Tag: consumer lending

This article was updated on February 13, 2024. Traditional credit data has long been a reliable source for measuring consumers' creditworthiness. While that's not changing, new types of alternative credit data are giving lenders a more complete picture of consumers' financial health. With supplemental data, lenders can better serve a wider variety of consumers and increase financial access and opportunities in their communities. What is alternative credit data? Alternative credit data, also known as expanded FCRA-regulated data, is data that can help you evaluate creditworthiness but isn't included in traditional credit reports.1 To comply with the Fair Credit Reporting Act (FCRA), alternative credit data must be displayable, disputable and correctable. Lenders are increasingly turning to new types and sources of data as the use of alternative credit data becomes the norm in underwriting. Today, lenders commonly use one or more of the following: Alternative financial services data: Alternative financial services (AFS) credit data can include information on consumers' use of small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Consumer permission data: With a consumer's permission, you can get transactional and account-level data from financial accounts to better assess income, assets and cash flow. The access can also give insight into payment history on non-traditional accounts, such as utilities, cell phone and streaming services. Rental payment history: Property managers, electronic rent payment services and rent collection companies can share information on consumers' rent payment history and lease terms. Full-file public records: Local- and state-level public records can tell you about a consumer's professional and occupational licenses, education, property deeds and address history. Buy Now Pay Later (BNPL) data: BNPL tradeline and account data can show you payment and return histories, along with upcoming scheduled payments. It may become even more important as consumers increasingly use this new type of point-of-sale financing. By gathering more information, you can get a deeper understanding of consumers' creditworthiness and expand your lending universe. From market segmentation to fraud prevention and collections, you can also use alternative credit data throughout the customer lifecycle. READ: 2023 State of Alternative Credit Data Report Challenges in underwriting today While unemployment rates are down, high inflation, rising interest rates and uncertainty about the economy are impacting consumer sentiment and the lending environment.2 Additionally, lenders may need to shift their underwriting approaches as pandemic-related assistance programs and loan accommodations end. Lenders may want to tighten their credit criteria. But, at the same time, consumers are becoming accustomed to streamlined application processes and responses. A slow manual review could lead to losing customers. Alternative credit data can help you more accurately assess consumers' creditworthiness, which may make it easier to identify high-risk applicants and find the hidden gems within medium-risk segments. Layering traditional and alternative credit data with the latest approaches to model building, such as using artificial intelligence, can also help you implement precise and predictive underwriting strategies. Benefits of using alternative data for credit underwriting Using alternative data for credit underwriting — along with custom credit attributes and automation — is the modern approach to a risk-based credit approval strategy. The result can offer: A greater view of consumer creditworthiness: Personal cash flow data and a consumer's history of making (or missing) payments that don't appear on traditional credit reports can give you a better understanding of their financial position. Improve speed and accuracy of credit decisions: The expanded view helps you create a more efficient underwriting process. Automated underwriting tools can incorporate alternative credit data and attributes with meaningful results. One lender, Atlas Credit, worked with Experian to create a custom model that incorporated alternative credit data and nearly doubled its approvals while reducing risk by 15 to 20 percent.3 Increase financial inclusion: There are 28 million American adults who don't have a mainstream credit file and 21 million who aren't scoreable by conventional scoring models.4 With alternative credit data, you may be able to more accurately assess the creditworthiness of adults who would otherwise be deemed thin file or unscorable. Broadening your pool of applications while appropriately managing risk is a measurable success. What Experian builds and offers Experian is continually expanding access to expanded FCRA-regulated data. Our Experian RentBureau and Clarity Services (the leading source of alternative financial credit data) have long given lenders a more complete picture of consumers' financial situation. Experian also helps lenders effectively use these new types of data. You can also incorporate the data into your proprietary marketing, lending and collections strategies. Experian is also using alternative credit data for credit scoring. The Lift Premium™ model can score 96 percent of U.S. adults — compared to the 81 percent that conventional models can score using traditional data.5 The bottom line Lenders have been testing and using alternative credit data for years, but its use in underwriting may become even more important as they need to respond to changing consumer expectations and economic uncertainty. Experian is supporting this innovation by expanding access to alternative data sources and helping lenders understand how to best use and implement alternative credit data in their lending strategies. Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply and can be used interchangeably. 2Experian (2024). State of the Economy Report 3Experian (2020). OneAZ Credit Union [Case Study] 4Oliver Wyman (2022). Financial Inclusion and Access to Credit [White Paper] 5Ibid.

