Tag: identity management

The gig economy — also called the sharing economy or access economy — is an activity where people earn income by providing on-demand work, services, or goods. Often, it is through a digital platform like an application (app) or website. The gig economy seamlessly connects individuals with a diverse range of services, whether it be a skilled handyman for those long-awaited office shelves, or an experienced chauffeur to quickly drive you to the airport to not miss your flight. However, there are instances when these arrangements fall short of expectations. The hired handyman may send a substitute who’s ill-equipped for the task, or the experienced driver takes the wrong shortcut leaving you scrambling to make your flight on time. On the flip side, there are numerous risks faced by those working in the gig/sharing economy, from irritable customers to dangerous situations. In such cases, trust takes a hit. The gig economy has witnessed a surge in recent years, as individuals gravitate towards flexible, freelance, and contract work instead of traditional full-time employment. This shift has unlocked a multitude of opportunities for both workers and businesses. Nevertheless, it has also ushered in challenges pertaining to security and trust. One such challenge revolves around the escalating significance of digital identity verification within the gig economy. Digital identity verification and the gig economy Digital identity verification encompasses validating a person's identity through digital means, such as biometric data, facial recognition, or document verification. Within the gig economy, this process has high importance, as it establishes trust between businesses and their pool of freelance or contract workers. With the escalating number of remote workers and the proliferation of online platforms connecting businesses with gig workers, verifying the identities of these individuals has become more vital than ever before. Protecting gig users and improving the customer experience One primary rationale behind the mounting importance of digital identity verification in the gig economy is its role in curbing fraud. As the gig economy gains traction, the risk of individuals misrepresenting themselves or their qualifications to secure work burgeons. This scenario can lead businesses to hire unqualified or even fraudulent workers, thereby posing severe repercussions for both the company and its customers. By adopting digital identity verification processes, businesses can ensure the legitimacy and competence of their workforce, subsequently decreasing the risk of fraudulent activities. In the digital age, trust and safety are crucial for businesses to succeed. Consumers prioritize brands they can trust, and broken trust can lead to loss of customers.According to Experian's 2023 Fraud and Identity Report, over 52% of US consumers feel they’re more of a target for online fraud than they were a year ago. As such, online security continues to be a real concern for most consumers. Nearly 64% of consumers say that they are very or somewhat concerned with online security, with 32% saying they are very concerned. Establishing trust and safety measures not only protects your brand but also enhances the user experience, fosters loyalty, and boosts your business. Role of a dedicated Trust and safety team Trust and safety are the set of business practices for online platforms to follow to reduce the risk of users being exposed to harm, fraud, or other behaviors outside community guidelines. This is becoming an increasingly important function as online platforms look to protect their users while improving customer acquisition, engagement, and retention. That team also safeguards organizations from security threats and scams. They verify customers' identities, evaluate actions and intentions, and ensure a safe environment for all platform users. This enables both organizations and customers to trust each other and have confidence in the platform. Their role has evolved from fraud prevention to encompass broader areas, such as user-generated content and the metaverse. With the rise of user-generated content, platforms face challenges like fake accounts, imitations, malicious links, and inappropriate content. As a result, trust and safety teams have expanded their focus and are involved in product engineering and customer journey design. Another noteworthy factor contributing to the growing emphasis on digital identity verification for trust and safety teams stems from the necessity to adhere to diverse regulations and laws. Many countries have implemented stringent regulations to safeguard workers and ensure the legal and ethical operations of businesses. In the United States, for instance, businesses must verify the identities and work eligibility of all employees, including freelancers and contractors, as part of the Form I-9 process. By leveraging digital identity verification tools, businesses can streamline these procedures and guarantee compliance with prevailing regulations. Mitigating risk in online marketplaces To mitigate risks in online marketplaces, businesses can take several steps, including creating a clear set of user guidelines, implementing identity verification during onboarding, enforcing multi-factor authentication for all accounts, leveraging reverification during high-risk moments, performing link analysis on the user base, and applying automation. Online identity verification plays a pivotal role in safeguarding gig workers themselves. With the surge of online platforms connecting businesses with freelancers and contractors, there comes an augmented risk of workers falling prey to scams or identity theft. By mandating digital identity verification as an integral part of the onboarding process, these platforms can shield workers and ensure they only engage with bona fide businesses. While automation can be a powerful tool for fraud detection and mitigation, it is not a cure-all solution. Automated identity verification has its strengths, but it also has its weaknesses. While automation can spot risk signals that a human might miss, a human might spot risk signals that automation would have skipped. Therefore, for many companies, the goal should not be full automation but achieving the right ratio of automation to manual review. Manual review takes time, but it's necessary to ensure that all potential risks are identified and addressed. The more efficient these processes can be, the better, as it allows for a quicker response to potential threats. As the number of individuals embracing freelance and contract work surges, and businesses increasingly rely on these workers to carry out vital responsibilities, ensuring the security and trustworthiness of these individuals becomes paramount. By integrating digital identity verification processes, businesses can shield themselves against fraud, comply with regulations, and cultivate trust with their gig workers. Finding the right partner While trust and safety are concerns for all online marketplaces, there’s no universal solution that will apply to all businesses and in all cases. Your trust and safety policies need to be tailored to the realities of your business. The industries you serve, regions you operate in, regulations you are subject to, and expectations of your users should all inform your processes. Experian’s comprehensive suite of customizable identity verification solutions can help you solve the problem of trust and safety once and for all. Learn more *This article leverages/includes content created by an AI language model and is intended to provide general information.

