Tag: alternative lending

Over the past few decades, the financial industry has gone through significant changes. One of the most notable changes is the use of alternative credit data1 for lending. This type of data is becoming increasingly essential in consumer and small business lending. In this blog post, we’ll explore the importance of alternative credit data and the insights you can gain from our new 2023 State of Alternative Credit Data Report. Benefits and uses of alternative credit data and alternative lending Alternative credit data and alternative financial services offer substantial benefits to lenders, borrowers, and society as a whole. The primary advantage of alternative credit data is that it provides a more comprehensive and accurate credit history of the borrower. Unlike traditional credit data that focuses on a borrower’s financial past, alternative credit data includes information from non-traditional sources like rent payments, full-file public records, utility bills, and income and employment data. This additional data allows you to gain a better understanding of financial behavior and assess creditworthiness more accurately.Alternative credit data can be used throughout the loan lifecycle, from underwriting to servicing. In the underwriting phase, alternative credit data can help lenders expand their pool of potential borrowers, especially those who lack or have limited traditional credit history. Additionally, alternative credit data can help lenders identify risks and minimize fraud. In the servicing phase, alternative credit data can help lenders monitor financial health and provide relevant services and an enhanced customer experience.Alternative lending is critical for driving financial inclusion and profitability. Traditional credit models often exclude individuals who have limited or no access to credit, causing them to turn to high-cost alternatives like payday loans. Alternative credit data can provide a more accurate assessment of their ability to pay, making it easier for them to access affordable credit. This increased accessibility improves the borrower's financial health and creates new opportunities to expand your customer base. “Lenders can access credit data and real-time information about consumers’ incomes, employment statuses, and how they are managing their finances and get a more accurate view of a consumer’s financial situation than previously possible.”— Scott Brown, President of Consumer Information Services, Experian State of alternative credit data Our new 2023 State of Alternative Credit Data Report provides exclusive insight into the alternative lending market, new data sources, inclusive finance opportunities and innovations in credit attributes and scoring that are making credit scoring more accurate, transparent and inclusive. For instance, the use of machine learning algorithms and artificial intelligence is enabling lenders to develop more predictive alternative credit scoring models and enhance risk assessment. Findings from the report include: 54% of Gen Z and 52% of millennials feel more comfortable using alternative financing options rather than traditional forms of credit.2 62% of financial institution firms are using alternative data to improve risk profiling and credit decisioning capabilities.3 Modern credit scoring methods could allow lenders to grow their pool of new customers by almost 20%.4 By understanding the power of alternative credit data and staying on top of the latest industry trends, you can widen your pool of borrowers, drive financial inclusion, and grow sustainably. Download now 1When we refer to “Alternative Credit Data,” this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.2Experian commissioned Atomik Research to conduct an online survey of 2,001 adults throughout the United States. Researchers controlled for demographic variables such as gender, age, geographic region, race and ethnicity in order to achieve similar demographic characteristics reported in the U.S. census. The margin of error of the overall sample is +/-2 percentage points with a confidence level of 95 percent. Fieldwork took place between August 22 and August 28, 2023. Atomik Research is a creative market research agency. 3Experian (2022). Reaching New Heights with Financial Inclusion 4Oliver Wyman (2022). Financial Inclusion and Access to Credit

Alternative credit scoring has become mainstream. Lenders that use alternative credit scores can find opportunities to expand their lending universe without taking on additional risk and more accurately assess the credit risk of traditionally scoreable consumers. Obtaining a more holistic consumer view can help lenders improve automation and efficiency throughout the customer lifecycle. What is alternative credit scoring? Alternative credit scoring models incorporate alternative credit data* that isn't typically found on consumer credit reports. These scores aren't necessarily trying to predict alternative outcomes. The goal is the same — to understand the likelihood that a borrower will miss payments in the future. What's different is the information (and sometimes the analytical techniques) that inform these predictions.Traditional credit scoring models solely consider information found in consumer