Fintech

Fintech

Congress recently took several actions signaling a growing interest in regulatory issues surrounding the Fintech sector. This growing attention follows a number of recent inquiries by federal and state regulators into the business practices in the industry. Subcommittee takes a deep dive into Fintech and OML regulatory landscape In July, the House Subcommittee on Financial Institutions and Consumer Credit held a hearing entitled Examining the Opportunities and Challenges with Financial Technology (“Fintech”). Witnesses and lawmakers voiced optimism that online marketplace lending can help to expand access to capital for consumers and small businesses, but the hearing also focused on a growing schism as to whether new regulations or changes to the underlying framework is necessary to ensure consumers are protected. Some lawmakers and the witness from the American Banking Association expressed concerns that the Fintech and marketplace lenders may benefit from being outside of the supervisory scope of prudential regulators and the Consumer Financial Protection Bureau (CFPB). Witnesses from the marketplace lending industry argued that they are obligated to meet all of the same regulatory compliance requirements as traditional lenders. Rep. McHenry introduces package of Fintech bills aimed at spurring innovation In addition, Congressman Patrick McHenry (R-NC), a member of the House Republican Leadership team and the Vice Chairman of the House Financial Services Committee, introduced two bills this month aimed at spurring innovation in the Fintech industry. H.R. 5724, the Protecting Consumers’ Access to Credit Act of 2016, would clarify that federal law preempts a loan’s interest rate as valid when made. The bill is in response to the Supreme Court’s recent decision not to hear Madden v Midland, a case in which the Second Circuit court ruled that the National Bank Act does not have a preemptive effect after the national bank has sold or otherwise assigned the loan to another party. The reading of this law has created uncertainty for Fintech companies and the banks that partner with them. H.R. 5725, the IRS Data Verification Modernization Act of 2016, requires the IRS to automate the Income Verification Express Service process by creating an Application Programming Interface (API). The legislation is aimed at speeding up and improving the automation of the loan application process. In particular, it is aimed at streamlining the process by which lenders gain access to tax transcript data. Currently, lenders may require applicants to fill out IRS form “4506-T,” which gives the lender the right to access a summarized version of their tax transcript as part of the process to confirm certain data points on their application. According to industry reports, this manual process at the IRS takes two to eight days, creating unnecessary delays for Fintech companies and banks that rely on leveraging data and technology to make faster, informed decision for consumer and small business lending Both bills have been referred to the House Financial Services Committee for review.

All customers are not created equally – at least when it comes to one’s ability to pay. Incomes differ, financial circumstances vary and economic challenges surface. Lost job. Totaled car. Unplanned medical bills. Life happens. Research conducted by a recent Bankrate study revealed just 38 percent of Americans said they could cover an unexpected emergency room visit or a $500 car repair with available cash in a checking or savings account. It’s a scary situation for individuals, and also a source of stress for the lender expecting payment. So what are the natural moments for a lender to assess “ability to pay?” Moment No. 1: When prepping for a prescreen campaign and at origination. Many lenders leverage an income estimation model, designed to give an indication of the customer’s capacity to take on additional debt by providing an estimation of their annual income. Within the model, multiple attributes are used to calculate the income, including: Number of accounts Account balances Utilization Average number of months since trade opened Combined, all of these insights determine a customer’s current obligations, as well as an estimation of their current income, to see if they can realistically take on more credit. The right models and criteria on the front-end – whether used when a consumer applies for new credit or when a lender is executing a prescreen campaign to acquire new customers – minimizes the risk for default. It’s a no-brainer. Moment No. 2: When a customer is already on your books. As the Bankrate study mentioned, sudden life events can send some customers’ lives into a financial tailspin. On the other hand, financial circumstances can change for the better too. Aggressively paying down a HELOC, doubling down on a mortgage, or wiping out a bankcard balance could signal an opportunity to extend more credit, while the reverse could be the first signs of payment stress. Attaching triggers to accounts can give lenders indications on what to do with either scenario, helping to grow a portfolio and protect it. Moment No. 3: When an account goes south. While a lender hates to think any of its accounts will plummet into collections, sometimes, it’s inevitable. Even prime customers fall behind, and suddenly financial institutions are faced with looking at collections strategies. Where should they place their bets? You can’t treat all delinquent customer equally and work the accounts the same way. Collection resources can be wasted on customers who are difficult or impossible to recover, so it’s best to turn to predictive analytics and a collections scoring strategy to prioritize efforts. Again, who has the greatest ability to pay? Then place your manpower on those individuals where you can recover the most dollars. --- Assessing one’s ability to pay is a cornerstone to the financial services business. The quest is to find the sweet spot with a combination of application data, behavioral data and credit risk scoring analytics.