As the sophistication of fraudulent schemes increases, so must the sophistication of your fraud detection analytics. This is especially important in an uncertain economic environment that breeds opportunities for fraud. It's no longer enough to rely on old techniques that worked in the past. Instead, you need to be plugged into machine learning, artificial intelligence (AI) and real-time monitoring to stay ahead of criminal attempts. Your customers have come to expect cutting-edge security, and fraud analytics is the best way to meet — and surpass — those expectations. Leveraging these analytics can help your business better understand fraud techniques, uncover hidden insights and make more strategic decisions. What is fraud analytics? Fraud analytics refers to the idea of preventing fraud through sophisticated data analysis that utilizes tools like machine learning, data mining and predictive AI.1 These services can analyze patterns and monitor for anomalies that signal fraud attempts.2 While at first glance this may sound like a lot of work, it's necessary in today's technologically savvy culture. Fraud attempts are becoming more sophisticated, and your fraud detection services must do the same to keep up. Why is fraud analytics so important? According to the Experian® 2023 US Identity and Fraud Report, fraud is a growing issue that businesses cannot ignore, especially in an environment where economic uncertainty provides a breeding ground for fraudsters. Last year alone, consumers lost $8.8 billion — an increase of 30 percent over the previous year. Understandably, nearly two-thirds of consumers are at least somewhat concerned about online security. Their worries range from authorized push payment scams (such as phishing emails) to online privacy, identity theft and stolen credit cards. Unfortunately, while 75 percent of surveyed businesses feel confident in protecting against fraud, only 45 percent understand how fraud impacts their business. There's a lot of unearned confidence out there that can leave businesses vulnerable to attack, especially with nearly 70 percent of businesses admitting an increase in fraud loss in recent years. The types of fraud that businesses most frequently encounter include: Authorized push payment fraud: Phishing emails and other schemes that persuade consumers to deposit funds into fraudulent accounts. Transactional payment fraud: When fraudulent actors steal credit card or bank account information, for example, to make unauthorized payments. Account takeover: When a fraudster gains access to an account that doesn't belong to them and changes login details to make unauthorized transactions. First-party fraud: When an account holder uses their own account to commit fraud, like misrepresenting their income to get a lower loan rate. Identity theft: Any time a person's private information is used to steal their identity. Synthetic identity theft: When someone combines real and fake personal data to create an identity that's used to commit fraud. How can fraud analytics be used to help your business? More than 85% of consumers expect businesses to respond to their security and fraud concerns. A good portion of them (67 percent) are even ready to share their personal data with trusted sources to help make that happen. This means that investing in risk and fraud analytics is not only vital for keeping your business and customer data secure, but it will score points with your consumers as well. So how can your business utilize fraud analytics? Machine learning is a great place to start. Rather than relying on outdated rules-based analytic models, machine learning can vastly increase your speed in identifying fraud attempts. This means that when a new fraudulent trend emerges, your machine learning software can pinpoint it fast and flag your security team. Machine learning also lets you automatically analyze large data sets across your entire customer portfolio, improving customer experiences and your response time. In general, the best way for your business to use fraud analytics is by utilizing a multi-layered approach, such as the robust fraud management solutions offered by Experian. Instead of a one-size-fits-all solution, Experian lets you customize a framework of physical and digital data security that matches your business needs. This framework includes a cloud-based platform, machine learning for streamlined data analytics, biometrics and other robust identity-authentication tools, real-time alerts and end-to-end integration. How Experian can help Experian's platform of fraud prevention solutions and advanced data analytics allows you to be at the forefront of fraud detection. The platform includes options such as: Account takeover prevention. Account takeovers can go unnoticed without strong fraud detection. Experian's account takeover prevention tools automatically flag and monitor unusual activities, increase efficiency and can be quickly modified to adapt to the latest technologies. Bust-out fraud prevention. Experian utilizes proactive monitoring and early detection via machine learning to prevent bust-out fraud. Access to premium credit data helps enhance detection. Commercial entity fraud prevention. Experian's Sentinel fraud solutions blend consumer and business datasets to create predictive insights on business legitimacy and credit abuse likelihood. First-party fraud prevention. Experian's first-party fraud prevention tools review millions of transactions to detect patterns, using machine learning to monitor credit data and observations. Global data breach protection. Experian also offers data breach protection services, helping you use turnkey solutions to build a program of customer notifications and identity protection. Identity protection. Experian offers identity protection tools that deliver a consistent brand experience across touchpoints and devices. Risk-based authentication. Minimize risk with Experian's adaptive risk-based authentication tools. These tools use front- and back-end authentication to optimize cost, risk management and customer experience. Synthetic identity fraud protection. Synthetic identity fraud protection guards against the fastest-growing financial crimes. Automated detection rules evaluate behavior and isolate traits to reduce false positives. Third-party fraud prevention. Experian utilizes third-party prevention analytics to identify potential identity theft and keep your customers secure. Your business's fraud analytics system needs to increase in sophistication faster than fraudsters are fine-tuning their own approaches. Experian's robust analytics solutions utilize extensive consumer and commercial data that can be customized to your business's unique security needs. Experian can help secure your business from fraud Experian is committed to helping you optimize your fraud analytics. Find out today how our fraud management solutions can help you. Learn more 1 Pressley, J.P. "Why Banks Are Using Advanced Analytics for Faster Fraud Detection," BizTech, July 25, 2023. https://biztechmagazine.com/article/2023/07/why-banks-are-using-advanced-analytics-faster-fraud-detection 2 Coe, Martin and Melton, Olivia. "Fraud Basics," Fraud Magazine, March/April 2022. https://www.fraud-magazine.com/article.aspx?id=4295017143

