Tag: portfolio management

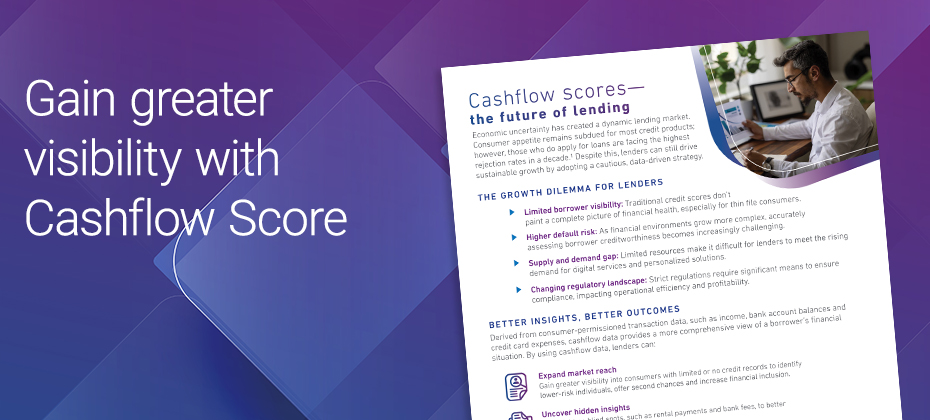

Consumers are experiencing the highest loan rejection rates in a decade, driven by strict lending standards.1 While crucial for mitigating risk, these measures can also limit growth opportunities for financial institutions. Our latest one pager explores how cash flow data, obtained from consumer-permissioned transaction data, empowers lenders with unique insights into consumers’ financial health, enabling them to expand their portfolios while managing risk effectively. Read the full one pager to learn how cashflow data can help you make smarter, more confident lending decisions. Access one pager 12024 Q4 Lending Conditions Chartbook, Experian.

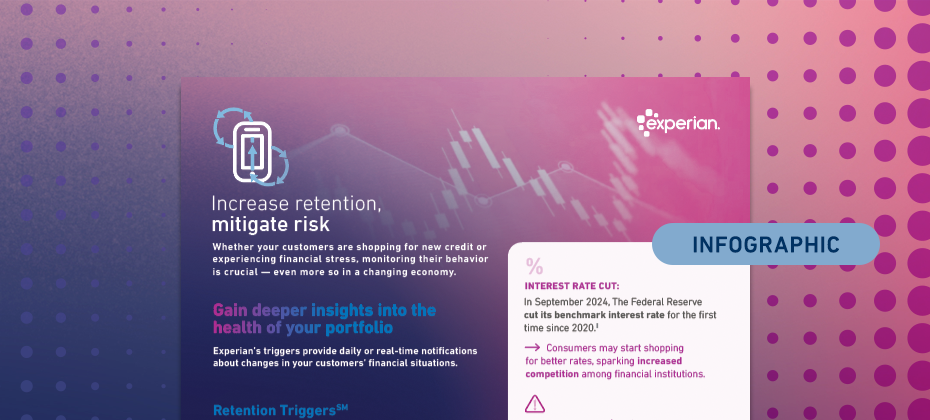

Whether consumers are shopping for new credit or experiencing financial stress, monitoring their behavior is crucial — even more so in an ever-changing economy. Our latest infographic explores economic trends impacting consumers’ financial behaviors and how Experian’s Risk and Retention TriggersSM enable lenders to detect early signs of risk or churn. Key highlights include: Credit card balances climbed to $1.17 trillion in Q3 2024. As prices of goods and services remain elevated, consumers may continue to experience financial stress, potentially leading to higher delinquency rates. Increasing customer retention rates by 5% can boost profits by 25% to 95%. View the infographic to learn how Risk and Retention Triggers can help you advance your portfolio management strategy. Access infographic

