Tag: creditworthiness

This article was updated on February 13, 2024. Traditional credit data has long been a reliable source for measuring consumers' creditworthiness. While that's not changing, new types of alternative credit data are giving lenders a more complete picture of consumers' financial health. With supplemental data, lenders can better serve a wider variety of consumers and increase financial access and opportunities in their communities. What is alternative credit data? Alternative credit data, also known as expanded FCRA-regulated data, is data that can help you evaluate creditworthiness but isn't included in traditional credit reports.1 To comply with the Fair Credit Reporting Act (FCRA), alternative credit data must be displayable, disputable and correctable. Lenders are increasingly turning to new types and sources of data as the use of alternative credit data becomes the norm in underwriting. Today, lenders commonly use one or more of the following: Alternative financial services data: Alternative financial services (AFS) credit data can include information on consumers' use of small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Consumer permission data: With a consumer's permission, you can get transactional and account-level data from financial accounts to better assess income, assets and cash flow. The access can also give insight into payment history on non-traditional accounts, such as utilities, cell phone and streaming services. Rental payment history: Property managers, electronic rent payment services and rent collection companies can share information on consumers' rent payment history and lease terms. Full-file public records: Local- and state-level public records can tell you about a consumer's professional and occupational licenses, education, property deeds and address history. Buy Now Pay Later (BNPL) data: BNPL tradeline and account data can show you payment and return histories, along with upcoming scheduled payments. It may become even more important as consumers increasingly use this new type of point-of-sale financing. By gathering more information, you can get a deeper understanding of consumers' creditworthiness and expand your lending universe. From market segmentation to fraud prevention and collections, you can also use alternative credit data throughout the customer lifecycle. READ: 2023 State of Alternative Credit Data Report Challenges in underwriting today While unemployment rates are down, high inflation, rising interest rates and uncertainty about the economy are impacting consumer sentiment and the lending environment.2 Additionally, lenders may need to shift their underwriting approaches as pandemic-related assistance programs and loan accommodations end. Lenders may want to tighten their credit criteria. But, at the same time, consumers are becoming accustomed to streamlined application processes and responses. A slow manual review could lead to losing customers. Alternative credit data can help you more accurately assess consumers' creditworthiness, which may make it easier to identify high-risk applicants and find the hidden gems within medium-risk segments. Layering traditional and alternative credit data with the latest approaches to model building, such as using artificial intelligence, can also help you implement precise and predictive underwriting strategies. Benefits of using alternative data for credit underwriting Using alternative data for credit underwriting — along with custom credit attributes and automation — is the modern approach to a risk-based credit approval strategy. The result can offer: A greater view of consumer creditworthiness: Personal cash flow data and a consumer's history of making (or missing) payments that don't appear on traditional credit reports can give you a better understanding of their financial position. Improve speed and accuracy of credit decisions: The expanded view helps you create a more efficient underwriting process. Automated underwriting tools can incorporate alternative credit data and attributes with meaningful results. One lender, Atlas Credit, worked with Experian to create a custom model that incorporated alternative credit data and nearly doubled its approvals while reducing risk by 15 to 20 percent.3 Increase financial inclusion: There are 28 million American adults who don't have a mainstream credit file and 21 million who aren't scoreable by conventional scoring models.4 With alternative credit data, you may be able to more accurately assess the creditworthiness of adults who would otherwise be deemed thin file or unscorable. Broadening your pool of applications while appropriately managing risk is a measurable success. What Experian builds and offers Experian is continually expanding access to expanded FCRA-regulated data. Our Experian RentBureau and Clarity Services (the leading source of alternative financial credit data) have long given lenders a more complete picture of consumers' financial situation. Experian also helps lenders effectively use these new types of data. You can also incorporate the data into your proprietary marketing, lending and collections strategies. Experian is also using alternative credit data for credit scoring. The Lift Premium™ model can score 96 percent of U.S. adults — compared to the 81 percent that conventional models can score using traditional data.5 The bottom line Lenders have been testing and using alternative credit data for years, but its use in underwriting may become even more important as they need to respond to changing consumer expectations and economic uncertainty. Experian is supporting this innovation by expanding access to alternative data sources and helping lenders understand how to best use and implement alternative credit data in their lending strategies. Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply and can be used interchangeably. 2Experian (2024). State of the Economy Report 3Experian (2020). OneAZ Credit Union [Case Study] 4Oliver Wyman (2022). Financial Inclusion and Access to Credit [White Paper] 5Ibid.