This article was originally published on multifamilyinsiders.com One of the challenges currently facing the rental housing industry is the amount of lease application fraud. An Entrata study found a 111% increase in lease application fraud between 2019 and 2020. In the same study, 55% of surveyed apartment managers and rental operators said their properties experience fraudulent lease application attempts every few months, and 15% said their communities were subjected to multiple attempts each month. One-third of respondents described themselves as "very concerned" about application fraud. Just as alarming as the rise in attempts is the apparent likelihood of success. In the study, 65% of apartment managers said they are not confident in their current fraud prevention efforts. Some applicants can use a range of tools to commit fraud such as fake pay stubs, bank statements, employment records, and other falsified documents. Unfortunately, readily available computer technology makes it all too easy for applicants to produce these falsified documents. Tools to fight against fraud Apartment communities that rely on an overly manual screening process may find themselves at a disadvantage in the current landscape. Relying on associates to manually verify things like income and employment history can increase the risk of a deceitful applicant being successful. In addition, these processes can be extraordinarily time-consuming, which means leasing associates have less bandwidth for their many other important duties and responsibilities. Not to mention, the units stay unoccupied while these time-consuming verifications are being done manually. Among the general screening technologies that operators should consider: Automated verification of income, assets and employment — These solutions eliminate the need for operators to collect this kind of documentation from applicants. Furthermore, it eliminates the opportunity for applicants to supply falsified supporting documentation. Frictionless authentication — A multi-layered identity verification process for those applying for rental housing, frictionless authentication detects the subtle and not-so-subtle signs that an applicant is, to one degree or another, using a false identity. By highlighting discrepancies, the process assigns a “score” to quantify the likelihood that misrepresentation is taking place. Additional confirmation of the applicant’s identity can be completed using a one-time passcode (OTP) or knowledge-based authentication (KBA). This technology also uses device intelligence to recognize the risks associated with the physical devices (such as computers, tablets, and smartphones) that consumers use for online applications to identify potential imposters. In today's landscape, apartment owners and operators need to make sure they're protecting themselves against fraudulent applicants, who may not fulfill their financial obligations as outlined in their leases. By embracing the ever-growing array of advanced screening tools and technologies, owners and operators can achieve that protection and reduce their risk significantly — and save their associates time and energy.

Trust is the primary factor in any business building a long-lasting relationship, especially when a company operates globally and wants to build a loyal customer base. With the rapid acceleration of digital shopping and transactions comes a growing fraud landscape. And, given the continual increase of people wanting to transact online, marketplace companies – from ecommerce apps, ridesharing, to rental companies – need to have ideal strategies in place to protect themselves and their customers from fraudulent activities. Without ideal risk mitigation or comprehensive fraud and identity proofing strategies, marketplaces may find themselves facing the following: Card-not-present (CNP) Fraud: As online shopping increases, customers can’t provide a credit card directly to the merchant. That’s why fraudsters can use stolen credit card information to make unauthorized transactions. And in most cases, card owners are unaware of being compromised. Without an integrated view of risk, existing credit card authentication services used in isolation can result in high false positives, friction and a lack of card issuer support. Unverified Consumer Members, Vendors, Hosts & Drivers: From digital marketplace merchants like Etsy and Amazon, to peer-to-peer sharing economies like AirBnB, Uber and Lyft, the marketplace ecosystem is prone to bad actors who use false ID techniques to exploit both the platform and consumers for monetary gain. Additionally, card transaction touchpoints across the customer lifecycle increases risks of credit card authentication. This can be at account opening, account management when changes to existing account information is necessary, or at checkout. Buy Now, Pay Later (BNPL) Muling: While a convenient way for consumers to plan for their purchases, experts warn that without cautionary and security measures, BNPL can be a target for digital fraud. Fraudsters may use their own or fabricated identities or leverage account takeover to gain access to a legitimate user’s account and payment information to make purchases with no intent to repay. This leaves the BNPL provider at the risk of unrecoverable monetary losses that can impact the business’ risk tolerance. Forged Listings & Fake Accounts: Unauthorized vendors that create a fake account using falsified identities, stolen credit cards and publish fake listings and product reviews are another threat faced by ecommerce marketplaces. These types of fraud can happen without the vast data sources necessary to assess the risk of a customer and authenticate credit cards among other fraud and identity verification solutions. By not focusing on establishing trust, fraud mitigation management solutions and identity proofing strategies, businesses can often find themselves with serious monetary, reputational, and security qualms. Interested in learning more? Download Experian’s Building Trust in Digital Marketplaces e-book and discover the strategies digital marketplaces, like the gig economy and peer-to-peer markets, can take to keep their users safe, and protected from fraudulent activity. For additional information on how Experian is helping businesses mitigate fraud, explore our comprehensive suite of identity and fraud solutions. Download e-book

Experian’s eighth annual identity and fraud report found that consumers continue to express concerns with online security, and while businesses are concerned with fraud, only half fully understand its impact – a problem we previously explored in last year’s global fraud report. In our latest report, we explore today’s evolving fraud landscape and influence on identity, the consumer experience, and business strategies. We surveyed more than 2,000 U.S. consumers and 200 U.S. businesses about their concerns, priorities, and investments for our 2023 Identity and Fraud Report. This year’s report dives into: Consumer concerns around identity theft, credit card fraud, online privacy, and scams such as phishing.Business allocation to fraud management solutions across industries.Consumer expectations for both security and their experience.The benefits of a layered solution that leverages identity resolution, identity management, multifactor authentication solutions, and more. To identify and treat each fraud type appropriately, you need a layered approach that keeps up with ever-changing fraud and applies the right friction at the right time using identity verification solutions, real-time fraud risk alerts, and enterprise orchestration. This method can reduce fraud risks and help provide a more streamlined, unified experience for your consumers. To learn more about our findings and how to implement an effective solution, download Experian’s 2023 Identity and Fraud Report. Download the report

