Tag: credit lending

Mid-sized banks are large enough to pursue ambitious growth strategies, like expanding loan portfolios or entering new markets, but not so large that they can withstand major credit losses without consequence. So how do lending organizations manage their credit risk strategies to grow without taking on more risk than they can handle?

Credit decisioning has traditionally relied on static data like credit bureau scores, income statements, and past repayment history. As financial behavior becomes more dynamic and consumer expectations shift toward instant decisions, real-time data is emerging as a powerful tool in reshaping how lenders assess risk.

This article was updated on February 13, 2024. Traditional credit data has long been a reliable source for measuring consumers' creditworthiness. While that's not changing, new types of alternative credit data are giving lenders a more complete picture of consumers' financial health. With supplemental data, lenders can better serve a wider variety of consumers and increase financial access and opportunities in their communities. What is alternative credit data? Alternative credit data, also known as expanded FCRA-regulated data, is data that can help you evaluate creditworthiness but isn't included in traditional credit reports.1 To comply with the Fair Credit Reporting Act (FCRA), alternative credit data must be displayable, disputable and correctable. Lenders are increasingly turning to new types and sources of data as the use of alternative credit data becomes the norm in underwriting. Today, lenders commonly use one or more of the following: Alternative financial services data: Alternative financial services (AFS) credit data can include information on consumers' use of small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Consumer permission data: With a consumer's permission, you can get transactional and account-level data from financial accounts to better assess income, assets and cash flow. The access can also give insight into payment history on non-traditional accounts, such as utilities, cell phone and streaming services. Rental payment history: Property managers, electronic rent payment services and rent collection companies can share information on consumers' rent payment history and lease terms. Full-file public records: Local- and state-level public records can tell you about a consumer's professional and occupational licenses, education, property deeds and address history. Buy Now Pay Later (BNPL) data: BNPL tradeline and account data can show you payment and return histories, along with upcoming scheduled payments. It may become even more important as consumers increasingly use this new type of point-of-sale financing. By gathering more information, you can get a deeper understanding of consumers' creditworthiness and expand your lending universe. From market segmentation to fraud prevention and collections, you can also use alternative credit data throughout the customer lifecycle. READ: 2023 State of Alternative Credit Data Report Challenges in underwriting today While unemployment rates are down, high inflation, rising interest rates and uncertainty about the economy are impacting consumer sentiment and the lending environment.2 Additionally, lenders may need to shift their underwriting approaches as pandemic-related assistance programs and loan accommodations end. Lenders may want to tighten their credit criteria. But, at the same time, consumers are becoming accustomed to streamlined application processes and responses. A slow manual review could lead to losing customers. Alternative credit data can help you more accurately assess consumers' creditworthiness, which may make it easier to identify high-risk applicants and find the hidden gems within medium-risk segments. Layering traditional and alternative credit data with the latest approaches to model building, such as using artificial intelligence, can also help you implement precise and predictive underwriting strategies. Benefits of using alternative data for credit underwriting Using alternative data for credit underwriting — along with custom credit attributes and automation — is the modern approach to a risk-based credit approval strategy. The result can offer: A greater view of consumer creditworthiness: Personal cash flow data and a consumer's history of making (or missing) payments that don't appear on traditional credit reports can give you a better understanding of their financial position. Improve speed and accuracy of credit decisions: The expanded view helps you create a more efficient underwriting process. Automated underwriting tools can incorporate alternative credit data and attributes with meaningful results. One lender, Atlas Credit, worked with Experian to create a custom model that incorporated alternative credit data and nearly doubled its approvals while reducing risk by 15 to 20 percent.3 Increase financial inclusion: There are 28 million American adults who don't have a mainstream credit file and 21 million who aren't scoreable by conventional scoring models.4 With alternative credit data, you may be able to more accurately assess the creditworthiness of adults who would otherwise be deemed thin file or unscorable. Broadening your pool of applications while appropriately managing risk is a measurable success. What Experian builds and offers Experian is continually expanding access to expanded FCRA-regulated data. Our Experian RentBureau and Clarity Services (the leading source of alternative financial credit data) have long given lenders a more complete picture of consumers' financial situation. Experian also helps lenders effectively use these new types of data. You can also incorporate the data into your proprietary marketing, lending and collections strategies. Experian is also using alternative credit data for credit scoring. The Lift Premium™ model can score 96 percent of U.S. adults — compared to the 81 percent that conventional models can score using traditional data.5 The bottom line Lenders have been testing and using alternative credit data for years, but its use in underwriting may become even more important as they need to respond to changing consumer expectations and economic uncertainty. Experian is supporting this innovation by expanding access to alternative data sources and helping lenders understand how to best use and implement alternative credit data in their lending strategies. Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply and can be used interchangeably. 2Experian (2024). State of the Economy Report 3Experian (2020). OneAZ Credit Union [Case Study] 4Oliver Wyman (2022). Financial Inclusion and Access to Credit [White Paper] 5Ibid.