Conventional credit scoring systems are based on models developed over six decades. As consumer behavior evolves, it's important to seek newer, fresher sources of data to assess creditworthiness. Because the data used by conventional credit scoring models does not provide the full picture of a consumer's financial health, a large population segment of the United States is excluded from accessing credit.With changing times and new technology, forward-thinking financial institutions are using alternative data1 to gain a more holistic consumer view. A move toward inclusive finance, including incorporating alternative data in credit scoring models, is a crucial step towards promoting financial inclusion and helping millions of consumers achieve their financial and personal goals. More importantly, it provides the insight needed for lender confidence, which can help fuel business growth. Understanding limitations of the conventional scoring system Credit scores can be obtained from any one of the major credit bureaus based on information found in a consumer's credit report and are incorporated into a lender's credit-decisioning process. While there are various credit scoring models based on lender preference that could yield slightly different scores, all traditional scores are comprised of credit characteristics within these categories: payment history, credit mix, credit history length, amounts owed and new credit account inquires. Lenders use past credit performance to predict whether extending credit is a risk, posing a major challenge for credit invisible and thin-file consumers and leaving millions at a disadvantage. This dilemma also limits business growth for lenders. Consumers who are unable to access mainstream credit often turn to the alternative financial services (AFS) industry, a $140 billion market that continues to grow by 7-10 percent each year.2 The AFS industry offers consumers additional products, like payday loans, cash advances, short-term installment loans, and rent-to-own loans, none of which are included in a traditional credit file. With alternative credit data, lenders can obtain a more holistic view of creditworthiness and risk, helping to enhance inclusive lending by broadening their pool of potential loan candidates. Why conventional scoring models simply aren't enough Because of the criteria used to assess creditworthiness, conventional credit scoring models do not accurately capture an individual's financial behavior or health. Indeed, many people demonstrate financial responsibility in other legitimate ways that are not reported to the major credit bureaus.In contrast, non-traditional data considers a consumer's everyday financial behavior to provide a more accurate score for lenders. It can include a range of indicators, such as: Bill payments: Consistent payment history on typical household bills (which may have been paid from a debit account). Bank account data: Shows average balance and withdrawal activity and recurring payroll deposits (indicating that a consumer is employed and receives a regular income). Rental data: Indicates a consumer's long-term stability in making regular, on-time monthly rent payments. Registered licenses: Registered licenses or membership with a skilled trade or profession can indicate the likelihood to generate income. Including this type of data can benefit both lenders and applicants. According to an Experian report, by adding alternative credit data to a near-prime population, lenders could see an increase in approvals for consumers historically being left behind. When Clear Early Risk Score™ is paired with the VantageScore® credit score, approvals climb to 16 percent of the population inside the same risk criteria, representing a 60 percent lift in credit approvals for near-prime consumers.2 The pool of people from whom this type of alternative data can reliably be collected is growing, with 70 percent of consumers willing to provide additional financial information to a lender if it increases their chance for approval or improves their interest rate for a mortgage or car loan.3 Plenty of available yet untapped data exists that can add value to a consumer's profile and lead to greater inclusive lending. For example, 95 percent of Americans own a cell phone and about two-thirds of households headed by young adults are being rented. Reporting on this data could potentially "thicken" a credit file and provide deeper insight into a consumer's credit behavior.3Indeed, turning to non-traditional data can expand the credit universe and lead to more inclusive credit scoring models, especially by leveraging existing technology and financial inclusion solutions. Research shows that with Lift Premium™, virtually all of the 21 million conventionally unscorable consumers would become scoreable, and over 1 million of them would have scores in the near-prime range or better. Of these, 1.7 million would be Black American and Hispanic/Latino people.3 For lenders, these numbers reveal potential opportunities to grow their businesses. Of the 255 million adults in the U.S., 19 percent of credit eligible adults are left out of mainstream scoring systems. 28 million are considered credit invisible – meaning they have no credit history (11%). 21 million are considered unscorable – have partial credit history but not enough to generate a score using conventional models (8%). Of the remaining credit eligible adults, 57 million were considered subprime (22%). 106 million U.S. adults can't get mainstream credit rates (42%). Adopting inclusive finance lending practices is not only the right thing to do but also provides financial institutions with the chance to reach untapped markets, grow their business and promote a healthier economy. Financial inclusion is not a destination, but an ever-evolving journey. Don't miss out on this critical opportunity to join the movement. Learn more about our financial inclusion tools to help enhance your inclusive lending approach. 1"Alternative Credit Data,” refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.2Experian: 2020 State of Alternative Credit Data.3Oliver Wyman white paper, “Financial Inclusion and Access to Credit," January 12, 2022.

