Customer Targeting & Segmentation

Payments and the Internet of things has been colliding for a while now – and it surfaced again recently with Mastercard announcing that it is working with an array of partners including Capital One to launch payments in connected devices. The thinking here seems to be that payments is a function in the Marlow’s pyramid of needs for any new consumer device. I am conflicted on this point – not that I don’t believe the Internet of Things isn’t important, but that we may be overthinking in how payments is important to be shoved inside everything that has a radio baked in. And not everything will have a radio in the future, and the role of a smartphone as the center of the connected device commerce universe isn’t going away. It is important to keep perspective here – as this announcement is less about coat sleeves hiding NFC chips with tokenized credit cards – rather it’s the commerce enablement of devices that we may carry on our person so that they can be armed for payment. Though I may disagree on whether a coat sleeve or jewelry are essential end-points in commerce, a platform of capabilities to challenge, authenticate and verify, and ultimately trust and provision a tokenized representation of something, whether its a card or a fragment of a consumer's identity, to a device that itself represents a collection of radios and sensors is very exciting. It is exciting because as device counts and assortments grow, they each have their own residual identity as a combination of things and behaviors that are either deterministic or probabilistic. The biggest shift we will see is that the collective device identities can be a far better and complete representation of customer identity that the latter will be replaced by the former. Name-centric identities will give away to algorithmically arrived ones. As Dan Geer puts it, no longer will I need to announce that I am Cherian, but my collection of devices will indeed do so on my behalf, perhaps in consultation with each other. More over, none of these devices need to replicate my identity in order to be trusted and tethered, either. Coming back to Payments, today my Fitbit’s claim to make a successful payment is validated way before the transaction, when I authorized provisioning by authenticating through a bank app or wallet. What would be interesting is when the reverse becomes true – when these class of devices that I own can together or separately vouch for my identity. We may forget usernames and passwords, fingerprints may prove to be irrevocable and rigid, but we will always be surrounded by a fog of devices that each carry a cryptographically unique and verifiable signature. And it will be up to the smartphone, its ecosystem and the devices that operate in its periphery to individually negotiate and establish trust among each of them. So this is why I believe the MasterCard effort in tokenizing devices is important when you view it in conjunction with the recent launch of SwiftID from CapitalOne. Payments getting shoved in to everyday things like wearables, disguises the more important effort of becoming a beachhead in establishing trust between devices, by using tokenization as the method of delivery. As you may have gathered by now, I am less excited of pushing cards in to devices (least of all – cars!) and more about how a trusted framework to carve out a tamper proof and secure cache within an untrusted device, along with the process to securely provision a token or a signed hash representing something of value, can serve as the foundation for future device – and by extension – user identity. On a side note, here’s a bit about pushing cards in to cars, and mistaking them for connected cars. To me there are only two connected car classes today. One is Tesla where each car on the road is part of the whole, each learning separately and together as they examine, encounter and learn the world around them to maneuver safely. The other is a button in an app that I hit to have a car magically appear in front of me. Other than Tesla and Uber, there are no other commercial instances of a connected car that appeals (Google has no cars you can buy, yet).

With Black Friday quickly approaching, a recent Experian study shows online Black Friday searches are already tracking ahead of last year. This October, the weekly search share for Black Friday averaged 12% higher than October 2014 and is expected to increase dramatically between now and Thanksgiving week. Top product searches for the week ending October 31, 2015 include: Marketers can design more successful campaigns and maximize rewards for both consumers and brands by staying on top of the latest search trends. >> Holiday Hot Sheet

While marketers typically begin deploying Halloween emails in September, last-minute mailings receive the highest response.

With the holidays around the corner, retailers are getting ready to release their holiday campaigns.