Do you know where your customers stand? Not literally, of course, but do you know how recent macroeconomic changes and their personal circumstances are currently affecting your portfolio? While refreshing your customers’ credit data quarterly works for some aspects of portfolio management, you need more frequent access to fresh data to quickly respond to risky customer behavior and new credit needs before your portfolio takes a hit. Use triggers to improve portfolio management Event-based credit triggers provide daily or real-time alerts about important changes in your customers’ financial situations. You can use these to manage risk by promptly responding to signs of changing creditworthiness or to prevent attrition by proactively reaching out to customers who are shopping for credit. Risk Triggers℠ and Retention Triggers℠ offer a real-time solution that can be customized to fit your needs for daily portfolio management. What are Risk Triggers? Experian’s Risk Triggers alert you of notable information, such as unfavorable utilization rate changes, delinquencies with other lenders and recent activity with high-interest, short-term loan products. This solution allows you to monitor how your customers manage accounts with other lenders to get ahead of potential risk on your book. You can use Risk Triggers to get daily insights into your customers’ activity — allowing you to quickly identify potentially risky behavior and take appropriate action to limit your exposure and losses. Types of Risk Triggers Choose from a defined Risk Triggers package that could help you identify high-risk customers, including: New trades Increasing credit utilization or balances over limit New collection accounts An account is charged-off A credit grantor closes an account New delinquency statuses (30 to 180 days past due) Consumers seeking access to short-term, high-risk financing options Bankruptcy and deceased events How to use Risk Triggers You can use the daily alerts from Risk Triggers to help inform your account management strategy. Depending on the circumstances, you might: Decrease credit limits Close or freeze accounts Accelerate payment requests Continue monitoring accounts for other signs of risk Spotlight on Experian’s Clarity Services events Included in Risk Triggers are events from Experian’s Clarity Services, which draw on expanded FCRA-regulated data* from a leading source of alternative financial credit data. For example, you could get an alert when someone has a new inquiry from non-traditional loans. These triggers provide a broader view of the customer – offering added protection against risky behavior. What are Retention Triggers? Experian’s Retention Triggers can alert you when a customer improves their creditworthiness, is shopping for new credit, opens a new tradeline or lists property. Proactively responding to these daily alerts can help you retain and strengthen relationships with your customers — which is often less expensive than acquiring new customers. Types of Retention Triggers Choose from over 100 Retention Triggers to bundle, including: New trades New inquiries Credit line increases Property listing statuses Improving delinquency status Past-due accounts are brought current or paid off How to use Retention Triggers You can use Retention Triggers to increase lifetime customer value by proactively responding to your customers’ needs and wants. You might: Increase credit limits Offer promotional financing, such as balance transfers Introduce perks or rewards to strengthen the relationship Append attributes for improved decisioning By appending credit attributes to Risk and Retention Trigger outputs, you can gain greater insight into your accounts. Premier AttributesSM is Experian's core set of 2,100-plus attributes. These can quickly summarize data from consumers' credit reports, allowing you to more easily segment accounts to make more strategic decisions across your portfolio. Trended 3DTM attributes can help you spot and understand patterns in a customer's behavior over time. Integrating trended attributes into a triggers program can help you identify risk and determine the next best action. Trended 3D includes more than 2,000 attributes and provides insights into industries such as bankcard, mortgage, student loans, personal loans, collections and much more. By working with both triggers and attributes, you'll proactively review an account, so you can then take the next best action to improve your portfolio's profits. Customize your trigger strategy When you partner with Experian, you can bundle and choose from hundreds of Risk and Retention Triggers to focus on risk, customer retention or both. Additionally, you can work with Experian’s experts to customize your trigger strategy to minimize costs and filter out repetitive or unneeded triggers: Use cool-off periods Set triggering thresholds Choose which triggers to monitor Establish hierarchies for which triggers to prioritize Create different strategies for segments of your portfolio Learn more about Risk and Retention Triggers. Learn more *Disclaimer: “Alternative Financial Credit Data” refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA-Regulated Data” may also apply in this instance, and both can be used interchangeably.

