Latest Posts

Meeting Know Your Customer (KYC) regulations and staying compliant is paramount to running your business with ensured confidence in who your customers are, the level of risk they pose, and maintained customer trust. What is KYC?KYC is the mandatory process to identify and verify the identity of clients of financial institutions, as required by the Financial Conduct Authority (FCA). KYC services go beyond simply standing up a customer identification program (CIP), though that is a key component. It involves fraud risk assessments in new and existing customer accounts. Financial institutions are required to incorporate risk-based procedures to monitor customer transactions and detect potential financial crimes or fraud risk. KYC policies help determine when suspicious activity reports (SAR) must be filed with the Department of Treasury’s FinCEN organization. According to the Federal Financial Institutions Examinations Council (FFIEC), a comprehensive KYC program should include:• Customer Identification Program (CIP): Identifies processes for verifying identities and establishing a reasonable belief that the identity is valid.• Customer due diligence: Verifying customer identities and assessing the associated risk of doing business.• Enhanced customer due diligence: Significant and comprehensive review of high-risk or high transactions and implementation of a suspicious activity-monitoring system to reduce risk to the institution. The following organizations have KYC oversight: Federal Financial Institutions Examinations Council (FFIEC), Federal Reserve Board, Federal Deposit Insurance Corporation (FDIC), national Credit Union Administration (NCUA), Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB). How to get started on building your Know Your Customer checklist 1. Define your Customer Identification Program (CIP) The CIP outlines the process for gathering necessary information about your customers. To start building your KYC checklist, you need to define your CIP procedure. This may include the documentation you require from customers, the sources of information you may use for verification and the procedures for customer due diligence. Your CIP procedure should align with your organization’s risk appetite and be comply with regulations such as the Patriot Act or Anti-money laundering laws. 2. Identify the customer's information Identifying the information you need to gather on your customer is key in building an effective KYC checklist. Typically, this can include their first and last name, date of birth, address, phone number, email address, Social Security Number or any government-issued identification number. When gathering sensitive information, ensure that you have privacy and security controls such as encryption, and that customer data is not shared with unauthorized personnel. 3. Determine the verification method There are various methods to verify a customer's identity. Some common identity verification methods include document verification, facial recognition, voice recognition, knowledge-based authentication, biometrics or database checks. When selecting an identity verification method, consider the accuracy, speed, cost and reliability. Choose a provider that is highly secure and offers compliance with current regulations. 4. Review your checklist regularly Your KYC checklist is not a one and done process. Instead, it’s an ongoing process that requires periodic review, updates and testing. You need to periodically review your checklist to ensure your processes are up to date with the latest regulations and your business needs. Reviewing your checklist will help your business to identify gaps or outdated practices in your KYC process. Make changes as needed and keep management informed of any changes. 5. Final stage: quality control As a final step, you should perform a quality control assessment of the processes you’ve incorporated to ensure they’ve been carried out effectively. This includes checking if all necessary customer information has been collected, whether the right identity verification method was implemented, if your checklist matches your CIP and whether the results were recorded correctly. KYC is a vital process for your organization in today's digital age. Building an effective KYC checklist is essential to ensure compliance with regulations and mitigate risk factors associated with fraudulent activities. Building a solid checklist requires a clear understanding of your business needs, a comprehensive definition of your CIP, selection of the right verification method, and periodic reviews to ensure that the process is up to date. Remember, your customers' trust and privacy are at stake, so iensuring that your security processes and your KYC checklist are in place is essential. By following these guidelines, you can create a well-designed KYC checklist that reduces risk and satisfies your regulatory needs. Taking the next step Experian offers identity verification solutions as well as fully integrated, digital identity and fraud platforms. Experian’s CrossCore & Precise ID offering enables financial institutions to connect, access and orchestrate decisions that leverage multiple data sources and services. By combining risk-based authentication, identity proofing and fraud detection into a single, cloud-based platform with flexible orchestration and advanced analytics, Precise ID provides flexibility and solves for some of financial institutions’ biggest business challenges, including identity and fraud as it relates to digital onboarding and account take over; transaction monitoring and KYC/AML compliance and more, without adding undue friction. Learn more *This article includes content created by an AI language model and is intended to provide general information.