credit reports. There's a lot of information there — Experian's consumer credit database has data on over 245 million consumers. But although traditional consumer data can be insightful, it doesn't necessarily give lenders a complete picture of consumers' creditworthiness. Alternative credit scores draw from additional data sources, including: Alternative financial services: Credit data from alternative financial services (AFS) can tell you about consumers' experiences with small-dollar installment loans, single-payment loans, point-of-sale financing, auto title loans and rent-to-own agreements. Buy Now Pay Later: Buy Now Pay Later (BNPL) borrowing is popular with consumers across the scoring spectrum, and lenders can use access to open BNPL loans to better assess consumers' current capacity. Rental payments: Landlords, property managers, collection companies, rent payment services and consumer-permissioned data can give lenders access to consumers' rent payment history. Full-file public records: Credit reports generally only include bankruptcy records from the previous seven to ten years. However, lenders with access to full-file public records can also learn about consumers' property deeds, address history, and professional and occupational licenses. READ: Take a deep dive into Experian's State of Alternative Credit Data report to learn more about the different types of alternative credit data and uses across the loan lifecycle. With open banking, consumers can now easily and securely share access to their banking and brokerage account data — and they're increasingly comfortable doing so. In fact, 70% would likely share their banking data for better loan rates, financial tools or personalized spending insights.Tools like Experian Boost allow consumers to add certain types of positive payment information to their Experian credit reports, including rent, utility and select streaming service payments. Some traditional scores consider these additional data points, and users have seen their FICO Score 8 from Experian boosted by an average of 13 points.1 Experian Go also allows credit invisible consumers to establish a credit report with consumer-permissioned alternative data. The benefits of using alternative credit data The primary benefit for lenders is access to new borrowers. Alternative credit scores help lenders accurately score more consumers — identifying creditworthy borrowers who might otherwise be automatically denied because they don't qualify for traditional credit scores. The increased access to credit may also align with lenders' financial inclusion goals.Lenders may additionally benefit from a more precise understanding of consumers who are scoreable. When integrated into a credit decisioning platform, the alternative scores could allow lenders to increase automation (and consumers' experiences) without taking on more credit risk. The future of alternative credit scoring Alternative credit scoring might not be an alternative for much longer, and the future looks bright for lenders who can take advantage of increased access to data, advanced analytics and computing power.Continued investment in alternative data sources and machine learning could help bring more consumers into the credit system — breaking barriers and decreasing the cost of basic lending products for millions. At the same time, lenders can further customize offers and automate their operations throughout the customer lifecycle. Partnering with Experian Small and medium-sized lenders may lack the budget or expertise to unlock the potential of alternative data on their own. Instead, lenders can turn to off-the-shelf alternative models that can offer immediate performance lifts without a heavy IT investment.Experian's Lift PlusTM score draws on industry- leading mainstream credit data and FCRA-regulated alternative credit data to provide additional consumer behavior insights. It can score 49% of mainstream credit-invisible consumers and for thin file consumers with a new trade, a 29% lift in scoreable accounts. Learn more about our alternative credit data scoring solutions. Learn more * When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions as regulated by the Fair Credit Reporting Act (FCRA). Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.1Experian (2023). Experian Boost

Conventional credit scoring systems are based on models developed over six decades. As consumer behavior evolves, it's important to seek newer, fresher sources of data to assess creditworthiness. Because the data used by conventional credit scoring models does not provide the full picture of a consumer's financial health, a large population segment of the United States is excluded from accessing credit.With changing times and new technology, forward-thinking financial institutions are using alternative data1 to gain a more holistic consumer view. A move toward inclusive finance, including incorporating alternative data in credit scoring models, is a crucial step towards promoting financial inclusion and helping millions of consumers achieve their financial and personal goals. More importantly, it provides the insight needed for lender confidence, which can help fuel business growth. Understanding limitations of the conventional scoring