Latest Posts

Earlier this year, the Consumer Financial Protection Bureau (CFPB) issued a Notice of Proposed Rulemaking (NPRM) to implement the Fair Debt Collection Practices Act (FDCPA). The proposal, which will go into deliberation in September and won't be finalized until after that date at the earliest, would provide consumers with clear-cut protections against disturbance by debt collectors and straightforward options to address or dispute debts. Additionally, the NPRM would set strict limits on the number of calls debt collectors may place to reach consumers weekly, as well as clarify how collectors may communicate lawfully using technologies developed after the FDCPA’s passage in 1977. So, what does this mean for collectors? The compliance conundrum is ever present, especially in the debt collection industry. Debt collectors are expected to continuously adapt to changing regulations, forcing them to spend time, energy and resources on maintaining compliance. As the most recent onslaught of developments and proposed new rules have been pushed out to the financial community, compliance professionals are once again working to implement changes. According to the Federal Register, here are some key ways the new regulation would affect debt collection: Limited to seven calls: Debt collectors would be limited to attempting to reach out to consumers by phone about a specific debt no more than seven times per week. Ability to unsubscribe: Consumers who do not wish to be contacted via newer technologies, including voicemails, emails and text messages must be given the option to opt-out of future communications. Use of newer technologies: Newer communication technologies, such as emails and text messages, may be used in debt collection, with certain limitations to protect consumer privacy. Required disclosures: Debt collectors will be obligated to send consumers a disclosure with certain information about the debt and related consumer protections. Limited contact: Consumers will be able to limit ways debt collectors contact them, for example at a specific telephone number, while they are at work or during certain hours. Now that you know the details, how can you prepare? At Experian, we understand the importance of an effective collections strategy. Our debt collection solutions automate and moderate dialogues and negotiations between consumers and collectors, making it easier for collection agencies to reach consumers while staying compliant. Powerful locating solution: Locate past-due consumers more accurately, efficiently and effectively. TrueTraceSM adds value to each contact by increasing your right-party contact rate. Exclusive contact information: Mitigate your compliance risk with a seamless and unparalleled solution. With Phone Number IDTM, you can identify who a phone is registered to, the phone type, carrier and the activation date. If you aren’t ready for the new CFPB regulation, what are you waiting for? Learn more Note: Click here for an update on the CFPB's proposal.

Big Data, once thought to be overhyped consultant-speak, is now a term and business model so ubiquitous it underpins billions of dollars in revenue across nearly every industry. Similarly, the advanced analytics derived from big data are key to staying relevant in an everchanging global economy and to consumers with expanding expectations. But for many financial institutions, using big data and advanced analytics seemed to only be in reach for big banks with large, advanced data teams. With the expansion of the Experian Ascend Technology PlatformTM, the conversation is changing. Financial institutions of all sizes can now leverage advanced analytics, artificial intelligence and machine learning with new configurations in the award-winning platform. In a release earlier this week, Experian announced new tools and configurations in the Ascend Analytical SandboxTM to fit teams of every size and skill level. Now fintechs, banks and credit unions of every size can have access to Experian’s one-stop source for advanced analytics, business intelligence and ultimately, better decisions. The secure hybrid-cloud environment allows users to combine their own data sets with Experian’s exclusive data assets, including credit, alternative, commercial, auto and more. From there, users can build and test models across different stages of the lending cycle, including originations, prescreen, account management and collections, and seamlessly put their models into production. Experian’s Ascend Analytical Sandbox also allows users to benchmark their portfolios against the industry, identify credit trends and explore new product opportunities. All the insights gathered through the Ascend Analytical Sandbox can be viewed and shared through interactive dashboards and customizable reports that can be pulled in near real time. Additional use cases include: Reject inferencing – refine models, scorecards and strategies by analyzing trades opened by previous applicants who were rejected or approved but did not move forward Prescreen campaigns – design prescreen campaigns, evaluate results and improve strategies Cross-sell – identify cross-sell opportunities for existing customers and identify how they may be working with other lenders Collections strategies, stress testing and loss forecasting – build stronger models to identify customers that have ability and willingness to pay debts, stress test and forecast loss Peer benchmarking and industry trends – compare current portfolio against peers and the industry Recession planning – identify areas to adjust your portfolio to prepare for an economic downturn OneMain Financial, a large provider of personal installment loans serving 10 million total customers across more than 1,700 branches, turned to Experian to improve its risk modeling and credit portfolio management capabilities with the Ascend Analytical Sandbox. Since using the solution, the company has seen significant improvements in reject inferencing – a process that is traditionally expensive, manually-intensive and time consuming. According to OneMain Financial, the Ascend Analytical Sandbox has shortened the process to less than two weeks from up to 180 days. "Experian's Ascend Technology Platform and Analytical Sandbox is an industry gamechanger," said Michael Kortering, OneMain Financial's Senior Managing Director and Head of Model Development. "We're completing analyses that just weren't possible before and we're getting decisions to our clients faster, without compromising risk.” For more information on Ascend Analytical Sandbox SX – the latest solution for financial institutions of all sizes – or other enterprise-wide capabilities of the Experian Ascend Technology Platform, click here.