His car, more than 10 years old and not worth salvaging, was in the shop again. Time to invest in something new – or at least “new-ish.” He headed to a local dealership, selected a practical model and applied for financing. “We can’t give you a loan,” said the manager. “Your income is not high enough, but perhaps if you bring in a co-signer ...” Denied. Her college degree hung on the wall of her childhood bedroom. In the months since she celebrated graduation with family and friends, she landed a job, but not one providing enough income to cover rent, a car payment and her hefty student loan payments. “I didn’t realize my payments would be so high,” said the woman. “I don’t know how I’ll ever climb out from under this debt and start my life.” Stalled. His attempt at applying for a bankcard, much needed to begin the journey of establishing credit in the country, was met with failure. “We can’t find any credit history on you,” says the lender. “Try again in the future.” Invisible. These stories are all too common in America. A lack of financial education, coupled with a few poor choices, can derail an individual’s financial trajectory. More light has certainly been shone on the topic of financial education and the importance of making smart credit decisions from a young age, but there is no nationwide financial education program offered in schools, and many parents feel ill-equipped to handle the task. Consider a few of these numbers: 71 percent of college grads recently surveyed by Experian said they did not learn about credit and debt management in college, giving their schools an average grade of “C” when it comes to preparing them to manage credit and debt after college The latest "State of Credit" revealed the average debt per consumer is $29,093 39 percent of newlyweds say credit scores is a source of stress in their marriage Money management is tough, and we expect people to just figure it out. But clearly, that’s not working. So we need to think about the world of credit differently. As Experian says, we need to treat it as a skill. We need to practice and learn and adjust. As you get better at credit, it opens doors, creates opportunities, and enables people to live the lives they wish to live. Suddenly, you can get the car loan, move out, have access to credit cards, and manage it all responsibly. In other words, you claim financial health. On the other hand, if you don’t work at this skill, a lack of financial health ensues. Unruly amounts of debt, irregular income and sporadic savings create stress, resentment and pain. Increasingly, more financial institutions are boosting efforts to educate about credit. Schools are exploring curriculum to talk finances and inject real-life money management scenarios into everyday lessons. Millennials are seeking transparency around credit transactions. The more financially healthy consumers we have in this country, building credit skills, means overall economies will grow. So yes, financial health matters. It matters to individuals, to lending institutions, to retailers and to communities big and small. Building those credit skills is essential. Your health depends on it.

What you give, you get. At least that is what popular philosophers claim. And if you think about it, this statement is also applicable to the world of data accuracy. As organizations of all sizes increasingly rely on data to interact with customers and create insights to drive strategy, it’s no secret bad data can quickly lead a company or financial institution down the wrong path, even landing them into regulatory troubles. A recent Experian Data Quality study found: Seventy-five percent of organizations believe inaccurate data is undermining their ability to provide an excellent customer experience. Sixty-five percent of organizations wait until there are specific issues with their data before they address and fix them. Fifty-six percent of organizations believe mistakes can be attributed to human error. For years, organizations have wanted good data simply for operational efficiencies and cost savings, but now a shift has taken place where businesses are using data for nearly every aspect of their organization. The majority of sales decisions are expected to be driven by customer data by 2020, with companies determined to turn data into actionable insight to find new customers, increase customer retention, better understand their needs, and increase the value of each customer. Additionally, the Fair Credit Reporting Act (FCRA) requires those contributing data to provide accurate and complete information to the credit reporting agencies. If they fail to meet accuracy obligations when reporting negative account histories to credit reporting companies, the result could be bureau action and fines. Organizations still deal with a high degree of inaccurate data because there are a number of challenges to maintaining it. Some of them are external forces, but many are internal challenges – most notably a reliance on reactive data management strategies. The biggest problem organizations face around data management today actually comes from within. Businesses get in their own way by refusing to create a culture around data and not prioritizing the proper funding and staffing for data management. Many businesses know they need to improve their data quality, but often have a hard time defining why an investment is needed in the current structure. Solutions exist to get in front of data accuracy challenges. DataArc 360 Powered by Experian Pandora, for example, is designed to check the consumer credit information provided by data furnishers prior to submission to credit bureaus. This allows data suppliers to take more of a proactive approach to ensuring the accuracy of information, that may result in fewer credit disputes and a more positive interaction between consumers and their credit. Creating a clear governance plan, and centralizing data management policies and policies can also clean up internal challenges and improve accuracy standards. The importance of data cannot be neglected, but again, the data has to be clean for it to matter. What you give is what you’ll get.