Today's top lenders use traditional and alternative credit data1 – or expanded Fair Credit Reporting Act (FCRA) regulated data – including consumer permissioned data, to enhance their credit decisioning. The ability to gain a more complete and timely understanding of consumers' financial situation allows lenders to better gauge creditworthiness, make faster decisions and grow their portfolios without taking on additional risk. Why lenders need to go beyond traditional credit data Traditional credit data is — and will remain — important to understanding the likelihood that a borrower will repay a loan as agreed. However, lenders who solely base credit decisions on traditional credit data and scores may overlook creditworthy consumers who don't qualify for a credit score — sometimes called unscorable or credit invisible consumers. Additionally, they may be spending time and money on manual reviews for applications that are low risk and should be automatically approved. Or extending offers that aren't a good fit. What is consumer permissioned data? Consumer permissioned data, or user permissioned data, includes transactional and account-level data, often from a bank, credit union or brokerage account, that a consumer gives permission to view and use in credit decisioning. To access the data, lenders create secure connections to financial institutions or data aggregators. The process and approach give consumers the power to authorize (and later retract) access to accounts of their choosing — putting them in control of their personal information — while setting up security measures that keep their information secure. In return for sharing access to their account information, consumers may qualify for more financial products and better terms on credit offers. What does consumer permissioned data include? Consumers can choose to share different types of information with lenders, including their account balances and transaction history. While there may be other sources for estimated or historic account-level data, permissioned data can be updated in real-time to give lenders the most accurate and timely view of a consumer's finances. There is also a wealth of information available within these transaction records. For example, consumers can use Experian Boost™ to get credit for non-traditional bills, including phone, utility, rent and streaming service payments. These bills generally don't appear in traditional credit reports and don't impact every type of credit score. But seeing a consumer's history of making these payments can be important for understanding their overall creditworthiness. What are the benefits of leveraging consumer permissioned data? You can incorporate consumer permissioned data into custom lending models, including the latest explainable machine learning models. As part of a loan origination system, the data can help with: Portfolio expansion Accessing and using new data can expand your lending universe in several ways. There are an estimated 28 million U.S. adults who don't have a credit file at the bureaus, and an additional 21 million who have a credit file but lack enough information to be scorable by conventional scoring models. These people aren't necessarily a credit risk — they're simply an unknown. Increased insights can help you understand the real risk and make an informed decision. Additionally, a deeper insight into consumers' creditworthiness allows you to swap in applications that are a good credit risk. In other words, approving applications that you wouldn't have been able to approve with an older credit decision process. Increase financial inclusion Many credit invisibles and thin-file applicants also fall into historically marginalized groups.2 Almost a third of adults in low-income neighborhoods are credit invisible.3 Black Americans are much more likely (1.8 times) to be credit invisible or unscorable than white Americans.4 Recent immigrants may have trouble accessing credit in the U.S., even if they had a good credit history in their home country.5 As a result, using consumer permissioned data to expand your portfolio can align with your financial inclusion efforts. It's one example of how financial inclusion is good for business and society. Enhance decisioning and minimize risk Consumer-permissioned data can also improve and expand automated decisions, which can be important throughout the entire loan underwriting journey. In particular, you may be able to: Verify income faster: By linking to consumers’ accounts and reviewing deposits, lenders can quickly verify their income and ability to pay. Make better decisions: Consumer permissioned data also give lenders a new lens for understanding an applicant’s credit risk, which can let you say yes more often without taking on additional risk. Process more applications: A better understanding of applicants’ credit risk can also decrease how many applications you send to manual review, which allows you to process more applications using the same resources. Increase customer satisfaction: Put it all together, and faster decisions and more approvals lead to happier customers. While consumer permissioned data can play a role in all of these, it's not the only type of alternative data that lenders use to grow their portfolios. What are other types of alternative data sources? In addition to consumer permissioned data, alternative credit data can include information from: Alternative financial services: Credit data from alternative financial services firms includes information on small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Rental agreement: Rent payment data from landlords, property managers, collection companies and rent payment services. Public records: Full-file public records go beyond what’s in a consumer’s credit report and can include professional and occupational licenses, property deeds and address history. Why partner with Experian? As an industry leader in consumer credit and data analytics, Experian is continuously building on its legacy in the credit space to help lenders access and use various types of alternative data. Along with Experian Boost™ for consumer permissioned data, Experian RentBureau and Clarity Services are trusted sources of alternative data that comply with the FCRA. Experian also offers services for lenders that want help understanding and using the data for marketing, lending and collections. For originations, the Lift Premium™ credit model can use alternative credit data to score over 65% of traditionally credit-invisible consumers. Expand your lending universe Lenders are turning to new data sources to expand their portfolios and remain competitive. The results can provide a win-win, as lenders can increase approvals and decrease application processing times without taking on more risk. At the same time, these new strategies are helping financial inclusion efforts and allowing more people to access the credit they need. Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.2-5Oliver Wyman (2022). Driving Growth With Greater Credit Access