This article was updated on February 12, 2024. The Buy Now, Pay Later (BNPL) space has grown massively over the last few years. But with rapid growth comes an increased risk of fraud, making "Buy Now, Pay Never" a crucial fraud threat to watch out for in 2024 and beyond. What is BNPL? BNPL, a type of short-term financing, has been around for decades in different forms. It's attractive to consumers because it offers the option to split up a specific purchase into installments rather than paying the full total upfront. The modern form of BNPL typically offers four installments, with the first payment at the time of purchase, as well as 0% APR and no hidden fees. According to an Experian survey, consumers cited managing spending (34%), convenience (31%), and avoiding interest payments (23%) as main reasons for choosing BNPL. Participating retailers generally offer BNPL at point-of-sale, making it easy for customers to opt-in and get instantly approved. The customer then makes a down payment and pays off the installments from their preferred account. BNPL is on the rise The fintech and online-payment-driven world is seeing a rise in the popularity of BNPL. According to Experian research, 3 in 4 consumers have used BNPL in 2023, with 11% using BNPL weekly to make purchases. The interest in BNPL also spans generations — 36% of Gen Z, 43% of Millennials, 32% of Gen X, and 12% of Baby Boomers have used this payment method. The risks of BNPL While BNPL is a convenient, easy way for consumers to plan for their purchases, experts warn that with lax checkout and identity verification processes it is a target for digital fraud. Experian predicts an uptick in three primary risks for BNPL providers and their customers: identity theft, first-party fraud, and synthetic identity fraud. WATCH: Fraud and Identity Challenges for Fintechs Victims of identity theft can be hit with charges from BNPL providers for products they have never purchased. First-party and synthetic identity risks will emerge as a shopper's buying power grows and the temptation to abandon repayment increases. Fraudsters may use their own or fabricated identities to make purchases with no intent to repay. This leaves the BNPL provider at the risk of unrecoverable monetary losses and can impact the business' risk tolerance, causing them to narrow their lending band and miss out on properly verified consumers. An additional risk lies with fraudsters who may leverage account takeover to gain access to a legitimate user's account and payment information to make unauthorized purchases. READ: Payment Fraud Detection and Prevention: What You Need to Know Mitigating BNPL risks Luckily, there are predictive credit, identity verification, and fraud prevention tools available to help businesses minimize the risks associated with BNPL. Paired with the right data, these tools can give businesses a comprehensive view of consumer payments, including the number of outstanding BNPL loans, total BNPL loan amounts, and BNPL payment status, as well as helping to detect and apply the relevant treatment to different types of fraud. By accurately identifying customers and assessing risk in real-time, businesses can make confident lending and fraud prevention decisions. To learn more about how Experian is enabling the protection of consumer credit scores, better risk assessments, and more inclusive lending, visit us or request a call. And keep an eye out for additional in-depth explorations of our Future of Fraud Forecast. Learn more Future of Fraud Forecast

Credit portfolio management has often involved navigating uncertainty, but some periods are more extreme than others. With the right data and analytics you can gain deeper insight into financial behaviors and risk to make better decisions and drive profitable growth. Along with access to an increasing amount of data, advanced analytics can help lenders more accurately: Forecast losses under different economic scenarios to estimate liquidity requirements. Identify fraud by detecting behaviors that could indicate identity theft, account takeover fraud, first-party or synthetic identity fraud. Incorporate real-time and alternative data,1 such as cash flow transaction data and specialty bureau data, in decisioning and scoring to accurately assess creditworthiness and expand your lending pool without taking on undue risk. Precisely segment consumers using internal and external data to increase automation during underwriting and identify cross-sell opportunities. Improve collections using AI-driven strategies and automated debt collection software to enhance operations and increase recovery rates. It’s imperative to take a proactive approach to portfolio monitoring. Monthly portfolio reviews with bureau scores, credit attributes and specialized scores — and using the results to manage credit lines and loan terms — are critical during volatile times. View our interactive e-book for the latest economic and consumer trends and learn how to set your portfolio up to succeed in any economic cycle. Download e-book 1"Alternative credit data" refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “expanded FCRA data" may also apply in this instance, and both can be used interchangeably.