How businesses respond to economic uncertainty can determine whether they get ahead or fall behind. To better prepare for the coming months, you must remain up to date on the latest economic developments to better understand and evolve with changing consumer needs. With insight into critical macroeconomic and consumer trends, you can proactively manage your portfolio, enhance your decisioning and seize new opportunities. Grab a cup of coffee and join Experian's Shawn Rife, Client Executive, and Josee Farmer, Economic Analyst, during our fireside chat on February 16 @ 1 P.M. ET/10 A.M. PT. Our expert speakers will provide a view of the latest economic and market trends, their impact on consumers, and how financial institutions can survive and thrive. Highlights include: Macroeconomic and consumer credit trends Economic implications on consumer behavior How financial institutions can adapt Register now

Credit reports and conventional credit scores give lenders a strong starting point for evaluating applicants and managing risk. But today's competitive environment often requires deeper insights, such as credit attributes. Experian develops industry-leading credit attributes and models using traditional methods, as well as the latest techniques in machine learning, advanced analytics and alternative credit data — or expanded Fair Credit Reporting Act (FCRA)-regulated data)1 to unlock valuable consumer spending and payment information so businesses can drive better outcomes, optimize risk management and better serve consumers READ MORE: Using Alternative Credit Data for Credit Underwriting Turning credit data into digestible credit attributes Lenders rely on credit attributes — specific characteristics or variables based on the underlying data — to better understand the potentially overwhelming flow of data from traditional and non-traditional sources. However, choosing, testing, monitoring, maintaining and updating attributes can be a time- and resource-intensive process. Experian has over 45 years of experience with data analytics, modeling and helping clients develop and manage credit attributes and risk management. Currently, we offer over 4,500 attributes to lenders, including core attributes and subsets for specific industries. These are continually monitored, and new attributes are released based on consumer trends and regulatory requirements. Lenders can use these credit attributes to develop precise and explainable scoring models and strategies. As a result, they can more consistently identify qualified prospects that might otherwise be missed, set initial limits, manage credit lines, improve loyalty by applying appropriate treatments and limit credit losses. Using expanded credit data effectively Leveraging credit attributes is critical for portfolio growth, and businesses can use their expanding access to credit data and insights to improve their credit decisioning. A few examples: Spot trends in consumer behavior: Going beyond a snapshot of a credit report, Trended 3DTM attributes reveal and make it easier to understand customers' behavioral patterns. Use these insights to determine when a customer will likely revolve, transact, transfer a balance or fall into distress. Dig deeper into credit data: Making sense of vast amounts of credit report data can be difficult, but Premier AttributesSM aggregates and summarizes findings. Lenders use the 2,100-plus attributes to segment populations and define policy rules. From prospecting to collections, businesses can save time and make more informed decisions across the customer lifecycle. Get a clear and complete picture: Businesses may be able to more accurately assess and approve applicants, simply by incorporating attributes overlooked by traditional credit bureau reports into their decisioning process. Clear View AttributesTM uses data from the largest alternative financial services specialty bureau, Clarity Services, to show how customers have used non-traditional lenders, including auto title lenders, rent-to-own and small-dollar credit lenders. The additional credit attributes and analysis help lenders make more strategic approval and credit limit decisions, leading to increased customer loyalty, reduced risk and business growth. Additionally, many organizations find that using credit attributes and customized strategies can be important for measuring and reaching financial inclusion goals. Many consumers have a thin credit file (fewer than five credit accounts), don’t have a credit file or don’t have information for conventional scoring models to score them. Expanded credit data and attributes can help lenders accurately evaluate many of these consumers and remove barriers that keep them from accessing mainstream financial services. There's no time to wait Businesses can expand their customer base while reducing risk by looking beyond traditional credit bureau data and scores. Download our latest e-book on credit attributes to learn more about what Experian offers and how we can help you stay ahead of the competition. Download e-book Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.

