Tag: financial habits

"Out with the old and in with the new" is often used when talking about a fresh start or change we make in life, such as getting a new job, breaking bad habits or making room in our closets for a new wardrobe. But the saying doesn't exactly hold true in terms of business growth. While acquiring new customers is critical, increasing customer retention rates by just 5% can increase profits by up to 95%.1 So, what can your organization do to improve customer retention? Here are three quick tips: Stay informed Keeping up with your customers’ changing interests, behaviors and life events enables you to identify retention opportunities and create personalized credit marketing campaigns. Are they new homeowners? Or likely to purchase a vehicle within the next five months? With a comprehensive consumer database, like Experian’s ConsumerView®, you can gain granular insights into who your customers are, what they do and even what they will potentially do. To further stay informed, you can also leverage Retention TriggersSM, which alert you of your customers changing credit needs, including when they shop for new credit, open a new trade or list their property. This way, you can respond with immediate and relevant retention offers. Be more than a business – be human Gen Z's spending power is projected to reach $12 trillion by 2030, and with 67% looking for a trusted source of personal finance information,2 financial institutions have an opportunity to build lifetime loyalty now by serving as their trusted financial partners and advisors. To do this, you can offer credit education tools and programs that empower your Gen Z customers to make smarter financial decisions. By providing them with educational resources, your younger customers will learn how to strengthen their financial profiles while continuing to trust and lean on your organization for their credit needs. Think outside the mailbox While direct mail is still an effective way to reach consumers, forward-thinking lenders are now also meeting their customers online. To ensure you’re getting in front of your customers where they spend most of their time, consider leveraging digital channels, such as email or mobile applications, when presenting and re-presenting credit offers. This is important as companies with omnichannel customer engagement strategies retain on average 89% of their customers compared to 33% of retention rates for companies with weak omnichannel strategies. Importance of customer retention Rather than centering most of your growth initiatives around customer acquisition, your organization should focus on holding on to your most profitable customers. To learn more about how your organization can develop an effective customer retention strategy, explore our marketing solutions. Increase customer retention today 1How investing in cardholder retention drives portfolio growth, Visa. 2Experian survey, 2023.