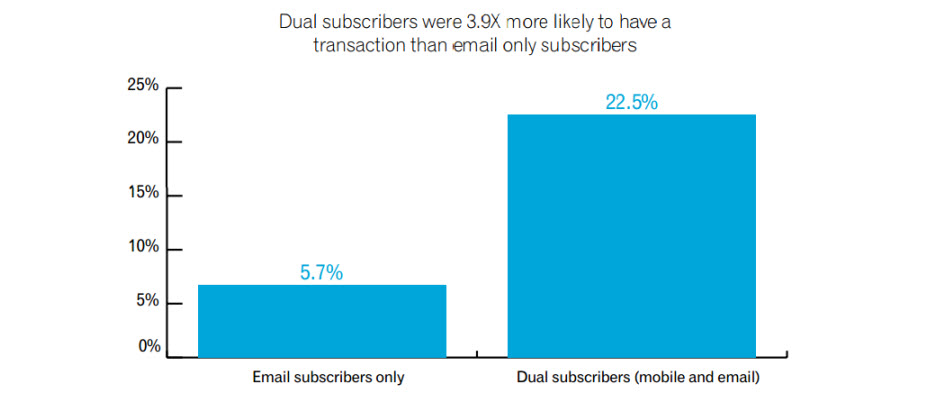

While mobile subscriber lists typically are much smaller than email lists, mobile subscribers tend to be loyal and highly engaged customers.

According to a recent Experian Marketing Services study, informational or "thanks for joining" messages drive significantly higher open and transaction rates than promotional emails, as well as higher revenue per email.

Customer experience strategies for success Sometimes it’s easier to describe something as the opposite of something else. Being “anti-” something can communicate something meaningful. Cultural movements in the past have taken on these monikers: consider the “anti-establishment” or “anti-war” movements. We all need effective anti-virus protection. And there are loads of skin products marketed as “anti-aging”, “anti-wrinkle”, or “anti-blemish.” But when you think about a vision for the customer experience that your company aspires to deliver, this approach of the “anti-X” falls flat. Would you want to aspire to basically “not stink?” Would that inspire you and your team to run through walls to deliver on that grand aspiration? Would it motivate customers to stick with you, buy more of what you sell, and tell others about you? I think not…But it sure seems like many out there indeed do aspire to “not stink.” Sure, there are great companies out there who have a set a high standard for customer experience, placing it at the center of their strategies and their success. Some, like Zappos, started that way from the beginning. Others, like The Ritz-Carlton, realized that they had lost their way and made the commitment to do the hard work of reaching and sustaining excellence. On the other hand, there are hundreds of firms who have a weak commitment to or even understanding of the importance of customer experience to their strategy and performance. Their leaders may give lip service or just pay attention for a few days or hours following the release of reports from leading analysts and firms. They may have posters and slogans that talk about putting the customer first or similar platitudes. These companies probably even have talented and passionate professionals working tirelessly to improve the customer experience in spite of the fact that nobody seems to care much. What these firms lack is a clear customer experience strategy. As nature abhors a vacuum, customers and employees are free to infer or just guess at it. Focusing on customer experience only when a report comes out – and paying special attention only when weak results put the firm near the bottom of the ranking leads people to conclude that all that really matters is to “not stink.” In other words, don’t stand out for being bad…but don’t worry much about being good as it is not important to the company’s strategy or results. I think that this “don’t stink” implicit strategy helps explain a fascinating insight from a Forrester survey in 2013: “80% of executives believe their company is delivering a superior customer experience, yet in 2013 only 8% of companies surveyed received a top grade from their customers.” Many leaders simply have not invested the energy and commitment necessary to define a real customer experience vision that reflects a deep understanding of the role that it plays in the company’s strategy. Beyond setting that vision, there is a big and sustained commitment required to deliver on the vision, measure results, and continuously adjust as customer needs evolve. Like all journeys, a great customer experience starts with one step. Establishing a customer experience strategy is the first one – and “don’t stink” simply stinks as a strategy. Download our recent perspective paper to learn how exceptional customer experience can give companies the competitive edge they need in a market where price, products and services can no longer be a differentiator.