The fact that the last recession started right as smartphones were introduced to the world gives some perspective into how technology has changed over the past decade. Organizations need to leverage the same technological advancements, such as artificial intelligence and machine learning, to improve their collections strategies. These advanced analytics platforms and technologies can be used to gauge customer preferences, as well as automate the collections process. When faced with higher volumes of delinquent loans, some organizations rapidly hire inexperienced staff. With new analytical advancements, organizations can reduce overhead and maintain compliance through the collections process. Additionally, advanced analytics and technology can help manage customers throughout the customer life cycle. Let’s explore further: Why use advanced analytics in collections? Collections strategies demand diverse approaches, which is where analytics-based strategies and collections models come into play. As each customer and situation differs, machine learning techniques and constraint-based optimization can open doors for your organization. By rethinking collections outreach beyond static classifications (such as the stage of account delinquency) and instead prioritizing accounts most likely to respond to each collections treatment, you can create an improved collections experience. How does collections analytics empower your customers? Customer engagement, carefully considered, perhaps comprises the most critical aspect of a collections program—especially given historical perceptions of the collections process. Experian recently analyzed the impact of traditional collections methods and found that three percent of card portfolios closed their accounts after paying their balances in full. And 75 percent of those closures occurred shortly after the account became current. Under traditional methods, a bank may collect outstanding debt but will probably miss out on long-term customer loyalty and future revenue opportunities. Only effective technology, modeling and analytics can move us from a linear collections approach towards a more customer-focused treatment while controlling costs and meeting other business objectives. Advanced analytics and machine learning represent the most important advances in collections. Furthermore, powerful digital innovations such as better criteria for customer segmentation and more effective contact strategies can transform collections operations, while improving performance and raising customer service standards at a lower cost. Empowering consumers in a digital, safe and consumer-centric environment affects the complete collections agenda—beginning with prevention and management of bad debt and extending through internal and external account resolution. When should I get started? It’s never too early to assess and modernize technology within collections—as well as customer engagement strategies—to produce an efficient, innovative game plan. Smarter decisions lead to higher recovery rates, automation and self-service tools reduce costs and a more comprehensive customer view enhances relationships. An investment today can minimize the negative impacts of the delinquency challenges posed by a potential recession. Collections transformation has already begun, with organizations assembling data and developing algorithms to improve their existing collections processes. In advance of the next recession, two options present themselves: to scramble in a reactive manner or approach collections proactively. Which do you choose? Get started