Today's top lenders use traditional and alternative credit data1 – or expanded Fair Credit Reporting Act (FCRA) regulated data – including consumer permissioned data, to enhance their credit decisioning. The ability to gain a more complete and timely understanding of consumers' financial situation allows lenders to better gauge creditworthiness, make faster decisions and grow their portfolios without taking on additional risk. Why lenders need to go beyond traditional credit data Traditional credit data is — and will remain — important to understanding the likelihood that a borrower will repay a loan as agreed. However, lenders who solely base credit decisions on traditional credit data and scores may overlook creditworthy consumers who don't qualify for a credit score — sometimes called unscorable or credit invisible consumers. Additionally, they may be spending time and money on manual reviews for applications that are low risk and should be automatically approved. Or extending offers that aren't a good fit. What is consumer permissioned data? Consumer permissioned data, or user permissioned data, includes transactional and account-level data, often from a bank, credit union or brokerage account, that a consumer gives permission to view and use in credit decisioning. To access the data, lenders create secure connections to financial institutions or data aggregators. The process and approach give consumers the power to authorize (and later retract) access to accounts of their choosing — putting them in control of their personal information — while setting up security measures that keep their information secure. In return for sharing access to their account information, consumers may qualify for more financial products and better terms on credit offers. What does consumer permissioned data include? Consumers can choose to share different types of information with lenders, including their account balances and transaction history. While there may be other sources for estimated or historic account-level data, permissioned data can be updated in real-time to give lenders the most accurate and timely view of a consumer's finances. There is also a wealth of information available within these transaction records. For example, consumers can use Experian Boost™ to get credit for non-traditional bills, including phone, utility, rent and streaming service payments. These bills generally don't appear in traditional credit reports and don't impact every type of credit score. But seeing a consumer's history of making these payments can be important for understanding their overall creditworthiness. What are the benefits of leveraging consumer permissioned data? You can incorporate consumer permissioned data into custom lending models, including the latest explainable machine learning models. As part of a loan origination system, the data can help with: Portfolio expansion Accessing and using new data can expand your lending universe in several ways. There are an estimated 28 million U.S. adults who don't have a credit file at the bureaus, and an additional 21 million who have a credit file but lack enough information to be scorable by conventional scoring models. These people aren't necessarily a credit risk — they're simply an unknown. Increased insights can help you understand the real risk and make an informed decision. Additionally, a deeper insight into consumers' creditworthiness allows you to swap in applications that are a good credit risk. In other words, approving applications that you wouldn't have been able to approve with an older credit decision process. Increase financial inclusion Many credit invisibles and thin-file applicants also fall into historically marginalized groups.2 Almost a third of adults in low-income neighborhoods are credit invisible.3 Black Americans are much more likely (1.8 times) to be credit invisible or unscorable than white Americans.4 Recent immigrants may have trouble accessing credit in the U.S., even if they had a good credit history in their home country.5 As a result, using consumer permissioned data to expand your portfolio can align with your financial inclusion efforts. It's one example of how financial inclusion is good for business and society. Enhance decisioning and minimize risk Consumer-permissioned data can also improve and expand automated decisions, which can be important throughout the entire loan underwriting journey. In particular, you may be able to: Verify income faster: By linking to consumers’ accounts and reviewing deposits, lenders can quickly verify their income and ability to pay. Make better decisions: Consumer permissioned data also give lenders a new lens for understanding an applicant’s credit risk, which can let you say yes more often without taking on additional risk. Process more applications: A better understanding of applicants’ credit risk can also decrease how many applications you send to manual review, which allows you to process more applications using the same resources. Increase customer satisfaction: Put it all together, and faster decisions and more approvals lead to happier customers. While consumer permissioned data can play a role in all of these, it's not the only type of alternative data that lenders use to grow their portfolios. What are other types of alternative data sources? In addition to consumer permissioned data, alternative credit data can include information from: Alternative financial services: Credit data from alternative financial services firms includes information on small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Rental agreement: Rent payment data from landlords, property managers, collection companies and rent payment services. Public records: Full-file public records go beyond what’s in a consumer’s credit report and can include professional and occupational licenses, property deeds and address history. Why partner with Experian? As an industry leader in consumer credit and data analytics, Experian is continuously building on its legacy in the credit space to help lenders access and use various types of alternative data. Along with Experian Boost™ for consumer permissioned data, Experian RentBureau and Clarity Services are trusted sources of alternative data that comply with the FCRA. Experian also offers services for lenders that want help understanding and using the data for marketing, lending and collections. For originations, the Lift Premium™ credit model can use alternative credit data to score over 65% of traditionally credit-invisible consumers. Expand your lending universe Lenders are turning to new data sources to expand their portfolios and remain competitive. The results can provide a win-win, as lenders can increase approvals and decrease application processing times without taking on more risk. At the same time, these new strategies are helping financial inclusion efforts and allowing more people to access the credit they need. Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.2-5Oliver Wyman (2022). Driving Growth With Greater Credit Access

From awarding bonus points on food delivery purchases to incorporating social media into their marketing efforts, credit card issuers have leveled up their acquisition strategies to attract and resonate with today’s consumers. But as appealing as these rewards may seem, many consumers are choosing not to own a credit card because of their inability to qualify for one. As card issuers go head-to-head in the battle to reach and connect with new consumers, they must implement more inclusive lending strategies to not only extend credit to underserved communities, but also grow their customer base. Here’s how card issuers can stay ahead: Reach: Look beyond the traditional credit scoring system With limited or no credit history, credit invisibles are often overlooked by lenders who rely solely on traditional credit information to determine applicants’ creditworthiness. This makes it difficult for credit invisibles to obtain financial products and services such as a credit card. However, not all credit invisibles are high-risk consumers and not every activity that could demonstrate their financial stability is captured by traditional data and scores. To better evaluate an applicant’s creditworthiness, lenders can leverage expanded data sources, such as an individual’s cash flow or bank account activity, as an additional lens into their financial health. With deeper insights into consumers’ banking behaviors, card issuers can more accurately assess their ability to pay and help historically disadvantaged populations increase their chances of approval. Not only will this empower underserved consumers to achieve their financial goals, but it provides card issuers with an opportunity to expand their customer base and improve profitability. Connect: Become a financial educator and advocate Credit card issuers looking to build lifelong relationships with new-to-credit consumers can do so by becoming their financial educator and mentor. Many new-to-credit consumers, such as Generation Z, are anxious about their finances but are interested in becoming financially literate. To help increase their credit understanding, card issuers can provide consumers with credit education tools and resources, such as infographics or ‘how-to’ guides, in their marketing campaigns. By learning about the basics and importance of credit, including what a credit score is and how to improve it, consumers can make smarter financial decisions, boost their creditworthiness, and stay loyal to the brand as they navigate their financial journeys. Accessing credit is a huge obstacle for consumers with limited or no credit history, but it doesn’t have to be. By leveraging expanded data sources and offering credit education to consumers, credit card issuers can approve more creditworthy applicants and unlock barriers to financial well-being. Visit us to learn about how Experian is helping businesses grow their portfolios and drive financial inclusion. Visit us

