to the game of AI and/or are spending too much time and money designing and redesigning models and deploying them over weeks and months. By the time these models are deployed, markets may have already shifted again, forcing strategy teams to go back to the drawing board. And if these models and strategies are not being continuously monitored, they can become less effective over time and lead to missed opportunities and lost revenue. By implementing artificial intelligence in predictive modeling and strategy optimization, financial institutions and lenders can design and deploy their decisioning strategies faster than ever before and make incremental changes on the fly to adapt to evolving market trends. While most organizations say they want to incorporate artificial intelligence and machine learning into their business strategy, many do not know where to start. Targeting, portfolio management, and collections are some of the top use cases for AI/ML strategy initiatives. Targeting One way businesses are using AI-driven modeling is for targeting the audiences that will most likely meet their credit criteria and respond to their offers. Financial institutions need to have the right data to inform a decisioning strategy that recognizes credit criteria, can respond immediately when prospects meet that criteria and can be adjusted quickly when those factors change. AI-driven response models and optimized decision strategies perform these functions seamlessly, giving businesses the advantage of targeting the right prospects at the right time. Credit portfolio management Risk models optimized with artificial intelligence and machine learning, built on comprehensive data sets, are being used by credit lenders to acquire new revenue and set appropriate balance limits. Strategies built around AI-driven risk models enable businesses to send new offers and cross-sell offers to current customers, while appropriately setting initial credit limits and managing limits over time for increased wallet share and reduced risk. Collections AI- and ML-driven analytics models are also optimizing collections strategies to improve recovery rates. Employing AI-powered balance and response models, credit lenders can make smarter collections decisions based on the most predictive and accurate information available. For lending businesses who are already tight on resources, or those whose IT teams cannot meet the demand of quickly adapting to ever-changing market conditions and decisioning criteria, a managed service for AI-powered models and strategy design might be the best option. Managed service teams work closely with businesses to determine specific use cases, develop models to meet those use cases, deploy models quickly, and monitor models to ensure they keep producing and predicting optimally. Experian offers Ascend Intelligence Services, the only managed service solution to provide data, analytics, strategy and performance monitoring. Experian’s data scientists provide expert guidance as they collaborate with businesses in developing and deploying models and strategies around targeting, acquisitions, limit-setting, and collections. Once those strategies are deployed, Experian continually monitors model health to ensure scores are still predictive and presents challenger models so credit lenders can always have the most accurate decisioning models for their business. Ascend Intelligence Services provides an online dashboard for easy visibility, documentation for regulatory compliance, and cloud capabilities to deliver scores and decisions in real-time. Experian’s Ascend Intelligence Services makes getting into the AI game easy. Start realizing the power of data and AI-driven analytics models by using our ROI calculator below: initIframe('611ea3adb1ab9f5149cf694e'); For more information about Ascend Intelligence Services, visit our webpage or join our upcoming webinar on October 21, 2021. Learn more Register for webinar

The collections landscape is changing as a result of new and upcoming legislation and increased expectations from consumers. Because of this, businesses are looking to create more effective, consumer-focused collections processes while remaining within regulatory guidelines. Our latest tip sheet has insights that can help businesses and agencies optimize their collections efforts and remain compliant, including: Start with the best data Keep pace with changing regulations Focus on agility Pick the right partner Download the tip sheet to learn how to maximize your collections efforts while reducing costs, avoiding reputational damage and fines, and improving overall engagement. Download tip sheet

The Telephone Consumer Protection Act (TCPA), which regulates telemarketing calls, autodialed calls, prerecorded calls, text messages and unsolicited faxes, was originally passed in 1991. Since that time, there have been many rulings and updates that impact businesses’ ability to maintain TCPA compliance. Recent TCPA Changes On December 30, 2020, the Federal Communications Commission (FCC) updated a number of TCPA exemptions, adding call limits and opt-out requirements, and codifying exemptions for calls to residential lines. These changes, along with other industry changes, have added additional layers of complication to keeping compliant while still optimizing operations and the consumer experience. Maintaining TCPA Compliance Businesses who do not maintain TCPA compliance could be subject to a lawsuit and paying out damages, and potential hits to their reputation. With the right partner in place, businesses can maintain data hygiene and accuracy to increase right-party contact (and reduce wrong-party contact) to keep collections streamlined and improve the customer experience. Using the right technology in place, it’s easier to: Monitor and verify consumer contact information for a better customer experience while remaining compliant. Receive and monitor daily notifications about changes in phone ownership information. Maintain compliance with Regulation F by leveraging a complete and accurate database of consumer information. When searching for a partner, be sure to look for one who offers data scrubbing, phone type indicators, phone number scoring, phone number identity verification, ownership change monitoring, and who has direct access to phone carriers. To learn more about how the right technology can help your business maintain TCPA compliance, visit us or request a call. Learn more