According to Experian’s Automotive Consumer Trends Report: Q3 2023, CUVs accounted for 48.3% of new retail registrations and SUVs comprised 13.0%.

As vehicle inventory continues to restore post-pandemic, data through the third quarter of 2023 showed new vehicle registrations are on the rise again—a positive sign that the market is leveling out. According to Experian’s Automotive Market Trends Report: Q3 2023, new vehicle registrations increased 12.7% year-over-year, reaching 11.5 million. On the used side, registrations declined to 29.3 million through Q3 2023, a 2% decrease from 29.9 million last year. Digging a bit deeper, CUVs/SUVs were the most registered new vehicle segment at 56.9%, up from 56.2% compared to last year. Pickup trucks declined from 18.6% to 17.4% year-over-year and sedans went from 17.1% to 16.8% in the same time frame. While knowing what types of vehicles consumers are interested in is beneficial for automotive professionals, breaking down the most sought-after models will paint a fuller picture as they assist shoppers in finding a vehicle that fits their needs. For instance, despite new pickup truck registrations declining year-over-year, the Ford F-150 made up the highest share of new vehicle registrations through Q3 2023—reaching 3%. The Tesla Model Y and Toyota RAV4 were not far behind, both coming in at 2.5% this quarter. They were followed by the Chevrolet Silverado 1500 and Honda CR-V tying at 2.3%. ICE vehicles continue to grow Taking a deeper dive into the fuel type share, ICE vehicles continue to grow year-over-year, even with electric vehicles (EVs) making headway into the market. Experian Automotive’s Vehicles in Operation (VIO) data as of Q3 2023 shows ICE vehicle registrations grew to 265.7 million, up from 264.5 million last year, while hybrid vehicles increased to 8.0 million, from 6.9 million in the same time frame. Meanwhile, EVs went from 2.0 million last year to 3.0 million this year and diesel saw a slight uptick from 9.6 million to 9.9 million in the same period. Leveraging different data points and staying up to date on vehicle registration trends can better prepare professionals as the market remains ever-changing and consumer preference continues to shift. To learn more about vehicle market trends, view the full Automotive Market Trends Report: Q3 2023 presentation on demand.

The online gaming industry has experienced tremendous growth. This surge in popularity has also sparked an increase in online gaming fraud.

Vehicles with recalls are on the road. In fact, as of July 2023, there were over 15M vehicles on the road in the United States that have a recall that was reported for that vehicle between January and June 2023². Awareness of Open Recalls and the availability of remedies is important for our Automotive clients. As a result, we have added the National Highway Transportation Safety Administration (NHTSA) number and remedy availability flag to three of our Vehicle History Data Solutions: AutoCheck Vehicle History Report Dealers and consumers will be aware of open recalls and if there is a remedy available for the recall. This can alleviate consumer concern over an open recall if there is no remedy available facilitating consumer confidence in a vehicle purchase. AutoCheck Triggers Clients will be aware of any open recalls and the remedy viability in their vehicle portfolio. Many clients use AutoCheck Triggers to make business decisions regarding their vehicle portfolio. Auto AccuSelect Adding the NHTSA recall number and remedy availability flag to Auto AccuSelect allows clients to be aware and take action regarding the vehicles they are evaluating. It is critical to know open recall information, as well as the overall history of a vehicle before buying or selling a used car. Experian Automotive’s vehicle history data solutions, such as a the AutoCheck vehicle history report, can help you buy and sell vehicles with confidence. AutoCheck has 98.96% of manufacturer coverage for recall data based on vehicles in operation. If you’d like to learn more about a recent analysis Experian Automotive conducted about the number of recalls reported for the first half of 2023, where those events were reported and where those vehicles are currently in operation, click to view our Recall Insights Infographic.