There are thousands of potential car buyers heading into dealerships and browsing websites for their next vehicle every day. And that means thousands of opportunities for automotive manufacturers to market their vehicles to prospective buyers. But not every vehicle is going to meet the needs and wants of every car buyer. So, how do automotive brand marketers reach the individuals most likely to be interested in their products? Simply put, it comes down to better understanding the brand’s audience. But, today’s digitally-driven world creates a significant challenge for brand marketers – the overreliance on mobile devices and digital channels creates hundreds of digital touchpoints for brand marketers to consider. But, the data also creates an opportunity. If automotive marketers can bridge the gap between online and offline touchpoints, they’ll be better positioned to develop messages that resonate with their desired audience and deliver communications through the most effective channels. The end result? More meaningful interaction with potential car buyers. To get there, automotive marketers need to consider these concepts: Navigate the identity resolution process The secret to a more relevant conversation begins and ends with knowing who you are addressing. People interact with brands through a variety of channels. For example, a person may see an advertisement for a new vehicle on their smartphone, later research the same vehicle at home on their desktop or on a mobile app and test drive the vehicle a few days later. The automotive marketer that can reconcile these three different interactions will be able to deliver relevant advertisements to the individual and cut down on wasted advertising spend. Knowledge-based identity resolution is what allows you to be smarter with your marketing. Present the right offer People are bombarded with hundreds, if not thousands, of advertisements daily. Automotive marketers need to cut through the noise and deliver messages that resonate with the target audience – whether it’s through e-newsletters, 30-second TV spots, banner ads or direct mail pieces. If automotive manufacturers miss the mark, it could lead to a frustrated consumer and poor brand reputation. For instance, an automotive marketer would not want to advertise the latest minivan to a couple who are empty nesters. Create customer loyalty It’s important to stay on top of current market statistics and data to fine-tune marketing campaigns. Vehicle ownership and purchase patterns can vary greatly in each market, and that means brands might need to fine-tune long-term loyalty strategies. A loyalty program that works in the Northeast might not work well for the Midwest market based on car buying patterns and the reasons behind owning a car. Data can help prioritize resources in areas with the highest potential for sales growth. Experian Marketing EngineTM helps automotive manufacturers engage customers across every channel while making the most of a marketing budget. It’s designed to seamlessly collect, consolidate and use customer data by connecting offline and online identifiers to create a single customer view. Experian’s North American Vehicle Database alone has over 11 billion records and over 900 million vehicles, of which over 68 million are Canadian vehicles. Marketing Engine leverages automotive specific insights, including vehicle purchase behaviors and ownership data, and combines that with other marketing data such as demographics and lifestyle interests. These automotive tools provide a more unified approach so that brands can make more informed decisions, gain and retain new customers, and drive sales. Learn more at https://www.experian.com/automotive/marketing.

Today, Experian and Oliver Wyman announced the launch of Ascend CECL ForecasterTM, a solution built to help financial institutions of all sizes more quickly and accurately forecast lifetime credit losses. The Financial Accounting Standards Board’s current expected credit loss (CECL) model has been a hot discussion topic throughout the financial services industry - first when it was announced (and considered one of the most significant accounting changes in decades), and most recently with the FASB’s delay for implementation for smaller lenders. As the compliance deadlines approach, Experian and Oliver Wyman have joined forces to help financial institutions adhere their loan portfolios to the new guidelines. Delivered through Experian’s Ascend Technology PlatformTM, Ascend CECL Forecaster is a new user-friendly, web-based application that combines Experian’s vast loan-level data and Premier AttributesSM, third-party macroeconomic data, valuation data and Oliver Wyman’s industry-leading CECL modeling methodology to accurately calculate potential losses over the life of a loan. “Ascend CECL Forecaster is a critical capability needed urgently by all lending and financial institutions,” said Ash Gupta, a Senior Advisor to Oliver Wyman and former Chief Risk Officer for American Express, in a press release. “The collaboration between Experian and Oliver Wyman allows a frictionless synthesis of industry data, capabilities and experience to serve customers in both first and second line of defense.” The premise behind the model, which will need access to more data than that used to calculate reserves under the incurred loss model, Allowance for Loan and Lease Losses (ALLL), is for financial institutions to estimate the expected loss over the life of a loan by using historical information, current conditions and reasonable forecasts. Built using advanced machine learning and statistical techniques, the web-based application maximizes the more than 15 years of historical credit data spanning previous economic cycles to help financial institutions gauge loan portfolio performance under various scenarios. Ascend CECL Forecaster does not require additional data nor does it require a secondary integration from the financial institution and enables organizations to more quickly test their portfolios under different economic factors. Moreover, financial institutions receive guidance from industry experts to assist with implementation and strategy. Additionally, Experian and Oliver Wyman will host a webinar to help financial institutions better understand and prepare for the upcoming CECL standards. Register today! Read the Press Release Register for Webinar