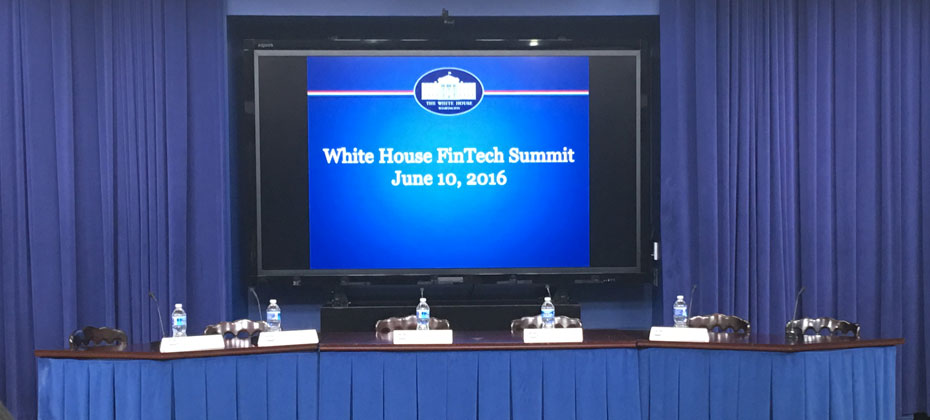

Experian consultant offers his recap from attending a half-day event hosted at The White House called the “FinTech Summit” largely focused on how government agencies can tap into the innovation, in which new firms are offering small-business owners and consumers faster forms of loans and digital payments. Federal regulators have been studying the industry to determine how it can be regulated while still encouraging innovation.

Part four in our series on Insights from Vision 2016 fraud and identity track It was a true honor to present alongside Experian fraud consultant Chris Danese and Barbara Simcox of Turnkey Risk Solutions in the synthetic and first-party fraud session at Vision 2016. Chris and Barbara, two individuals who have been fighting fraud for more than 25 years, kicked off the session with their definition of first-party versus third-party fraud trends and shared an actual case study of a first-party fraud scheme. The combination of the qualitative case study overlaid with quantitative data mining and link analysis debunked many myths surrounding the identification of first-party fraud and emphasized best practices for confidently differentiating first-party, first-pay-default and synthetic fraud schemes. Following these two passionate fraud fighters was a bit intimidating, but I was excited to discuss the different attributes included in first-party fraud models and how they can be impacted by the types of data going into the specific model. There were two big “takeaways” from this session for me and many others in the room. First, it is essential to use the correct analytical tools to find and manage true first-party fraud risk successfully. Using a credit score to identify true fraud risk categorically underperforms. BustOut ScoreSM or other fraud risk scores have a much higher ability to assess true fraud risk. Second is the need to for a uniform first-party fraud bust-out definition so information can be better shared. By the end of the session, I was struck by how much diversity there is among institutions and their approach to combating fraud. From capturing losses to working cases, the approaches were as unique as the individuals in attendance This session was both educational and inspirational. I am optimistic about the future and look forward to seeing how our clients continue to fight first-party fraud.