To stay competitive and engage high-value customers, you’ll need to optimize your customer acquisition process.

. As we reflect on 2023, let’s look at the biggest fraud trends and their continued potential impact on your business.

Offering identity theft protection is an effective way to maintain strong customer relationships and deliver an engaging experience.

Cris Ryan, Go to Market Lead for Experian Identity and Fraud, shares his thoughts on demand deposit account fraud and how to combat it.

Future-proof your business and safeguard your customers with fraud detection leveraging machine learning solutions.

Learn how expanded data, AI-driven models, and increased automation can help you enhance your credit risk management strategies.

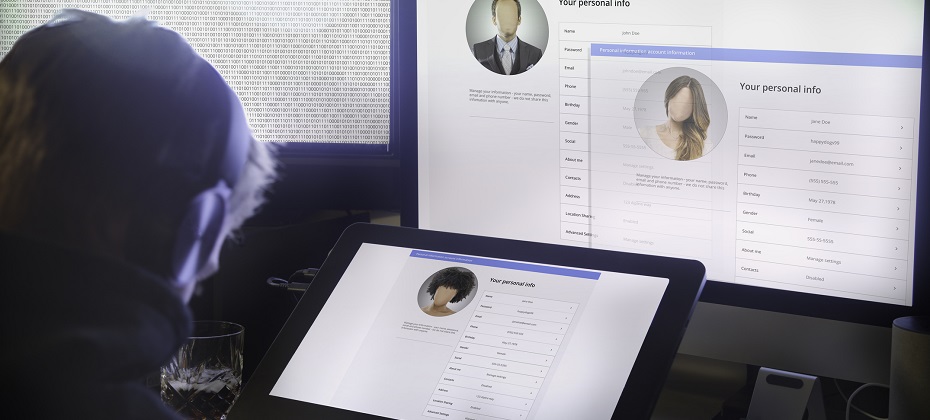

Sometimes logging into an account feels a bit like playing 20 questions. Security is vital for a positive customer experience, and engaging the right identity verification strategies is essential to proactive fraud prevention. For financial institutions and businesses, secure authentication is more important than ever. It is imperative for customer safety – which drives retention and loyalty – and your bottom line – as fraud has determinantal effects on and off the balance sheet. Information sharing has proliferated, as has the number of times consumers are prompted to provide access to sensitive information. While today’s consumer has grown accustomed to providing such information, there’s also a heightened demand for security. According to Experian’s 2023 U.S. Identity and Fraud Report, nearly two-thirds (64%) of consumers say they’re very or somewhat concerned with online safety, listing identity theft, stolen card information and online privacy as top concerns. Customers want to know who they are providing access to and whether that entity will have their safety in mind. From a business perspective, one way to ensure that only the right people can get in is by using (KBA). KBA takes traditional authentication methods, like passwords and Personal Identification Numbers (PINs), one step further by creating an additional layer of security through collecting private facts from each user. In this post, we'll look at how KBA works, what its benefits are as a form of identity verification, and how it can improve customer trust. Introducing Knowledge Based Authentication (KBA): What it is and how it works Knowledge Based Authentication can be part of a multifactor authentication solution and is one way to stay on top of privacy and security for your customers – existing and new. KBA is a feature designed to protect online accounts by verifying the account holder’s identity. It involves answering a series of personal questions, such as mother's maiden name or first pet's name, that only the account holder should know. This system has become increasingly popular due to its effectiveness in preventing fraud and identity theft. With KBA, businesses and individuals can have peace of mind that their information is protected by a reliable authentication system that is difficult for unauthorized users to breach. Benefits of implementing KBA and a multifactor authentication strategy By implementing KBA into your business, customers experience an additional layer of security by verifying the identity of users through personalized questions. This reduces the risk of fraud and enhances customer trust and confidence. Secondly, it improves the customer experience by making the authentication process faster and user-friendly. Lastly, KBA reduces costs by automating the authentication process and reducing the need for manual intervention. However, KBA is just one facet of an ideal strategy. Multifactor authentication provides confidence while reducing friction. Risk-based authentication tools allow organizations to assess risk to apply the appropriate level of security. Factors to consider adding to your authentication processes include: Generating unique one-time passwords (OTPs): By creating a new OTP for each transaction, you can increase the level of security. Confirm device ownership: A multifactored approach applies device intelligence checks to increase confidence that the message is reaching the correct user. Maintain low friction with secondary options: If the OTP fails or can’t be attempted by the user, working with a provider who allows an automatic default to another