The availability and opportunities for customers to conduct business through mobile devices continues to multiply, challenging organizations to protect customers without impacting their experience. Our infographic highlights five challenges of customer authentication that businesses face and what customers feel in an increasingly mobile world. Personally Identifiable Information (PII) is more available, but less reliable, than ever before. 35% performance improvement using models built with attributes beyond simple identity element validation. More transactions are taking place in an omnichannel environment. 36% of organizations interact with their customer in five or more channels. Diversity of devices and technology complicates customer authentication. 85% of consumers use online or mobile to conduct business. 17% of consumers reported having an online transaction declined when device information was not available. Increased online transactions have multiplied fraud opportunities, resulting in more false positives. Of those surveyed who have had Card Not Present (CNP) transactions declined: 31% blame the merchant 38% blame the credit card network 83% felt embarassed or angry Stringent requirements change the way organizations interact with customers. 80% expect the focus on managing regulatory risk to be more than it is today Download our fraud prevention perspective paper to gain more insight on how you can prepare your business.

Have a look ‘Inside Experian’ through this documentary on our global business explaining who we are, what we do and how we’re helping people and businesses around the world protect, manage and make the most of their data. This ‘Inside Experian’ video focuses on 41st Parameter, a leading provider of dedicated fraud prevention solutions. Their methodology and patented technologies are responsible for reductions in fraud losses and subsequent declining attack rates at some of the largest institutions in e-commerce, financial services, and travel services. Here are some highlights of 41st Parameter’s solutions: $25 trillion in e-commerce orders and financial services transactions scored for risk 500 million transactions processed each month with daily volumes exceeding 8 million transactions a day PCI Certified as a Level 1 Service Provider and ISO-27000, SAS-70 and Safe Harbour Compliant 600 million devices detected by their patented tagless device identification technology captures no PII 41st Parameter works to make the process of preventing and detecting fraud easier and more effective, reducing potential losses while protecting operating costs and the customer experience. Download our fraud prevention whitepaper to gain more insight on how you can prepare your business.

This season’s peak week, the Wednesday before Thanksgiving through the Tuesday after Cyber Monday, had an 18 percent increase in email volume, an 11 percent rise in transactions and a 7 percent increase in email revenue in comparison to peak week 2013. Cyber Monday provided 27 percent of total peak week revenue followed by Black Friday, which accounted for 18 percent of revenue. Marketers can design more successful holiday campaigns by staying on top of the latest email trends. View the December Holiday Hot Sheet

41st Parameter, a part of Experian, surveyed 250 marketers to understand the relationship between omnichannel retailing, fraud prevention and the holiday shopping season. The findings show that few marketers understand the full benefit of fraud-prevention systems on their activities as 60% of marketers were unsure of the cost of fraud to their organization. The survey also indicated that 40% of marketers said their organization had been targeted by hackers or cybercriminals. Download the Holiday Marketing Fraud Survey: http://snip.ly/JoyF With holiday shopping in full stride, 35% of businesses said they planned to increase their digital spend for the 2014 holiday season. Furthermore, Experian Marketing Services reported that during 2014, 80%t of marketers planned on running cross-channel marketing campaigns. As marketers integrate more channels into their campaigns, new challenges emerge for fraud-risk managers who face continuous pressure to adopt new approaches. Here are three steps to help marketers and risk managers maintain a frictionless experience for customers: Marketers should communicate their plans early to the fraud-risk team, especially if they are planning to target a new or unexpected audience. Making this part of the process will reduce the chances that risk management will stop or inhibit customers. Ensure that marketers understand what the risk-management department is doing with respect to fraud detection. Chances are risk managers are waiting to tell you. Marketers shouldn’t assume that fraud won’t affect their business and talk to their risk-management division to learn how much fraud truly costs their company. Then they can understand what they need to do to make sure that their marketing efforts are not thwarted. “Marketers spend a great deal of time and money bringing in new customers and increasing sales, especially this time of year, and in too many cases, those efforts are negated in the name of fraud prevention,” said David Britton, vice president of industry solutions, 41st Parameter. “Marketers can help an organization’s bottom line by working with their fraud-risk department to prevent bad transactions from occurring while maintaining a seamless customer experience. Reducing fraud is important and protecting the customer experience is a necessity.” Few marketers understand the resulting impact of declined transactions because of suspected fraud and this is even more pronounced among small businesses, with 70% saying they were unsure of fraud’s impact. Fifty percent of mid-sized business marketers and 67% of large-enterprise marketers were unsure of the impact of fraud as well An uncoordinated approach to new customer acquisition can result in lost revenue affecting the entire organization. For example, the industry average for card-not-present declines is 15%. However, one to three percent of those declined transactions turn out to be valid transactions, equating to $1.2 billion in lost revenue annually. Wrongfully declined transactions can be costly as the growth of cross-channel marketing increases and a push towards omnichannel retailing pressures marketers to find new customers. “Many businesses loosen their fraud detection measures during high peak time because they don’t have the tools to review potentially risky orders manually during the higher-volume holiday shopping period,” said Britton. “Criminals look to capitalize on this and exploit these gaps in any way possible, taking an omnifraud approach to maximizing their chances of success. Striking the right balance between sales enablement and fraud prevention is the key to maximizing growth for any business at all times of the year.” Download Experian’s fraud prevention report to learn more about how businesses can address these new marketing challenges.