Experian recently attended Fintech Nexus USA, formally known as LendIt Fintech USA, the leading event for innovation in financial services. The event was held at the Javits Center in New York City on May 25-26. This year’s event housed over 4,000 attendees, 350 speakers and 225 sponsors. Experian was a proud platinum sponsor and participated in two expert sessions. Day one Gasan Awad, Product Management Vice President for Experian Fraud and Analytics, led the session, “Frictionless Fraud Prevention: Fintech’s Balancing Act.” Gasan was joined by Ibo Dusi, Chief Risk Officer for Revolut, and Ashish Gupta, Chief Risk Officer for LendingPoint, to discuss the growing fraud landscape. “ Fraud is not slowing down; it is getting more complex as customers continue to grow their online and digital usage.” Gasan Award There has been $56 billion in identity fraud losses since 2020, $13 billion stemmed from traditional identity fraud and $43 billion from identity fraud scams. 53% of consumers say security is the most important aspect of their online experience. During the session, our experts delved into important questions, including: What fraud and identity-proofing strategies should you consider to prevent sophisticated attacks and balance ease of interactions? How do you detect fraudsters without disrupting the customer experience? Want more insight? Access the discussion here. Learn more about how Experian supports fintechs by visiting our fintech resources page, and how we’re helping businesses of all types stay guarded against fraud with our fraud prevention solutions. Day two Greg Wright, Executive Vice President and Chief Product Officer for Experian, joined Afterpay, Sunbit and Jifiti in the session, “Reconciling Responsible Buy Now Pay Later (BNPL) with the Need for Access.” BNPL industry fast facts: Last year in the U.S., 45 million Americans used BNPL. The number of U.S. users has grown 300% since 2018. Spending in the U.S. was $20.8B in 2021 and is forecasted to grow globally to $1T by 2025. Real-time data is critical for the BNPL industry. Greg provided insight into what Experian is doing to incorporate BNPL data into the lending ecosystem. Through The Buy Now Pay Later Bureau™, Experian plans to bring transparency to the BNPL and financial services industries. We are currently working with large BNPLs to support data furnishing of BNPL tradelines to the new bureau. “We figured out a way to work with the BNPL clients to bring BNPL data into the lending ecosystem to where it does not have an immediate impact on your credit score just because you chose to use a BNPL option rather than a credit card,” said Greg Wright. Typical lending risk models limit the accessibility of financing, but the nature of BNPL dictates that merchants and consumers need instant decision-making. Experian's response to the BNPL finance method is a consumer-friendly solution that supports end-to-end credit risk insights and point-of-sale financing solutions that do not fit into mainstream credit processes and aren’t adequately handled by traditional credit scores. This one-of-a-kind specialty bureau allows consumers to benefit from successful repayment behaviors and lenders of all types to drive more inclusive and responsible practices. Additionally, Experian has plans to make BNPL data visible on the core consumer credit profile. Ready to learn more? Access the discussion here. Discover how you can bring transparency to the industry with The Buy Now Pay Later Bureau and power innovative fintech lending solutions. Fintech resources The Buy Now Pay Later Bureau