system Credit scores can be obtained from any one of the major credit bureaus based on information found in a consumer's credit report and are incorporated into a lender's credit-decisioning process. While there are various credit scoring models based on lender preference that could yield slightly different scores, all traditional scores are comprised of credit characteristics within these categories: payment history, credit mix, credit history length, amounts owed and new credit account inquires. Lenders use past credit performance to predict whether extending credit is a risk, posing a major challenge for credit invisible and thin-file consumers and leaving millions at a disadvantage. This dilemma also limits business growth for lenders. Consumers who are unable to access mainstream credit often turn to the alternative financial services (AFS) industry, a $140 billion market that continues to grow by 7-10 percent each year.2 The AFS industry offers consumers additional products, like payday loans, cash advances, short-term installment loans, and rent-to-own loans, none of which are included in a traditional credit file. With alternative credit data, lenders can obtain a more holistic view of creditworthiness and risk, helping to enhance inclusive lending by broadening their pool of potential loan candidates. Why conventional scoring models simply aren't enough Because of the criteria used to assess creditworthiness, conventional credit scoring models do not accurately capture an individual's financial behavior or health. Indeed, many people demonstrate financial responsibility in other legitimate ways that are not reported to the major credit bureaus.In contrast, non-traditional data considers a consumer's everyday financial behavior to provide a more accurate score for lenders. It can include a range of indicators, such as: Bill payments: Consistent payment history on typical household bills (which may have been paid from a debit account). Bank account data: Shows average balance and withdrawal activity and recurring payroll deposits (indicating that a consumer is employed and receives a regular income). Rental data: Indicates a consumer's long-term stability in making regular, on-time monthly rent payments. Registered licenses: Registered licenses or membership with a skilled trade or profession can indicate the likelihood to generate income. Including this type of data can benefit both lenders and applicants. According to an Experian report, by adding alternative credit data to a near-prime population, lenders could see an increase in approvals for consumers historically being left behind. When Clear Early Risk Score™ is paired with the VantageScore® credit score, approvals climb to 16 percent of the population inside the same risk criteria, representing a 60 percent lift in credit approvals for near-prime consumers.2 The pool of people from whom this type of alternative data can reliably be collected is growing, with 70 percent of consumers willing to provide additional financial information to a lender if it increases their chance for approval or improves their interest rate for a mortgage or car loan.3 Plenty of available yet untapped data exists that can add value to a consumer's profile and lead to greater inclusive lending. For example, 95 percent of Americans own a cell phone and about two-thirds of households headed by young adults are being rented. Reporting on this data could potentially "thicken" a credit file and provide deeper insight into a consumer's credit behavior.3Indeed, turning to non-traditional data can expand the credit universe and lead to more inclusive credit scoring models, especially by leveraging existing technology and financial inclusion solutions. Research shows that with Lift Premium™, virtually all of the 21 million conventionally unscorable consumers would become scoreable, and over 1 million of them would have scores in the near-prime range or better. Of these, 1.7 million would be Black American and Hispanic/Latino people.3 For lenders, these numbers reveal potential opportunities to grow their businesses. Of the 255 million adults in the U.S., 19 percent of credit eligible adults are left out of mainstream scoring systems. 28 million are considered credit invisible – meaning they have no credit history (11%). 21 million are considered unscorable – have partial credit history but not enough to generate a score using conventional models (8%). Of the remaining credit eligible adults, 57 million were considered subprime (22%). 106 million U.S. adults can't get mainstream credit rates (42%). Adopting inclusive finance lending practices is not only the right thing to do but also provides financial institutions with the chance to reach untapped markets, grow their business and promote a healthier economy. Financial inclusion is not a destination, but an ever-evolving journey. Don't miss out on this critical opportunity to join the movement. Learn more about our financial inclusion tools to help enhance your inclusive lending approach. 1"Alternative Credit Data,” refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.2Experian: 2020 State of Alternative Credit Data.3Oliver Wyman white paper, “Financial Inclusion and Access to Credit," January 12, 2022.