authentication service, such as a knowledge-based authentication solution, decreases end-user friction. Identifying potential security risks associated with KBA KBA relies on personal information that may easily be discovered via social media and other public records, which makes it vulnerable to fraud and identity theft. This highlights the need for a multilayered fraud and identity solution. The landscape of digital security is constantly changing, leveraging an arsenal of fraud and identity prevention strategies, like document verification, one-time passcode, and various identity authentication and verification measures, is critical for keeping your customers and business safe. Commonly used technologies for enhancing KBA security With the rising need for secure authentication, KBA systems have become increasingly popular. However, cyberthreats evolve at an alarming rate, making it imperative to stay current with the latest fraud schemes and how to enhance and supplement your security. Biometrics, like facial recognition and fingerprint scans, as a tactic is gaining traction, as evidenced by “85% of consumers report physical biometrics as the most trusted and secure authentication method they have recently encountered,” according to Experian’s 2023 U.S. Identity and Fraud Report. Additionally, machine learning algorithms detect patterns and anomalies in user behavior and flag any potential security breaches. Multi-factor authentication is another tool that adds an extra layer of security by requiring users to provide multiple forms of identification before logging in. Keeping up with these and other technological advancements can help ensure your KBA system stays one step ahead of potential cyberattacks. Interestingly, there’s a disconnect between the technologies consumers feel safe with and/or are prepared to use versus the technologies and strategies that organizations implement. According to the U.S. Identity and Fraud Report, biometrics are only currently used by 33% of businesses to detect and protect against fraud. An opportunity for business differentiation and driving customer loyalty through a better customer experience may be tapping into some of these lesser used – but sought after – technologies. Compliance with industry standards regarding KBA Ensuring that your system complies with industry standards regarding KBA is crucial for protecting sensitive information from unauthorized access. By implementing the following tips, you can stay ahead of the game and safeguard your organization's data. Analyze your system's current authentication methods and evaluate if they meet industry standards. Additionally, follow standard guidelines for data storage and encryption, limit access to only authorized personnel, and y current with regulations. Lastly, conduct frequent security audits and perform vulnerability tests to identify and address any potential threats. Knowledge-based authentication offers a robust security solution for businesses of all sizes, and incorporating KBA as part of a multifactor authentication strategy is a winning course of action. It provides an added layer of protection for personal data, encourages user accountability, and safeguards against unauthorized access. By leveraging appropriate KBA technologies and maintaining compliance with industry standards, it is possible to create a secure system for customers that gives you peace of mind for your business and bottom line. Experian can help you with knowledge-based authentication offerings, a multifactor authentication strategy and everything in between to enhance your existing authentication process without causing user fatigue. Increase your pass rates, confirm device ownership and add security to risky or high-value transactions, all while executing identity verification and fraud detection to protect your business from risk. The most important step is getting started. Learn more

According to Experian’s State of the Automotive Finance Market Report: Q3 2023, the average new vehicle loan amount decreased to $40,184, from $41,543 in Q3 2022 and the average used vehicle loan amount went from $28,684 to $27,167 year-over-year.

Learn how a well-designed underwriting strategy can help you drive growth and create more value out of your member relationships.

Learn about travel, hospitality and hotel fraud and how you can best detect and combat it. Read more here!