Have you seen the latest Telephone Consumer Protection Act (TCPA) class action lawsuit? TCPA litigations in the communications, energy and media industries are dominating the headlines, with companies paying up to millions of dollars in damages. Consumer disputes have increased more than 500 percent in the past five years, and regulations continue to tighten. Now more than ever, it’s crucial to build effective and cost-efficient contact strategies. But how? First, know your facts. Second, let us help. What is the TCPA? As you’re aware, TCPA aims to safeguard consumer privacy by regulating telephone solicitations and the use of prerecorded messages, auto-dialed calls, text messages and unsolicited faxes. The rule has been amended and more tightly defined over time. Why is TCPA compliance important? Businesses found guilty of violating TCPA regulations face steep penalties – fines range from $500 to $1500 per individual infraction! Companies have been delivered hefty penalties upwards of hundreds of thousands, and in some cases, millions of dollars. Many have questions and are seeking to understand how they might adjust their policies and call practices. How can you protect yourself? To help avoid risk for compliance violations, it’s integral to assess call strategies and put best practices in place to increase right-party contact rates. Strategies to gain compliance and mitigate risk include: Focus on right and wrong-party contact to improve customer service: Monitoring and verifying consumer contact information can seem like a tedious task, but with the right combination of data, including skip tracing data from consumer credit data, alternative and other exclusive data sources, past-due consumers can be located faster. Scrub often for updated or verified information: Phone numbers can continuously change, and they’re only one piece of a consumer’s contact information. Verifying contact information for TCPA compliance with a partner you can trust can help make data quality routine. Determine when and how often you dial cell phones: Or, given new considerations proposed by the CFPB, consider looking at collections via your consumers’ preferred communication channel – online vs. over the phone. Provide consumers user-friendly mechanisms to opt-out of receiving communications At Experian, our TCPA solutions can help you monitor and verify consumer contact information, locate past-due consumers, improve your right-party contact rates and automate your collections process. Get started

Consumer behavior is constantly evolving — from the channels they prefer to the economic trends spurring varying interest and activity. It’s no surprise that businesses find it challenging to know what their customers want today or tomorrow. But knowing and understanding this information is essential to growing your bottom line. Through years of working with businesses across every vertical, we’ve found that a solid approach to growing your business revolves around your customers. The better you know your customers, the better you can achieve your goals. Seeing the future. How well can you identify and rank your current customer population? Are you leveraging that insight to acquire new customers, manage current customers and prioritize collections efforts? If so, you’re probably using custom models in your business strategy. But if your organization is like many businesses, you may use a more traditional approach. In our highly competitive market, strategy and decisions must be based on the right data and insights. No excuses. The data is there, and we can help you turn it into actionable insights. Implementing a custom model can maximize your return on investment and help you make more profitable business decisions — now and in the future. No palm reading required. Without visiting your local fortuneteller, you still can predict the future. You need a model, but not the “runway” type. What constitutes a highly predictive and effective model? Many factors. A highly predictive custom model should incorporate robust data, advanced modeling methodologies, analytical expertise and attributes. Having these foundational components is essential to knowing your customers and making confident decisions. Models aren’t one-size-fits-all. When you take an innovative approach to model development, the model is targeted to support your specific business goals while providing the documentation required for regulatory reviews. Consider these items as you develop your custom model: Data — It all starts with the right data. Combining multiple data assets — your master-file data, our credit data and any additional data sources — is key to developing a robust model development sample. In other words, a model development sample should represent your future through-the-door population. Model design — To ensure the custom model is designed to help you achieve your specific goals, you’ll want to incorporate the latest analytics and modeling methodologies. An experienced analytics team will be essential here. Segmentation — With the right model development and segmentation strategies, you can identify optimal segments that will result in a more predictive custom model. This way, each consumer is scored on a scorecard developed using a credit profile similar to theirs. Validation — To ensure the model’s predictive ability and longevity, validate each custom model on a holdout sample and compare it with other scores to ensure it accounts for the current and future (through-the-door) consumer populations, as well as policy rule and behavioral changes. Regulatory review — Don’t forget about the documentation needed for compliance. While audits are unpleasant , fines and extensive scrutiny can significantly impact your business. Take your fortunetelling to the next level. Machine learning is all the rage. This cutting-edge technology can be embedded in your predictive models to help uncover patterns in data that may not be apparent otherwise. This can be done by comparing the performance of the machine learning model with your existing models. Once you know that machine learning can add the lift you’re looking for, you can apply that methodology to develop a custom model focused on stability, cost-efficiency, transparency and predictive performance. Predicting behavior across the Customer Life Cycle. How can a custom model benefit you? From improving baseline performance and increasing profitability by approving more good accounts to uncovering opportunities within your target market, custom models can provide the confidence needed to grow your business. Which one of these models can help you achieve your business goals? When it comes to accurately predicting customer behavior, you don’t need a crystal ball. You need a well-built, highly predictive custom model. Use the data that’s available to gain insight into your customers and grow your bottom line. If you need help, we’re here. We have the data, analytics and expertise to help you get started.