James W. Paulsen, Chief Investment Strategist for Wells Capital Management, kicked off the second day of Experian’s Vision 2016, sharing his perspective on the state of the economy and what the future holds for consumers and businesses alike. Paulsen joked this has been “the most successful, disappointing recovery we’ve ever had.” While media and lenders project fear for a coming recession, Paulsen stated it is important to note we are in the 8th year of recovery in the U.S., the third longest in U.S. history, with all signs pointing to this recovery extending for years to come. Based on his indicators – leverage, restored household strength, housing, capital spending and better global growth – there is still capacity to grow. He places recession risk at 20 to 25 percent – and only quotes those numbers due the length of the recovery thus far. “What is the fascination with crisis policies when there is no crisis,” asks Paulsen. “I think we have a good chance of being in the longest recovery in U.S. history.” Other noteworthy topics of the day: Fraud prevention Fraud prevention continues to be a hot topic at this year’s conference. Whether it’s looking at current fraud challenges, such as call-center fraud, or looking to future-proof an organization’s fraud prevention techniques, the need for flexible and innovative strategies is clear. With fraudsters being quick, and regularly ahead of the technology fighting them, the need to easily implement new tools is fundamental for you to protect your businesses and customers. More on Regulatory The Military Lending Act has been enhanced over the past year to strengthen protections for military consumers, and lenders must be ready to meet updated regulations by fall 2016. With 1.46 million active personnel in the U.S., all lenders are working to update processes and documentation associated with how they serve this audience. Alternative Data What is it? How can it be used? And most importantly, can this data predict a consumer’s credit worthiness? Experian is an advocate for getting more entities to report different types of credit data including utility payments, mobile phone data, rental payments and cable payments. Additionally, alternative data can be sourced from prepaid data, liquid assets, full file public records, DDA data, bill payment, check cashing, education data, payroll data and subscription data. Collectively, lenders desire to assess someone’s stability, ability to pay and willingness to repay. If alternative data can answer those questions, it should be considered in order to score more of the U.S. population. Financial Health The Center for Financial Services Innovation revealed insights into the state of American’s financial health. According to a study they conducted, 57 percent of Americans are not financially healthy, which equates to about 138 million people. As they continue to place more metrics around defining financial health, the center has landed on four components: how people plan, spend, save and borrow. And if you think income is a primary factor, think again. One-third of Americans making more than $60k a year are not healthy, while one-third making less than $60k a year are healthy. --- Final Vision 2016 breakouts, as well as a keynote from entertainer Jay Leno, will be delivered on Wednesday.

It’s impossible to capture all of the insights and learnings of 36 breakout sessions and several keynote addresses in one post, but let’s summarize a few of the highlights from the first day of Vision 2016. 1. Who better to speak about the state of our country, specifically some of the threats we are facing than Leon Panetta, former Secretary of Defense and Director of the CIA. While we are at a critical crossroads in the United States, there is room for optimism and his hope that we can be an America in Renaissance. 2. Alex Lintner, Experian President of Consumer Information Services, conveyed how the consumer world has evolved, in large part due to technology: 67 percent of consumers made purchases across multiple channels in the last six months. More than 88M U.S. consumers use their smartphone to do some form of banking. 68 percent of Millennials believe within five years the way we access money will be totally different. 3. Peter Renton of Lend Academy spoke on the future of Online Marketplace Lending, revealing: Banks are recognizing that this industry provides them with a great opportunity and many are partnering with Online Marketplace Lenders to enter the space. Millennials are not the largest consumers in this space today, but they will be in the future. Sustained growth will be key for this industry. The largest platforms have everything they need in place to endure – even through an economic downturn.In other words, Online Marketplace Lenders are here to stay. 4. Tom King, Experian’s Chief Information Security Officer, addressed the crowds on how the world of information security is growing increasingly complex. There are 1.9 million records compromised every day, and sadly that number is expected to rise. What can businesses do? “We need to make it easier to make the bad guys go somewhere else,” says King. 5. Look at how the housing market has changed from just a few years ago: Inventory continues to be extraordinarily lean. Why? New home building continues to run at recession levels. And, 8.5 percent of homeowners are still underwater on their mortgage, preventing them from placing it on the market. In the world of single-family home originations, 2016 projections show that there will be more purchases, less refinancing and less volume. We may see further growth in HELOC’s. With a dwindling number of mortgages benefiting from refinancing, and with rising interest rates, a HELOC may potentially be the cheapest and easiest way to tap equity. 6. As organizations balance business needs with increasing fraud threats, the important thing to remember is that the customer experience will trump everything else. Top fraud threats in 2015 included: Card Not Present (CNP) First Party Fraud/Synthetic ID Application Fraud Mobile Payment/Deposit Fraud Cross-Channel FraudSo what do the experts believe is essential to fraud prevention in the future? Big Data with smart analytics. 7. The need for Identity Relationship Management can be seen by the dichotomy of “99 percent of companies think having a clear picture of their customers is important for their business; yet only 24 percent actually think they achieve this ideal.” Connecting identities throughout the customer lifecycle is critical to bridging this gap. 8. New technologies continue to bring new challenges to fraud prevention. We’ve seen that post-EMV fraud is moving “upstream” as fraudsters: Apply for new credit cards using stolen ID’s. Provision stolen cards into mobile wallet. Gain access to accounts to make purchases.Then, fraudsters are open to use these new cards everywhere. 9. Several speakers addressed the ever-changing regulatory environment. The Telephone Consumer Protection Act (TCPA) litigation is up 30 percent since the last year. Regulators are increasingly taking notice of Online Marketplace Lenders. It’s critical to consider regulatory requirements when building risk models and implementing business policies. 10. Hispanics and Millennials are a force to be reckoned with, so pay attention: Millennials will be 81 million strong by 2036, and Hispanics are projected to be 133 million strong by 2050. Significant factors for home purchase likelihood for both groups include VantageScore® credit score, age, student debt, credit card debt, auto loans, income, marital status and housing prices. More great insights from Vision coming your way tomorrow!