It's one thing to make a corporate commitment to financial inclusion, but quite another to set specific goals and measure outcomes. What goals should lenders set to make financial inclusion a reality? How can success be quantified? What actionable steps must be taken to put policy into practice? The road to financial inclusion may feel long, but this step-by-step checklist can help you measure diversity and achieve goals to become more inclusive as an organization. Step 1: Set quantifiable goals with realistic outcomes Start by defining what you plan to achieve with a financial inclusion strategy. When setting goals, Alpa Lally, Experian's Vice President of Data Business at Consumer Information Services, recommends organizations "assess the strategic opportunity at the enterprise level." "It is important that KPIs are aligned across each business unit and functional groups in order to understand the investment opportunity and what the business must achieve together," said Lally. "The key focus here is 'together', the path to financial inclusion is a journey for all groups and everyone must participate, be committed and be aligned to be successful." Figuring out your short- and long-term goals should be the first step to kickstarting a financial inclusion strategy. But equally important is driving towards outcomes. For instance, if the goal is to increase the number of loans made to previously overlooked or excluded consumers, you may want to start by examining your declination population to better understand who is being left out. Or if financial inclusion is tied to a wider strategy or vision on corporate social responsibility, your goals may include an education component, community outreach, and a re-examination of your hiring practices. No matter what KPIs you're using, here are relevant questions to ask in four key areas – which will help draw out your organizational goals and priorities: Organizational awareness: What action is your organization taking to enhance Diversity, Equity and Inclusion and embrace Corporate Social Responsibility (CSR) around financial inclusion? If you already have financial inclusion programs in place, what are the primary goals? Barriers: What barriers prevent the organization from pursuing equity, diversity and inclusion programs? Education: How do you create awareness and education around financial inclusion? Which community or third-party organizations can help you reach consumers who aren't aware of ways to access financial services? Markers of success: What benchmarks will your organization use to measure and analyze success? Step 2: Do a financial inclusion audit Before developing and implementing a robust financial inclusion program, Lally recommends conducting a financial inclusion audit – which is a "detailed assessment of where you are today, relative to the goals and results you've outlined". In a nutshell, it allows you to assess your current systems and results within your financial institution. According to Lally, a financial inclusion audit should address the following key areas: Roadmap: What are your strategic priorities and how will financial inclusion fit within them? Tracking: Track the actual volume and distribution of different underserved populations (e.g., young adults, low-income communities, immigrants, etc.) within your book of business. Look at the applications and the approval rates by segment. In addition, assess the interest rates these consumers are offered by credit score bands for each group: “Benchmarking is critical. Understanding how they compare to national averages? How do they compare to the rest of your portfolio?" said Lally. Hiring practices: Is diversity, equity and inclusion (DEI) central to your talent management strategy? Is there a link between a lack of DEI in hiring practices and the level of financial inclusion within an organization? Affordability and access: Determine if the products and services you offer are easily accessible, can be understood by a reasonable consumer and are affordable to a broad base. Internal practices: What policies exist that influence the culture and behavior of employees around financial inclusion? Partnerships: Identify outside organizations that can help you develop financial literacy programs to promote financial inclusion. Advertising: Does your advertising promote equal and diverse representation across a wide range of consumer groups? Tools to measure: Are you financially inclusive as a company? How can you improve? The Bayesian Improved Surname Geocoding (BISG) method used by the Consumer Financial Protection Bureau (CFPB) predicts the probability of an individual's race and ethnicity based on demographic information associated with the consumer's surname. Lenders can use this type of information to conduct internal audits or set benchmarks to help ensure accountability in their diversity goals. Step 3: Tap into technology New technology is emerging that gives lenders powerful tools to evaluate a wider pool of prospective borrowers while also mitigating risk. For instance, scoring models that incorporate expanded FCRA-regulated data provide greater insight into 'credit invisible' or 'unscorable' consumers because they look at a wider set of data assets (or 'alternative data'), which allows lenders to assess a larger pool of applicants. It also improves the accuracy of those scores and better assesses the creditworthiness of consumers. Consider these resources, among others: Lift Premium™: Experian estimates that lenders using Lift Premium™ can score 96 percent of U.S. adults, a vast improvement over the 81 percent that are scorable today with conventional scores relying on mainstream data. Such enhanced scores would enable six million consumers who are considered subprime today to qualify for “mainstream" (prime or near-prime) credit. Experian® RentBureau®: RentBureau collects rent payment data from landlords and management companies, which allows consumers to leverage positive rent payment history similarly to how consumers leverage consistent mortgage payments. Clarity Credit Data: Clarity Credit Data allows lenders to see how consumers use alternative financial products and examine payment behaviors that might exist outside of the traditional credit report. Clarity's expanded FCRA -regulated data provides a deeper view of the consumer, allowing lenders to identify those who may not have previously been classified as "at risk" and approve consumers that may have previously been denied using a traditional credit score. Income Verification: Consumers can grant access to their bank accounts so lenders can assess their ability to pay based on verified income and cash flow. In addition, artificial intelligence (AI) and greater automation can reduce operational costs for lenders, while increasing the affordability of financial products and services for customers. AI and machine learning (ML) can also improve risk profiling and credit decisioning by filling in some of the gaps where credit history is not available. These are just a few examples of a wide range of cutting-edge solutions and technologies that enable lenders to promote greater financial inclusion through their decisioning processes. As new solutions are introduced to the market, it is imperative that lenders look into these technologies to help grow their business. Step 4: Monitor and measure Measuring your progress on financial inclusion isn't a one-and-done proposition. After you've set your goals and created a roadmap, it's important to continue monitoring and measuring your progress. That means your performance to gauge the impact of financial inclusion at both the community and business levels. Lally recommends the following examples: Compare your lending pool to the latest population data from the United States census. Is your portfolio representative of the U.S. population or are there segments that should have greater access? How does it compare against other lenders competing in the same space? Keep in mind that it has been widely reported that certain populations were undercounted, so you may want to factor this reality into your assessments. Work to understand how traditionally underserved consumers are performing in terms of their payment behaviors, purchase patterns and delinquencies. Measure the impact of financial inclusion on your company's overall revenue growth, ROI and brand reputation. Conduct an analysis to better understand your company's brand reputation, how it's perceived across different groups and what your customers are saying. Last word Financial inclusion represents a big step towards closing the wealth gap and helping marginalized communities build generational wealth. Given the prevalence of socioeconomic and racial inequality in our country today, it's a complex issue that disproportionately impacts marginalized groups, such as consumers of color, low-income communities and immigrants. Adopting more financially inclusive practices can help improve access to credit for these groups. For financial institutions and lenders, the first step is to identify realistic, quantifiable goals. A successful financial inclusion initiative also hinges on completing a financial inclusion audit, tapping into the right technology and continually monitoring and measuring progress. "It is paramount that financial institutions hold themselves accountable and demonstrate their commitment to make these practices a part of their DNA." - Alpa Lally. Learn more