A data-driven customer experience certainly has a nice ring, but can your organization deliver on the promise? What we're really getting at is whether you can provide convenience and personalization throughout the customer journey. Using data to personalize the customer journey About half of consumers say personalization is the most important aspect of their online experience. Forward-thinking lenders know this and are working to implement digital transformations, with 87 percent of business leaders stating that digital acceleration has made them more reliant on quality data and insights. For many organizations, lack of data isn't the issue — it's collecting, cleaning and organizing this data. This is especially difficult if your departments are siloed or if you're looking to incorporate external data. What's more, you would need the capabilities to analyze and execute the data if you want to gain meaningful insights and results. LEARN: Infographic: Automated Loan Underwriting Journey Taking a closer look at two important parts of the customer journey, here's how the right data can help you deliver an exceptional user experience. Prescreening To grow your business, you want to identify creditworthy consumers who are likely to respond to your credit offers. Conversely, it's important to avoid engaging consumers who aren't seeking credit or may not meet your credit criteria. Some of the external data points you can incorporate into a digital prescreening strategy are: Core demographics: Identify your best customers based on core demographics, such as location, marital status, family size, education and household income. Lifestyle and financial preferences: Understand how consumers spend their time and money. Home and auto loan use: Gain insight into whether someone rents or owns a home, or if they'll likely buy a new or used vehicle in the upcoming months. Optimized credit marketing strategies can also use standard (and custom) attributes and scores, enabling you to segment your list and create more personalized offers. And by combining credit and marketing data, you can gain a more complete picture of consumers to better understand their preferred channels and meet them where they are. CASE STUDY: Clear Mountain Bank used Digital Prescreen with Micronotes to extend pre-approved offers to consumers who met their predetermined criteria. The refinance marketing campaign generated over $1 million in incremental loans in just two months and saved customers an average of $1,615. Originations Once your precise targeting strategy drives qualified consumers to your application, your data-driven experience can offer a low-friction and highly automated originations process. Alternative credit data: Using traditional and alternative credit data* (or expanded FCRA-regulated data), including consumer-permissioned data, allows you to expand your lending universe, offer more favorable terms to a wider pool of applicants and automate approvals without taking on additional risk. Behavioral and device data: Leveraging behavioral and device data, along with database verifications, enables you to passively authenticate applicants and minimize friction. Linked and digital applications: Offering a fully digital and intuitive experience will appeal to many consumers. In fact, 81 percent of consumers think more highly of brands after a positive digital experience that included multiple touchpoints. And if you automate verifications and prefill applications, you can further create a seamless customer experience. READ: White paper: Getting AI-driven decisioning right in financial services Personalization depends on persistent identification The vast majority (91 percent) of businesses think that improving their digital customer journey is very important. And rightly so: By personalizing digital interactions, financial institutions can identify the right prospects, develop better-targeted marketing campaigns and stay competitive in a crowded market. DOWNLOAD: A 5-Step Checklist for Identifying Credit-Active Prospect To do this, you need an identity management platform that enables you to create a single view of your customer based on data streams from multiple sources and platforms. From marketing to account management, you can use this persistent identity to inform your decisions. This way, you can ensure you're delivering relevant interactions and offers to consumers no matter where they are. WATCH: Webinar: Omnichannel Marketing - Think Outside the Mailbox Personalization offers a win-win Although they want personalization, only 33 percent of consumers have high confidence in a business' ability to recognize them repeatedly.4 To meet consumer expectations and remain competitive, you must deliver digital experiences that are relevant, seamless, and cohesive. Experian Consumer View helps you make a good first impression with consumer insights based on credit bureau and modeled data. Enrich your internal data, and use segmentation solutions to further refine your target population and create offers that resonate and appeal. You can then quickly deliver customized and highly targeted campaigns across 190 media destinations. From there, Experian Decisioning, an automated decisioning engine, can incorporate multiple external and internal data sources to optimize your strategy. *Disclaimer: When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.