Rising balances and delinquency rates are causing lenders to proactively minimize credit risk through pre-delinquency treatments. However, the success of these types of account management strategies depends on timely and predictive data. Credit attributes summarize credit data into specific characteristics or variables to provide a more granular view of a consumer’s behavior. Credit attributes give context about a consumer’s behavior at a specific point in time, such as their current revolving credit utilization ratio or their total available credit. Trended credit attributes analyze credit history data for consumer behavior patterns over time, including changes in utilization rates or how often a balance exceeded an account’s credit limit during the previous 12 months. In a recent analysis, we found that credit attributes related to utilization were highly predictive of future delinquencies in bankcard accounts, with many lenders better managing their credit risk when incorporating these attributes into their account management processes. READ: Find out how custom attributes and models can help you stay ahead of your competitors in the "Build a profitable portfolio with credit attributes" e-book. Using attributes to manage credit risk An enhanced understanding of credit attributes can be leveraged to manage risk throughout the customer lifecycle. They can be important when you want to: Improve credit strategies and efficiencies: Overlay attributes and incorporate them into credit policy rules, such as knockout criteria, to expand your lending population and increase automation without taking on more credit risk. Better understand customers' credit trends: Experian’s wide range of credit data, including trended credit attributes, can help you quickly understand how consumers are faring off-book for visibility into other lending relationships and if they’ll likely experience financial stress in the future. Credit attributes can also help precisely segment populations. For example, attributes can help you distinguish between two people who have similar credit risk scores — but very different trajectories — and will better determine who's the least risky customer. Predicting 60+ day delinquencies with credit attributes To evaluate the effectiveness of credit attributes during account review, we looked at 2.9 million open and active bankcard accounts to see which attributes best predicted the likelihood of an account reaching 60 days past due. For this analysis, we used snapshots of bankcard accounts that were reported in October 2022 and April 2023. Additionally, we analyzed the predictive power of over 4,000 attributes from Experian Premier AttributesSM and Trended 3DTM. Key findings Nine of the top 20 most predictive credit attributes were related to credit utilization rates. Delinquency-related attributes were predictive but weren’t part of the top 10. Three of the top 10 attributes were related to available credit. Turning insight into action While we analyzed credit attributes for account review, determining attribute effectiveness for other use cases will depend on your own portfolio and goals. However, you can use a similar approach to finding the predictive power of attributes. Once you identify the most predictive credit attributes for your population, you can also create an account review program to track these metrics, such as changes in utilization rates or available credit balances. Using Experian’s Risk and Retention Triggers℠ can immediately notify you of customers' daily credit activity to monitor those changes. Ongoing monitoring of attributes and triggers can help you identify customers who are facing financial stress and are headed toward delinquency. You can then proactively take steps to reduce your risk exposure, prioritize accounts, and modify pre-collections strategy based on triggering events. Experian offers credit attributes and the tools to use them Creating and managing credit attributes can be a complex and never-ending task. You need to regularly monitor attributes for performance drift and to address changing regulatory requirements. You may also want to develop new attributes based on expanding data sources and industry trends. Many organizations don’t have the resources to create, manage, and update credit attributes on their own. That’s where Experian’s 4,500+ attributes and tools can help to save time and money. Premier Attributes includes our core attributes and subsets for over 50 industries. Trended 3D attributes can help you better understand changes in consumer behavior and creditworthiness. Clear View AttributesTM offers insights from expanded FCRA data* that generally isn’t reported to consumer credit bureaus. You can easily review and manage your portfolios with Experian’s Ascend Quest™ platform. The always-on access allows you to request thousands of data elements, including credit attributes, risk scores, income models, segmentation data, and payment history, at any time. Use insights from the data and leverage Ascend Quest to quickly identify accounts that may be experiencing financial stress to limit your credit risk — and target others with retention and up-selling opportunities. Watch the Ascend Quest demo to see it in action, or contact us to learn more about Experian’s credit attributes and account review solutions. Watch demo Contact us

In the dynamic consumer credit landscape, understanding emerging trends is paramount for fintechs to thrive. Experian's latest fintech trends report provides deep insights into the evolving market, shedding light on crucial areas such as origination volumes, average loan balances, and delinquency trends. Let's delve into some key findings and their implications for fintech lenders. Fintech lending origination volume trends The report reveals intriguing shifts in origination volumes for unsecured personal loans and credit cards. While overall origination amounts dipped, fintechs experienced a notable decrease, signaling potential challenges in funding availability and economic uncertainties. Despite this, the total origination volume for fintechs remains robust, underlining their continued significance in the market. Fintech market share versus traditional lenders Fintechs, known for their agility and digital prowess, witnessed fluctuations in market share, particularly in the unsecured personal loan segment. While digital loans continue to drive a significant portion of originations, there's a discernible shift in market dynamics, urging fintech lenders to explore diversification strategies, including expanding into credit card offerings. Fintech lending average loan balance trends Amidst changing economic landscapes, average loan balances for both unsecured personal loans and credit cards exhibited intriguing patterns. Fintech lenders, although maintaining a competitive edge in average balances, face the challenge of balancing risk and profitability, especially amidst rising delinquency levels. Fintech lending delinquency trends One of the most critical aspects highlighted in the report is the uptick in delinquency levels for unsecured personal loans and credit cards. While fintechs navigate through economic uncertainties, there's a growing imperative to enhance risk management strategies and focus on prime and above credit tiers to mitigate potential risks. Understanding the digital borrower As digital borrowing continues to gain prominence, it's essential for fintechs to grasp the nuances of the digital borrower. With millennials emerging as key players in the digital lending landscape, fintechs must tailor their offerings to cater to the unique preferences and behaviors of this demographic segment. Looking ahead to 2024 for fintech lenders As we look to the future, data-driven decision-making and strategic portfolio management are more important than ever for fintechs. With economic uncertainties still in the mix, fintechs must leverage data and analytics to fuel growth while safeguarding against potential risks. Experian's fintech trends report serves as a guiding beacon, equipping fintechs with the knowledge and strategies needed to navigate through uncertainties and unlock opportunities for sustainable growth. The report offers actionable insights, including the imperative to conduct periodic portfolio reviews, retool data analytics and models, and remodel lending criteria to stay ahead in the competitive landscape. Learn more about our fintech solutions and how we can work together to drive profitable growth for your company. Learn more Download the report About the report: Experian's Fintech Trends Report 2024 offers a comprehensive analysis of credit trends, leveraging data from January 2019 to November 2023. The report provides valuable insights into the evolving landscape of unsecured personal loans and credit cards, empowering fintechs with actionable intelligence to thrive in a competitive market environment.