For decades, the credit scoring system has relied on traditional data that only examines existing credit captured on a credit report – such as credit utilization ratio or payment history – to calculate credit scores. But there's a problem with that approach: it leaves out a lot of consumer activity. Indeed, research shows that an estimated 28 million U.S. adults are “credit invisible," while another 21 million are “unscorable."1 But times are changing. While conventional credit scoring systems cannot generate a score for 19 percent of American adults,1 many lenders are proactively turning to expanded FCRA-regulated data – or "alternative data" – for solutions. Types of expanded FCRA-regulated data By tapping into technology, lenders can access expanded FCRA-regulated data, which offers a powerful and complete view of consumers' financial situations. Expanded public record data This can include professional and occupational licenses, property deeds and address history – a step beyond the limited public records information found in standard credit reports. Such expanded public record data is available through consumer reporting agencies and does not require the customer's permission to use it since it's a public record.1 “Experian has partnerships with these agencies and can access public records that provide insight into factors like income and housing stability, which have a direct correlation with how they'll perform," said Greg Wright, Chief Product Officer for Experian Consumer Information Services. “For example, lenders can see if a consumer's professional license is in good standing, which is a strong correlation to income stability and the ability to pay back a loan." Rental payment data Experian RentBureau draws updated rental payment history data every 24 hours from property managers, electronic rent payment services and collection companies. It can also track the frequency of address changes. “Such information can be a good indicator of risk," said Wright. “It allows lenders to make informed judgments about the financial health and positive payment history of consumers." Consumer-permissioned data With permission from consumers, lenders can look at different types of financial transactions to assess creditworthiness. Experian Boost™, for example, enables consumers to factor positive payment history, such as utilities, cell phone or even streaming services, into an Experian credit file. “Using the Experian Boost is free, and for most users, it instantly improves their credit scores," said Wright. “Overall, those 'boosted' credit scores allow for fairer decisioning and better terms from lenders – which gives customers a second chance or opportunity to receive better terms." Financial Management Insights Financial Management Insights considers data that is not captured by the traditional credit report such as cash flow and account transactions. For instance, this could include demand deposit account (DDA) data, like recurring payroll deposits, or prepaid account transactions. “Examining bank account transaction data, prepaid accounts, and cash flow data can be a good indicator of ability to pay as it helps verify income, which gives lenders insights into consumers' cash flow and ability to pay," Wright added. Clarity Credit Data With Experian's Clarity Credit Data, lenders can see how consumers use expanded FCRA-regulated data along with their related payment behavior. It provides visibility into critical non-traditional loan information, including more insights into thin-file and no-file segments allowing for a more comprehensive view of a consumer's credit history. Lift Premium™ By using multiple sources of expanded FCRA-regulated data to feed composite scores, along with artificial intelligence and machine learning, Lift Premium™ can vastly increase the number of consumers who can be scored. For example, research shows that Lift Premium™ can score 96 percent of American adults – a significant increase from the 81 percent that are scorable with conventional scores relying on only traditional credit data. Additionally, such enhanced composite scores could enable 6 million of today's subprime population to qualify for “mainstream" (prime or near-prime) credit.1 How is expanded FCRA-regulated data changing the credit scoring system? The current credit scoring system is rapidly evolving, and modern technology is making it easier for lenders to access expanded FCRA-regulated data. Indeed, this data disruption is changing lender business in a positive way. “When lenders use expanded credit data assets, they see that many unscorable and credit invisible consumers are in fact creditworthy," said Wright. “Layering in expanded FCRA-regulated data gives a clearer picture of consumers' financial situation." By expanding data assets, tapping into artificial intelligence and machine learning, lenders can now score many more consumers quickly and accurately. Moreover, forward-thinking lenders see these expanded data assets as offering a competitive edge: it's estimated that modern credit scoring methods could allow lenders to grow their pool of new customers by almost 20 percent.1 Case study: Consumer-permissioned data To date, over 9 million people have used Experian Boost. The technology uses positive payment history as a way to recognize customers who exhibit strong credit behaviors outside of traditional credit products. “Boosted" consumers were able to add on average 14 points to their FICO scores in 2022 so far, making many eligible for additional financial products with better terms or better product offerings. Active Boost consumers, post new origination performed on par or better than the average U.S. originator, consistently over time. “In other words, having this additional lens into a consumer's financial health means lenders can expand their customer base without taking on additional credit risk," explains Wright. The bottom line The world of credit data is undergoing a revolution, and forward-thinking lenders can build a sound business strategy by extending credit to consumers previously excluded from it. This not only creates a more equitable system, but also expands the customer base for proactive lenders who see its potential in growing business. Learn more 1Oliver Wyman white paper, “Financial Inclusion and Access to Credit,” January 12, 2022.