More than seven million Americans who are unbanked cite high account fees, insufficient funds to meet minimum balances and a lack of needed products and services as the main reasons for not having a checking or savings account.1 Credit unions understand that being unbanked comes at a steep cost and have turned their focus to developing products and strategies that prioritize financial inclusion — a movement to combat inequities in banking and better serve the financial needs of marginalized communities. In 2022, the House passed Expanding Financial Access for Underserved Communities Act to allow federal credit unions to add underserved areas to their fields of membership as a means of improving financial inclusion. “We believe diversity, inclusion, equity, belonging and accessibility has to be weaved into the strategic fabric of an organization [and its] culture," says Max Villaronga, President and Chief Executive Officer of Raiz Federal Credit Union. “When we don't participate in [diversity, equity and inclusion], we are complicit in essentially keeping people out of the banking system." For credit unions, driving financial inclusion starts with setting a vision that will leave a lasting legacy that includes fostering financial empowerment, closing the credit gap and building generational wealth among the communities they serve. Here's a roadmap for getting started. Best practices for engagement Establishing a set of best practices is the essential starting point for improving financial inclusion. The process begins with the mission statement and extends to all aspects of operations from hiring procedures to sponsorships and donations. Villaronga advocates three strategies for engagement: Engage the leadership team Conversations about financial inclusion need to start at the top. The C-suite must be willing to be honest about the barriers and willing to adopt changes that will make credit unions more inclusive. “[T]hese systemic barriers will exist until somebody deliberately moves them out of the way," Villaronga says. “The people who are feeling those barriers are not in the position to do the moving it's up to [CEOs and CFOs] to decide to do something to make a difference." Making a difference starts with choosing a leadership team that reflects the demographics of local communities. Case in point: At Raiz Federal Credit Union in El Paso, Texas, senior management and the board have LGBTQIA+ representation and include members from diverse racial and ethnic identities. The board of directors has also prioritized creating a pipeline that will attract more diverse talent to the board. “Many of [our board members] come from underserved backgrounds in our border community," Villaronga says. “This is a very personal journey for them because they can see themselves in the lives of the people we're serving." Build trust in underserved communities According to an FDIC Survey, “unbanked" U.S. households listed a lack of trust in financial institutions as a top reason for not having a bank account. And lack of access to a checking or savings account is most prominent among racial and ethnic minorities and low-income communities.2 Actions speak louder than words, according to Villaronga. Raiz Federal Credit Union uses diverse images in its advertising and provides information in both English and Spanish. The credit union was also awarded the Juntos Avanzamos (Together We Advance) designation from Inclusiv for its commitment to serving and empowering Hispanic communities by providing safe, affordable and relevant financial services. Villaronga believes that a designation like Juntos Avanzamos sends the message to the community that the credit union is committed to improving general financial literacy and pre-loan education, as well as reducing higher charge-offs and other barriers to accessing financial services that exist in lending and serving underserved communities. Dispel financial inclusion myths Among traditional financial institutions, myths about financial inclusion are widespread and include falsehoods that pricing products for marginalized communities are too challenging, reaching out is not profitable, and providing financial products to underserved markets is too risky. “Credit unions were really built to extend credit [and] were also originally established to serve consumers that were being ignored by the existing systems that were in place but those consumers are still being ignored today," Villaronga says. “Are those communities too risky to serve? Some companies are serving them [and] they would not be doing so if it was not profitable." Raiz Federal Credit Union offers several affordable loan products — from credit builder loans to citizenship loans and payday lender payoff loans along with credit cards — that allow members to build their credit scores and establish positive credit histories. Rather than pricing loans based on what the competition is charging, Villaronga calculates the fixed and variable costs, failure fraction and target return on assets to get a floor pricing per unit. The approach, he adds, allowed Raiz Federal Credit Union to report earnings of over 150 basis points in 2021 while maintaining a 12 percent capital ratio, proving that financial inclusion is good for the bottom line. “THE IDEA THAT YOU CANNOT [ACHIEVE FINANCIAL INCLUSION] IN A WAY THAT'S SAFE AND SOUND AND SATISFIES THE [NATIONAL CREDIT UNION ADMINISTRATION] IS TRULY A MYTH." - Max Villaronga, President and CEO, Raiz Federal Credit Union Partner for Success For credit unions, an important part of achieving financial inclusion goals is identifying partners that can help. Raiz Federal Credit Union set a goal to increase automated lending from 20 percent to 60 percent, but using a traditional loan origination program was insufficient to hit that target. A partnership with Experian allowed the credit union to access tools that allowed it to better identify non-traditional risks and opportunities, as well as develop more robust lending and optimized decision strategies. Experian launched Inclusion ForwardTM, an initiative to help boost financial inclusion and close the wealth gap, and support financial institutions by enhancing their inclusion approach by leveraging FCRA-regulated data sources (otherwise known as alternative data).3 In addition to providing a deeper view of unbanked and underbanked consumers and reducing friction and speed of decisioning through increased automation, Experian Lift PremiumTM uses income and employer data, social security and financial management insights — transaction behaviors that were historically credit invisible or unscorable — to help credit unions meet the needs of underserved markets and increase opportunities for inclusion. “This automation also allows us to reduce our fixed cost per unit — [and] it's a really big deal because this is not by little, but a lot," Villaronga says. “This lower cost to produce [a loan] allows us to improve our interest rates to underserved members, further creating an appealing value proposition that's in line with our financial inclusion strategy." Access our case study to learn more about how Experian can help grow your business with a frictionless digital prequalification experience. Access now 1Federal Reserve Bank of Cleveland (May 2022). Unbanked in America: A Review of Literature 2 Federal Deposit Insurance Corporation (December 2021). American Banks: Household use of Banking and Financial Services 3When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably

With consumers having more credit options than ever before, it’s imperative for lenders to get their message in front of ideal customers at the right time and place. But without clear insights into their interests, credit behaviors or financial capacity, you may risk extending preapproved credit offers to individuals who are unqualified or have already committed to another lender. To increase response rates and reduce wasted marketing spend, you must develop an effective customer targeting strategy. What makes an effective customer targeting strategy? A customer targeting strategy is only as good as the data that informs it. To create a strategy that’s truly effective, you’ll need data that’s relevant, regularly updated, and comprehensive. Alternative data and credit-based attributes allow you to identify financially stressed consumers by providing insight into their ability to pay, whether their debt or spending has increased, and their propensity to transfer balances and consolidate loans. With a more granular view of consumers’ credit behaviors over time, you can avoid high-risk accounts and focus only on targeting individuals that meet your credit criteria. While leveraging additional data sources can help you better identify creditworthy consumers, how can you improve the chances of them converting? At the end of the day, it’s also the consumer that’s making the decision to engage, and if you aren’t sending the right offer at the precise moment of interest, you may lose high-value prospects to competitors who will. To effectively target consumers who are most likely to respond to your credit offers, you must take a customer-centric approach by learning about where they’ve been, what their goals are, and how to best cater to their needs and interests. Some types of data that can help make your targeting strategy more customer-centric include: Demographic data like age, gender, occupation and marital status, give you an idea of who your customers are as individuals, allowing you to enhance your segmentation strategies. Lifestyle and interest data allow you to create more personalized credit offers by providing insight into your consumers’ hobbies and pastimes. Life event data, such as new homeowners or new parents, helps you connect with consumers who have experienced a major life event and may be receptive to event-based marketing campaigns during these milestones. Channel preference data enables you to reach consumers with the right message at the right time on their preferred channel. Target high-potential, high-value prospects By using an effective customer targeting strategy, you can identify and engage creditworthy consumers with the greatest propensity to accept your credit offer. To see if your current strategy has what it takes and what Experian can do to help, view this interactive checklist or visit us today. Review your customer targeting strategy Visit us