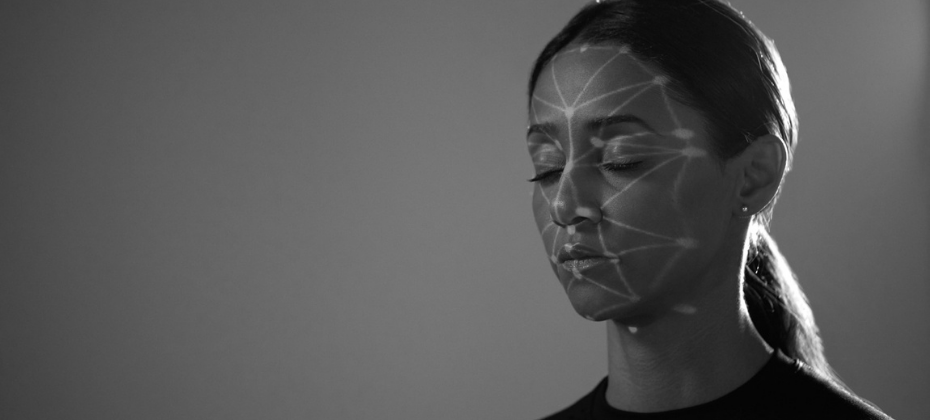

What Is Identity Proofing? Identity proofing, authentication and management are becoming increasingly complex and essential aspects of running a successful enterprise. Organizations need to get identity right if they want to comply with regulatory requirements and combat fraud. It's also becoming table stakes for making your customers feel safe and recognized. 63 percent of consumers expect businesses to recognize them online, and 48 percent say they're more trusting of businesses when they demonstrate signs of security. Identify proofing is the process organizations use to collect, validate and verify information about someone. There are two goals — to confirm that the identity is real (i.e., it's not a synthetic identity) and to confirm that the person presenting the identity is its true owner. The identity proofing process also relates to and may overlap with other aspects of identity management. Identity proofing vs identity authentication Identity proofing generally takes place during the acquisition or origination stages of the customer lifecycle — before someone creates an account or signs up for a service. Identity authentication is the ongoing process of re-checking someone's identity or verifying that they have the authorization to make a request, such as when they're logging into an account or trying to make a large transaction. How does identity proofing work? Identity proofing typically involves three steps: resolution, validation, and verification. Resolution: The goal of the first step is to accurately identify the single, unique individual that the identity represents. Resolution is relatively easy when detailed identity information is provided. In the real world, collecting detailed data conflicts with the need to provide a good customer experience. Resolution still has to occur, but organizations have to resolve identities with the minimum amount of information. Validation: The validation step involves verifying that the person's information and documentation are legitimate, accurate and up to date. It potentially involves requesting additional evidence based on the level of assurance you need. Verification: The final step confirms that the claimed identity actually belongs to the person submitting the information. It may involve comparing physical documents or biometric data and liveness tests, such as a comparison of the driver's license to a selfie that the person uploads. Different levels of identity proofing may require various combinations of these steps, with higher-risk scenarios calling for additional checks such as biometric or address verification. Service providers can implement a range of methods based on their specific needs, including document verification, database validation, or knowledge-based authentication. Building an effective identity proofing strategy By requiring identity proofing before account opening, organizations can help detect and deter identity fraud and other crimes. You can use different online identity verification methods to implement an effective digital identity proofing and management system. These may include: Document verification plus biometric data: The consumer uploads a copy of an identification document, such as a driver's license, and takes a selfie or records a live video of their face. Database validations: The proofing solution verifies the shared identifying information, such as a name, date of birth, address and Social Security number against trusted databases, including credit bureau and government agency data. Knowledge-based authentication (KBA): The consumer answers knowledge-based questions, such as account information, to confirm their identity. It can be a helpful additional step, but they offer a low level of assurance, partially because data breaches have exposed many people's personal information. In part, the processes you'll use may depend on business policies, associated risks and industry regulations, such as know your customer (KYC) and anti-money laundering (AML) requirements. But organizations also have to balance security and ease of use. Each additional check or requirement you add to the identity proofing flow can help detect and prevent fraud, but the added friction they bring to your onboarding process can also leave customers frustrated — and even lead to customers abandoning the process altogether. Finding the right amount of friction can require a layered, risk-based approach. And running different checks during identity proofing can help you gauge the risk involved. For example, comparing information about a device, such as its location and IP address, to the information on an application. Or sending a one-time password (OTP) to a mobile device and checking whether the phone number is registered to the applicant's name. With the proper systems in place, you can use high-risk signals to dynamically adjust the proofing flow and require additional identity documents and checks. At the same time, if you already have a high level of assurance about the person's identity, you can allow them to quickly move through a low-friction flow. Experian goes beyond identity proofing Experian builds on its decades of experience with identity management and access to multidimensional data sources to help organizations onboard, authenticate and manage customer identities. Our identity proofing solutions are compliant with National Institute of Standards and Technology (NIST) and enable agencies to confidently verify user identities prior to or during account opening, biometric enrollment or while signing up for services. Learn more This article includes content created by an AI language model and is intended to provide general information.

Financial institutions have gone through a whirlwind in the last few years, with the pandemic forcing many to undergo digital transformations. More recently, rising interest rates and economic uncertainty are leading to a pullback, highlighting the need for lenders to level up their marketing strategies to win new customers. To get started, here are a few key trends to look out for in the new year and fresh marketing ideas for lenders. Challenges and consumers expectations in 2023 It might be cliche to mention the impact that the pandemic had on digital transformations — but that doesn't make it any less true. Consumers now expect a straightforward online experience. And while they may be willing to endure a slightly more manual process for certain purchases in their life, that's not always necessary. Lenders are investing in front-end platforms and behind-the-scenes technology to offer borrowers faster and more intuitive services. For example, A McKinsey report from December 2021 highlighted the growth in nonbank mortgage lenders. It suggested nonbank lenders could hold onto and may continue taking market share as these tech-focused lenders create convenient, fast and transparent processes for borrowers.2 Marketers can take these new expectations to heart when discussing their products and services. To the extent you have one in place, highlight the digital experience that you can offer borrowers throughout the application, verifications, closing and loan servicing. You can also try to show rather than tell with interactive online content and videos. Build a data-driven mortgage lending marketing strategy The McKinsey report also highlighted a trend in major bank and nonbank lenders investing in proprietary and third-party technology and data to improve the customer experience.2 Marketers can similarly turn to a data-driven credit marketing strategy to help navigate shifting lending environments. Segment prospects with multidimensional data Successful marketers can incorporate the latest technological and multidimensional data sources to find, track and reach high-value prospects. By combining traditional credit data with marketing data and Fair Credit Report Act-compliant alternative credit data* (or expanded FCRA-regulated data), you can increase the likelihood of connecting with consumers who meet your credit criteria and will likely respond. For example, Experian's mortgage-specific In the Market Models predict a consumer's propensity to open a new mortgage within a one to four-month period based on various inputs, including trended credit data and Premier Attributes. You can use these propensity models as part of your prescreen criteria, to cross-sell current customers and to help retain customers who might be considering a new lender. But propensity models are only part of the equation, especially when you're trying to extend your marketing budget with hyper-segmented campaigns. Incorporating your internal CRM data and non-FCRA data can help you further distinguish look-alike populations and help you customize your messaging. LEARN MORE: Use this checklist to find and fix gaps in your prospecting strategy Maintain a single view of your borrowers An identity management platform can give you a single view of a consumer as they move through the customer journey. The persistent identity can also help you consistently reach consumers in a post-cookie world and contact them using their preferred channel. You can add to the persistent identity as you learn more about your prospects. However, you need to maintain data accuracy and integrity if you want to get a good ROI. Use triggers to guide your outreach You can also use data-backed credit triggers to implement your marketing plan. Experian's Prospect Triggers actively monitors a nationwide database to identify credit-active consumers who have new tradelines, inquiries or a loan nearing term. Lenders using Prospect Triggers can receive real-time or periodic updates and customize the results based on their screening strategy and criteria, such as score ranges and attributes. They can then make firm credit offers to the prospects who are most likely to respond, which can improve cross-selling opportunities along with originations. Benefit from our expertise Forward-thinking lenders should power their marketing strategies with a data-backed approach to incorporate the latest information from internal and external sources and reach the right customer at the right time and place. From list building to identity management and verification, you can turn to Experian to access the latest data and analytics tools. Learn about Experian credit prescreen and marketing solutions. Explore our credit prescreen solutions Learn about our marketing solutions 1Mortgage Bankers Association (October 2022). Mortgage Applications Decrease in Latest MBA Weekly Survey 2McKinsey & Company (2021). Five trends reshaping the US home mortgage industry