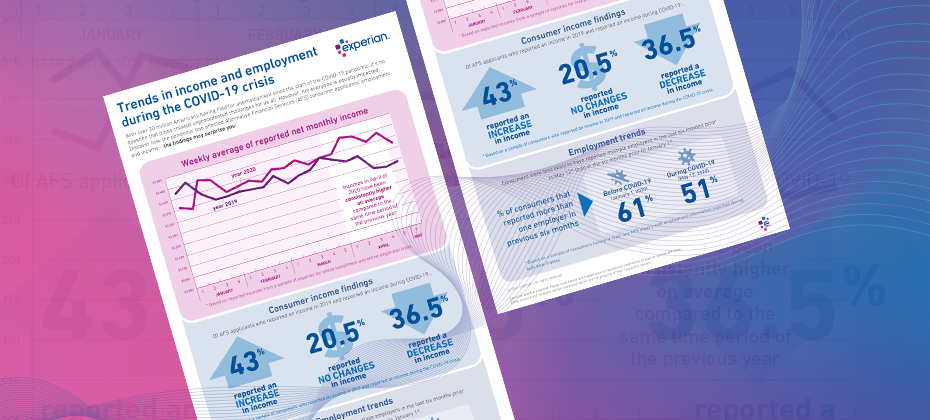

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

Article written by Melanie Smith, Senior Copywriter, Experian Clarity Services, Inc. It’s been almost a decade since the Great Recession in the United States ended, but consumers continue to feel its effects. During the recession, millions of Americans lost their jobs, retirement savings decreased, real estate reduced in value and credit scores plummeted. Consumers that found themselves impacted by the financial crisis often turned to alternative financial services (AFS). Since the end of the recession, customer loyalty and retention has been a focus for lenders, given that there are more options than ever before for AFS borrowers. To determine what this looks like in the current climate, we examined today’s non-prime consumers, what their traditional scores look like and if they are migrating to traditional lending. What are alternative financial services (AFS)? Alternative financial services (AFS) is a term often used to describe the array of financial services offered by providers that operate outside of traditional financial institutions. In contrast to traditional banks and credit unions, alternative service providers often make it easier for consumers to apply and qualify for lines of credit but may charge higher interest rates and fees. More than 50% of new online AFS borrowers were first seen in 2018 To determine customer loyalty and fluidity, we looked extensively at the borrowing behavior of AFS consumers in the online marketplace. We found half of all online borrowers were new to the space as of 2018, which could be happening for a few different reasons. Over the last five years, there has been a growing preference to the online space over storefront. For example, in our trends report from 2018, we found that 17% of new online customers migrated from the storefront single pay channel in 2017, with more than one-third of these borrowers from 2013 and 2014 moving to online overall. There was also an increase in AFS utilization by all generations in 2018. Additionally, customers who used AFS in previous years are now moving towards traditional credit sources. 2017 AFS borrowers are migrating to traditional credit As we examined the borrowing behavior of AFS consumers in relation to customer loyalty, we found less than half of consumers who used AFS in 2017 borrowed from an AFS lender again in 2018. Looking into this further, about 35% applied for a loan but did not move forward with securing the loan and nearly 24% had no AFS activity in 2018. We furthered our research to determine why these consumers dropped off. After analyzing the national credit database to see if any of these consumers were borrowing in the traditional credit space, we found that 34% of 2017 borrowers who had no AFS activity in 2018 used traditional credit services, meaning 7% of 2017 borrowers migrated to traditional lending in 2018. Traditional credit scores of non-prime borrowers are growing After discovering that 7% of 2017 online borrowers used traditional credit services in 2018 instead of AFS, we wanted to find out if there had also been an improvement in their credit scores. Historically, if someone is considered non-prime, they don’t have the same access to traditional credit services as their prime counterparts. A traditional credit score for non-prime consumers is less than 600. Using the VantageScore® credit score, we examined the credit scores of consumers who used and did not use AFS in 2018. We found about 23% of consumers who switched to traditional lending had a near-prime credit score, while only 8% of those who continued in the AFS space were classified as near-prime. Close to 10% of consumers who switched to traditional lending in 2018 were classified in the prime category. Considering it takes much longer to improve a traditional credit rating, it’s likely that some of these borrowers may have been directly impacted by the recession and improved their scores enough to utilize traditional credit sources again. Key takeaways AFS remains a viable option for consumers who do not use traditional credit or have a credit score that doesn’t allow them to utilize traditional credit services. New AFS borrowers continue to appear even though some borrowers from previous years have improved their credit scores enough to migrate to traditional credit services. Customers who are considered non-prime still use AFS, as well as some near-prime and prime customers, which indicates customer loyalty and retention in this space. For more information about customer loyalty and other recently identified trends, download our recent reports. State of Alternative Data 2019 Lending Report