In today’s highly competitive landscape, credit card issuers face the challenge of optimizing portfolio profitability while also effectively managing their overall risk. Financial institutions successfully navigating the current market put more focus on proactively managing their credit limits. By appropriately assigning initial credit limits and actively overseeing current limits, these firms are improving profitability, reducing potential risk, and creating a better customer experience. But how do you get started with this important tool? Let’s explore how and why proactive credit limit management could impact your business. The importance of proactive credit limit management Enhanced profitability: Assigning the optimal credit limit that caters to a customer’s spending behavior while also considering their capacity to repay can stimulate increased credit card usage without taking on additional risk. This will generate higher transaction volumes, increase interest income, promote top-of-wallet use, and improve wallet share, all positively impacting the institution’s profitability. Mitigating risk exposure: A proactive review of the limits assigned within a credit card portfolio helps financial institutions assess their exposure to overextended credit usage or potential defaults. Knowing when to reduce a credit limit and assigning the right amount can help financial institutions mitigate their portfolio risk. Minimizing default rates: Accurately assigning the right credit limit reduces the likelihood of customers defaulting on payments. When an institution aligns their credit limits with a cardholder's financial capability, it reduces the probability of customers exceeding their spending capacity and defaulting on payments. Improving the customer experience: A regular review of a credit card portfolio can help financial institutions find opportunities to proactively increase credit limits. This reduces the need for a customer to call in and request a higher credit limit and can increase wallet share and customer loyalty. Strategies for effective credit limit management Utilizing advanced analytics: Leveraging machine learning models and mathematically optimized decision strategies allows financial institutions to better assess risk and determine the optimal limit assignment. By analyzing spending patterns, credit utilization, and repayment behavior, institutions can dynamically adjust credit limits to match evolving customer financial profiles. Regular review and adjustments: As part of portfolio risk management, implementing a system for a recurring review and adjustment of credit limits is crucial. It ensures that credit limits are still aligned with the customer's financial situation and spending habits, while also reducing the risk of default. Customization and flexibility: Personalized credit limits tailored to individual customer needs improve customer satisfaction and loyalty. Proactively increasing limits based on improved creditworthiness or income reassessment can foster stronger customer relationships. Protect profitability and control risk exposure Using the right data analytics, processing regular reviews, and customizing limits to individual customer needs helps reduce risk exposure while maximizing profitability. As the economic landscape evolves, institutions that prioritize proactive credit limit management will gain a competitive edge by fostering responsible customer spending behavior, minimizing default rates, and optimizing their bottom line. With Experian, automating your credit limit management process is easy Experian’s Ascend Intelligence ServicesTM Limit provides you with the optimal credit limits at the customer level to generate a higher share of plastic spend, reduce portfolio risk, and proactively meet customer expectations. Let us help automate your credit limit management process to better serve your customers and quickly respond to the volatile market. To find out more, please visit our website. Ready for a demo? Contact us now!

Changes in your portfolio are a constant. To accelerate growth while proactively identifying risk, you’ll need a well-informed portfolio risk management strategy. What is portfolio risk management? Portfolio risk management is the process of identifying, assessing, and mitigating risks within a portfolio. It involves implementing strategies that allow lenders to make more informed decisions, such as whether to offer additional credit products to customers or identify credit problems before they impact their bottom line. Leveraging the right portfolio risk management solution Traditional approaches to portfolio risk management may lack a comprehensive view of customers. To effectively mitigate risk and maximize revenue within your portfolio, you’ll need a portfolio risk management tool that uses expanded customer data, advanced analytics, and modeling. Expanded data. Differentiated data sources include marketing data, traditional credit and trended data, alternative financial services data, and more. With robust consumer data fueling your portfolio risk management solution, you can gain valuable insights into your customers and make smarter decisions. Advanced analytics. Advanced analytics can analyze large volumes of data to unlock greater insights, resulting in increased predictiveness and operational efficiency. Model development. Portfolio risk modeling methodologies forecast future customer behavior, enabling you to better predict risk and gain greater precision in your decisions. Benefits of portfolio risk management Managing portfolio risk is crucial for any organization. With an advanced portfolio risk management solution, you can: Minimize losses. By monitoring accounts for negative performance, you can identify risks before they occur, resulting in minimized losses. Identify growth opportunities. With comprehensive consumer data, you can connect with customers who have untapped potential to drive cross-sell and upsell opportunities. Enhance collection efforts. For debt portfolios, having the right portfolio risk management tool can help you quickly and accurately evaluate collections recovery. Maximize your portfolio potential Experian offers portfolio risk analytics and portfolio risk management tools that can help you mitigate risk and maximize revenue with your portfolio. Get started today. Learn more