Kathleen Peters, Chief Innovation Officer, Decision Analytics for Experian, was recently featured on the Eliances Heroes podcast as part of the new weekly segment, the “Experian Identity Report.” In the introductory show, podcast host David Cogan, spoke with Kathleen about why identity is so important to our society. Listen to the podcast for the full discussion and see the transcript below. Learn more about Experian Identity David Cogan: How critical is it? Well, I’ll tell you. Payment fraud will exceed $206 billion in the next five years and let’s face it. Managing one’s personal identity is very complicated on its own and if the business enterprise managing customer identities in a strategic and secure way and scale across countless interaction is extremely complicated. And it’s only going to get more complex with the future from what I understand and all the technology that’s coming out if not by the day, by the hour. And that’s why we’re bringing this to you. Interviews with the world’s leading experts on the game changing impact of identity and the need to use reliable data to make confident decisions that securely accelerate customer engagement and that’s why we’re honored here today to have with us Kathleen Peters, Chief Innovation Officer, Experian Decision Analytics North America. Kathleen Peters: Thanks so much David, it’s great to be here with you. DC: $206 billion of payment fraud in the next five years? I mean who’s going to want to turn on their computer after this. That is a serious number. What do we do? KP: It’s really important that we get our arms around this both as consumers as well as businesses because we want to engage online. So much of what we’re doing is digital. It especially started in COVID when we were having our groceries delivered and everything else and even our grandparents are having to do their banking transactions online. The world is changing, and fraudsters take notice of that as well. Fraudsters are opportunistic and when they see a bunch of folks doing stuff online that they’ve never done before, they’re seeing that as an opportunity too. DC: You know the days of people horseback riding and overtaking trains are long gone and now it’s all digital. KP: It’s a lot easier these days. DC: Why is identity so important to our daily digital lives and in business? KP: It’s a great question, David. And as a consumer myself, you, and I when we transact online whether that’s to have food delivered, or I’m buying something for my kids or I’m even paying a bill, I want to be able to trust that my information will be safe, that my privacy will be protected and that my experience will be as smooth as possible. I think that’s what we all want. So as consumers and as businesses, how do we enable all the opportunities this new digital world is presenting to us in a way that we are safe and also businesses can transact with us securely and have confidence on who’s engaging with them online. DC: Let’s talk about identity. What really makes identity so challenging to manage at a business enterprise level especially with how complex the business portion is? KP: Absolutely. It really comes down to there are so many elements that comprise our identity. It’s multidimensional. So historically, when we think about identity, we probably think about the things that were on our DL or passport the kind of information that’s pretty static – name, address, SSN, date of birth – those kinds of things. Once we get online, that identity becomes a little more challenging. We’re not necessarily physically in front of the business that we’re engaging with so the business needs to determine if the person is who we say we are. There’s a famous Far Side comic from years ago where a dog is sitting in front of the computer and he says “On the internet, no one knows you’re a dog.” And that still rings true in that you need to be able to ensure that the customer that’s coming to your business online is a real person and not a bot, is a person with good intent and not a fraudster. You need to look no farther than some of the recent controversies around Twitter and Elon Musk’s on-again, off-again, on-again intent to buy the company. A few months ago he had pulled back because he wanted to know definitively how many users on Twitter are humans versus bots and sometimes determining that can be really hard. And that comes down to managing all these new definitions of identity. DC: That’s very important. The thing is businesses and consumers want to know really what to be able to do. So, what kinds of things is Experian able to offer to help with all of that? KP: We’re in a great position as Experian because we have such a depth and breadth of identity data. We have the analytics horsepower and really touchpoints that are really unique when it comes to thinking about identity. So we’ve been talking about these traditional identity elements and digital, online identity. When you think about it, Experian also really understands your financial identity. So when you bring those things together and a consumer is looking to maybe understand what their financial identity means, their credit score or even how to improve their credit score, Experian’s there. We’ve got a robust direct to consumer business, we’ve got offerings like Boost and Go that help people establish and build their credit. We’ve got marketplaces for cards, insurance, etc. And then when consumers want to open a new account at a financial institution, or a fintech, or a retailer, or even maybe buy some crypto or log into a business, Experian can bring that wealth of capability to help our clients, help businesses, separate those good consumers with good intent from the fraudsters and do that very quickly and efficiently so that consumers can have a great experience and build that trust with who they’re engaging with. DC: Kathleen, that’s really amazing. Alright, now with all of that going on, what is Experian doing now with innovating for the identity space? KP: This is a real passion of mine David and this is where I spend a lot of my time. We’re always looking ahead to see what is the new data, new capabilities that can help us improve that consumer experience and engagement, help clients find the right consumers online to engage and target, and really allow our clients to grow their businesses safely. So, we’re building some products in house, where we’re connecting new pieces that might be new to Experian like linking some of that traditional identity data with particular payment instruments. Is this Kathleen’s credit card? Is this my bank account? When I come and try to do transactions online. But we’re also partnering with new companies. There are a number of startups that are being formed that have been in business looking at new ways to stop fraud and new ways to help identify and authenticate users online. So, as we innovate, we’re building some things in house, we’re partnering, we’re investing in young companies, and sometimes we’re even acquiring. So, bringing together that breadth of data, analytics, really trying to think about what will be the next way that we’ll think about identifying ourselves online is some of the ways we’re innovating. DC: Well, we’re very fortunate to have you and your company here to be able to do that because it’s growing by leaps and bounds. I’m amazed by the number $206 billion which is probably going to go higher, so we’re very fortunate that Experian is around and really identifying this issue and trying to do something now. What do you think our audience will learn about these weekly, critical chats about identity with Experian experts? KP: These are going to be great conversations that we’re going to be able to share and talk about how rapidly things are changing and evolving and how this really relates to our daily lives and the things that are going on in this very dynamic economic climate, digital climate, the way things are changing the way we’re engaging. I think people are also going to learn a lot about Experian’s mission around financial inclusion and opportunity creation. We’re a very mission driven company and we’re the consumer’s bureau, so we want to do this journey in partnership with consumers so that you can take an active part in protecting yourself, understanding what’s going on, helping us fight fraud, but also just really be able to take advantage of all of these new opportunities in a safe way.