Over the last year and a half, strong trends emerged in how businesses and consumers interact online - specifically when validating identities and preventing fraud. We initially explored these trends at a global level, and now we've explored U.S.-specific insights into online security, the customer experience, and digital activities and operations. Download the North America findings report to learn more about business and consumer fraud and identity trends impacting the way we live, work, and interact. Review your fraud strategy

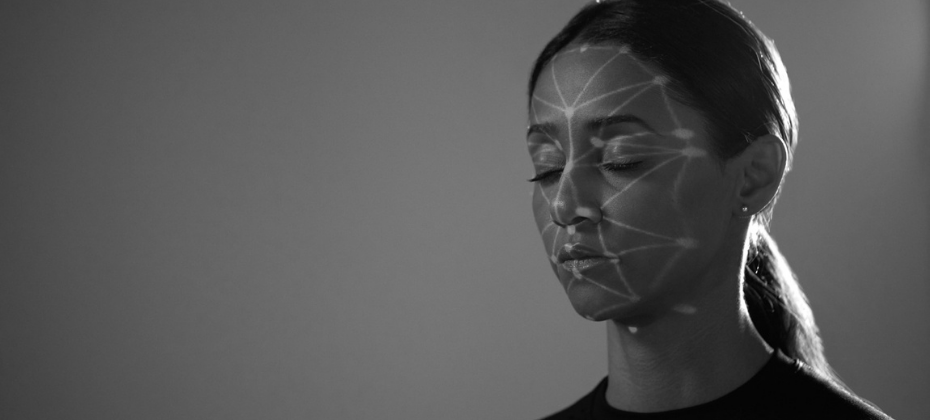

Lately, I’ve been surprised by the emphasis that some fraud prevention practitioners still place on manual fraud reviews and treatment. With the market’s intense focus on real-time decisions and customer experience, it seems that fraud processing isn’t always keeping up with the trends. I’ve been involved in several lively discussions on this topic. On one side of the argument sit the analytical experts who are incredibly good at distilling mountains of detailed information into the most accurate fraud risk prediction possible. Their work is intended to relieve users from the burden of scrutinizing all of that data. On the other side of the argument sits the human side of the debate. Their position is that only a human being is able to balance the complexity of judging risk with the sensitivity of handling a potential customer. All of this has led me to consider the pros and cons of manual fraud reviews. The Pros of Manual Review When we consider the requirements for review, it certainly seems that there could be a strong case for using a manual process rather than artificial intelligence. Human beings can bring knowledge and experience that is outside of the data that an analytical decision can see. Knowing what type of product or service the customer is asking for and whether or not it’s attractive to criminals leaps to mind. Or perhaps the customer is part of a small community where they’re known to the institution through other types of relationships—like a credit union with a community- or employer-based field of membership. In cases like these, there are valuable insights that come from the reviewer’s knowledge of the world outside of the data that’s available for analytics. The Cons of Manual Review When we look at the cons of manual fraud review, there’s a lot to consider. First, the costs can be high. This goes beyond the dollars paid to people who handle the review to the good customers that are lost because of delays and friction that occurs as part of the review process. In a past webinar, we asked approximately 150 practitioners how often an application flagged for identity discrepancies resulted in that application being abandoned. Half of the audience indicated that more than 50% of those customers were lost. Another 30% didn’t know what the impact was. Those potentially good customers were lost because the manual review process took too long. Additionally, the results are subjective. Two reviewers with different levels of skill and expertise could look at the same information and choose a different course of action or make a different decision. A single reviewer can be inconsistent, too—especially if they’re expected to meet productivity measures. Finally, manual fraud review doesn’t support policy development. In another webinar earlier this year, a fraud prevention practitioner mentioned that her organization’s past reliance on manual review left them unable to review fraud cases and figure out how the criminals were able to succeed. Her organization simply couldn’t recreate the reviewer’s thought process and find the mistake that lead to a fraud loss. To Review or Not to Review? With compelling arguments on both sides, what is the best practice for manually reviewing cases of fraud risk? Hopefully, the following list will help: DO: Get comfortable with what analytics tell you. Analytics divide events into groups that share a measurable level of fraud risk. Use the analytics to define different tiers of risk and assign each tier to a set of next steps. Start simple, breaking the accounts that need scrutiny into high, medium and low risk groups. Perhaps the high risk group includes one instance of fraud out of every five cases. Have a plan for how these will be handled. You might require additional identity documentation that would be hard for a criminal to falsify or some other action. Another group might include one instance in every 20 cases. A less burdensome treatment can be used here – like a one-time-passcode (OTP) sent to a confirmed mobile number. Any cases that remain unverified might then be asked for the same verification you used on the high-risk group. DON’T: Rely on a single analytical score threshold or risk indicator to create one giant pile of work that has to be sorted out manually. This approach usually results