Digital channels undoubtedly create convenient experiences for consumers. We have the luxury of applying for loans or creating investment accounts from the comfort of home. However, the same opportunities are available to fraudsters. Fraudsters continue to find creative and innovative ways to expose vulnerabilities across all types of businesses. They prey on inexperienced or low-bandwidth teams that have not invested in the appropriate fraud tools in the past. Despite the imminent fraud risk involved, both consumers and businesses continue to embrace digital channels. With 90 percent of consumers worldwide conducting personal banking online, how do we protect these digital platforms with finite resources? A leading digital financial services company was forced to address this question when they experienced a large-scale fraud attack. But they weren’t in this fight alone. Download the full case study to see how our risk analyst used FraudNet to prevent millions of dollars in fraudulent funding. Client: A leading digital financial services company that operates with zero in-person branches with more than 7,000 employees Challenge/Objective: In October 2018, fraudsters deployed a large-scale, scripted attack against a North American financial services company. The fraud team was extremely understaffed. The fraud team was unable to detect and respond to the attack quickly. The fraudulent account opening activities eventually blended into account takeovers. Resolution: Our risk analyst worked quickly to analyze the geolocation, velocity and device rules firing within FraudNet for Account Opening. By having these rules in place, FraudNet was able to flag and outsort thousands of suspicious applications. Despite being a small team, the fraud investigators were able to work efficiently within the FraudNet workbench and review the true, high-risk applications. Results: Thanks to our risk analyst’s quick remediation and the FraudNet proprietary device rules: 23,800 fraudulent applications were outsorted for review. An estimated $35.7 million in fraudulent funding was prevented. However, the fight against fraud is ongoing. Our risk analyst continues to work closely with the fraud team to develop an effective strategy to prepare against future attacks.

Preparation is key – whether you’re an amateur/professional sports, free-soloing up El Capitan, or business contingency planning as part of a recession readiness strategy. It’s not so much predicting when events will occur, or trying to foresee and pivot for every possible outcome, but rather, acting now so that your business can act faster and smarter in the future. There are certain priorities that have come to be associated with what are widely accepted as the three environments the economy can sustain at any one time: As with recessions throughout the country’s history, those periods have often been characterized by layoffs, charge-offs, delinquencies, and other behaviors as the economy turns to a counter-cycle environment. Rather than wait to implement reactive strategies , the time to manage accounts, plan, stress test and implement contingency plans for when the next economic correction comes, is now. While economists and financial services industry experts argue over when a recession will hit and how severe its implications may be (in comparison with the Great Recession of 2008), there’s a need to start tactical business discussions now. Even in the face of a strong economy, that has seen high employment levels and increased spending, 45% of Americans (112.5 million) say they do not have enough savings to cover at least three months of living expenses, according to a 2018 survey by the Center for Financial Services Innovation. Regardless of the economic environment – pro-cycle, counter-cycle, and cycle-neutral – those statistics paint an alarming picture of consumers' financial health as a whole. These are four crucial considerations you should be taking now: Create individualized treatments while reducing manual interactions Meet the growing expectation for digital consumer self-service Understand your customer to ensure fair treatment React quickly and effectively to market changes While it may not be on the immediate horizon just yet, it’s important to prepare. For more information, including portfolio mixes, collections considerations and macroeconomic trends, download our latest white paper on recession readiness. Download white paper now

It's been over 10 years since the start of the Great Recession. However, its widespread effects are still felt today. While the country has rebounded in many ways, its economic damage continues to influence consumers. Discover the Great Recession’s impact across generations: Americans of all ages have felt the effects of the Great Recession, making it imperative to begin recession proofing and better prepare for the next economic downturn. There are several steps your organization can take to become recession resistant and help your customers overcome personal financial difficulties. Are you ready should the next recession hit? Get started today