Nearly 28 million American consumers are credit invisible, and another 21 million are unscorable.1 Without a credit report, lenders can’t verify their identity, making it hard for them to obtain mortgages, credit cards and other financial products and services. To top it off, these consumers are sometimes caught in cycles of predatory lending; they have trouble covering emergency expenses, are stuck with higher interest rates and must put down larger deposits. To further our mission of helping consumers gain access to fair and affordable credit, Experian recently launched Experian GOTM, a first-of-its-kind program aimed at helping credit invisibles take charge of their financial health. Supporting the underserved Experian Go makes it easy for credit invisibles and those with limited credit histories to establish, use and grow credit responsibly. After authenticating their identity, users will have their Experian credit report created and will receive educational guidance on improving their financial health, including adding bill payments (phone, utilities and streaming services) through Experian BoostTM. As of January 2022, U.S. consumers have raised their scores by over 87M total points with Boost.2 From there, they’ll receive personalized recommendations and can accept instant card offers. By leveraging Experian Go, disadvantaged consumers can quickly build credit and become scorable. Expanding your lending portfolio So, what does this mean for lenders? With the ability to increase their credit score (and access to financial literacy resources), thin-file consumers can more easily meet lending eligibility requirements. Applicants on the cusp of approval can move to higher score bands and qualify for better loan terms and conditions. The addition of expanded data can help you make a more accurate assessment of marginal consumers whose ability and willingness to pay aren’t wholly recognized by traditional data and scores. With a more holistic customer view, you can gain greater visibility and transparency around inquiry and payment behaviors to mitigate risk and improve profitability. Learn more Download white paper 1Data based on Oliver Wyman analysis using a random sample of consumers with Experian credit bureau records as of September 2020. Consumers are considered ‘credit invisible’ when they have no mainstream credit file at the credit bureaus and ‘unscorable’ when they have partial information in their mainstream credit file, but not enough to generate a conventional credit score. 2https://www.experian.com/consumer-products/score-boost.html

Experian’s Sure Profile was selected as a Platinum winner in the “Fraud and Security Innovation” category in the sixth annual Fintech & Payments awards from Juniper Research, a firm dedicated to delivering thought leadership and analysis in the Fintech and Payment industries. An innovative service in the fight against synthetic identity fraud, Sure Profile is a comprehensive credit profile that provides a composite history of a consumer’s identification, public record, and credit information in order to detect synthetic identities. It utilizes premium data to help businesses identify potential synthetic fraud threats across credit inquiries, thus allowing lenders to transact more confidently with the vast majority of legitimate consumers. “Experian has always been a leader in delivering innovative services that both combat fraud and provide identity verification and trust to lending environments. Sure Profile delivers an industry-first fraud offering—integrated directly into the credit profile—that mitigates lender losses while protecting millions of legitimate consumers’ identities,” said Keir Breitenfeld, Senior Vice President, Portfolio Marketing, Experian Decision Analytics. “In times of rapid changes to customer interactions, growth strategies, and risk management practices, it’s particularly important to focus on building tools that can help businesses make better decisions and I’m proud that Experian has again provided an instrument to enable those decisions.” To learn more about Sure Profile and how Experian is working to solve this multibillion-dollar problem, visit us or request a call. Learn more

To grow in today’s economic climate and beat the competition, financial institutions need to update their acquisition and cross-sell strategies. By doing so, they are able to drive up conversions, minimize risk, and ultimately connect consumers with the right offers at the right time. Businesses and consumers are spending more time online than ever before, with 40% of consumers increasing the number of businesses they visit online. They’ve also made it clear that they expect easy, frictionless transactions with their providers. This includes new accounts and offers of credit – creating the need for better delivery systems. Effective targeting and conversion come down to more than just direct mail and email subject lines, especially now in a volatile economy where consumers are seeking appropriate products for their current situation. Be the first to meet consumers’ needs by leveraging the freshest data, advanced analytics, and automated decision systems. For example, when a consumer tries to open a checking account, the system can initiate a “behind-the-scenes” real-time prescreen request while assessing information needed to open the deposit account. The financial institution can then see if the consumer qualifies for overdraft protection, refinancing offers, loans, credit cards, and more. By performing the pre-approval process in seconds, financial institutions can be sure that they're making the right offers to the right customer, and doing it at the right time. All of this helps to increase the offer acceptance rate, improving customer retention, and maximizing customer account life-time value. The pandemic upended a lot of the ways that your businesses run day-to-day – from where you work to how you (better) engage with customers. Arguably, some of the changes have been long overdue, particularly the acceleration to digital and better customer acquisition strategies. Ahead lies the opportunity to grow – strategies enacted now will determine the extent of that opportunity. To learn more about how Experian can help you assess your prescreen strategy and grow, contact us today. Request a call

Big data is bringing changes to the way credit scores are reported and making it easier for lenders to find creditworthy consumers, and for consumers to qualify for the financing they need. Since last year’s annual report, alternative credit data1 has continued to gain in popularity. In Experian’s latest 2020 State of Alternative Credit Data report, we take a closer look at why alternative credit data is supplemental and essential to consumer lending and how it’s being adopted by both consumers and financial institutions. While the topic of alternative credit data has become more well known, its capabilities and benefits are still not widely discussed. For instance, did you know that … 89% of lenders agree that alternative credit data allows them to extend credit to more consumers. 96% of lenders agree that in times of economic stress, alternative credit data allows them to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure. 3 out of 4 consumers believe they are a better borrower than their credit score represents. Not only do consumers believe they’re more financially astute than their credit score depicts – but they’re happy to prove it, with 80% saying they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates. This year’s report provides a deeper look into lenders’ and consumers’ perceptions of alternative credit data, as well as an overview of the regulatory landscape and how alternative credit data is being used across the lending marketplace. Lenders who incorporate alternative credit data and machine learning techniques into their current processes can harness the data to unlock their portfolio’s growth potential, make smarter lending decisions and mitigate risk. Learn more in the 2020 State of Alternative Credit Data white paper. Download now