Four Experian employees reflect on financial lessons and challenges learned during their time served in the military. Pedro Martinez, based at Camp Lejeune in North Carolina, was earning a monthly salary of just $680 as a Private First Class for the Marine Corps. in 1988. Winter was nearing, and since he was living off base, he needed a heater. “I was able to purchase one with ‘easy credit’ for $15 per month, for 18 months,” said Martinez, now living in Costa Rica. “I ended up paying a lot more than driving to Kmart and getting one there if I had the money. But for the purchase I was able to make at the time, I had to finance it, and I remember the interest rate was almost 40 percent.” Fast forward decades later, and Martinez recalls those same “easy credits” and payday loans surround local bases. Advance paycheck services offering rates of 30 percent and beyond for brief, 15-day cycles abound. While military base consumer advisors can encourage personnel to steer clear, more formal protections have been lacking. Until now. “The Military Lending Act is definitely a great measure to assure a fair consumer treatment, regulate high-interest rates, and safeguard families from going bankrupt,” said Martinez. No one can tell the stories of military life better than those who have lived it. They understand the training, sacrifices, day-to-day grind as well as the experiences of managing life on base and far from home. Financial education is lacking among all consumer groups in the country, and it is easy for a few credit mishaps to take individuals to a place where they soon find themselves struggling to get out of debt and obtain affordable credit. “I witnessed countless friends in the military finance furniture, receive cash advances and take out loans on their cars, which ultimately hurt them financially,” said Marshall Abercrombie, who served five years as a Navy Corpsman with the Marines. “Unfortunately, there are more title loans, cash advance and furniture leasing companies found within military towns compared to legitimate financial institutions. So, when you combine word-of-mouth, inexperience and easy access you end up with necessary legislature like the Military Lending Act.” Abercrombie, who currently resides in the southeast, claims his first “solo” experience with a financial institution saved him from falling down a bad path. “I can remember gripping my diploma thinking ‘now what am I going to do with all this money I’m about to start making?’” said Abercrombie. “Fortunate for me I was immediately greeted by a very eager representative of Armed Forces Bank. Despite being only 19 years old, looking back it’s apparent how much opportunity someone like me represented to a bank given I now had a government job that required I set up auto-deposit for future paychecks.” Especially for those military members sent overseas, opportunities and challenges can be unique. Michael Kilander, now a Southern California resident, was deployed overseas in Germany in the early 90s with his wife and ran into trouble with a large U.S. bank. “We had a credit card that we fell a month behind in paying,” says Kilander. “We had the money each time but did not receive the statement/ bill until a week after the due date. The military mail system took a great deal of time, particularly if you lived off base in the local Germany economy, as we did. We asked if the bank could mail the bill a little earlier, but they refused and were uninterested in the challenges of the APO system. Consequently we had to keep track of the amount spend on the card and estimate the likely charges and pay before we received the bill. We switched cards a few months later.” Raymond Reed, who enlisted with the Navy out of high school, was luckily advised by his parents to join a military credit union. “I did not realize I needed credit, and assumed credit was only offered to those with savings,” said Reed. “During my Navy tour, I joined a military credit union and since I did not have standard expenses, other than car insurance, which was covered by my paychecks. At the end of my tour, I saved and paid cash for my motorcycle, as I was accustomed to since I had a nice savings established.” The stories of stresses and opportunities surrounding military and credit are diverse and widespread, but the positive news is updated regulations will add increased protections. Learn more about the Servicemembers Civil Relief Act and now enhanced Military Lending Act to understand the varying protections, as well as discover how financial institutions can comply and best support military credit consumers and their families.