In today’s age of digital transformation, consumers have easy access to a variety of innovative financial products and services. From lending to payments to wealth management and more, there is no shortage in the breadth of financial products gaining popularity with consumers. But one market segment in particular – unsecured personal loans – has grown exceptionally fast. According to a recent Experian study, personal loan originations have increased 97% over the past four years, with fintech share rapidly increasing from 22.4% of total loans originated to 49.4%. Arguably, the rapid acceleration in personal loans is heavily driven by the rise in digital-first lending options, which have grown in popularity due to fintech challengers. Fintechs have earned their position in the market by leveraging data, advanced analytics and technology to disrupt existing financial models. Meanwhile, traditional financial institutions (FIs) have taken notice and are beginning to adopt some of the same methods and alternative credit approaches. With this evolution of technology fused with financial services, how are fintechs faring against traditional FIs? The below infographic uncovers industry trends and key metrics in unsecured personal installment loans: Still curious? Click here to download our latest eBook, which further uncovers emerging trends in personal loans through side-by-side comparisons of fintech and traditional FI market share, portfolio composition, customer profiles and more. Download now

Would you hire a new employee strictly by their resume? Surely not – there’s so much more to a candidate than what’s written on paper. With that being said, why would you determine your consumers’ creditworthiness based only on their traditional credit score? Resumes don’t always give you the full picture behind an applicant and can only tell a part of someone’s story, just as a traditional credit score can also be a limited view of your consumers. And lenders agree – findings from Experian’s 2019 State of Alternative Credit Data revealed that 65% of lenders are already leveraging information beyond the traditional credit report to make lending decisions. So in addition to the resume, hiring managers should look into a candidate’s references, which are typically used to confirm a candidate’s positive attributes and qualities. For lenders, this is alternative credit data. References are supplemental but essential to the resume, and allow you to gain new information to expand your view into a candidate – synonymous to alternative credit data’s role when it comes to lending. Lenders are tasked with evaluating their consumers to determine their stability and creditworthiness in an effort to prevent and reduce risk. While traditional credit data contains core information about a consumer’s credit data, it may not be enough for a lender to formulate a full and complete evaluation of the consumer. And for over 45 million Americans, the issue of having no credit history or a “thin” credit history is the equivalent of having a resume with little to no listed work experience. Alternative credit data helps to fill in the gaps, which has benefits for both lenders and consumers. In fact, 61% of consumers believe adding payment history would have a positive impact on their credit score, and therefore are willing to share their data with lenders. Alternative credit data is FCRA-compliant and includes information like alternative finance data, rental payments, utility payments, bank account information, consumer-permissioned data and full-file public records. Because this data shows a holistic view of the customer, it helps to determine their ability to repay debts and reveals any delinquent behaviors. These insights help lenders to expand their consumer lending universe– all while mitigating and preventing risk. The benefits can also be seen for home-based and small businesses. Fifty percent of all US small businesses are home-based, but many small business owners lack visibility due to their thin-file nature – making it extremely difficult to secure bank loans and capital to fund their businesses. And, younger generations and small business owners account for 58% of business owners who rely on short term lending. By leveraging alternative credit data, lenders can get greater insights into a small business owner’s credit profile and gauge risk. Entrepreneurs can also benefit from this information being used to build their credit profiles – making it easier for them to gain access to investment capital to fund their new ventures. Like a hiring manager, it’s important for lenders to get a comprehensive view to find the most qualified candidates. Using alternative credit data can expand your choices – read our 2019 State of Alternative Credit Data Whitepaper to learn more and register for our upcoming webinar. Register Now