To combat the growing threat of synthetic identity fraud, Experian recently announced the launch of Sure ProfileTM, a revolutionary change to the credit profile that gives lenders peace of mind with Experian’s commitment to share in losses that result from an identity we’ve assured. “Experian has always been a leader in combatting fraud, and with Sure Profile, we’re proud to deliver an industry-first fraud offering integrated into the credit profile that mitigates lender losses while protecting millions of consumers’ identities,” said Robert Boxberger, President of Decision Analytics, Experian North America. Synthetic identity fraud is expected to drive $48 billion in annual online payment fraud losses by 2023. Between opportunistic fraudsters and a lack of a unified definition for synthetic identity theft it can be nearly impossible to detect—and therefore prevent—this type of fraud. This breakthrough solution provides a composite history of a consumer’s identification, public record, and credit information and determines the risk of synthetic fraud associated with that consumer. It’s not just a fraud tool, it’s a comprehensive credit profile that utilizes premium data so lenders can make positive credit decisions. Sure Profile leverages the capabilities of the Experian Ascend Identity PlatformTM and uses Experian’s industry-leading data assets and data quality to drive advanced analytics that set a higher level of protection for lenders. It’s powered by newly-developed machine learning and AI models. And it offers a streamlined approach to define and detect synthetic identities early in the originations process. Most importantly, Sure Profile differentiates between real people and potentially risky applicants so lenders can increase application approvals with greater assurance and less risk. “Experian can confidently define and help detect synthetic fraud. That's why we can help stop it,” said Craig Boundy, CEO of Experian North America. “Experian stands behind our data with assurance given to our clients. It’s better for lenders and it’s better for consumers.” Sure Profile is a complement to our robust set of identity protection and fraud management capabilities, which are designed to address fraud and identity challenges including account openings, account takeovers, e-commerce fraud and more. This first-of-its kind profile is the future of underwriting and portfolio protection and it’s here now. Read press release Learn More About Sure Profile