Television had its Twilight Zone, the Emmy-winning anthology series featuring tales rich in fantasy, morality and irony. Today's economy has its own Twilight Zone. It lies between the legitimate economy with its weekly paychecks, W2 forms and 401(K) plans, and the underground economy with its unreported, all-cash transactions. Call them "The Unbanked." Call them "The Credit Invisibles." Whatever label you choose, these men and women -- who number in the millions - want access to credit, but can’t be easily accessed with traditional credit models, and they lack a smooth on-ramp to grow in the credit universe. How a Worker Becomes "Credit Invisible" America's "credit invisibles" tend to be minimum- or low-wage workers. They exist in virtually every industry, although they tend to be concentrated in agriculture, food service, construction and manufacturing. Some work full-time for a single employer, while others work part-time or on a gig-by-gig basis. The FDIC estimates some 10 million Americans currently fit the definition of unbanked, while an additional 28.4 million are underbanked. Instead of traditional banks, this population tends to use the services of private check-cashing services and payday lenders for their financial services, which is not always advantageous for the consumer with these services’ sizeable expenses and transaction fees. The Payroll Card Alternative Recognizing the perils inherent in the current system, a number of companies have developed solutions to help those individuals who cannot and will not establish traditional checking and savings accounts. SOLE® Financial, a financial services company headquartered in Portland, Ore, offers the SOLE Visa® Payroll Card, allowing employees to enjoy the benefits associated with direct deposit checking accounts without the costs and restrictions traditional banks often impose. "From a payroll standpoint, paycards function just like bank accounts,” explained Taylor Ellsworth, content marketing manager for SOLE Financial. “The transfer happens on the exact same timeline as the paychecks that employers deposit to traditional bank accounts.” Additionally, any bill from a vendor that accepts electronic payments - either online or with a card number over the phone - can accept payments from the SOLE paycard. "For bills like rent, which sometimes can only be paid with a check or money order, cardholders can log in and use the bill pay option for $1 per bill to have a check issued to their landlord -- or any other recipient -- from their account,” said Ellsworth. Helping Credit Invisibles Build Personal Credit Files Another way companies are helping credit invisibles become visible is by considering non-retail payments, such as payments to utility companies, as part of a personal payment history. Traditionally payments to gas, electric, telephone, cable and other household service providers are generally not being reported unless the consumer is severely delinquent and thus on-time payment history is not included in credit scores. Experian recently investigated how including payments to energy utilities could affect men and women with "thin-file" credit portfolios. The subprime and nonprime consumers in the study received the greatest positive score impact, with 95 percent of subprime consumers and 75 percent of nonprime consumers experiencing a positive score change. A resounding 82 percent of subprime consumers in the study received a positive score impact of 11 points or more. The average VantageScore® credit score change for all participants was an increase of 28 points. Experian concluded, "positive energy-utility reporting presents an opportunity for energy companies to play a key role in helping their consumers build credit history. The ability for many of these consumers to become credit-scoreable, build a more robust credit file and potentially migrate to a better risk segment simply by paying their energy bills on time each month is powerful and represents an opportunity for positive change that should be not overlooked." Conclusion With income inequality growing, there is an increasing pressure to find ways to improve the prospects of the tens of millions of Americans who live on the farthest edges of the American economy. New technologies and ways of looking at credit can offer the unbanked and the under-banked ways to improve their economic situation and move closer to the mainstream. By bringing these millions into the light, those who issue and evaluate credit will create millions of new customers who can, in turn, add new energy to the American economy.

The numbers are staggering: more than $1.2 trillion in outstanding student loan debt, 40 million borrowers, and an average balance of $29,000. In fact, a recent Experian study revealed consumer debt is decreasing in every major consumer lending category with the exception of student loans. Student loans have increased by 84 percent since the recession (from 2008 to 2014) and surpassed home equity loans, home-equity lines of credit (HELOC), credit card debt and automotive debt. While the student loan issue has been looming for years, the magnitude is now taking center stage with each 2016 presidential candidate weighing in on solutions. In an effort to provide deeper insights into the student debt universe, Experian’s Kelley Motley and Holly Deason will share a new analysis at Vision 2016 in a session titled, Get educated – a study in the student lending marketplace. They will be joined by Gordon Cameron, executive vice president of PNC. Among the findings they will share include a snapshot of consumers with student loans from three time periods – Pre-recession (December 2007), Recession (December 2009) and Post-Recession/Current (December 2015). At each of these time periods, they will reveal trends around outstanding debt, delinquencies, originations, and also a compare how consumers with student loans rank when it comes to Vantage Score distribution. Finally, their data will explore opportunities for consolidation, showing segments that might be best suited for receiving offers from financial institutions based on Vantage Score, debt and total number of trades. Click here to learn more about Vision 2016 and the session on student loans.