Even before the COVID-19 pandemic, many Americans lacked equal access to financial products and services — from tapping into affordable banking services to credit cards to financing a home purchase. The global pandemic likely exacerbated those existing issues and inequalities. That reality makes financial inclusion — a concerted effort to make financial products and services affordable and accessible to all consumers — more crucial than ever. The playing field wasn't level before the pandemic The Federal Reserve reported that in 2019, Black and Hispanic/Latino families had median wealth that was just 13 to 19 percent of that of White families — $24,100 and $36,100, respectively, compared to $188,200 for White families. That inequity is also reflected in credit score disparities. While credit scores, income, and wealth aren't synonymous, the traditional credit scoring system leads marginalized communities to be disproportionately labeled unscoreable or credit invisible, and face challenges in accessing credit. New research from Experian shows that in over 200 cities, there can be more than a 100-point difference in credit scores between neighborhoods — often within just a few miles from each other. Marginalized communities bore the financial brunt Minority communities were also disproportionately impacted by COVID-19 in terms of infections, job losses, and financial hardship. In mid-2020, the Economic Policy Institute (EPI) reported Black and Hispanic/Latino workers were more likely than White workers to have lost their jobs or to be classified as essential workers — leading to economic or health insecurity. Government initiatives — including the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the Paycheck Protection Program (PPP) and the American Rescue Plan — created expanded unemployment benefits, paused loan payments, eviction moratoriums, and direct cash payments. These helped consumers' immediate financial well-being. The National Bureau of Economic Research found that, on average, U.S. households spent approximately 40 percent of their first two stimulus checks, with about 30 percent used for savings and another 30 percent used to pay down debt. In some communities highly affected by COVID-19, consumers were able to pay down nearly 40 percent of their credit card balances and close more than 9 percent of their bank card accounts, according to recent data. Stimulus payments have been credited with reducing childhood poverty and helping families save for financial emergencies. That being said, people on the upper end of the income scale were able to improve their financial situation even more. Their wealth grew at a much faster pace than people at the bottom end of the income distribution scale, according to data from the Federal Reserve. How the pandemic deepened financial exclusion Although hiring has picked up in low-wage industries, research indicates that low-wage jobs have been the slowest to return. According to a survey by the Pew Research Center, among respondents who said their financial situation worsened during the pandemic, 44 percent believe it will take three years or more to get back to where they were a year ago. About 10 percent don't think their finances will ever recover. Recent Experian data shows that consumers in certain communities that were already struggling to pay their debts fell into an even bigger hole. These consumers missed payments on 56 percent more accounts in the period between spring 2019 to spring 2020 compared to the year prior. Credit scores in these neighborhoods fell by an average of over 20 points during the first 18 months of COVID-19. That being said, U.S. consumers overall increased their median credit scores by an average of 21 points from the end of 2019 to the end of 2021. When consumers with deteriorating credit encounter financial stresses, often their only recourse is to pile on additional debt. Even worse, those who can't access traditional credit often turn to alternative credit arrangements, such as short-term loans, which may charge significantly higher interest rates. READ MORE: More Than a Score: The Case for Financial Inclusion What can the financial sector do? Without access to affordable financial services and products, subprime or credit invisible consumers may not get approved for a mortgage or car loan — things that might come much easier for consumers with better scores. This is just one reason why financial inclusion is so important — and why financial services companies have a big role to play in driving it. One place to start is by taking a broader view of what makes a creditworthy consumer. In addition to traditional credit scoring models, new tools can leverage artificial intelligence and machine learning, along with alternative data, to analyze the creditworthiness of consumers. By qualifying for credit, more consumers can access affordable mortgages, car loans, business loans and insurance - freeing up money for other expenses and allowing them to grow their wealth.. READ MORE: What Is Alternative and Non-Traditional Data? Last word Marginalized communities were already struggling economically before the pandemic, and the impact of COVID-19 has made the wealth disparities worse. With the pandemic waning, now is the time for financial institutions to take action on financial inclusion. Not only does it help improve your customers' lives and make them better prepared for the next crisis, but it also fuels your business's growth and bottom line.