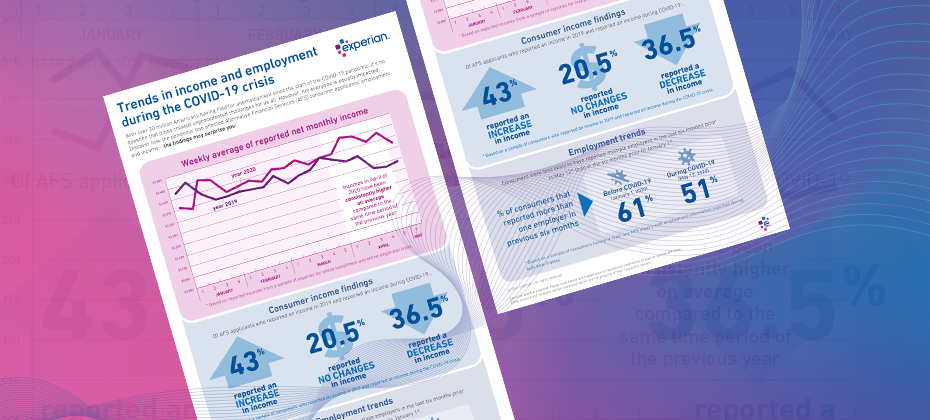

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

This is the third in a series of blog posts highlighting optimization, artificial intelligence, predictive analytics, and decisioning for lending operations in times of extreme uncertainty. The first post dealt with optimization under uncertainty and the second with predicting consumer payment behavior. In this post I will discuss how well credit scores will work for consumer lenders during and after the COVID-19 crisis and offer some recommendations for what lenders can be doing to measure and manage that model risk in a time like this. Perhaps no analytics innovation has created opportunity for more individuals than the credit score has. The first commercially available credit score was developed by MDS (now part of Experian) in 1987. Soon afterwards FICO® popularized the use of scores that evaluate the risk that a consumer would default on a loan. Prior to that, lending decisions were made by loan officers largely on the basis on their personal familiarity with credit applicants. Using data and analytics to assess risk not only created economic opportunity for millions of borrowers, but it also greatly improved the financial soundness of lending institutions worldwide. Predictive models such as credit scores have become the most critical tools for consumer lending businesses. They determine, among other things, who gets a loan and at what price and how an account such as a credit line is managed through its life cycle. Predictive models are in many cases critical for calculating loan and loss reserves, for stress testing, and for complying with accounting standards. Nearly all lenders rely on generic scores such as the FICO® score and VantageScore® credit score. Most larger companies also have a portfolio of custom scorecards that better predict particular aspects of payment behavior for the customers of interest. So how well are these scorecards likely to perform during and after the current pandemic? The models need to predict consumer credit risk even as: Nearly all consumers change their behaviors in response to the health crisis, Millions of people—in America and internationally—find their income suddenly reduced, and Consumers receive large numbers of accommodations from creditors, who have in turn temporarily changed some of their credit reporting practices in response to guidelines in the federal CARES Act. In an earlier post, I pointed out that there is good reason to believe that credit scores will tend to continue to rank order consumers from most likely to least likely to repay their debts even as we move from the longest economic expansion in history to a period of unforeseen and unexpected challenges. But the interpretation of the score (for example, the log odds or the bad rate) may need to be adjusted. Furthermore, that assumes that the model was working well on a lender’s population before this crisis started. If it has been a long time since a scorecard was validated, that assumption needs to be questioned. Because experts are considering several different scenarios regarding both the immediate and long-term economic impacts of COVID-19, it’s important to have a plan for ongoing monitoring as long as necessary. Some lenders have strong Model Risk Management (MRM) teams complying with requirements from the Federal Reserve, Federal Deposit Insurance Corporation (FDIC), the Office of the Comptroller of the Currency (OCC). Those resources are now stretched thin. Other institutions, with fewer resources for MRM, are now discovering gaps in their model inventories as they implement operational changes. In either case, now’s the time to reassess how well scorecards are working. Good model validation practices are especially critical now if lenders are to continue to make the sound data-driven decisions that promote fairness for consumers and financial soundness for the institution. If you’re a credit risk manager responsible for the generic or custom models driving your lending, servicing, or capital allocation policies, there are several things you can do--starting now--to be sure that your organization can continue to make fair and sound lending decisions throughout this volatile period: Assess your model inventory. Do you have good documentation showing when each of the models in your organization was built? When was it last validated? Assign a level of criticality to each model in use. Starting with your most critical models, perform a baseline validation to determine how the model was performing prior to the global health crisis. It may be prudent to conduct not only your routine validation (verifying that the model was continuing to perform at the beginning of the period) but also a baseline validation with a shortened performance window (such as 6-12 months). That baseline validation will be useful if the downturn becomes a protracted one—in which case your scorecard models should be validated more frequently than usual. A shorter outcome window will allow a timelier assessment of the relationship between the score and the bad rate—which will help you update your lending and servicing policies to prevent losses. Determine if any of your scorecards had deteriorated even before the global pandemic. Consider recalibrating or rebuilding those scorecards. (Use metrics such as the Population Stability Index, the K-S statistic and the Gini Coefficient to help with that decision.) Many lenders chose not to prioritize rebuilding their behavioral scorecards for account management or collections during the longest period of economic growth in memory. Those models may soon be among the most critical models in your organization as you work to maintain the trust of your accountholders while also maintaining your institution’s financial soundness. Once the CARES accommodation period has expired, it will be important to revalidate your models more frequently than in the past—for as long as it takes until consumer behavior normalizes and the economy finds its footing. When you find it appropriate to rebuild a scorecard model, consider whether now is the time to implement ethical and explainable AI. Some of our clients are finding that Machine Learned models are more predictive than traditional scorecards. Early Experian research using data from the last recession indicates this will continue to be true for the foreseeable future. Furthermore, Experian has invested in Research and Development to help these clients deliver FCRA-compliant Adverse Action reasons to their consumers and to make the models explainable and transparent for model risk governance and compliance purposes. The sudden economic volatility that has resulted from this global health crisis has been a shock to all organizations. It is important for lenders to take the pulse of their predictive models now and throughout the downturn. They are especially critical tools for making sound data-driven business decisions until the economy is less volatile. Experian is committed to helping your organization during times of uncertainty. For more resources, visit our Look Ahead 2020 Hub. Learn more

When running a credit report on a new applicant, you must ensure Fair Credit Reporting Act (FCRA) compliance before accessing, using and sharing the collected data. The Coronavirus Aid, Relief, and Economic Security (CARES) Act has impacted credit reporting under the FCRA, as has new guidance from the Consumer Financial Protection Bureau (CFPB). Recent updates include: The CARES Act amended the FCRA to require furnishers who agree to an “accommodation,”1 to report the account as current, although it is permitted to continue to report the account as delinquent if the account was delinquent before the accommodation was made. Although not legally obligated, data furnishers should continue furnishing information to the credit reporting agencies (CRAs) during the COVID-19 crisis, and make sure that information reported is complete and accurate. Below is a brief FCRA-related compliance overview2 covering various FCRA requirements3 when requesting and using consumer credit reports for an extension of credit permissible purpose. For more information regarding your responsibilities under the FCRA as a user of consumer reports, please consult your Legal Counsel and the Notice to Users of Consumer Reports: Obligations of Users Under the FCRA handbook located on our website. Before obtaining a consumer report you have… Reviewed your federal and state regulations and laws related to consumer reports, scores, decisions, etc. Made sure you have a valid permissible purpose for pulling the consumer report. Certified compliance to the CRA from which you are getting the consumer report. You have certified that you complied with all the federal and state requirements. After you take an adverse action based on a consumer report you… Provide the consumer with an oral, written or electronic notice of the adverse action. Provide written or electronic disclosure of the numerical credit score used to take the adverse action, or when providing a “risk-based pricing” notice. Provide the consumer with an oral, written or electronic notice, which includes the below information: Name, address and telephone number of CRA that supplied the report, if nationwide. A statement that the CRA did not make the adverse decision and therefore can’t explain why the decision was made. Notice of the consumer’s right to a free copy of their report from the CRA, if requested within 60 days. Notice of the consumer’s right to dispute with the CRA the accuracy or completeness of any information in a consumer report provided by the CRA. Provide the consumer with a “risk-based pricing” notice if credit was granted but on less favorable terms based on information in their consumer report. We understand how challenging it is to understand and meet all your obligations as a data furnisher – we’re here to make it a little easier. Click below to speak with a representative and gain more insight on how the CARES Act impacts FCRA reporting. Download overview Speak with a representative 1An “accommodation” is defined as “an agreement to defer one or more payments, make a partial payment, forbear any delinquent amounts, modify a loan or contract, or any other assistance or relief” granted to a consumer affected by COVID-19 during the covered period. 2This FCRA overview is not legal guidance and does not enumerate all your requirements under the FCRA as a user of consumer reports. Additionally, this FCRA Overview is not intended to provide legal advice or counsel you regarding your obligations under the FCRA or any other federal or state law or regulation. Should you have any questions about your institution’s specific obligations under the FCRA or any other federal or state law or regulation, you should consult with your Legal Counsel. 3This FCRA overview is intended to be used solely by financial service providers when extending credit to consumers and does not include all FCRA regulatory obligations. You are responsible for regulatory compliance when requesting and using consumer reports, which includes adhering to all applicable federal and state statutes and regulations and ensuring that you have the correct policies and procedures in place.