It's one thing to make a corporate commitment to financial inclusion, but quite another to set specific goals and measure outcomes. What goals should lenders set to make financial inclusion a reality? How can success be quantified? What actionable steps must be taken to put policy into practice? The road to financial inclusion may feel long, but this step-by-step checklist can help you measure diversity and achieve goals to become more inclusive as an organization. Step 1: Set quantifiable goals with realistic outcomes Start by defining what you plan to achieve with a financial inclusion strategy. When setting goals, Alpa Lally, Experian's Vice President of Data Business at Consumer Information Services, recommends organizations "assess the strategic opportunity at the enterprise level." "It is important that KPIs are aligned across each business unit and functional groups in order to understand the investment opportunity and what the business must achieve together," said Lally. "The key focus here is 'together', the path to financial inclusion is a journey for all groups and everyone must participate, be committed and be aligned to be successful." Figuring out your short- and long-term goals should be the first step to kickstarting a financial inclusion strategy. But equally important is driving towards outcomes. For instance, if the goal is to increase the number of loans made to previously overlooked or excluded consumers, you may want to start by examining your declination population to better understand who is being left out. Or if financial inclusion is tied to a wider strategy or vision on corporate social responsibility, your goals may include an education component, community outreach, and a re-examination of your hiring practices. No matter what KPIs you're using, here are relevant questions to ask in four key areas – which will help draw out your organizational goals and priorities: Organizational awareness: What action is your organization taking to enhance Diversity, Equity and Inclusion and embrace Corporate Social Responsibility (CSR) around financial inclusion? If you already have financial inclusion programs in place, what are the primary goals? Barriers: What barriers prevent the organization from pursuing equity, diversity and inclusion programs? Education: How do you create awareness and education around financial inclusion? Which community or third-party organizations can help you reach consumers who aren't aware of ways to access financial services? Markers of success: What benchmarks will your organization use to measure and analyze success? Step 2: Do a financial inclusion audit Before developing and implementing a robust financial inclusion program, Lally recommends conducting a financial inclusion audit – which is a "detailed assessment of where you are today, relative to the goals and results you've outlined". In a nutshell, it allows you to assess your current systems and results within your financial institution. According to Lally, a financial inclusion audit should address the following key areas: Roadmap: What are your strategic priorities and how will financial inclusion fit within them? Tracking: Track the actual volume and distribution of different underserved populations (e.g., young adults, low-income communities, immigrants, etc.) within your book of business. Look at the applications and the approval rates by segment. In addition, assess the interest rates these consumers are offered by credit score bands for each group: “Benchmarking is critical. Understanding how they compare to national averages? How do they compare to the rest of your portfolio?" said Lally. Hiring practices: Is diversity, equity and inclusion (DEI) central to your talent management strategy? Is there a link between a lack of DEI in hiring practices and the level of financial inclusion within an organization? Affordability and access: Determine if the products and services you offer are easily accessible, can be understood by a reasonable consumer and are affordable to a broad base. Internal practices: What policies exist that influence the culture and behavior of employees around financial inclusion? Partnerships: Identify outside organizations that can help you develop financial literacy programs to promote financial inclusion. Advertising: Does your advertising promote equal and diverse representation across a wide range of consumer groups? Tools to measure: Are you financially inclusive as a company? How can you improve? The Bayesian Improved Surname Geocoding (BISG) method used by the Consumer Financial Protection Bureau (CFPB) predicts the probability of an individual's race and ethnicity based on demographic information associated with the consumer's surname. Lenders can use this type of information to conduct internal audits or set benchmarks to help ensure accountability in their diversity goals. Step 3: Tap into technology New technology is emerging that gives lenders powerful tools to evaluate a wider pool of prospective borrowers while also mitigating risk. For instance, scoring models that incorporate expanded FCRA-regulated data provide greater insight into 'credit invisible' or 'unscorable' consumers because they look at a wider set of data assets (or 'alternative data'), which allows lenders to assess a larger pool of applicants. It also improves the accuracy of those scores and better assesses the creditworthiness of consumers. Consider these resources, among others: Lift Premium™: Experian estimates that lenders using Lift Premium™ can score 96 percent of U.S. adults, a vast improvement over the 81 percent that are scorable today with conventional scores relying on mainstream data. Such enhanced scores would enable six million consumers who are considered subprime today to qualify for “mainstream" (prime or near-prime) credit. Experian® RentBureau®: RentBureau collects rent payment data from landlords and management companies, which allows consumers to leverage positive rent payment history similarly to how consumers leverage consistent mortgage payments. Clarity Credit Data: Clarity Credit Data allows lenders to see how consumers use alternative financial products and examine payment behaviors that might exist outside of the traditional credit report. Clarity's expanded FCRA -regulated data provides a deeper view of the consumer, allowing lenders to identify those who may not have previously been classified as "at risk" and approve consumers that may have previously been denied using a traditional credit score. Income Verification: Consumers can grant access to their bank accounts so lenders can assess their ability to pay based on verified income and cash flow. In addition, artificial intelligence (AI) and greater automation can reduce operational costs for lenders, while increasing the affordability of financial products and services for customers. AI and machine learning (ML) can also improve risk profiling and credit decisioning by filling in some of the gaps where credit history is not available. These are just a few examples of a wide range of cutting-edge solutions and technologies that enable lenders to promote greater financial inclusion through their decisioning processes. As new solutions are introduced to the market, it is imperative that lenders look into these technologies to help grow their business. Step 4: Monitor and measure Measuring your progress on financial inclusion isn't a one-and-done proposition. After you've set your goals and created a roadmap, it's important to continue monitoring and measuring your progress. That means your performance to gauge the impact of financial inclusion at both the community and business levels. Lally recommends the following examples: Compare your lending pool to the latest population data from the United States census. Is your portfolio representative of the U.S. population or are there segments that should have greater access? How does it compare against other lenders competing in the same space? Keep in mind that it has been widely reported that certain populations were undercounted, so you may want to factor this reality into your assessments. Work to understand how traditionally underserved consumers are performing in terms of their payment behaviors, purchase patterns and delinquencies. Measure the impact of financial inclusion on your company's overall revenue growth, ROI and brand reputation. Conduct an analysis to better understand your company's brand reputation, how it's perceived across different groups and what your customers are saying. Last word Financial inclusion represents a big step towards closing the wealth gap and helping marginalized communities build generational wealth. Given the prevalence of socioeconomic and racial inequality in our country today, it's a complex issue that disproportionately impacts marginalized groups, such as consumers of color, low-income communities and immigrants. Adopting more financially inclusive practices can help improve access to credit for these groups. For financial institutions and lenders, the first step is to identify realistic, quantifiable goals. A successful financial inclusion initiative also hinges on completing a financial inclusion audit, tapping into the right technology and continually monitoring and measuring progress. "It is paramount that financial institutions hold themselves accountable and demonstrate their commitment to make these practices a part of their DNA." - Alpa Lally. Learn more