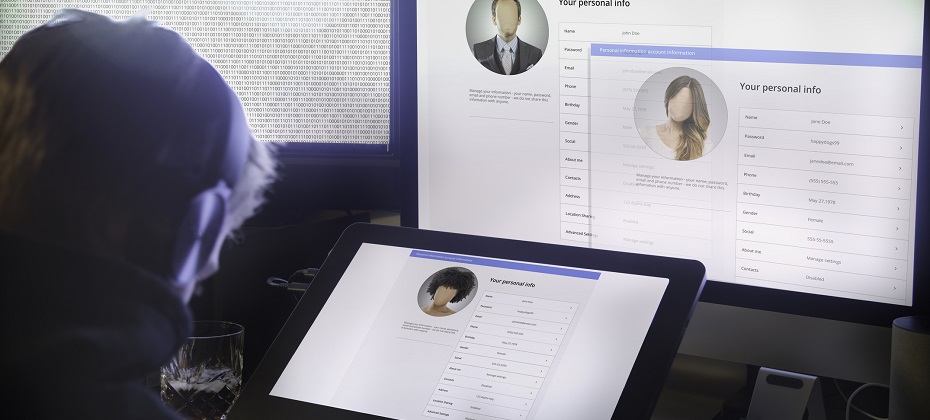

If you’ve seen an uptick in photos of friends and celebrities looking older with wrinkles on your social media feeds, you’re not alone. A new free photo editor has taken the internet by a storm, featuring an AI-powered image-altering application that allows users to see their “future self.” All you have to do is upload a single photo (or few) from your camera roll to be enhanced. While this may seem like harmless fun, the app is now making headlines over increased privacy concerns about what occurs behind the scenes once users submit their selfies. Red flags were raised when multiple alleged negative implications were connected to the app – including the app’s ownership and the potential risk that the app downloaded a user’s entire photo album onto their database. In fact, the privacy concerns also prompted Democratic Party officials to implore federal agencies, including the FBI, “to look into the potential national security and privacy risks the phone app poses to the United States.” Since then, the app’s creators have addressed these concerns, stating most of the photo processing occurs in the cloud and most photos are deleted within 48 hours. Additionally, the only photos uploaded are ones that have been personally submitted by the user. Regardless, a database of user-submitted photos could be seen as a goldmine to fraudsters. In a time where personal and biometric data (including facial recognition) are some of the key ways to validate security, it’s important for consumers to be aware of how and where they’re sharing their data, whether it’s for an age-progression photo app, or their financial accounts. Consumers, businesses, financial institutions – everyone – should exhibit caution and take measures to ensure personal information remains secure and is not being used for nefarious reasons. While consumers may be aware that businesses are collecting data, companies should take steps to form digital trust with transparency. This could be achieved by: Educating consumers on how their data is being used Effectively communicating privacy policies and service terms more concisely Helping consumers feel in control of their information To learn more about research that indicates a shift to advanced authentication methods (including biometrics), fraud trends and how to combat them, download our e-book. Download Now

Friend or foe? Sophisticated criminals put a great deal of effort into creating convincing, verifiable personas (AKA synthetic identities). Once the fictional customer has embedded itself in your business, everything from the acquisition of financial instruments to healthcare benefits, utility services, and tax filings and refunds become vulnerable to synthetic identity fraud. Information attached to synthetic IDs can run several levels deep and be so complete that it includes public record data, credit information, documentary evidence and social media profiles that may even contain photo sets and historical details intended to deceive—all complicating your efforts to identify these fake customers before you do business with them. See real-world examples of how synthetic identity fraud is souring various markets – from auto and healthcare to financial services and public sector – in our tip sheet, Four common synthetic scenarios. Stopping synthetic ID fraud — at the door and thereafter. There are efforts underway in the market to collectively improve your ability to identify, shut down and prevent synthetic identities from entering your portfolio. This overall trend is great news for the future, but there are also near-term solutions you can apply to protect your business starting now. While it’s important to identify synthetic identities when they knock on your door, it’s just as important to conduct regular portfolio checkups to prevent negative impacts to your collections efforts. Every circumstance has its own unique parameters, but the overarching steps necessary to mitigate fraud from synthetic IDs remain the same: Identify current and near-term exposure using targeted segmentation analysis. Apply technology that alerts you when identity data doesn’t add up. Differentiate fraudulent identities from those simply based on bad data. Review front- and back-end screening procedures until they satisfy best practices. Achieve a “single view of the customer” for all account holders across access channels—online, mobile, call center and face-to-face. The right tools for the job. In addition to the steps mentioned above, stopping these fake customers from entering and then stealing from your organization isn’t easy—but with the right tools and strategies, it is possible. Here are a few of our top recommendations: Forensics Isolate and segment identities based on signals received during early account pathing, from both individuals and their device. For example, even sophisticated fraud networks can’t mimic natural per-device user interaction because these organizations work with hundreds or thousands of synthetic identities using just a few devices. It’s highly unlikely that multiple geographically separate account holders would share the same physical device. High-risk fraud scores Not all synthetic identity fraud manifests the same way. Using sophisticated logic and unique combinations of data, a high-risk fraud score looks at a consumer’s credit behavior and credit relationships over time to uncover previously undetectable risk. These scores are especially successful in detecting identities that are products of synthetic identity farms. And by targeting a specific data set and relationships, you can maintain a frictionless customer experience and reduce false positives. Analytics Use a solution that develops models of bad applicant behavior, then compares and scores your portfolio against these models. There isn’t a single rule for detecting fraudulent identities, but you can develop an informed set of rules and targeted models with the right service partner. Cross-referencing models designed to isolate high-risk identity theft cases, first-party or true-name fraud schemes, and synthetic identities can be accomplished in a decisioning strategy or via a custom model that incorporates the aggregate scores and attributes holistically. Synthetic identity detection rules These specialized rules consist of numerous conditions that evaluate a broad selection of consumer behaviors. When they occur in specific combinations, these behaviors indicate synthetic identity fraud. This broad-based approach provides a comprehensive evaluation of an identity to more effectively determine if it’s fabricated. It also helps reduce the incidence of inaccurately associating a real identity with a fictitious one, providing a better customer experience. Work streams Address synthetic identities confidently by applying analytics to work streams throughout the customer life cycle: Credit risk assessment Know Your Customer/Customer Identification Program checks Risk-based identity proofing and authentication Existing account management Manual reviews, investigations and charge-offs/collections activities Learn more about these tools and others that can help you mitigate synthetic identities in our white paper, Synthetic identities: getting real with customers. If your organization is like most, detecting SIDs hasn't been your top priority. So, there's no time to waste in preventing them from entering your portfolio. Criminals are highly motivated to innovate their approaches as rapidly as possible, and it’s important to implement a solution that addresses the continued rise of synthetic IDs from multiple engagement points. With the right set of analytics and decisioning tools, you can reduce exposure to fraud and losses stemming from synthetic identity attacks from the beginning and across the customer life cycle. We can help you detect and mitigate these fake customers before they become delinquent. Learn more