Millions of consumers are excluded from the credit economy, whether it’s because they have limited credit history, dated information within their credit file, or are a part of a historically disadvantaged group. Without credit, it can be difficult for consumers to access the tools and services they need to achieve their financial goals. This February, Experian surveyed over 1,000 consumers across census demographics, including income, ethnicity, and age, to understand the perceptions, needs, and barriers underserved communities face along their credit journey. Our research found that: 75% of consumers with an average household income of less than $50,000 have less than $1,000 in savings. 1 in 5 consumers with an average household income of less than $35,000 say they’re confident in getting approved for credit. 80% of respondents who are not or slightly confident in getting approved for credit were women. When asked why they believed they would not get approved for credit, participants shared common responses, such as having poor payment history, a low credit score, and insufficient income. Given these findings, what can lenders provide to help underserved consumers strengthen their financial profiles and gain access to the credit they need and deserve? The power of credit education While only 20% of respondents were familiar with credit education tools, the majority expressed interest in these offerings. With Experian, lenders can develop and implement credit education programs, tools, and solutions to help consumers understand their credit and the impact certain choices can have on their credit scores. From interactive tools like Score Simulator and Score Planner to real-time alerts from Credit Monitoring, consumers can actively assess their financial health, take steps to improve their creditworthiness, and ultimately become better candidates for credit offers. In turn, consumers can feel more confident and empowered to achieve their financial goals. Credit education tools not only help consumers increase their credit literacy, confidence, and chances of approval, but they also create opportunities for lenders to build lasting customer relationships. Consumers recognize that healthy credit plays an important role in their financial lives, and by helping them navigate the credit landscape, lenders can increase engagement, build loyalty, and enhance their brand’s reputation as an organization that cares about their customers. Empowering consumers with credit education is also a way for lenders to unlock new revenue streams. By learning to borrow, save, and spend responsibly, consumers can improve their creditworthiness and be in a better position to accept extended credit offerings, driving more cross-sell and upsell opportunities for lenders. More ways experian can help Experian is deeply committed to helping marginalized and low-income communities access the financial resources they need. In addition to our credit education tools, here are a few of our other offerings: Our expanded data helps lenders make better lending decisions by providing greater visibility and transparency around a consumer’s inquiry and payment behaviors. With a holistic view of their current and prospective customers, lenders can more accurately identify creditworthy applicants, uncover new growth opportunities, and expand access to credit for underserved consumers. Experian GoTM is a free, first-of-its-kind program to help credit invisibles and those with limited credit histories begin building credit on their own terms. After authenticating their identities and obtaining an Experian credit report, users will receive ongoing education about how credit works and recommendations to further build their credit history. To learn more about building profitable customer relationships with credit education, check out our credit education solutions and watch our Three Ways to Uncover Financial Growth Opportunities that Benefit Underserved Communities webinar. Learn more Watch webinar