The lending market has seen a significant shift from traditional financial institutions to fintech companies providing alternative business lending. Fintech companies are changing the brick-and-mortar landscape of lending by utilizing data and technology. Here are four ways fintech has changed the lending process and how traditional financial institutions and lenders can keep up: 1. They introduced alternative lending models In a traditional lending model, lenders accept deposits from customers to extend loan offers to other customers. One way that fintech companies disrupted the lending process is by introducing peer-to-peer lending. With peer-to-peer lending, there is no need to take a deposit at all. Instead, individuals can earn interest by lending to others. Banks who collaborate with peer-to-peer lenders can improve their credit appraisal models, enhance their online lending strategy, and offer new products at a lower cost to their customers. 2. They offer fast approvals and funding In certain situations, it can take banks and credit card providers weeks to months to process and approve a loan. Conversely, fintech lenders typically approve and fund loans in less than 24 hours. According to Mintel, only 30% of consumers find various banking features easy-to-use. Financial experts at Toptal suggest that banks consider speeding up the loan application and funding process within their online lending platforms to keep up with high-tech companies, such as Amazon, that offer customers an overall faster lending process from applications to approval, to payments. 3. They're making use of data Typically, fintech lenders pull data from several different alternative sources to quickly determine how likely a borrow is to pay back the loan. The data is collected and analyzed within seconds to create a snapshot of the consumer's creditworthiness and risk. The information can include utility, rent. auto payments, among other sources. To keep up, financial institutions have begun to implement alternative credit data to get a more comprehensive picture of a consumer, instead of relying solely upon the traditional credit score. 4. They offer perks and savings By enacting smoother automated processes, fintech lenders can save money on overhead costs, such as personnel, rent, and administrative expenses. These savings can then be passed onto the customer in the form of competitive interest rates. While traditional financial institutions generally have low overall interest rates, the current high demand for loans could help push their rates even lower. Additionally, financial institutions have started to offer more customer perks. For example, Goldman Sachs recently created an online lending platform, called Marcus, that offers unsecured consumer loans with no fees. Financial institutions may feel stuck in legacy systems and unable to accomplish the agile environments and instant-gratification that today's consumers expect. However, by leveraging new data sets and innovation, financial institutions may be able to improve their product offerings and service more customers. Looking to take the next step? We can help. Learn More About Banks Learn More About Fintechs

From the time we wake up to the minute our head hits the pillow, we make about 35,000 conscious and unconscious decisions a day. That’s a lot of processing in a 24-hour period. As part of that process, some decisions are intuitive: we’ve been in a situation before and know what to expect. Our minds make shortcuts to save time for the tasks that take a lot more brainpower. As for new decisions, it might take some time to adjust, weigh all the information and decide on a course of action. But after the new situation presents itself over and over again, it becomes easier and easier to process. Similarly, using traditional data is intuitive. Lenders have been using the same types of data in consumer credit worthiness decisions for decades. Throwing in a new data asset might take some getting used to. For those who are wondering whether to use alternative credit data, specifically alternative financial services (AFS) data, here are some facts to make that decision easier. In a recent webinar, Experian’s Vice President of Analytics, Michele Raneri, and Data Scientist, Clara Gharibian, shed some light on AFS data from the leading source in this data asset, Clarity Services. Here are some insights and takeaways from that event. What is Alternative Financial Services? A financial service provided outside of traditional banking institutions which include online and storefront, short-term unsecured, short-term installment, marketplace, car title and rent-to-own. As part of the digital age, many non-traditional loans are also moving online where consumers can access credit with a few clicks on a website or in an app. AFS data provides insight into each segment of thick to thin-file credit history of consumers. This data set, which holds information on more than 62 million consumers nationwide, is also meaningful and predictive, which is a direct answer to lenders who are looking for more information on the consumer. In fact, in a recent State of Alternative Credit Data whitepaper, Experian found that 60 percent of lenders report that they decline more than 5 percent of applications because they have insufficient information to make a loan decision. The