For decades, the credit scoring system has relied on traditional data that only examines existing credit captured on a credit report – such as credit utilization ratio or payment history – to calculate credit scores. But there's a problem with that approach: it leaves out a lot of consumer activity. Indeed, research shows that an estimated 28 million U.S. adults are “credit invisible," while another 21 million are “unscorable."1 But times are changing. While conventional credit scoring systems cannot generate a score for 19 percent of American adults,1 many lenders are proactively turning to expanded FCRA-regulated data – or "alternative data" – for solutions. Types of expanded FCRA-regulated data By tapping into technology, lenders can access expanded FCRA-regulated data, which offers a powerful and complete view of consumers' financial situations. Expanded public record data This can include professional and occupational licenses, property deeds and address history – a step beyond the limited public records information found in standard credit reports. Such expanded public record data is available through consumer reporting agencies and does not require the customer's permission to use it since it's a public record.1 “Experian has partnerships with these agencies and can access public records that provide insight into factors like income and housing stability, which have a direct correlation with how they'll perform," said Greg Wright, Chief Product Officer for Experian Consumer Information Services. “For example, lenders can see if a consumer's professional license is in good standing, which is a strong correlation to income stability and the ability to pay back a loan." Rental payment data Experian RentBureau draws updated rental payment history data every 24 hours from property managers, electronic rent payment services and collection companies. It can also track the frequency of address changes. “Such information can be a good indicator of risk," said Wright. “It allows lenders to make informed judgments about the financial health and positive payment history of consumers." Consumer-permissioned data With permission from consumers, lenders can look at different types of financial transactions to assess creditworthiness. Experian Boost™, for example, enables consumers to factor positive payment history, such as utilities, cell phone or even streaming services, into an Experian credit file. “Using the Experian Boost is free, and for most users, it instantly improves their credit scores," said Wright. “Overall, those 'boosted' credit scores allow for fairer decisioning and better terms from lenders – which gives customers a second chance or opportunity to receive better terms." Financial Management Insights Financial Management Insights considers data that is not captured by the traditional credit report such as cash flow and account transactions. For instance, this could include demand deposit account (DDA) data, like recurring payroll deposits, or prepaid account transactions. “Examining bank account transaction data, prepaid accounts, and cash flow data can be a good indicator of ability to pay as it helps verify income, which gives lenders insights into consumers' cash flow and ability to pay," Wright added. Clarity Credit Data With Experian's Clarity Credit Data, lenders can see how consumers use expanded FCRA-regulated data along with their related payment behavior. It provides visibility into critical non-traditional loan information, including more insights into thin-file and no-file segments allowing for a more comprehensive view of a consumer's credit history. Lift Premium™ By using multiple sources of expanded FCRA-regulated data to feed composite scores, along with artificial intelligence and machine learning, Lift Premium™ can vastly increase the number of consumers who can be scored. For example, research shows that Lift Premium™ can score 96 percent of American adults – a significant increase from the 81 percent that are scorable with conventional scores relying on only traditional credit data. Additionally, such enhanced composite scores could enable 6 million of today's subprime population to qualify for “mainstream" (prime or near-prime) credit.1 How is expanded FCRA-regulated data changing the credit scoring system? The current credit scoring system is rapidly evolving, and modern technology is making it easier for lenders to access expanded FCRA-regulated data. Indeed, this data disruption is changing lender business in a positive way. “When lenders use expanded credit data assets, they see that many unscorable and credit invisible consumers are in fact creditworthy," said Wright. “Layering in expanded FCRA-regulated data gives a clearer picture of consumers' financial situation." By expanding data assets, tapping into artificial intelligence and machine learning, lenders can now score many more consumers quickly and accurately. Moreover, forward-thinking lenders see these expanded data assets as offering a competitive edge: it's estimated that modern credit scoring methods could allow lenders to grow their pool of new customers by almost 20 percent.1 Case study: Consumer-permissioned data To date, over 9 million people have used Experian Boost. The technology uses positive payment history as a way to recognize customers who exhibit strong credit behaviors outside of traditional credit products. “Boosted" consumers were able to add on average 14 points to their FICO scores in 2022 so far, making many eligible for additional financial products with better terms or better product offerings. Active Boost consumers, post new origination performed on par or better than the average U.S. originator, consistently over time. “In other words, having this additional lens into a consumer's financial health means lenders can expand their customer base without taking on additional credit risk," explains Wright. The bottom line The world of credit data is undergoing a revolution, and forward-thinking lenders can build a sound business strategy by extending credit to consumers previously excluded from it. This not only creates a more equitable system, but also expands the customer base for proactive lenders who see its potential in growing business. Learn more 1Oliver Wyman white paper, “Financial Inclusion and Access to Credit,” January 12, 2022.