It’s time for organizations to harness the power artificial intelligence (AI) can bring to digital identity management – quickly and accurately identifying consumers throughout the lifecycle. The rise in crime The acceleration to digital platforms created a perfect storm of new opportunities for fraudsters. Synthetic identity fraud, stimulus-related fraud, and other types of cybercrime have seen huge upticks within the past year and a half. In fact, the Federal Trade Commission revealed that consumers reported over 360,000 complaints, resulting in more than $580 million in COVID-19-related fraud losses as of October 2021. To protect both themselves and consumers, businesses — especially lenders — will have to find and incorporate new strategies to identify customers, deter fraudsters and mitigate cybercrime. The benefits of AI for digital identity In our latest e-book, we explore the impacts of AI on organizations’ digital identity strategies, including: How changing consumer expectations increased the need for speed The challenges associated with both AI and digital identities The path forward for digital identity and AI How to develop the right strategy Building a solution It’s clear that current digital identity and fraud prevention tools are not enough to stop cybercriminals. To stay ahead of fraudsters and keep consumers happy, businesses need to look to new technologies — ones that can intake and compute large data sets in near-real time for better and faster decisions throughout the customer lifecycle. By using AI, businesses will enjoy a fast and consistent decisioning system that automatically routes questionable identities to additional authentication steps, allowing employees to focus on the riskiest cases and maximizing efficiency. Read our latest e-book to dive into the ways artificial intelligence and digital identity interact, and the benefits a clear identity strategy can have for the entire user journey. Download the e-book

Over the past year and a half, the development of digital identity has shifted the ways businesses interact with consumers. Companies across every industry have incorporated digital services, biometrics, and other verification tools to enhance the consumer experience without increasing risk. Changing consumer expectations A digital identity strategy is no longer a nice-to-have, it’s table stakes. Consumers expect to be recognized across platforms and have a seamless experience every time. 89% of consumers use mobile banking 80% of companies now have a customer recognition strategy in place 55% of banking customers say they plan to visit the bank branch less often moving forward Businesses are responding to these changing expectations while working to grow during the economic recovery – trying to balance consumer experience with risk appetite and bottom-line goals. The present state of digital identity Digital identity strategies require both standardization and interoperability. The first provides the ability to consistently capture data and characteristics that can be used to recognize a specific individual. The second allows businesses to resolve an identity to a specific person – recognizing a phone number, user ID and password, or a device – and use that information to determine if the user of the identity is in fact the identity owner. There are some roadblocks on the road to a seamless digital identity strategy. Issues include a lack of consumer trust and an ambiguous regulatory landscape – creating friction on both ends of the equation. Recipe for success To succeed, businesses need a framework that can reliably use different combinations of physical and digital identity data to determine that the person behind the identity is a known, verified, and unique individual. A one-size-fits-all solution doesn’t exist. However, a layered approach allows businesses to modernize identity, providing the services consumers want and expect while remaining agile in an ever-changing environment. In our newest white paper, developed in partnership with One World Identity, we explore the obstacles hindering digital identity management, and the best way to build a layered solution that is flexible, trustworthy, and inclusive. To learn more, download our “Capturing the Digital Evolution Through a Layered Approach” white paper. Download white paper

For the last several months, Experian has participated as the only credit bureau in the pilot of the electronic Consent Based Social Security Number (SSN) Verification (eCBSV) service. As we move forward to general rollout and expanded availability later this year, it’s time to review the benefits of eCBSV and how it helps businesses prevent synthetic identity fraud. Service and program overview The eCBSV service combats synthetic identity fraud by comparing data provided electronically by approved financial institutions against the Social Security Administration’s (SSA) database in real time. This service helps financial institutions verify SSNs more efficiently and enables improved experiences for identifying legitimate or possibly synthetic identities applying for your products. The verification process begins with consent from the SSN holder – and with eCBSV this consent is provided electronically rather than via a wet signature. Then, the SSN is checked against the SSA database to validate the SSN, name, and date of birth combination are or are not a match. The verification will also indicate if the SSN is listed as deceased with the SSA. Together, these factors can help flag whether or not an identity is synthetic. By managing this process electronically, it is faster, more secure, and more efficient than before, offering an improved experience for consumers and the financial institutions that service them. Layering solutions While eCBSV is an excellent step forward in the fight against the rising threat of synthetic identity fraud, a layered fraud mitigation strategy is still necessary. It’s only by layering solutions that financial institutions can accurately identify different types of fraud and provide them with the correct treatment, which is especially important when it comes to rooting out fraud when it’s already embedded in a portfolio. To learn more about how Experian is helping to combat synthetic identity fraud and how eCBSV can benefit your financial institution, request a call. Request a call

Although half of businesses globally report an increase in fraud management over the past 12 months, many still experience fraud losses and attacks. To help address these challenges, Experian held its first-ever Fintech Fraud & Identity Meetup on February 5 in San Francisco, Calif. The half-day event was aimed at offering insights on the main business drivers of fraud, market trends, challenges and technology advancements that impact identity management and fraud risk strategy operations. “We understand the digital landscape is changing – inevitably, with technology enhancements come increased fraud risk for businesses operating in the online space,” said Jon Bailey, Experian’s Vice President of Fintech. “Our focus today is on fraud and identity, and providing our fintech customers with the tools and insights needed to grow and thrive.” The meetup was attended by number of large fintech companies with services spanning across a broad spectrum of fintech offerings. To kick off the event, Tony Hadley, Experian’s Senior Vice President of Government & Regulatory Affairs, provided an update on the latest regulatory news and trends impacting data and the fintech space. Next followed a fraud and identity expert panel, which engaged seasoned professionals in an in-depth discussion around two main themes 1) fraud trends and risk mitigation; and 2) customer experience, convenience, and trust. Expert panelists included: David Britton, Experian’s Vice President of Industry Solutions; Travis Jarae, One World Identity’s Founder & CEO; George Kurtyka, Joust’s Co-Founder & COO; and Filip Verley, Airbnb’s Product Manager. “The pace of fraud is so fast, by the time companies implement solutions, the shelf-life may already be old,” Britton said. “That is the crux – how to stay ahead. The goal is to future-proof your fraud strategy and capabilities.” At the close of the expert panel, Kathleen Peters, Experian’s Senior Vice President Head of Fraud and Identity, demoed Experian’s CrossCore™ solution – the first smart, open, plug-and-play platform for fraud and identity services. Peters began by stating, “Fraud is constant. Over 60% of businesses report an increase in fraud-related losses over the past year, with the US leading the greatest level of concern. The best way to mitigate risk is to create a layered approach; that’s why Experian invented CrossCore.” With the sophistication of fraudsters, it’s no surprise that many businesses are not confident with the effectiveness of their fraud strategy. Learn more about how you can stay one step ahead of fraudsters and position yourself for success in the ever-changing fraud landscape; download Experian’s 2019 Global Identity and Fraud Report here. For an inside look at Experian’s Fintech Fraud & Identity Meetup, watch our video below.