in a poor experience for a large number of customers, and a strong possibility that the next steps are not aligned to the level of risk. DO: Reserve manual review for situations where the reviewer can bring some new information or knowledge to the cases they review. DON’T: Use the same underlying data that generated the analytics as the basis of a review. Consider two simplistic cases that use a new address with no past association to the individual. In one case, there are several other people with different surnames that have recently been using the same address. In the other, there are only two, and they share the same surname. In the best possible case, the reviewer recognizes how the other information affects the risk, and they duplicate what the analytics have already done – flagging the first application as suspicious. In other cases, connections will be missed, resulting in a costly mistake. In real situations, automated reviews are able to compare each piece of information to thousands of others, making it more likely that second-guessing the analytics using the same data will be problematic. DO: Focus your most experienced and talented reviewers on creating fraud strategies. The best way to use their time and skill is to create a cycle where risk groups are defined (using analytics), a verification treatment is prescribed and used consistently, and the results are measured. With this approach, the outcome of every case is the result of deliberate action. When fraud occurs, it’s either because the case was miscategorized and received treatment that was too easy to discourage the criminal—or it was categorized correctly and the treatment wasn’t challenging enough. Gaining Value While there is a middle ground where manual review and skill can be a force-multiplier for strong analytics, my sense is that many organizations aren’t getting the best value from their most talented fraud practitioners. To improve this, businesses can start by understanding how analytics can help group customers based on levels of risk—not just one group but a few—where the number of good vs. fraudulent cases are understood. Decide how you want to handle each of those groups and reserve challenging treatments for the riskiest groups while applying easier treatments when the number of good customers per fraud attempt is very high. Set up a consistent waterfall process where customers either successfully verify, cascade to a more challenging treatment, or abandon the process. Focus your manual efforts on monitoring the process you’ve put in place. Start collecting data that shows you how both good and bad cases flow through the process. Know what types of challenges the bad guys are outsmarting so you can route them to challenges that they won’t beat so easily. Most importantly, have a plan and be consistent. Be sure to keep an eye out for a new post where we’ll talk about how this analytical approach can also help you grow your business. Contact us

Earlier this year, we shared our predictions for five fraud threats facing businesses in 2021. Now that we’ve reached the midpoint of the year and economic recovery is underway, we’re taking another look at how these threats can impact businesses and consumers. Putting a Face to Frankenstein IDs: Synthetic identity fraudsters will attempt to bypass fraud detection methods by using AI to combine facial characteristics from different people to form a new identity. Overexposure: As many as 80% of SSNs may have been exposed on the dark web, creating opportunities for account application fraud. The Heist: Surges in data breaches, advances in automation, expanded online banking services and vulnerabilities exposed from social engineering mistakes have lead to rises in account takeover fraud. Overstimulated: Opportunistic fraudsters may take advantage of ongoing relief payments by using stolen data from consumers. Behind the Times: Businesses with lackluster fraud prevention tools and insufficient online security technology will likely experience more attacks and suffer larger losses. To learn more about upcoming fraud threats and how to protect your business, download our new infographic and check out Experian’s fraud prevention solutions. Download infographic Request a call

As stimulus-generated fraud wanes, we anticipate a return of more traditional forms of fraud, including account opening fraud. As businesses embrace the digital evolution and look ahead to responsible growth, it’s important to balance the customer experience with the risks associated with account opening fraud. Preventing account opening fraud requires a layered fraud and identity management strategy that allows you to approve good customers while keeping criminals out. With the right tools in place, you can optimize the customer experience while still keeping risk low. Download infographic Review your fraud strategy