Millions of consumers lack credit history and/or have difficulty obtaining credit from mainstream financial institutions. As a result, the use of expanded Fair Credit Reporting Act (FCRA) – or alternative – data has continued to gain popularity among lenders and financial intuitions to enrich decisions across the entire lending lifecycle to meet the financial needs of their consumers. Experian presented in a recent webinar hosted by AFSA, where Alpa Lally, Vice President of Product Management, and David Elmore, Automotive Solutions Consultant, had a chance to speak about the benefits of FCRA data, and ways lenders can leverage this data to ease access to credit for “invisible” and below prime consumers. Watch the full webinar, “FCRA Data: The Key to Unlocking Credit Universe” and learn more about: How expanded FCRA data is being used throughout the lending lifecycle The benefits of leveraging FCRA data including providing a more holistic view of a consumer’s credit profile and behavior beyond financial services, leading to smarter, more informed lending decisions The lift FCRA data can offer when augmented with traditional credit data This webinar is a part of AFSA’s partner webinar series. To learn more about FCRA data and explore related content, please visit our FCRA Alternative Credit Data Resources Page. Learn More About FCRA-Alternative Credit Data

Big data is bringing changes to the way credit scores are reported and making it easier for lenders to find creditworthy consumers, and for consumers to qualify for the financing they need. Since last year’s annual report, alternative credit data1 has continued to gain in popularity. In Experian’s latest 2020 State of Alternative Credit Data report, we take a closer look at why alternative credit data is supplemental and essential to consumer lending and how it’s being adopted by both consumers and financial institutions. While the topic of alternative credit data has become more well known, its capabilities and benefits are still not widely discussed. For instance, did you know that … 89% of lenders agree that alternative credit data allows them to extend credit to more consumers. 96% of lenders agree that in times of economic stress, alternative credit data allows them to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure. 3 out of 4 consumers believe they are a better borrower than their credit score represents. Not only do consumers believe they’re more financially astute than their credit score depicts – but they’re happy to prove it, with 80% saying they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates. This year’s report provides a deeper look into lenders’ and consumers’ perceptions of alternative credit data, as well as an overview of the regulatory landscape and how alternative credit data is being used across the lending marketplace. Lenders who incorporate alternative credit data and machine learning techniques into their current processes can harness the data to unlock their portfolio’s growth potential, make smarter lending decisions and mitigate risk. Learn more in the 2020 State of Alternative Credit Data white paper. Download now

In today’s uncertain economic environment, the question of how to reduce portfolio volatility while still meeting consumers’ needs is on every lender’s mind. With more than 100 million consumers already restricted by traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By leveraging alternative credit data, you can continue to support your borrowers and expand your lending universe. In our most recent podcast, Experian’s Shawn Rife, Director of Risk Scoring and Alpa Lally, Vice President of Data Business, discuss how to enhance your portfolio analysis after an economic downturn, respond to the changing lending marketplace and drive greater access to credit for financially distressed consumers. Topics discussed, include: Making strategic, data-driven decisions across the credit lifecycle Better managing and responding to portfolio risk Predicting consumer behavior in times of extreme uncertainty Listen in on the discussion to learn more. Experian · Effective Lending in the Age of COVID-19