You can do everything you can to prepare for the unexpected. But similar to how any first-time parent feels… you might need some help. Call in the grandparents! Experian has extensive expertise and has been around for a long time in the industry, but unlike your traditional grandparents, Experian continuously innovates, researches trends, and validates best practices in fraud and identity verification. That’s why we explored two prominent fraud reports, Javelin’s 2019 Identity Fraud Study: Fraudsters Seek New Targets and Victims Bear the Brunt and Experian’s 2019 Global Identity and Fraud Report — Consumer trust: Building meaningful relationships online, to help you identify and respond to new trends surrounding fraud. What we found – and what you need to know – is there are trends, technology and tactics that can help and hinder your fraud-prevention efforts. Consider the many digital channels available today. A full 91 percent of consumers transacted online in 2018. This presents a great opportunity for businesses to serve and develop relationships with customers. It also presents a great opportunity for fraudsters as well – as almost half of consumers have experienced a fraudulent online event. Since the threat of fraud is not impacting customers’ willingness to transact online, businesses are held responsible for adapting and evolving to not only protect their customers, but to secure their bottom line. This becomes increasingly important as fraudsters continue to target and expose vulnerabilities across inexperienced lines of businesses. Or, how about passwords. Research has shown that both businesses and consumers have greater confidence in biometrics, but neither is ready to stop using passwords. The continued reliance on traditional authentication methods is a delicate balance between security, trust and convenience. Passwords provide both authentication and consumer confidence in the online experience. It also adds friction to the user experience – and sometimes aggravation when passwords are forgotten. Advanced methods, like physical and behavioral biometrics and device intelligence, are gaining user confidence by both businesses and consumers. But a completely frictionless authentication experience can leave consumers doubting the safeness of their transaction. As you respond and adapt to our ever-evolving world, we encourage you to build and strengthen a trusted relationship with your customers through transparency. Consumers know that businesses are collection data about them. When a business is transparent about the use of that data, digital trust and consumer confidence soars. Through a stronger relationship, customers are more willing to accept friction and need fewer signs of security. Learn more about these and other trends, technology and tactics that can help and hinder your authentication efforts in our new E-book, Upcoming fraud trends and how to combat them.