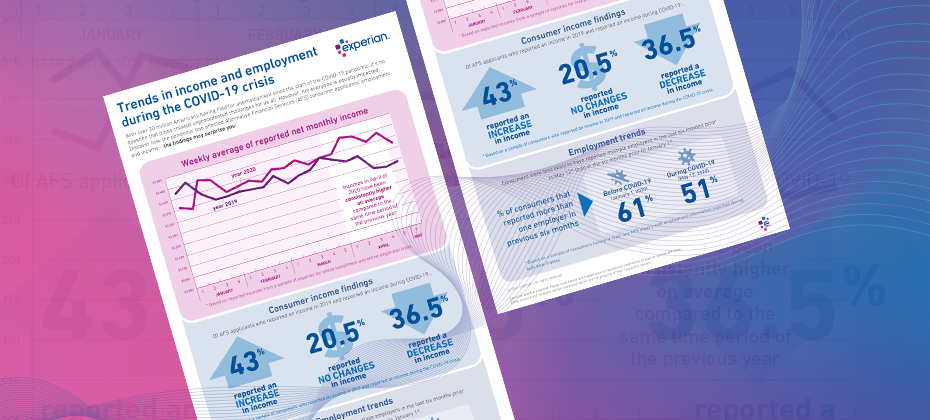

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

Originally posted by Experian Global News blog At Experian, we have an unwavering commitment to helping consumers and clients manage through this unprecedented period. We are actively working with consumers, lenders, lawmakers and regulators to help mitigate the potential impact on credit scores during times of financial hardship. In response to the urgent and rapid changes associated with COVID-19, we are accelerating and enhancing our financial education programming to help consumers maintain good credit and gain access to the financial services they need. This is in addition to processes and tools the industry has in place to help lenders accommodate situations where consumers are affected by circumstances beyond their control. These processes will be extended to those experiencing financial hardship as a result of COVID-19. As the Consumer’s Credit Bureau, our commitment at Experian is to inform, guide and protect our consumers and customers during uncertain times. With expected delays in bill payments, unprecedented layoffs, hiring freezes and related hardships, we are here to help consumers in understanding how the credit reporting system and personal finance overall will move forward in this landscape. One way we’re doing this is inviting everyone to join our special eight-week series of #CreditChat conversations surrounding COVID-19 on Wednesdays at 3 p.m. ET on Twitter. Our weekly #CreditChat program started in 2012 to help the community learn about credit and important personal finance topics (e.g. saving money, paying down debt, improving credit scores). The next several #CreditChats will be dedicated to discussing ways to manage finances and credit during the pandemic. Topics of these #CreditChats will include methods and strategies for bill repayment, paying down debt, emergency financial assistance and preparing for retirement during COVID-19. “As the consumer’s credit bureau, we are committed to working with consumers, lenders and the financial community during and following the impacts of COVID-19,” says Craig Boundy, Chief Executive Officer of Experian North America. “As part of our nation’s new reality, we are planning for options to help mitigate the potential impact on credit scores due to financial hardships seen nationwide. Our #CreditChat series and supporting resources serve as one of several informational touchpoints with consumers moving forward.” Being fully committed to helping consumers and lenders during this unprecedented period, we’ve created a dedicated blog page, “COVID-19 and Your Credit Report,” with ongoing and updated information on how COVID-19 may impact consumers’ creditworthiness and – ultimately – what people should do to preserve it. The blog will be updated with relevant news as we announce new solutions and tactics. Additionally, our “Ask Experian” blog invites consumers to explore immediate and evolving resources on our COVID-19 Updates page. In addition to this guidance, and with consumer confidence in the economy expected to decline, we will be listening closely to the expert voices in our Consumer Council, a group of leaders from organizations committed to helping consumers on their financial journey. We established a Consumer Council in 2009 to strengthen our relationships and to initiate a dialogue among Experian and consumer advocacy groups, industry experts, academics and other key stakeholders. This is in addition to ongoing collaboration with our regulators. Additionally, our Experian Education Ambassador program enables hundreds of employee volunteers to serve as ambassadors sharing helpful information with consumers, community groups and others. The goal is to help the communities we serve across North America, providing the knowledge consumers need to better manage their credit, protect themselves from fraud and identity theft and lead more successful, financially healthy lives. COVID-19 has impacted all industries and individuals from all walks of life. We want our community to know we are right there with you. Learn more about our weekly #CreditChat and upcoming schedule here. Learn more