There's no magic solution to undoing the decades of policies and prejudices that have kept certain communities unable to fully access our financial and credit systems. But you can take steps to address previous wrongs, increase financial inclusion and help underserved communities. If you want to engage consumers and keep them engaged, you could start with the following four areas of focus. 1. Find ways to build trust Historical practices and continued discriminatory behavior have created justifiable distrust of financial institutions among some consumers. In February 2022, Experian surveyed more than 1,000 consumers to better understand the needs and barriers of underserved communities. The respondents came from varying incomes, ethnicity and age ranges. Fewer than half of all the consumers (47 percent) said they trusted their bank's personal finance advice and information, and that dropped to 41 percent among Black Americans. In a follow-up webinar discussion of financial growth opportunities that benefitted underserved communities, we found that many financial institutions saw a connection between their financial inclusion efforts and building trust with customers and communities. Here is a sample question and a breakdown of the primary responses: What do you think is the greatest business advantage of executing financial inclusion in your financial institution or business?1 Building trust and retention with customers and communities (78%) Increasing revenue by expanding to new markets (6%) Enhancing our brand and commitment to DEI (14%) Staying in alignment with regulator and compliance guidelines (2%) Organizations may want to approach financial inclusion in different ways depending on their unique histories and communities. But setting quantifiable goals and creating a roadmap for your efforts is a good place to start. 2. Highlight data privacy and mobile access If you want to win over new customers, you'll need to address their most pressing needs and desires. Consumers' top four considerations when signing up for a new account were consistent, but the specific results varied by race. Keep this in mind as you consider messaging around the security and privacy measures. Also, consider how underserved communities might access your online services. Having an accessible and intuitive mobile app or mobile-friendly website is important and likely carries even more weight with these groups. According to the Pew Research Center, as of 2021, around a quarter of Hispanic/Latino and 17% of Black Americans are smartphone-dependent — meaning they have a smartphone but don't have broadband access at home. Low-income and minority communities are also less likely to live near bank branches or ATMs. 3. Offer lower rates and fees Low rates and fees are also a top priority across the board — everyone likes to save money. However, fewer Black and Hispanic households have $1,000 in savings or more compared to white households, which could make additional savings opportunities especially important. There have been several recent examples of large banks and credit unions eliminating overdraft fees. And the Bank On National Account Standards can be a helpful framework if you offer demand deposit accounts. Lowering interest rates on credit products can be more challenging, particularly when consumers don't have a thick (or any) credit file. But by integrating expanded FCRA-regulated data sources and new scoring models, such as Experian's Lift PremiumTM, creditors can score more applicants and potentially offer them more favorable terms. 4. Leverage credit education tools and messaging For consumers who've had negative credit experiences, are new to credit, or are recent immigrants with little understanding of the U.S. credit system, building and using credit can feel daunting. About 80% of women have little or no confidence in getting approved for credit or worry that applying could hurt them further. Only 20% of consumers who make less than $35,000 a year say they're "extremely" or "very" confident they'll be approved for credit. While most consumers haven't used credit education tools before, they're willing to try. More than 60 percent of Black and Hispanic respondents said they're likely to sign up for free credit education tools and resources from their banks. Offering these tools could be an opportunity to strengthen trust and help consumers build credit, which can also make it easier for them to qualify for financial products and services in the future. Moving forward with financial inclusion Broadening access to credit can be an important part of financial inclusion, and financial institutions can grow by expanding outreach to underserved communities. However, the relationship must be built on trust, security, and offerings that meet these consumers' needs. Through our Inclusion Forward™ initiative, Experian can support your financial inclusion goals — helping you empower underserved communities by helping them grow their financial futures. Learn more about Experian financial inclusion solutions and financial inclusion tools.

These days, the call for financial inclusion is being answered by a disruptive force of new financial products and services. From fintech to storied institutional players, we're seeing a variety of offerings that are increasingly accessible and affordable for consumers. It's a step in the right direction. And beyond the moral imperative, companies that meet the call are finding that financial inclusion can be a source of business growth and a necessity for staying relevant in a competitive marketplace. A diaspora of credit-invisible consumers To start, let's put the problem in context. A 2022 Oliver Wyman report found about 19 percent of the adult population is either credit invisible (has no credit file) or unscoreable (not enough credit information to be scoreable by conventional credit scoring models). But some communities are disproportionately impacted by this reality. Specifically, the report found: Black Americans are 1.8 times more likely to be credit invisible or unscoreable than white Americans. Recent immigrants may have trouble accessing credit in the U.S., even if they're creditworthy in their home country. About 40 percent of credit invisibles are under 25 years old. In low-income neighborhoods, nearly 30 percent of adults are credit invisible and an additional 16 percent are unscoreable. Younger and older Americans alike may shy away from credit products because of negative experiences and distrust of creditors. Similarly, the Federal Deposit Insurance Corporation (FDIC) reports that an estimated 5.4 percent (approximately 7.1 million) households, were unbanked in 2019 — often because they can't meet minimum balance requirements or don't trust banks. Credit invisibles and unscoreables may prefer to deal in a cash economy and turn to alternative credit and banking products, such as payday loans, prepaid cards, and check-cashing services. But these products can perpetuate negative spirals. High fees and interest can create a vicious cycle of spending money to access money, and the products don't help the consumers build credit. In turn, the lack of credit keeps the consumers from utilizing less expensive, mainstream financial products. The emergence of new players Recently, we've seen explosive growth in fintech — technology that aims to improve and automate the delivery and use of financial services. According to market research firm IDC, fintech is expected to achieve a compound annual growth rate (CAGR) of 25 percent through 2022, reaching a market value of $309 billion. It's reaching mass adoption by consumers: Plaid® reports that 88 percent of U.S. consumers use fintech apps or services (up from 58 percent in 2020), and 76 percent of consumers consider the ability to connect bank accounts to apps and services a top priority. Some of these new products and services are aimed at helping consumers get easier and less expensive access to traditional forms of credit. Others are creating alternative options for consumers. Free credit-building tools. Experian Go™ lets credit invisibles quickly and easily establish their credit history. Likewise, consumers can use Experian Boost™ to build their credit with non-traditional payments, including their existing phone, utility and streaming services bills. Alternative credit-building products. Chime® and Varo® , two neobanks, offer credit builder cards that are secured by a bank account that customers can easily add or withdraw money from. Mission Asset Fund, a nonprofit focused on helping immigrants, offers a fee- and interest-free credit builder loan through its lending circle program. Cash-flow underwriting. Credit card issuers and lenders, including Petal and Upstart, are using cash-flow underwriting for their consumer products. Buy now, pay later. Several Buy Now Pay Later (BNPL) providers make it easy for consumers to pay off a purchase over time without a credit check. Behind the scenes, it's easier than ever to access alternative credit data1 — or expanded Fair Credit Reporting Act (FCRA)-regulated data — which includes rental payments, small-dollar loans and consumer-permissioned data. And there are new services that can help turn the raw data into a valuable resource. For example, Lift PremiumTM uses multiple sources of expanded FCRA-regulated data to score 96 percent of American adults — compared to the 81 percent that conventional scoring models can score with traditional credit data. While we dig deeper to help credit invisibles, we're also finding that the insights from previously unreported transactions and behavior can offer a performance lift when applied to near-prime and prime consumers. It truly can be a win-win for consumers and creditors alike. Final word There's still a lot of work to be done to close wealth gaps and create a more inclusive financial system. But it's clear that consumers want to participate in a credit economy and are looking for opportunities to demonstrate their creditworthiness. Businesses that fail to respond to the call for more inclusive tools and practices may find themselves falling behind. Many companies are already using or planning to use alternative data, advanced analytics, machine learning, and AI in their credit-decisioning. Consider how you can similarly use these advancements to help others break out of negative cycles. 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.