After being in place for more than three years, the student loan payment pause is scheduled to end 60 days after June 30, with payments resuming soon after. As borrowers brace for this return, there are many things that loan servicers and lenders should take note of, including: Potential risk factors demonstrated by borrowers. About one in five student loan borrowers show risk factors that suggest they could struggle when scheduled payments resume.1 These include pre-pandemic delinquencies on student loans and new non-medical collections during the pandemic. The impact of pre-pandemic delinquencies. A delinquent status dating prior to the pandemic is a statistically significant indicator of subsequent risk. An increase in non-student loan delinquencies. As of March 2023, around 2.5 million student loan borrowers had a delinquency on a non-student loan, an increase of approximately 200,000 borrowers since September 2022.2 Transfers to new servicers. More than four in ten borrowers will return to repayment with a new student loan servicer.3 Feelings of anxiety for younger borrowers. Roughly 70% of Gen Z and millennials believe the current economic environment is hurting their ability to be financially independent adults. However, 77% are striving to be more financially literate.4 How loan servicers and lenders can prepare and navigate Considering these factors, lenders and servicers know that borrowers may face new challenges and fears once student loan payments resume. Here are a few implications and what servicers and lenders can do in response: Non-student loan delinquencies can potentially soar further. Increased delinquencies on non-student loans and larger monthly payments on all credit products can make the transition to repayment extremely challenging for borrowers. Combined with high balances and interest rates, this can lead to a sharp increase in delinquencies and heightened probability of default. By leveraging alternative data and attributes, you can gain deeper insights into your customers' financial behaviors before and during the payment holidays. This way, you can mitigate risk and improve your lending and servicing decisions. Note: While many student loan borrowers have halted their payments during forbearance, some have continued to pay anyway, demonstrating strong financial ability and willingness to pay in the future. Trended data and advanced modeling provide a clearer, up-to-date view of these payment behaviors, enabling you to identify low-risk, high-value customers. Streamlining your processes can benefit you and your customers. With some student loan borrowers switching to different servicers, creating new accounts, enrolling in autopay, and confirming payment information can be a huge hassle. For servicers that will have new loans transferred to them, the number of queries and requests from borrowers can be overwhelming, especially if resources are limited. To make transitions as smooth as possible, consider streamlining your administrative tasks and processes with automation. This way, you can provide fast and frictionless service for borrowers while focusing more of your resources on those who need one-on-one assistance. Providing credit education can help borrowers take control of their financial lives. Already troubled by higher costs and monthly payments on other credit products, student loan payments are yet another financial obligation for borrowers to worry about. Some borrowers have even stated that student loan debt has delayed or prevented them from achieving major life milestones, such as getting married, buying a home, or having children.5 By arming borrowers with credit education, tools, and resources, they can better navigate the return of student loan payments, make more informed financial decisions, and potentially turn into lifelong customers. For more information on effective portfolio management, click here. 1Consumer Financial Protection Bureau. (June 2023). Office of Research blog: Update on student loan borrowers as payment suspension set to expire. 2Ibid. 3Ibid. 4Experian. (May 2023). Take a Look: Millennial and Gen Z Personal Finance Trends 5AP News. (June 2023). The pause on student loan payment is ending. Can borrowers find room in their budgets?

Credit portfolio management has often involved navigating uncertainty, but some periods are more extreme than others. With the right data and analytics you can gain deeper insight into financial behaviors and risk to make better decisions and drive profitable growth. Along with access to an increasing amount of data, advanced analytics can help lenders more accurately: Forecast losses under different economic scenarios to estimate liquidity requirements. Identify fraud by detecting behaviors that could indicate identity theft, account takeover fraud, first-party or synthetic identity fraud. Incorporate real-time and alternative data,1 such as cash flow transaction data and specialty bureau data, in decisioning and scoring to accurately assess creditworthiness and expand your lending pool without taking on undue risk. Precisely segment consumers using internal and external data to increase automation during underwriting and identify cross-sell opportunities. Improve collections using AI-driven strategies and automated debt collection software to enhance operations and increase recovery rates. It’s imperative to take a proactive approach to portfolio monitoring. Monthly portfolio reviews with bureau scores, credit attributes and specialized scores — and using the results to manage credit lines and loan terms — are critical during volatile times. View our interactive e-book for the latest economic and consumer trends and learn how to set your portfolio up to succeed in any economic cycle. Download e-book 1"Alternative credit data" refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “expanded FCRA data" may also apply in this instance, and both can be used interchangeably.