Fintech is quickly changing. The word itself is synonymous with constant innovation, agile technology structures and being on the cusp of the future of finance. The rapid rate at which fintech challengers are becoming established, is in turn, allowing for greater consumer awareness and adoption of fintech platforms. It would be easy to assume that fintech adoption is predominately driven by millennials. However, according to a recent market trend analysis by Experian, adoption is happening across multiple generational segments. That said, it’s important to note the generational segments that represent the largest adoption rates and growth opportunities for fintechs. Here are a few key stats: Members of Gen Y (between 24-37 years old) account for 34.9% of all fintech personal loans, compared to just 24.9% for traditional financial institutions. A similar trend is seen for Gen Z (between 18-23 years old). This group accounts for 5% of all fintech personal loans as compared to 3.1% for traditional Let’s take a closer look at these generational segments… Gen Y represents approximately 19% of the U.S. population. These consumers, often referred to as “millennials,” can be described as digital-centric, raised on the web and luxury shoppers. In total, millennials spend about $600 billion a year. This group has shown a strong desire to improve their credit standing and are continuously increasing their credit utilization. Gen Z represents approximately 26% of the U.S. population. These consumers can be described as digital centric, raised on the social web and frugal. The Gen Z credit universe is growing, presenting a large opportunity to lenders, as the youngest Gen Zers become credit eligible and the oldest start to enter homeownership. What about the underbanked as a fintech opportunity? The CFPB estimates that up to 45 million people, or 24.2 million households, are “thin-filed” or underbanked, meaning they manage their finances through cash transactions and not through financial services such as checking and savings accounts, credit cards or loans. According to Angela Strange, a general partner at Andreessen Horowitz, traditional financial institutions have done a poor job at serving underbanked consumers affordable products. This has, in turn, created a trillion-dollar market opportunity for fintechs offering low-cost, high-tech financial services. Why does all this matter? Fintechs have a unique opportunity to engage, nurture and grow these market segments early on. As the fintech marketplace heats up and the overall economy begins to soften, diversifying revenue streams, building loyalty and tapping into new markets is a strategic move. But what are the best practices for fintechs looking to build trust, engage and retain these unique consumer groups? Join us for a live webinar on November 12 at 10:00 a.m. PST to hear Experian experts discuss financial inclusion trends shaping the fintech industry and tactical tips to create, convert and extend the value of your ideal customers. Register now

It's been over 10 years since the start of the Great Recession. However, its widespread effects are still felt today. While the country has rebounded in many ways, its economic damage continues to influence consumers. Discover the Great Recession’s impact across generations: Americans of all ages have felt the effects of the Great Recession, making it imperative to begin recession proofing and better prepare for the next economic downturn. There are several steps your organization can take to become recession resistant and help your customers overcome personal financial difficulties. Are you ready should the next recession hit? Get started today

Once you have kids, your bank accounts will never be the same. From child care to college, American parents spend, on average, over $233,000 raising a child from birth through age 17. While moms and dads are facing the same pile of bills, they often don’t see eye to eye on financial matters. In lieu of Father’s Day, where spending falls $8 million behind Mother’s Day (sorry dads!), we’re breaking down the different spending habits of each parent: Who pays the bills? With 80% of mothers working full time, the days of traditional gender roles are behind us. As both parents share the task of caring for the children, they also both take on the burden of paying household bills. According to Pew Research, when asked to name their kids’ main financial provider, 45% of parents agreed they split the role equally. Many partners are finding it more logical to evenly contribute to shared joint expenses to avoid fighting over finances. However, others feel costs should be divvied up according to how much each partner makes. What do they splurge on? While most parents agree that they rarely spend money on themselves, splurge items between moms and dads differ. When they do indulge, moms often purchase clothes, meals out and beauty treatments. Dads, on the other hand, are more likely to binge on gadgets and entertainment. According to a recent survey on millennial dads, there’s a strong correlation between the domestic tasks they’re taking on and how they’re spending their money. For instance, most dads are involved in buying their children’s books, toys and electronics, as well as footing the bill for their leisure activities. Who are they more likely to spend on? No parent wants to admit favoritism. However, research from the Journal of Consumer Psychology found that you’re more likely to spend money on your daughter if you’re a woman and more likely to spend on your son if you’re a man. The suggested reasoning behind this is that women can more easily identify with their daughters and men with their sons. Overall, parents today are spending more on their children than previous generations as the cost of having children in the U.S. has exponentially grown. How are they spending? When it comes to money management both moms and dads claim to be the “saver” and label the other as the “spender.” However, according to Experian research, there are financial health gaps between men and women, specifically when it pertains to credit. For example, women have 11% less average debt than men, a higher average VantageScore® credit score and the same revolving debt utilization of 30%. Even with more credit cards, women have fewer overall debts and are managing to pay those debts on time. There’s no definite way to say whether moms are spending “better” than dads, or vice versa. Rather, each parent has their own strengths and weaknesses when it comes to allocating money and managing expenses.