To combat the growing threat of synthetic identity fraud, Experian recently announced the launch of Sure ProfileTM, a revolutionary change to the credit profile that gives lenders peace of mind with Experian’s commitment to share in losses that result from an identity we’ve assured. “Experian has always been a leader in combatting fraud, and with Sure Profile, we’re proud to deliver an industry-first fraud offering integrated into the credit profile that mitigates lender losses while protecting millions of consumers’ identities,” said Robert Boxberger, President of Decision Analytics, Experian North America. Synthetic identity fraud is expected to drive $48 billion in annual online payment fraud losses by 2023. Between opportunistic fraudsters and a lack of a unified definition for synthetic identity theft it can be nearly impossible to detect—and therefore prevent—this type of fraud. This breakthrough solution provides a composite history of a consumer’s identification, public record, and credit information and determines the risk of synthetic fraud associated with that consumer. It’s not just a fraud tool, it’s a comprehensive credit profile that utilizes premium data so lenders can make positive credit decisions. Sure Profile leverages the capabilities of the Experian Ascend Identity PlatformTM and uses Experian’s industry-leading data assets and data quality to drive advanced analytics that set a higher level of protection for lenders. It’s powered by newly-developed machine learning and AI models. And it offers a streamlined approach to define and detect synthetic identities early in the originations process. Most importantly, Sure Profile differentiates between real people and potentially risky applicants so lenders can increase application approvals with greater assurance and less risk. “Experian can confidently define and help detect synthetic fraud. That's why we can help stop it,” said Craig Boundy, CEO of Experian North America. “Experian stands behind our data with assurance given to our clients. It’s better for lenders and it’s better for consumers.” Sure Profile is a complement to our robust set of identity protection and fraud management capabilities, which are designed to address fraud and identity challenges including account openings, account takeovers, e-commerce fraud and more. This first-of-its kind profile is the future of underwriting and portfolio protection and it’s here now. Read press release Learn More About Sure Profile

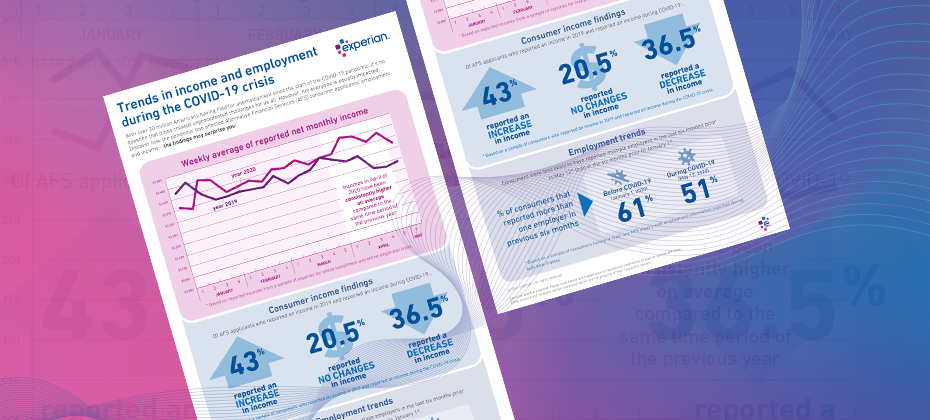

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

The current pandemic will affect the way financial institutions lend and provide credit. Shawn Rife, Experian’s Director of Product Scoring, discusses the ways that financial institutions can navigate the COVID-19 crisis. Check out what he had to say: What implications does the global pandemic have on financial institutions’ analytical needs? SR: In the customer lifecycle, there are 4 different stages: prospecting, acquisitions, portfolio management, and collections. During times of economic uncertainty, lenders typically take additional actions to ensure that there’s a first line of defense against delinquencies and payment stress. Expanding their focus to incorporate account review/portfolio management becomes particularly important. During this time, clients will be looking for leadership, early warning signs, and ways to recession-proof their portfolios (account management), while growing and maintaining their approvals in a healthy way (originations). Lenders may be well advised to delay any focus on collections, since many consumers may be facing major payment stress through no mismanagement of their own doing. Another critical component is with the rollout of government stimulus packages, which lenders can use to identify people in stress who could benefit for second chance opportunities they may not have otherwise been able to receive. As more consumers seek credit, from an analytics perspective, what considerations should financial institutions be making during this time? SR: Financial institutions should be assessing and pre-identifying situations that might place consumers in positions of elevated financial stress. That way, organizations can implement solutions to identify and help at-risk consumers before they fall delinquent. The recent Coronavirus Aid, Relief, and Economic Security Act (CARES Act) – coupled with Experian’s score treatment, are designed to protect consumers against score declines during times of crisis. Furthermore, lenders can provide forbearance and loan deferment programs to help consumers. For lenders, credit risk scores, models, and attributes are the best ways to identify – and even predict - delinquency risk. The FICO® Resilience Index can also identify consumers who are particularly susceptible to delinquency risk directly due to macroeconomic uncertainty. This gives lenders the opportunity to evaluate their portfolios for loss and connect with consumers who may be in need of further support. What is the smartest next play for financial institutions? SR: For financial institutions, the smart play is to add alternative data into their data-driven decisioning strategies as much as possible. Alternative data works to enhance your ability to see a consumer’s entire credit portfolio, which gives lenders the confidence to continue to lend – as well as the ability to track and monitor a consumer’s historical performance (which is a good indicator of whether or not a consumer has both the intention and ability to repay a loan). How will the new attribute subset list benefit financial institutions during this time? SR: Experian’s series of crisis attributes is an example of attributes that can be predictive in times of a crisis. These lists were designed to follow the 3 E’s – Expand, Enhance, and provide Ease of use. Enhance – With these attributes, lenders aren’t limited to traditional data. These attributes allow lenders to look at the entirety of a consumer’s credit or repayment behavior and use more data to make better lending decisions. This becomes crucial in a challenging environment. Expand – This data can also help lenders identify consumers who are in the market for products and services, even if there the lending criteria becomes more stringent. This can open doors and new opportunities for 40-50 million new customers, particularly ones that may not fit initial lending criteria. Ease of Use – Experian has put together the most predictive elements that can identify consumer resilience and potential financial stress in this challenging economy. Experian is committed to helping your organization during times of uncertainty. For more resources, visit our Look Ahead 2020 Hub. Learn more Shawn M. Rife, Director of Risk Scoring, Experian Consumer Information Services, North America Shawn Rife manages Experian’s credit risk scoring models, focused on empowering clients to maximize the scope and influence of their lending universe - while minimizing risk - and complying with ever-changing regulatory standards. Shawn also leads the implementation of Alternative Data within the lending environment, as well as key product implementation initiatives. Prior to Experian, Shawn held key consumer insights and predictive analytics roles for Consumer Packaged Goods and internet companies. Over his career, Shawn has focused on market segmentation, competitive research, new product development and consumer advocacy. He also holds a Master’s degree from Harvard University and a Bachelor’s degree in Political Science and Economics.