Managing your customer accounts at the identity level is ambitious and necessary, but possible Identity-related fraud exposure and losses continue to grow. The underlying schemes have elevated in complexity. Because it’s more difficult to perpetrate “card present” fraud in the post–chip-and-signature rollout here in the United States, bad guys are more motivated and getting better at identity theft and synthetic identity attacks. Their organized nefarious response takes the form of alternate attack vectors and methodologies — which means you need to stamp out any detected exposure point in your fraud prevention strategies as soon as it’s detected. Experian’s recently published 2018 Global Fraud and Identity Report suggests two-thirds, or 7 out of every ten, consumers want to see visible security protocols when they transact. But an ever-growing percentage of them, fueled in no small part by those tech-savvy millennials, expect to be recognized with little or no friction. In fact, 42 percent of the surveyed consumers who stated they would do more transactions online if there weren’t so many security hurdles to overcome were — you guessed it — millennials. So how do you implement identity and account management procedures that are effective and, in some cases, even obvious while being passive enough to not add friction to the user experience? In other words, from the consumer’s perspective, “Let me know you know me and are protecting me but not making it too difficult for me when I want to access or manage my account.” Let’s get one thing out of the way first. This isn’t a one-time project or effort. It is, however, a commitment to the continued informing of your account management strategies with updated identity intelligence. You need to make better decisions on when to let a low-risk account transaction (monetary or nonmonetary) pass and when to double down a bit and step up authentication or risk assessment checks. I’d suggest this is most easily accomplished through a single, real-time access point to myriad services that should, at the very least, include: Identity verification and reverification checks for ongoing reaffirmation of your customer identity data quality and accuracy. Know Your Customer program requirements, anyone? Targeted identity risk scores and underlying attributes designed to isolate identity theft, first-party fraud and synthetic identity. Fraud risk comes in many flavors. So must your analytics. Device intelligence and risk assessment. A customer identity is no longer just their name, address, Social Security number and date of birth. It’s their phone number, email address and the various devices they use to access your services as well. Knowing how that combination of elements presents itself over time is critical. Layered passive or more active authentication options such as document verification, biometrics, behavioral metrics, knowledge-based verification and alternative data sources. Ongoing identity monitoring and proactive alerting and segmentation of customers whose identity risk has shifted to the point of required treatment. Orchestration, workflow and decisioning capabilities that allow your team to make sense of the many innovative options available in customer recognition and risk assessment — without a “throw the kitchen sink at this problem” approach that will undoubtedly be way too costly in dollars spent and good customers annoyed. Fraud attacks are dynamic. Your customers’ perceptions and expectations will continue to evolve. The markets you address and the services you provide will vary in risk and reward. An innovative marketplace of identity management services can overwhelm. Make sure your strategic identity management partner has good answers to all of this and enables you to future-proof your investments.

Reinventing Identity for the Digital Age Electronic Signature & Records Association (ESRA) conference I recently had the opportunity to speak at the Electronic Signature & Records Association (ESRA) conference in Washington D.C. I was part of a fantastic panel delving into the topic, ‘Reinventing Identity for the Digital Age.’ While certainly hard to do in just an hour, we gave it a go and the dialogue was engaging, healthy in debate, and a conversation that will continue on for years to come. The entirety of the discussion could be summarized as: An attempt to directionally define a digital identity today The future of ownership and potential monetization of trusted identities And the management of identities as they reside behind credentials or the foundations of block chain Again, big questions deserving of big answers. What I will suggest, however, is a definition of a digital identity to debate, embrace, or even deride. Digital identities, at a minimum, should now be considered as a triad of 1) verified personally identifiable information, 2) the collective set of devices through which that identity transacts, and 3) the transactional (monetary or non-monetary) history of that identity. Understanding all three components of an identity can allow institutions to engage with their customers with a more holistic view that will enable the establishment of omni-channel communications and accounts, trusted access credentials, and customer vs. account-level risk assessment and decisioning. In tandem with advances in credentialing and transactional authorization such as biometrics, block chain, and e-signatures, focus should also remain on what we at Experian consider the three pillars of identity relationship management: Identity proofing (verification that the person is who they claim to be at a specific point in time) Authentication (ongoing verification of a person’s identity) Identity management (ongoing monitoring of a person’s identity) As stronger credentialing facilitates more trust and open functionality in non-face-to-face transactions, more risk is inherently added to those credentials. Therefore, it becomes vital that a single snapshot approach to traditionally transaction-based authentication is replaced with a notion of identity relationship management that drives more contextual authentication. The context thus expands to triangulate previous identity proofing results, current transactional characteristics (risk and reward), and any updated risk attributes associated with the identity that can be gleaned. The bottom line is that identity risk changes over time. Some identities become more trustworthy … some become less so. Better credentials and more secure transactional rails improve our experiences as consumers and better protect our personal information. They cannot, however, replace the need to know what’s going on with the real person who owns those credentials or transacts on those rails. Consumers will continue to become more owners of their digital identity as they grant access to it across multiple applications. Institutions are already engaged in strategies to monetize trusted and shareable identities across markets. Realizing the dynamic nature of identity risk, and implementing methods to measure that risk over time, will better enable those two initiatives. Click here to read more about Identity Relationship Management.