Pay your bills on time, have cash set aside for emergencies, and invest your money for the future. These are the rules financial pros say people should follow if they want to build wealth. Straightforward advice, but for many people these milestones can seem out of reach. A recent financial literacy study by Mintel shows that many Americans are struggling with money management and lack confidence in their financial knowledge, with just 19 percent of respondents giving themselves an “A” grade on financial knowledge. The survey and other reports released recently shed light on how well Americans are handling their money. Here are some of the prevailing trends: Young people are struggling. The Mintel study revealed less than 30 percent of Americans have an emergency savings account that equals 3-6 months of household income. Of that total number, 19 percent of iGeneration has saved for a rainy day, followed by Millennials (20 percent), Gen Xers (28 percent), Baby Boomers (37 percent) and World War II/Swing Generation (40 percent). Not surprisingly, people who make more money save a bigger percentage of their pay. People in the bottom 90 percent of the income scale save close to none of their pay each year, while those in the top 10 percent save close to 15 percent. Most are not planning for the future. The majority of people are not doing everything they can to prepare for retirement, including meeting with a financial adviser to devise a plan, researching Social Security or even talking to friends or family about planning. Even more, 21 percent of Americans are “not at all confident” they will be able to reach their financial goals. Parents plan more than non-parents. People with children have many demands on their money, and as a result think ahead and follow budgets, contribute to retirement accounts and hire a financial adviser to help them create plans and budgets. Consumers who don’t have children don’t have as many competing demands, but aren’t as sensible about following a financial plan. In Mintel’s study, just 10 percent of non-parents have a written financial plan and 26 percent contribute regularly to a retirement account. Most people have a budget. Nearly one in three Americans prepare a detailed written or computerized household budget each month that tracks their income and expenses, but a large majority do not. Those with at least some college education, conservatives, Republicans, independents, and those making $75,000 a year or more are slightly more likely to prepare a detailed household budget than are their counterparts, according to Gallup. The good news is, the majority of Americans are open to more financial education. April—which is Financial Literacy Month—is a great time to look at education efforts for your customers. Financial literacy won’t change overnight, nor in a year. Yet initiatives taken in schools, workplaces, and in communities add up. What are you doing for your customers to build financial literacy?

Good job, check. Shared interests, check. Chemistry, check. He seems like a perfect 10. Both of you enjoy your first date and while getting ready for the second, you dare to imagine that turning into another and another, and possibly happily ever after. Then one decidedly unromantic question comes to mind: What is his credit score? Reviewing a potential partner’s credit score and report is important to many singles who are looking for lasting love. According to Bankrate.com, 42 percent of Millennials said that knowing someone’s credit score would affect their desire to date them, slightly more than 40 percent of Gen Xers and 41 percent of Baby Boomers. They may be on to something. Research shows that knowing someone’s credit history and sense of financial responsibility could save people time – and potential heartache. A UCLA study about money and love shows a very strong link between high credit scores and long-lasting relationships. People with drastically different credit scores may experience more financial stress down the road, placing a burden on a relationship. An Experian report reveals 60 percent of people believe it’s important for their future spouse to have a good credit score, and 25 percent of people from the UCLA study were willing to leave a partner with poor credit before marriage so they aren’t held back. While that three-digit number doesn't tell a person’s whole financial story, it can reveal financial habits that could impact your life. Banks are wary of making loans to borrowers with tarnished scores, typically 660 and below. A low score could quash dreams of buying a home, and result in steep interest rates, up to 29 percent, for credit cards, car financing and other unsecured loans. A mid-range credit score can also hurt an application for an apartment and drive up the cost of mobile phone plans and auto insurance. Eight states have passed laws limiting employers’ ability to use credit checks when assessing job candidates, yet 13 percent of employers surveyed by the Society of Human Resource Management performed credit checks on all job applicants. Talking spending styles and revealing credit scores sooner rather than later in a relationship isn’t necessarily comfortable. But it may help you decide whether you have compatible financial outlooks and practices.