From awarding bonus points on food delivery purchases to incorporating social media into their marketing efforts, credit card issuers have leveled up their acquisition strategies to attract and resonate with today’s consumers. But as appealing as these rewards may seem, many consumers are choosing not to own a credit card because of their inability to qualify for one. As card issuers go head-to-head in the battle to reach and connect with new consumers, they must implement more inclusive lending strategies to not only extend credit to underserved communities, but also grow their customer base. Here’s how card issuers can stay ahead: Reach: Look beyond the traditional credit scoring system With limited or no credit history, credit invisibles are often overlooked by lenders who rely solely on traditional credit information to determine applicants’ creditworthiness. This makes it difficult for credit invisibles to obtain financial products and services such as a credit card. However, not all credit invisibles are high-risk consumers and not every activity that could demonstrate their financial stability is captured by traditional data and scores. To better evaluate an applicant’s creditworthiness, lenders can leverage expanded data sources, such as an individual’s cash flow or bank account activity, as an additional lens into their financial health. With deeper insights into consumers’ banking behaviors, card issuers can more accurately assess their ability to pay and help historically disadvantaged populations increase their chances of approval. Not only will this empower underserved consumers to achieve their financial goals, but it provides card issuers with an opportunity to expand their customer base and improve profitability. Connect: Become a financial educator and advocate Credit card issuers looking to build lifelong relationships with new-to-credit consumers can do so by becoming their financial educator and mentor. Many new-to-credit consumers, such as Generation Z, are anxious about their finances but are interested in becoming financially literate. To help increase their credit understanding, card issuers can provide consumers with credit education tools and resources, such as infographics or ‘how-to’ guides, in their marketing campaigns. By learning about the basics and importance of credit, including what a credit score is and how to improve it, consumers can make smarter financial decisions, boost their creditworthiness, and stay loyal to the brand as they navigate their financial journeys. Accessing credit is a huge obstacle for consumers with limited or no credit history, but it doesn’t have to be. By leveraging expanded data sources and offering credit education to consumers, credit card issuers can approve more creditworthy applicants and unlock barriers to financial well-being. Visit us to learn about how Experian is helping businesses grow their portfolios and drive financial inclusion. Visit us

Big data is bringing changes to the way credit scores are reported and making it easier for lenders to find creditworthy consumers, and for consumers to qualify for the financing they need. Since last year’s annual report, alternative credit data1 has continued to gain in popularity. In Experian’s latest 2020 State of Alternative Credit Data report, we take a closer look at why alternative credit data is supplemental and essential to consumer lending and how it’s being adopted by both consumers and financial institutions. While the topic of alternative credit data has become more well known, its capabilities and benefits are still not widely discussed. For instance, did you know that … 89% of lenders agree that alternative credit data allows them to extend credit to more consumers. 96% of lenders agree that in times of economic stress, alternative credit data allows them to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure. 3 out of 4 consumers believe they are a better borrower than their credit score represents. Not only do consumers believe they’re more financially astute than their credit score depicts – but they’re happy to prove it, with 80% saying they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates. This year’s report provides a deeper look into lenders’ and consumers’ perceptions of alternative credit data, as well as an overview of the regulatory landscape and how alternative credit data is being used across the lending marketplace. Lenders who incorporate alternative credit data and machine learning techniques into their current processes can harness the data to unlock their portfolio’s growth potential, make smarter lending decisions and mitigate risk. Learn more in the 2020 State of Alternative Credit Data white paper. Download now