Whether its new regulations and enforcement actions from the Consumer Financial Protection Bureau or emerging legislation in Congress, the public policy environment for consumer and commercial credit is dynamic and increasingly complex. If you are interested to learn more about how to navigate an increasingly choppy regulatory environment, consider joining a breakout session at Experian’s Vision 2016 Conference that I will be moderating. I’ll be joined by several experts and practitioners, including: John Bottega, Enterprise Data Management Conor French, Funding Circle Troy Dennis, TD Bank Don Taylor, President, Automated Collection Services During our session, you’ll learn about some of the most trying regulatory issues confronting the consumer and commercial credit ecosystem. Most importantly, the session will look at how to turn potential challenges into opportunities. This includes learning how to incorporate new alternative data sets into credit scoring models while still ensuring compliance with existing fair lending laws. We’ll also take a deep dive into some of the coming changes to debt collection practices as a result of the CFPB’s highly anticipated rulemaking. Finally, the panel will take a close look at the challenges of online marketplace lenders and some of the mounting regulations facing small business lenders. Learn more about Vision 2016 and how to register for the May conference.

Ensuring the quality of reported consumer credit data is a top priority for regulators, credit bureaus and consumers, and has increasingly become a frequent headline in press outlets when consumers find their data is not accurate. Think of any big financial milestone moment – securing a mortgage loan, auto loan, student loan, obtaining low-interest rate interest credit cards or even getting a job. These important transactions can all be derailed with an unfavorable and inaccurate credit report, causing consumers to hit social media, the press and regulatory entities to vent it out. Add in the laws and increased scrutiny from the Consumer Financial Protection Bureau (CFPB), and Federal Trade Commission (FTC) and it is clear data furnishers are seeking ways to manage their data in more effective ways. At Vision 2016, I am hosting a session, Achievements in data reporting accuracy – maximizing data quality across your organization, with several panel guests willing to share their journeys and learnings attached to the topic of data accuracy. Our diverse panel features leaders from varying industries: Jodi Cook, DriveTime Alissa Hess, USAA Bank Tom Danchik, Citi Julie Moroschan, Experian Each will speak to how they’ve overcome challenges to introduce a data quality program into their respective organizations, as well as best practices around assessing, monitoring and correcting credit reporting issues. One speaker will even touch on the challenging topic of securing funding for a data quality program, considering budgets are most often allocated to strategies, products and marketing directly tied to driving revenue. All lenders are advised to maintain a full 360-degree view of data reporting, from raw data submissions to the consumer credit profile. Better data input equals fewer inaccuracies, and an overarching data integrity program, can deliver a comprehensive view that satisfies regulators, improves the customer experience and provides better insight for internal decision making. To learn more about implementing a data quality plan for your organization, check out Vision 2016.