When running a credit report on a new applicant, you must ensure Fair Credit Reporting Act (FCRA) compliance before accessing, using and sharing the collected data. The Coronavirus Aid, Relief, and Economic Security (CARES) Act has impacted credit reporting under the FCRA, as has new guidance from the Consumer Financial Protection Bureau (CFPB). Recent updates include: The CARES Act amended the FCRA to require furnishers who agree to an “accommodation,”1 to report the account as current, although it is permitted to continue to report the account as delinquent if the account was delinquent before the accommodation was made. Although not legally obligated, data furnishers should continue furnishing information to the credit reporting agencies (CRAs) during the COVID-19 crisis, and make sure that information reported is complete and accurate. Below is a brief FCRA-related compliance overview2 covering various FCRA requirements3 when requesting and using consumer credit reports for an extension of credit permissible purpose. For more information regarding your responsibilities under the FCRA as a user of consumer reports, please consult your Legal Counsel and the Notice to Users of Consumer Reports: Obligations of Users Under the FCRA handbook located on our website. Before obtaining a consumer report you have… Reviewed your federal and state regulations and laws related to consumer reports, scores, decisions, etc. Made sure you have a valid permissible purpose for pulling the consumer report. Certified compliance to the CRA from which you are getting the consumer report. You have certified that you complied with all the federal and state requirements. After you take an adverse action based on a consumer report you… Provide the consumer with an oral, written or electronic notice of the adverse action. Provide written or electronic disclosure of the numerical credit score used to take the adverse action, or when providing a “risk-based pricing” notice. Provide the consumer with an oral, written or electronic notice, which includes the below information: Name, address and telephone number of CRA that supplied the report, if nationwide. A statement that the CRA did not make the adverse decision and therefore can’t explain why the decision was made. Notice of the consumer’s right to a free copy of their report from the CRA, if requested within 60 days. Notice of the consumer’s right to dispute with the CRA the accuracy or completeness of any information in a consumer report provided by the CRA. Provide the consumer with a “risk-based pricing” notice if credit was granted but on less favorable terms based on information in their consumer report. We understand how challenging it is to understand and meet all your obligations as a data furnisher – we’re here to make it a little easier. Click below to speak with a representative and gain more insight on how the CARES Act impacts FCRA reporting. Download overview Speak with a representative 1An “accommodation” is defined as “an agreement to defer one or more payments, make a partial payment, forbear any delinquent amounts, modify a loan or contract, or any other assistance or relief” granted to a consumer affected by COVID-19 during the covered period. 2This FCRA overview is not legal guidance and does not enumerate all your requirements under the FCRA as a user of consumer reports. Additionally, this FCRA Overview is not intended to provide legal advice or counsel you regarding your obligations under the FCRA or any other federal or state law or regulation. Should you have any questions about your institution’s specific obligations under the FCRA or any other federal or state law or regulation, you should consult with your Legal Counsel. 3This FCRA overview is intended to be used solely by financial service providers when extending credit to consumers and does not include all FCRA regulatory obligations. You are responsible for regulatory compliance when requesting and using consumer reports, which includes adhering to all applicable federal and state statutes and regulations and ensuring that you have the correct policies and procedures in place.