Vehicle affordability has been a main topic of conversation in the auto industry for some time, and based on the data, it’s not going unnoticed by consumers. The average new vehicle loan in Q1 2019 reached $32,187, while the average new vehicle monthly loan payment hit $554. How are car shoppers reacting? Perhaps the biggest shift in Q1 2019 was the growth of prime and super prime customers opting for used vehicles. The percentage of prime (61.88 percent) and super-prime (44.78 percent) consumers choosing used vehicles reached an all-time high in Q1 2019, according to Experian data. Not only are we seeing new payment amounts increase, but used loan amounts and payments are on the rise as well, though the delta between the two can be one of the reason we’re seeing more prime and super prime opt for used. The average used vehicle loan was slightly above $20,000 in Q1 2019, while the average used vehicle payment was $391. We know that consumers often shop based on the monthly payment amount, and given the $163 difference between average monthly payments for new and used, it’s not surprising to see more people opt for used vehicles. Another way that consumers can look to have a smaller payment amount is through leasing. We’re continuing to see that the top vehicles leased are more expensive CUVs, trucks and SUVs, which are pricier vehicles to purchase. But with the average lease payment being $457 per month, there’s an average difference of $97 compared to loan payments. In Q1 2019, leasing was down slightly year-over-year, but still accounted for 29.07 percent of all vehicle financing. On the other side of the affordability equation, beyond cost of vehicles, is concern around delinquencies: will consumers be able to make their payments in a timely manner? So far, so good. In Q1 2019, 30-day delinquencies saw an increase to 1.98 percent, up from 1.9 percent a year ago. That said, banks, credit unions and finance companies all saw slight decreases in 30-day delinquency rates, and 60-day delinquencies remained relatively stable at 0.68 percent year-over-year. It’s important to keep in mind that the 30-day delinquency rate is still well-below the high-water mark in Q1 2009 (2.81 percent). The vehicle finance market appears to remain strong overall, despite rising vehicle costs, loan amounts and monthly payments. Expect consumers to continue to find ways to minimize monthly payments. This could continue the shift into used vehicles. Overall, as long as delinquencies stay flat and vehicle sales don’t taper too badly, the auto finance market should stay on a positive course. To watch the full Q1 2019 State of the Automotive Finance Market webinar, click here.

Would you hire a new employee strictly by their resume? Surely not – there’s so much more to a candidate than what’s written on paper. With that being said, why would you determine your consumers’ creditworthiness based only on their traditional credit score? Resumes don’t always give you the full picture behind an applicant and can only tell a part of someone’s story, just as a traditional credit score can also be a limited view of your consumers. And lenders agree – findings from Experian’s 2019 State of Alternative Credit Data revealed that 65% of lenders are already leveraging information beyond the traditional credit report to make lending decisions. So in addition to the resume, hiring managers should look into a candidate’s references, which are typically used to confirm a candidate’s positive attributes and qualities. For lenders, this is alternative credit data. References are supplemental but essential to the resume, and allow you to gain new information to expand your view into a candidate – synonymous to alternative credit data’s role when it comes to lending. Lenders are tasked with evaluating their consumers to determine their stability and creditworthiness in an effort to prevent and reduce risk. While traditional credit data contains core information about a consumer’s credit data, it may not be enough for a lender to formulate a full and complete evaluation of the consumer. And for over 45 million Americans, the issue of having no credit history or a “thin” credit history is the equivalent of having a resume with little to no listed work experience. Alternative credit data helps to fill in the gaps, which has benefits for both lenders and consumers. In fact, 61% of consumers believe adding payment history would have a positive impact on their credit score, and therefore are willing to share their data with lenders. Alternative credit data is FCRA-compliant and includes information like alternative finance data, rental payments, utility payments, bank account information, consumer-permissioned data and full-file public records. Because this data shows a holistic view of the customer, it helps to determine their ability to repay debts and reveals any delinquent behaviors. These insights help lenders to expand their consumer lending universe– all while mitigating and preventing risk. The benefits can also be seen for home-based and small businesses. Fifty percent of all US small businesses are home-based, but many small business owners lack visibility due to their thin-file nature – making it extremely difficult to secure bank loans and capital to fund their businesses. And, younger generations and small business owners account for 58% of business owners who rely on short term lending. By leveraging alternative credit data, lenders can get greater insights into a small business owner’s credit profile and gauge risk. Entrepreneurs can also benefit from this information being used to build their credit profiles – making it easier for them to gain access to investment capital to fund their new ventures. Like a hiring manager, it’s important for lenders to get a comprehensive view to find the most qualified candidates. Using alternative credit data can expand your choices – read our 2019 State of Alternative Credit Data Whitepaper to learn more and register for our upcoming webinar. Register Now