There are many facets to promoting a more equitable society. One major driver is financial inclusion or reducing the racial wealth gap for underserved communities. No other tool has impacted generational wealth more than sustainable homeownership. However, the underserved and underbanked home buyers experience more barriers to entry than any other consumer segment. It is important to recognize the well-documented racial and ethnic homeownership gap; doing so will not only benefit the impacted communities, but also elevate the level of support of those lenders who serve them. What are we doing as an industry to reduce this gap? Many organizations are doing their part in removing barriers to homeownership and systemic inequities. In 2021, the FHFA published their Duty to Serve 2021 plans for Fannie Mae and Freddie Mac to focus on historically underserved markets. A part of this plan includes increasing liquidity of mortgage financing for lower- and moderate-income families. Fannie Mae and Freddie Mac each announced individual refinance offerings for lower-income homeowners – Fannie Mae’s RefiNow™ and Freddie Mac’s Refi PossibleSM. Eligible borrowers meet requirements including income at or below 100% area median income (AMI), a minimum credit score of 620, consideration for loans in forbearance and additional newly expanded flexibilities. As part of the plan, lenders will lower a borrower’s monthly payment by at least a half a percentage point reduction in their interest rate, which can translate into hundreds of dollars of savings per month and sustain their homeownership. Experian has the tools to help mortgage lenders take advantage of this offering As a leader in data, analytics and technology, we have the tools needed to help lenders recognize opportunities to be inclusive and identify borrowers who may be eligible for Fannie Mae’s and Freddie Mac’s lower-income refinance offerings. To illustrate, we performed a data study and identified over 6M eligible mortgages nationwide (impacting over 8M borrowers) for this plan, and some lenders had as much as 30% of mortgages in their portfolio eligible with lower- and moderate-incomes.1 These insights can have a positive impact on the borrowers you serve by promoting more inclusion and benefit lenders through improved customer retention, strengthened customer loyalty and an opportunity to continue to build generational wealth through housing. We are committed to enabling the industry's DEI evolution As the Consumer’s bureau, empowering consumers is at the heart of everything we do. We’re committed to developing products and services that increase credit access, greater inclusion in homeownership and narrowing the racial wealth gap. Below are a few of our recent initiatives, and be sure to check out our financial inclusion resources here: United for Financial Health: Promotes inclusion in underserved communities through partnerships and have committed to investing our time and resources to create a more inclusive tomorrow for our communities. Project REACh (Roundtable for Economic Access and Change): brings together leaders from banking, business, technology, and national civil rights organizations to reduce barriers that prevent equal and fair participation in the nation’s economy, and we are engaged with the Alternative Credit Scoring Utility group as part of this initiative. Operation Hope: Empowers youth and underserved communities to improve their financial health through education, so they can thrive (not just survive) in the credit ecosystem so they can sustain good credit and responsibly use credit. DEI-Centric Solutions: From Experian Boost to our recent launch of Experian Go, we offer a variety of consumer solutions designed to empower consumers to gain access to credit and build a brighter financial future. What does this mean for you? Our passion, knowledge and partnerships in DEI have enabled us to share best practices and can help lenders prescriptively look at their portfolios to create inclusive growth strategies, identify gaps, and track progress towards diversity objectives. The mortgage industry has a unique opportunity to create paths to homeownership for underserved communities. Together, we can drive impact for generations of Americans to come. Let’s drive inclusivity and revive the American dream of homeownership. 1Experian Ascend™ as of November 2021

Despite the constant narrative around “unprecedented times” and the “new normal,” if the current market volatility tells us anything, it’s to go back to basics. As financial institutions navigate COVID-19’s economic impact, and challenges that are likely to be different or more extreme than in the past, the best credit portfolio management practices are fundamental. The global pandemic impacts today’s data as existing data and analytics may not accurately reflect what is happening now, resulting in inaccurate portfolio assessment. In order to successfully navigate loss forecasting, predicting borrower behavior and controlling loss ratios, lenders must engage new data, analytics and economic scenarios suited for today’s changing times. In Experian’s latest white paper, “Credit Portfolio Management After the COVID-19 Recession,” we’ll explore best practices to combat the following challenges: Forecasting credit losses despite increased economic volatility Businesses have long used a variety of data, analytics and models to anticipate and project the future direction of their organization based on a number of data points; however, with the onset of the global pandemic, long-standing scenarios became suddenly irrelevant. Predicting borrower behavior given increased financial disparities The post-pandemic and pre-pandemic worlds are very different places for some borrowers. Pandemic-related job losses and other economic effects will not be spread evenly and this variability may be reflected in lenders’ portfolios. Controlling loss ratios In the post-COVID world, it will be mission critical for lenders to use high-quality and up-to-date data to balance priorities and identify which areas of their portfolio need attention now. Whether your portfolio is doing better than expected, as expected, or worse than expected, now is the time to refresh portfolio management strategy. Lenders should be watching for early indicators in loan portfolios to better navigate a fluctuating economy and that requires new resources and better tools. Take control of your business’ trajectory. Download now