Today’s lending market has seen a significant increase in alternative business lending, with companies utilizing new data assets and technology. As the lending landscape becomes increasingly competitive, consumers have more choices than ever when it comes to lending products. To drive profitable growth, lenders must find new ways to help applicants gain access to the loans they need. How Spring EQ is leveraging Experian BoostTM Home equity lender Spring EQ turned to Experian’s first-of-its-kind financial tool that empowers consumers to add positive payments directly into their credit file to assist applicants with attaining the best loan opportunities and rates. By using Experian BoostTM, which captures the value of consumer’s utility and telecom trade lines, in their current lending process, Spring EQ can help applicants near approval or risk thresholds move to higher risk tiers and qualify for better loan terms and conditions. Driving growth with consumer-permissioned data Over 40 million consumers in the U.S. either have no credit file or have insufficient information in their files to generate a traditional credit score. Consumer-permissioned data empowers these individuals to leverage their online financial data and payment histories to gain better access to loans and other financial services while providing lenders with a more comprehensive view of their creditworthiness. According to Experian research, 70% of consumers see the benefits of sharing additional financial information and contributing positive payment history to their credit file if it increases their odds of approval and helps them access more favorable credit terms. Read our case study for more insight on using Experian Boost to: Make better lending decisions Offer or underwrite credit to more people Promote the right credit products Increase conversion and utilization rates Read case study Learn more about Experian Boost

There are more than 100 million people in the United States who don’t have a fair chance at access to credit. These people are forced to rely on high-interest credit cards and loans for things most of us take for granted, like financing a family car or getting an apartment. At Experian, we have a fundamental mission to be a champion for the consumer. Our commitment to increasing financial inclusion and helping consumers gain access to the financial services they need is one of the reasons we have been selected as a Fintech Breakthrough Award winner for the third consecutive year. The Fintech Breakthrough Awards is the premier awards program founded to recognize the fintech innovators, leaders and visionaries from around the world. The 2020 Fintech Breakthrough Award program attracted more than 3,750 nominations from across the globe. Last year, Experian took home the award for Best Overall Analytics Platform for our Ascend Analytical Sandbox™, a first-to-market analytics environment that promised to move companies beyond just business intelligence and data visualization to data insights and answers they could use. The year prior, Experian won the Consumer Lending Innovation Award for our Text for Credit™ solution, a powerful tool for providing consumers the convenience to securely bypass the standard-length ‘pen & paper’ or keystroke intensive credit application process while helping lenders make smart, fraud protected lending decisions. This year, we are excited to announce that Experian has been selected once again as a winner in the Consumer Lending Innovation category for Experian Boost™. Experian Boost – with direct, active consumer consent – scans eligible accounts for ‘boostable’ positive payment data (e.g., utility and telecom payments) and provides the means for consumers to add that data to their Experian credit reports. Now, for the very first time, millions of consumers benefit from payments they’ve been making for years but were never reflected on their credit reports. Since launching in March 2019, cumulatively, more than 18 million points have been added to FICO® Scores via Experian Boost. Two-thirds of consumers who completed the Experian Boost process increased their FICO Score and among these, the average score increase has been more than 13 points, and 12% have moved up in credit score category. “Like many fintechs, our goal is to help more consumers gain access to the financial services they need,” said Alex Lintner, Group President of Experian Consumer Information Services. “Experian Boost is an example of our mission brought to life. It is the first and only service to truly put consumers in control of their credit. We’re proud of this recognition from Fintech Breakthrough and the momentum we’ve seen with Experian Boost to date.” Contributing consumer payment history to an Experian credit file allows fintech lenders to make more informed decisions when examining prospective borrowers. Only positive payment histories are aggregated through the platform and consumers can remove the new data at any time. There is no limit to how many times one can use Experian Boost to contribute new data. For more information, visit Experian.com/Boost.