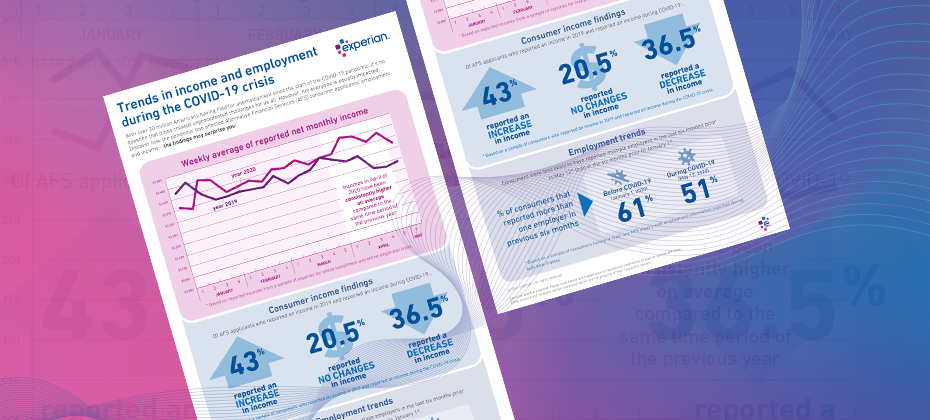

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

In today’s rapidly changing economic environment, the looming question of how to reduce portfolio volatility while still meeting consumers' needs is on every lender’s mind. So, how can you better asses risk for unbanked consumers and prime borrowers? Look no further than alternative credit data. In the face of severe financial stress, when borrowers are increasingly being shut out of traditional credit offerings, the adoption of alternative credit data allows lenders to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure without unnecessarily impacting insensitive or more “resilient” consumers. What is alternative credit data? Millions of consumers lack credit history or have difficulty obtaining credit from mainstream financial institutions. To ease access to credit for “invisible” and subprime consumers, financial institutions have sought ways to both extend and improve the methods by which they evaluate borrowers’ risk. This initiative to effectively score more consumers has involved the use of alternative credit data.1 Alternative credit data is FCRA-regulated data that is typically not included in a traditional credit report and helps lenders paint a fuller picture of a consumer, so borrowers can get better access to the financial services they need and deserve. How can it help during a downturn? The economic environment impacts consumers’ financial behavior. And with more than 100 million consumers already restricted by the traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By pulling in alternative credit data, such as consumer-permissioned data, rental payments and full-file public records, lenders can gain a holistic view of current and future customers. These insights help them expand their credit universe, identify potential fraud and determine an applicant’s ability to pay all while mitigating risk. Plus, many consumers are happy to share additional financial information. According to Experian research, 58% say that having the ability to contribute positive payment history to their credit files makes them feel more empowered. Likewise, many lenders are already expanding their sources for insights, with 65% using information beyond traditional credit report data in their current lending processes to make better decisions. By better assessing risk at the onset of the loan decisioning process, lenders can minimize credit losses while driving greater access to credit for consumers. Learn more 1When we refer to “Alternative Credit Data,” this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.

There are more than 100 million people in the United States who don’t have a fair chance at access to credit. These people are forced to rely on high-interest credit cards and loans for things most of us take for granted, like financing a family car or getting an apartment. At Experian, we have a fundamental mission to be a champion for the consumer. Our commitment to increasing financial inclusion and helping consumers gain access to the financial services they need is one of the reasons we have been selected as a Fintech Breakthrough Award winner for the third consecutive year. The Fintech Breakthrough Awards is the premier awards program founded to recognize the fintech innovators, leaders and visionaries from around the world. The 2020 Fintech Breakthrough Award program attracted more than 3,750 nominations from across the globe. Last year, Experian took home the award for Best Overall Analytics Platform for our Ascend Analytical Sandbox™, a first-to-market analytics environment that promised to move companies beyond just business intelligence and data visualization to data insights and answers they could use. The year prior, Experian won the Consumer Lending Innovation Award for our Text for Credit™ solution, a powerful tool for providing consumers the convenience to securely bypass the standard-length ‘pen & paper’ or keystroke intensive credit application process while helping lenders make smart, fraud protected lending decisions. This year, we are excited to announce that Experian has been selected once again as a winner in the Consumer Lending Innovation category for Experian Boost™. Experian Boost – with direct, active consumer consent – scans eligible accounts for ‘boostable’ positive payment data (e.g., utility and telecom payments) and provides the means for consumers to add that data to their Experian credit reports. Now, for the very first time, millions of consumers benefit from payments they’ve been making for years but were never reflected on their credit reports. Since launching in March 2019, cumulatively, more than 18 million points have been added to FICO® Scores via Experian Boost. Two-thirds of consumers who completed the Experian Boost process increased their FICO Score and among these, the average score increase has been more than 13 points, and 12% have moved up in credit score category. “Like many fintechs, our goal is to help more consumers gain access to the financial services they need,” said Alex Lintner, Group President of Experian Consumer Information Services. “Experian Boost is an example of our mission brought to life. It is the first and only service to truly put consumers in control of their credit. We’re proud of this recognition from Fintech Breakthrough and the momentum we’ve seen with Experian Boost to date.” Contributing consumer payment history to an Experian credit file allows fintech lenders to make more informed decisions when examining prospective borrowers. Only positive payment histories are aggregated through the platform and consumers can remove the new data at any time. There is no limit to how many times one can use Experian Boost to contribute new data. For more information, visit Experian.com/Boost.

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. If you typed “alternative data and credit” into a Google search today, you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – as Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as homeownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian, we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are others around the world. As I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time, there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-file consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game-changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s getting late.

Alex Lintner, Group President at Experian, recently had the chance to sit down with Peter Renton, creator of the Lend Academy Podcast, to discuss alternative credit data,1 UltraFICO, Experian Boost and expanding the credit universe. Lintner spoke about why Experian is determined to be the leader in bringing alternative credit data to the forefront of the lending marketplace to drive greater access to credit for consumers. “To move the tens of millions of “invisible” or “thin file” consumers into the financial mainstream will take innovation, and alternative data is one of the ways which we can do that,” said Lintner. Many U.S. consumers do not have a credit history or enough record of borrowing to establish a credit score, making it difficult for them to obtain credit from mainstream financial institutions. To ease access to credit for these consumers, financial institutions have sought ways to both extend and improve the methods by which they evaluate borrowers’ risk. By leveraging machine learning and alternative data products, like Experian BoostTM, lenders can get a more complete view into a consumer’s creditworthiness, allowing them to make better decisions and consumers to more easily access financial opportunities. Highlights include: The impact of Experian Boost on consumers’ credit scores Experian’s take on the state of the American consumer today Leveraging machine learning in the development of credit scores Expanding the marketable universe Listen now Learn more about alternative credit data 1When we refer to "Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term "Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.