In 2015, U.S. card issuers raced to start issuing EMV (Europay, Mastercard, and Visa) payment cards to take advantage of the new fraud prevention technology. Counterfeit credit card fraud rose by nearly 40% from 2014 to 2016, (Aite Group, 2017) fueled by bad actors trying to maximize their return on compromised payment card data. Today, we anticipate a similar tsunami of fraud ahead of the Social Security Administration (SSA) rollout of electronic Consent Based Social Security Number Verification (eCBSV). Synthetic identities, defined as fictitious identities existing only on paper, have been a continual challenge for financial institutions. These identities slip past traditional account opening identity checks and can sit silently in portfolios performing exceptionally well, maximizing credit exposure over time. As synthetic identities mature, they may be used to farm new synthetics through authorized user additions, increasing the overall exposure and potential for financial gain. This cycle continues until the bad actor decides to cash out, often aggressively using entire credit lines and overdrawing deposit accounts, before disappearing without a trace. The ongoing challenges faced by financial institutions have been recognized and the SSA has created an electronic Consent Based Social Security Number Verification process to protect vulnerable populations. This process allows financial institutions to verify that the Social Security number (SSN) being used by an applicant or customer matches the name. This emerging capability to verify SSN issuance will drastically improve the ability to detect synthetic identities. In response, it is expected that bad actors who have spent months, if not years, creating and maturing synthetic identities will look to monetize these efforts in the upcoming months, before eCBSV is more widely adopted. Compounding the anticipated synthetic identity fraud spike resulting from eCBSV, financial institutions’ consumer-friendly responses to COVID-19 may prove to be a lucrative incentive for bad actors to cash out on their existing synthetic identities. A combination of expanded allowances for exceeding credit limits, more generous overdraft policies, loosened payment strategies, and relaxed collection efforts provide the opportunity for more financial gain. Deteriorating performance may be disguised by the anticipation of increased credit risk, allowing these accounts to remain undetected on their path to bust out. While responding to consumers’ requests for assistance and implementing new, consumer-friendly policies and practices to aid in impacts from COVID-19, financial institutions should not overlook opportunities to layer in fraud risk detection and mitigation efforts. Practicing synthetic identity detection and risk mitigation begins in account opening. But it doesn’t stop there. A strong synthetic identity protection plan continues throughout the account life cycle. Portfolio management efforts that include synthetic identity risk evaluation at key control points are critical for detecting accounts that are on the verge of going bad. Financial institutions can protect themselves by incorporating a balance of detection efforts with appropriate risk actions and authentication measures. Understanding their portfolio is a critical first step, allowing them to find patterns of identity evolution, usage, and connections to other consumers that can indicate potential risk of fraud. Once risk tiers are established within the portfolio, existing controls can help catch bad accounts and minimize the resulting losses. For example, including scores designed to determine the risk of synthetic identity, and bust out scores, can identify seemingly good customers who are beginning to display risky tendencies or attempting to farm new synthetic identities. While we continue to see financial institutions focus on customer experience, especially in times of uncertainty, it is paramount that these efforts are not undermined by bad actors looking to exploit assistance programs. Layering in contextual risk assessments throughout the lifecycle of financial accounts will allow organizations to continue to provide excellent service to good customers while reducing the increasing risk of synthetic identity fraud loss. Prevent SID

Account management is a critical strategy during any type of economy (pro-cycle, counter-cycle, cycle neutral). In times like these, marked by economic volatility, it is an effective way to identify which parts of your portfolio and which of your consumers need the most attention. Check out this podcast where Cyndy Chang, Senior Director of Product Management, and Craig Wilson, Senior Director of Consulting, discuss the foundational elements of account management, best practices and use cases. Account management today looks very different than what it has been during over a decade of growth proactive; account review is a critical part of navigating the path forward. Questions that need to be addressed include: Do you have the right data? Are you monitoring between data loads? Are you reviewing accounts at the frequency that today’s changing demands require? Listen in on the discussion to learn more. Experian · Look Ahead Podcast