Establishing a strong digital strategy remains a top priority for most financial institutions. With more eyes on screens and electronic devices, the pandemic-induced shift to digital has increased the need to meet consumers where they are. New Innovations As a Result of an Accelerated Shift to Digital In Ernst & Young’s 2019 biannual Global Fintech Adoption Index, 46% of American respondents indicated they were using at least one fintech service. Fast forward, COVID-19 has accelerated the American adoption rate to 59%, according to a September survey conducted by Plaid, a leading digital payments infrastructure company. This shift to digital also resulted in an uptick in the creation of banking and savings processes that leverage advanced technologies. For example, digital-first technologies and artificial intelligence (AI) are changing the prescreen landscape as never before. For financial institutions, smart prescreen marketing solutions, coupled with a traditional approach to personalized service, present vast opportunities to build deeper consumer relationships. However, implementing an effective strategy can be challenging. In a recent webinar, Experian’s Vice President of Product Management Jacob Kong tackled the topic of using new analytics and AI to create a digital-first strategy. Joined by Mark Sievewright, founder of Sievewright & Associates and co-author of Digital Life, and Devon Kinkead, CEO of Micronotes.ai, they explored the evolution of banking and the possibilities offered by pairing data with technology in our new digital world. Watch the full webinar, 'Digital-First Strategies: New Analytics and Artificial Intelligence for Marketing,' and learn more about: The shift to digital life and banking, new analytics and AI How data and information value empowers prescreen marketing Emerging technologies and new tools that can support aggressive growth and marketing initiatives while mitigating risk How Experian is joining forces with Micronotes.ai to launch Micronotes ReFI powered by Experian, to help lower customers’ or members’ borrowing costs by refinancing mispriced debt Learn more about Micronotes ReFI powered by Experian To explore how Experian’s solutions and capabilities can power your prescreen and marketing strategies, please visit our solutions page or contact us for more information. Contact Us

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

Premier Awards Program Recognizes Breakthrough Financial Technology Products and Companies Experian’s Ascend Intelligence Services was selected as a winner of the “Consumer Lending Innovation Award” category in the fifth annual Fintech Breakthrough Awards conducted by Fintech Breakthrough, an independent market intelligence organization that recognizes the top companies, technologies and products in the global fintech market today. The Fintech Breakthrough Awards is the premier awards program founded to recognize the fintech innovators, leaders and visionaries from around the world in a range of categories, including digital banking, personal finance, lending, payments, investments, RegTech, InsurTech and many more. The 2021 Fintech Breakthrough Awards attracted more than 3,850 nominations from across the globe. One of the latest developments on Experian's trusted, award-winning Ascend platform, Ascend Intelligence Services empowers financial services firms with Experian’s revolutionary managed analytics solutions and services, delivered on a modern-tech AI platform. Ascend Intelligence Services includes rapid model development, seamless deployment, optimized decision strategies, ongoing performance monitoring and continuous retraining. The technology-enabled service uses a secure cloud-based AI platform to harness the power of machine learning, and deliver unique capabilities covering the entire credit lifecycle, through an easy-to-use web portal. “To stay ahead of the latest economic conditions, fintechs need high-quality analytical models running on large and varied data sets that empower them to act quickly and decisively. The breakthrough Ascend Intelligence Services platform answers this immediate market need,” said James Johnson, Managing Director, Fintech Breakthrough. “Congratulations to Experian and the Ascend team on winning our ‘Consumer Lending Innovation Award’ for 2021 with this game-changing solution.” “Data scientists are spending too much time on manual, repetitive and low value-add tasks, and organizations cannot afford to do this is in a state of constant change,” said Srikanth Geedipalli, Experian’s SVP Global Analytics/AI Products. “While building and deploying high-quality analytical models can be time-consuming and expensive, Ascend Intelligence Services streamlines this process by harnessing the power of machine learning and Experian’s rich data assets to drive better, faster and smarter decisions. We have been able to deliver analytical solutions to clients up to 4X faster, significantly improving decision automation rates and increasing approval rates by double digits. We are proud that Ascend Intelligence Services is being recognized as a breakthrough solution in the 2021 Fintech Breakthrough Awards program,” he said. Ascend Intelligence Services is comprised of four modules: Ascend Intelligence Services Challenger™ is a powerful, dynamic and collaborative model development service that enables Experian to rapidly build a model and quantify the benefit to business. Businesses can review, comment on and approve the model, all from within the web portal, while it’s being built. The resulting score is available for testing through an API endpoint and can be deployed in production with a few easy steps. Reports are customizable, downloadable and regulatory compliant. Ascend Intelligence Services Pulse™ is a proactive model monitoring and validation service, which aids companies in monitoring the health of models that drive their business decisions. Pulse, provides convenient dashboards that include a model health index, performance summary, stress-testing results, model risk management reporting, model health alerts and more. Additionally, Pulse automatically builds challengers for champion models, providing an estimated performance lift and financial benefit. Ascend Intelligence Services Strategy Advance™ is a powerful business strategy development service, enabling clients to make optimal lending decisions on their applicants. Strategy Advance uses Experian’s powerful optimization engine to build the right credit policy for clients, including sophisticated decision rules, model overlays and client specified knock-out rules. The resulting decision is available for testing through an API endpoint and can be deployed in production with a few easy steps. Ascend Intelligence Services Limit™ is a credit limit optimization service, enabling clients to make the right credit limit decisions at account origination and during account management. Limit uses Experian’s data, predictive risk and balance models and our powerful optimization engine to design the right credit limit strategy that maximizes product usage, while keeping losses low. The limit decision is available for testing through an API endpoint and can be deployed in production with a few easy steps. To learn more about how Ascend Intelligence Services can support your business, please explore our solutions page. Learn more For a list of all award winners selected for the Fintech Breakthrough Awards, read the full press release here.