implications of having more information on that 5 percent would make a measurable impact to the lender and consumer. AFS data is also meaningful and predictive. For example, inquiry data is useful in that it provides insight into the alternative financial services industry. There are also more stability indicators in this data such as number of employers, unique home phone, and zip codes. These interaction points indicate the stability or volatility of a consumer which may be helpful in decision making during the underwriting stage. AFS consumers tend to be younger and less likely to be married compared to the U.S. average and traditional credit data on File OneSM . These consumers also tend to have lower VantageScore® credit scores, lower debt, higher bad rates and much lower spend. These statistics lend themselves to seeing the emerging consumer; millennials, immigrants with little to no credit history and also those who may have been subprime or near prime consumers who are demonstrating better credit management. There also may be older consumers who may have not engaged in traditional credit history in a while or those who have hit a major life circumstance who had nowhere else to turn. Still others who have turned to nontraditional lending may have preferred the experience of online lending and did not realize that many of these trades do not impact their traditional credit file. Regardless of their individual circumstances, consumers who leverage alternative financial services have historically had one thing in common: their performance in these products did nothing to further their access to traditional, and often lower cost, sources of credit. Through Experian’s acquisition and integration of Clarity Services, the nation’s largest alternative finance credit bureau, lenders can gain access to powerful and predictive supplemental credit data that better detect risk while benefiting consumers with a more complete credit history. Alternative finance data can be used across the lending cycle from prospecting to decisioning and account review to collections. Alternative data gives lenders an expanded view of consumer behavior which enables more complete and confident lending decisions. Find out more about Experian’s alternative credit data: www.experian.com/alternativedata.

Whether it is an online marketplace lender offering to refinance the student loan debt of a recent college graduate or an online small-business lender providing an entrepreneur with a loan when no one else will, there is no doubt innovation in the online lending sector is changing how Americans gain access to credit. This expanding market segment takes great pride in using “next-generation” underwriting and credit scoring risk models. In particular, many online lenders are incorporating noncredit information such as income, education history (i.e., type of degree and college), professional licenses and consumer-supplied information in an effort to strike the right balance between properly assessing credit risk and serving consumers typically shunned by traditional lenders because of a thin credit history. Regulatory concerns The exponential growth of the online lending sector has caught the attention of regulators — such as the U.S. Treasury Department, the Federal Deposit Insurance Corporation, Congress and the California Business Development Office — who are interested in learning more about how online marketplace lenders are assessing the credit risk of consumers and small businesses. At least one official, Antonio Weiss, a counselor to the Treasury secretary, has publicly raised concerns about the use of so-called nontraditional data in the underwriting process, particularly data gleaned from social media accounts. Weiss said that “just because a credit decision is made by an algorithm, doesn’t mean it is fair,” citing the need for lenders to be aware of compliance with fair lending obligations when integrating nontraditional credit data. Innovative and “tried and true” are not mutually exclusive Some have suggested the only way to assuage regulatory concerns and control risk is by using tried-and-true legacy credit risk models. The fact is, however, online marketplace lenders can — and should — continue to push the envelope on innovative underwriting and business models, so long as these models properly gauge credit risk and ensure compliance with fair lending rules. It’s not a simple either-or scenario. Lenders always must ensure their scoring analytics are based upon predictive and accurate data. That’s why lenders historically have relied on credit history, which is based upon data consumers can dispute using their rights under the Fair Credit Reporting Act. Statistically sound and validated scores protect consumers from discrimination and lenders from disparate impact claims under the Equal Credit Opportunity Act. The Office of the Comptroller of the Currency guidance on model risk management is an example of regulators’ focus on