Today, Experian and Oliver Wyman launched the Ascend Portfolio Loss ForecasterTM, a solution built to help lenders make better decisions – during COVID-19 and beyond – with customized forecasts and macroeconomic data. Phrases like “the new normal,” “unprecedented times,” and “extreme economic volatility” have flooded not only media for the last few months, but also financial institutions’ strategic discussions regarding plans to move forward. What has largely been crisis response is quickly shifting to an urgent need to answer the many questions around “Will we survive this crisis?,” let alone “What’s next?” And arguably, we’ve entered a new era of loss forecasting. After the longest period of economic growth in post-war U.S. history, previously built models are not sufficient for the unprecedented and sudden changes in economic conditions due to COVID-19. Lenders need instant insights to assess impact and losses to their portfolios. The Ascend Portfolio Loss Forecaster combines advanced modeling from Oliver Wyman, pandemic-specific insights and macroeconomic scenarios from Oxford Economics, and Experian’s quality data to analyze and produce accurate loan loss forecasts. Additionally, all of the data, including the forecasts and models, are regularly updated as macroeconomic conditions change. “Experian’s agility and innovative technologies allow us to help lenders make informed decisions in real time to mitigate future risk,” said Greg Wright, chief product officer of Experian’s Consumer Information Services, in a recent press release. “We’re proud to work with our partners, Oxford Economics and Oliver Wyman, to bring lenders a product powered by machine learning, comprehensive data and macroeconomic forecast scenarios.” Built using advanced modeling and expert scenarios, the web-based application maximizes the more than 15 years of Experian’s loan-level data, including VantageScore® credit score, bankruptcy scores and customer-level attributes. Financial institutions can gauge loan portfolio performance under various scenarios. “It is important that the banks take into account the evolving credit behaviors due to the COVID-19 pandemic, in addition to the robust modeling technique for their loss forecasting and strategic decisioning,” said Anshul Verma, senior director of products at Oliver Wyman, also in the release. “With the Ascend Portfolio Loss Forecaster, lenders get robust models that work in the current conditions and take into account evolving consumer behaviors,” Verma said. To watch Experian’s webinar on portfolio loss forecasting, please click here and to learn more about the Ascend Portfolio Loss Forecaster, click the button below. Learn More

While an overdue economic downturn has been long discussed, arguably no one could have foreseen the economic disruption from COVID-19 to the extent that’s been witnessed thus far. But now that we’re here, is there a line of sight to financial institutions’ next move? With the current situation marked by a history-making rise in unemployment, massive amounts of uncertainty within the market as well as for consumers and small businesses and consumer spending changes, loss forecasting is more important now than ever before. After the longest period of economic growth in history, financial institutions are caught off guard. While large banks are more prepared as they have stress testing capabilities in place and are estimating the potential large impact on their loss allowances, the since-delayed CECL requirements emphasized forecasting for the masses, and yet many are still under-equipped. Loss forecasting has evolved from a need for a small few to now a necessary strategy for all. While some financial institutions will look to loss forecasting to potentially reduce the severity of impact for the path ahead during these times (or even how they might come out stronger than their competition), for many, loss forecasting is the key to survival. Bare necessities. Understanding the possible outcomes of the pandemic’s impact is necessary to make critical business decisions. Lenders are likely receiving numerous questions about their portfolios and possible outcomes. These questions include, but are not limited to: What could the range of outcomes to my portfolio based on expert forecasts of macroeconomic conditions? How will I make lending decisions in the short term? Do my models need to change? How bad could charge offs be for my portfolio? If I have reduced marketing and application flows, at what point do I need to begin opening new accounts or consider portfolio acquisitions? How can lenders get answers? Loss forecasting. As Mohammed Chaudhri, Experian Chief Economist, said, “Loss forecasting is more pivotal than ever…existing models are not going to be up to the task of accurately predicting losses.” Whatever questions you’re receiving, you need certain necessary pieces of information to navigate this new era of loss forecasting. Those pieces are frequently updated client and industry data; ongoing access to expert macroeconomic forecasts; and sophisticated and evolved forecasting models. Client and Industry Data Loan-level data, bankruptcy scores and customer-level attributes are key insights to fueling loss forecasting models. By combining several data sets and scores (and a comprehensive history of both) your organization can see greater benefits. Macroeconomic Forecasts As has been mentioned numerous times, the economic impact resulting from COVID-19 is not at all like the Great Recession. As such, leveraging macroeconomic forecasts, and specifically COVID-19 forecasts, is critical to analyzing the potential impacts to your organization. Sophisticated Models Whether building models on your own or leveraging an expert, the key ingredients include the innerworkings of the model, leveraging historical data and making sure that both the models and the data are updated regularly to ensure you have the most accurate, thorough forecasts available. Also, leveraging machine learning tools is imperative for model specification and evaluation. Fortunately, while model building and loss forecasting used to be synonymous with countless resources and dollar signs, innovation and digital transformation have made these strategies within reach for financial institutions of all sizes. Incorporating the right data (and ensuring that data is regularly updated), with the right tools and macroeconomic scenarios (including COVID-19, upside, baseline, adverse and severely adverse scenarios) enables you to get a line of sight into the actions you need to take now. Empowered with insights to compare and benchmark results, discover the cause of changes in results, explore result scenarios in advance, and access recommended optimizations, loss forecasting enables you to focus on the critical decisions your business depends on. Experian helps you with loss forecasting for now and the future. For more information, including an on-demand webinar Experian presented with Oliver Wyman as well as the opportunity to engage Experian experts into your loss forecasting strategy, please click the button below. Learn More