The pandemic changed nearly everything – and consumer credit is no exception. Data, analytics, and credit risk decisioning are gaining an even more significant role as we grow closer to the end of the global crisis. Consumers face uneven roads to recovery, and while some are ready to spend again, others are still dealing with pandemic-related financial stress. We surveyed nearly 9,000 consumers and 2,700 businesses worldwide about how consumers are stabilizing their finances and businesses are returning to growth for our new Global Decisioning Report. In this report, we dive into: Key business priorities in 2021 Financial concerns for consumers How to navigate an uneven recovery Business priorities for the year ahead The importance of the online experience As we begin to near the end of the pandemic, businesses need to prioritize technology that enables a responsive, flexible, efficient and confident approach. This can be done by leveraging advanced data and analytics and integrating machine learning tools into model development. By investing in the right credit risk decisioning tools now, you can help ensure your future. Download the report

The tax gap—the difference between what taxpayers should pay and what they actually pay on time—can have a substantial impact on states’ budgets. Tax agencies and other state departments are responsible for helping states manage their budgets by minimizing expected revenue shortfalls. Underreported income is a significant budget complication that continues to frustrate even the most effective tax agencies, until the right tools are brought into play. The Problem Underreporting is a large, complex issue for agencies. The IRS currently estimates the annual tax gap at $441 billion. There are multiple factors that comprise that total, but the most prevalent is underreporting, which represents 80% of the total tax gap. Of that, 54% is due to underreporting of individual income tax. In addition to being the largest contributor to the tax gap, underreporting is also extremely challenging to identify out of the millions of returns being filed. With 85% of taxes owed correctly reported and paid, finding underreporting can be like trying to locate a needle in the proverbial haystack. Making this even more challenging is the limited resources available for auditing returns, which makes efficiency key. The Solution Data, combined with artificial intelligence (AI) equals efficient detection. The problem with trying to detect which returns are most likely to have underreported income is similar to many other challenges Experian has solved with AI. Partnerships between Experian and state agencies combine what we know about consumers with what their agency knows about their population. We can take the data and use AI to separate the signal from the noise, finding opportunities to recoup lost revenue. Read our case study on how Experian was able to help an agency identify instances of underreporting, detecting an estimated $80 million annual lost revenue from underreported income. Download case study Contact us

The COVID-19 pandemic has created shifting economic conditions and rapidly evolving consumer preferences. Lenders must keep up by re-evaluating their strategies to accelerate growth and beat the competition. Here's how AI/ML can help your organization evolve post-COVID-19: With the democratization of AI/ML, lenders of all sizes can now use this technology to grow their lending and optimize for strategic growth. Register for our upcoming webinar to see how lenders like Elevate have incorporated this new technology into their business processes. Register now