April is Financial Literacy Month, a special window of time dedicated to educating Americans about money management. But as stats and studies reveal, it might be wise to spend every month shining some attention on financial education, an area so many struggle to understand. Obviously no one wants to talk money day in and day out. It can be complicated, make us feel bad and serve as a source of stress. But as the saying goes, information is power. Over the years, Experian has worked to understand the country’s state of credit. Which states sport higher scores? Which states struggle? How do people pay down their debts? And what are the triggers for when accounts trail into collections? In the consumer space especially, we’ve surveyed individuals about how they feel about their own credit as it pertains to a number of different variables and life stages. Home Buying: 34% of future home buyers say their credit might hurt their ability to purchase a home 45% of future home buyers delayed a purchase to improve their credit to get better interest rates Holiday Shopping: 10% of consumers and 18% of millennials say holiday shopping has negatively affected their credit score Newlywed Life: 60% believe it is important for their future spouse to have a good credit score 39% say their spouse’s credit score or their credit score has been a source of stress in their marriage 35% of newlyweds believe they are “very knowledgeable” regarding credit scores and reports And let’s not forget Millennials: 71% of millennials believe they are knowledgeable when it comes to credit, yet: millennials overestimate their credit score by 29 points 32% do not know their credit score 61% check their credit report less than every 3 months 57% feel like the odds are stacked against them when it comes to finances and 59% feel like they are “going it alone” when it comes to finances The message is clear. Finances are simply a part of life, but can obviously serve as a source of stress. Establishing and growing credit often starts at a young age, and runs through every major life event. Historically, high school is where the bulk of financial literacy programs have targeted their efforts. But even older adults, who have arguably learned something about personal finances by managing their own, could stand a refresher on topics ranging from refinancing to retirement to reverse mortgages. Over the next month, Experian will touch on several timely financial education topics, including highlighting the top credit questions asked, the future of financial education in the social media space, investing in retirement, ways to teach your kids about money, and how to find a legit credit counselor. But Experian explores financial education topics weekly too, committed to providing consistent resources to both businesses and consumers via weekly tweet chats, blog posts and live discussions on periscope. There is always an opportunity to learn more about finances. Throughout the year, different issues pop up, and milestone moments mean we need to brush up on the latest ways to spend and save. It’s nice so many financial institutions make a special point to highlight financial education in April, but hopefully consumers and lenders alike continue to dedicate time to this important topic every month. Managing money is a lifelong task, so tips and insights are always welcome. Right? Check out the wealth of resources and pass it on. For a complete picture of consumer credit trends from Experian's database of over 230 million consumers, purchase the Experian Market Intelligence Brief.

Whether it is an online marketplace lender offering to refinance the student loan debt of a recent college graduate or an online small-business lender providing an entrepreneur with a loan when no one else will, there is no doubt innovation in the online lending sector is changing how Americans gain access to credit. This expanding market segment takes great pride in using “next-generation” underwriting and credit scoring risk models. In particular, many online lenders are incorporating noncredit information such as income, education history (i.e., type of degree and college), professional licenses and consumer-supplied information in an effort to strike the right balance between properly assessing credit risk and serving consumers typically shunned by traditional lenders because of a thin credit history. Regulatory concerns The exponential growth of the online lending sector has caught the attention of regulators — such as the U.S. Treasury Department, the Federal Deposit Insurance Corporation, Congress and the California Business Development Office — who are interested in learning more about how online marketplace lenders are assessing the credit risk of consumers and small businesses. At least one official, Antonio Weiss, a counselor to the Treasury secretary, has publicly raised concerns about the use of so-called nontraditional data in the underwriting process, particularly data gleaned from social media accounts. Weiss said that “just because a credit decision is made by an algorithm, doesn’t mean it is fair,” citing the need for lenders to be aware of compliance with fair lending obligations when integrating nontraditional credit data. Innovative and “tried and true” are not mutually exclusive Some have suggested the only way to assuage regulatory concerns and control risk is by using tried-and-true legacy credit risk models. The fact is, however, online marketplace lenders can — and should — continue to push the envelope on innovative underwriting and business models, so long as these models properly gauge credit risk and ensure compliance with fair lending rules. It’s not a simple either-or scenario. Lenders always must ensure their scoring analytics are based upon predictive and accurate data. That’s why lenders historically have relied on credit history, which is based upon data consumers can dispute using their rights under the Fair Credit Reporting Act. Statistically sound and validated scores protect consumers from discrimination and lenders from disparate impact claims under the Equal Credit Opportunity Act. The Office of the Comptroller of the Currency guidance on model risk management is an example of regulators’ focus on holding responsible the entities they oversee for the validation, testing and accuracy of their models. Marketplace lenders who want to push the limit can look to credit scoring models now being used in the marketplace without negatively impacting credit quality or raising fair lending risk. For example, VantageScore® allows for the scoring of 30 million to 35 million more people who currently are unscoreable under legacy credit score models. The VantageScore® credit score does this by using a broader, deeper set of credit file data and more advanced modeling techniques. This allows the VantageScore® credit score model to capture unique consumer behaviors more accurately. In conclusion, online marketplace lenders should continue innovating with their own “secret sauce” and custom decisioning systems that may include a mix of noncredit factors. But they also can stay ahead of the curve by relying on innovative “tried-and-true” credit score models like the VantageScore® credit score model. These models incorporate the best of both worlds by leaning on innovative scoring analytics that are more inclusive, while providing marketplace lenders with assurances the decisioning is both statistically sound and compliant with fair lending laws. VantageScore® is a registered trademark of VantageScore Solutions, LLC.