holding responsible the entities they oversee for the validation, testing and accuracy of their models. Marketplace lenders who want to push the limit can look to credit scoring models now being used in the marketplace without negatively impacting credit quality or raising fair lending risk. For example, VantageScore® allows for the scoring of 30 million to 35 million more people who currently are unscoreable under legacy credit score models. The VantageScore® credit score does this by using a broader, deeper set of credit file data and more advanced modeling techniques. This allows the VantageScore® credit score model to capture unique consumer behaviors more accurately. In conclusion, online marketplace lenders should continue innovating with their own “secret sauce” and custom decisioning systems that may include a mix of noncredit factors. But they also can stay ahead of the curve by relying on innovative “tried-and-true” credit score models like the VantageScore® credit score model. These models incorporate the best of both worlds by leaning on innovative scoring analytics that are more inclusive, while providing marketplace lenders with assurances the decisioning is both statistically sound and compliant with fair lending laws. VantageScore® is a registered trademark of VantageScore Solutions, LLC.

Last December, American Banker named online marketplace lending its innovation of the year as a result of the “industry’s rapid growth and evolution.” Meanwhile, in 2015, millennials scored headlines in nearly every publication imaginable – industries, politicians and academics all trying to understand and articulate how the now largest-living generation will influence how we work, live and lead. So perhaps it’s no surprise the two hot topics have collided this year. Gen Y is tech-dependent and Internet-enabled. They have increasingly grown to expect the tools and services they use to be available online, including anything and everything in the financial services space. Marketplace lenders are ever-so eager to sweep in and serve. Online and mobile solutions are certainly one thing, but Experian’s latest research reveals this generation is also very receptive to “non-bank” lenders for the ease, speed and accessibility they provide. 47 percent of millennials said they are likely to use alternative finance sources in the near future 57 percent reported they are willing to use alternative companies and services that innovate to meet their needs 13 percent said they’ve already taken out a loan from an alternate or non-bank lender As they come of age, hitting those big milestones – college graduations, marriage, starting families, making home purchases – Gen Y is wading through its financial options. Research and logic suggest millennials will without a doubt have a greater openness toward nontraditional banking, representing a huge market for online marketplace lenders. For the millennial entrepreneurs especially, marketplace lending is proving to be a good fit. “They are on the earlier curve of their small business ownership and entrepreneurial paths,” David Solis, sales performance manager at Bank of America, told CNN Money. “It makes sense they’re going to be pursuing alternative forms of lending.” Affluent millennials are another segment open to alternative financial services. A 2015 LinkedIn study on this specific target stated affluent millennials are particularly likely to envision a cashless, sharing-based economy in the future, where banks no longer serve as their primary financial institutions. Nearly seven out of 10 affluent millennials are likely to consider such offerings outside of the traditional financial services space, compared to just 47 percent of affluent Gen X’ers. The millennial generation may not fully understand all products traditional banks offer, since they rarely set foot in “brick-and-mortar” establishments, but they are a prime market for online investing and lending services. They’re more experimental, more digital, less loyal. In short, they are looking for financial services that are as tech-savvy as they are; those who don’t keep up may get left behind, and online marketplace lenders are certainly positioning themselves to win over this generation. To be most successful in capturing this highly sought-after generation, online marketplace lenders will need to continue to innovate both in terms of differentiating their product offerings and getting more sophisticated in their targeted marketing approach. As the online marketplace continues to expand with more players, heating up with increased competition, segmentation strategies will be key in finding the right borrowers and matching them with the right offer. As we head into 2016, there is no doubt many will continue to monitor the financial services trends emerging. Chances are online marketplace lenders and millennials will likely be attached to many of the headlines. For more information, visit www.experian.com/marketplacelending.