Through all the rather “invented conflict” of MCX vs Apple Pay by the tech media these last few weeks – very little diligence was done on why merchants have come to reject NFC (near field communication) as the standard of choice. Maybe I can provide some color here – both as to why traditionally merchants have viewed this channel with suspicion leading up to CurrenC choosing QR, and why I believe its time for merchants to give up hating on a radio. Why do merchants hate NFC? Traditionally, any contactless usage in stores stems from international travelers, fragmented mobile NFC rollouts and a cornucopia of failed products using a variety of form factors – all of which effectively was a contactless chip card with some plastic around it. Any merchant supported tended to be in the QSR space – biggest of which was McDonalds - and they saw little to no volume to justify the upgrade costs. Magstripe, on the other hand, was a form factor that was more accessible. It was cheap to manufacture, provisioning was a snap, distribution depended primarily on USPS. Retailers used the form factor themselves for Gift cards, Pre-paid and Private Label. In contrast – complexity varies in contactless for all three – production, provisioning and distribution. If it’s a contactless card – all three can still follow pretty much the norm – as they require no customization or changes post-production. Mobile NFC was an entirely different beast. Depending on the litany of stakeholders in the value chain – from Hardware – OEM and Chipset support – NFC Controller to the Secure Element, the OS Support for the NFC stack, the Services – Trusted Service Managers of each flavor (SE vs SP), the Carriers (in case of OTA provisioning) and the list goes on. The NFC Ecosystem truly deters new entrants by its complexity and costs. Next – there was much ambiguity to what NFC/contactless could come to represent at the point of sale. Merchants delineated an open standard that could ferry over any type of credential – both credit and debit. Even though merchants prefer debit, the true price of a debit transaction varies depending on which set of rails carry the transaction – PIN Debit vs Signature Debit. And the lack of any PIN Debit networks around the contactless paradigm made the merchants fears real – that all debit transactions through NFC will be carried over the more costly signature debit route (favoring V/MA) and that a shift from magstripe to contactless would mean the end to another cost advantage the merchants had to steer transactions towards cheaper rails. The 13 or so PIN debit networks are missing from Apple Pay – and it’s an absence that weighed heavily in the merchants decision to be suspicious of it. Maybe even more important for the merchant – since it has little to do with payment – loyalty was a component that was inadequately addressed via NFC. NFC was effective as a secure communications channel – but was wholly inadequate when it came to transferring loyalty credentials, coupons and other things that justify why merchants would invest in a new technology in the first place. The contactless standards to move non-payment information, centered around ISO 18092 – and had fragmented acceptance in the retail space, and still struggled from a rather constricted pipe. NFC was simply useful as a payments standard and when it came to loyalty – the “invented a decade ago” standard is wholly inadequate to do anything meaningful at the point of sale. If the merchant must wrestle with new ways to do loyalty – then should they go back in time to enable payments, or should they jerry rig payments to be wrapped in to loyalty? What looks better to a merchant? Sending a loyalty token along with the payment credential (via ISO 18092) OR Encapsulating a payment token (as a QR Code) inside the Starbucks Loyalty App? I would guess – the latter. Even more so because in the scenario of accepting a loyalty token alongside an NFC payment – you are trusting the payment enabler (Apple, Google, Networks, Banks) with your loyalty token. Why would you? The reverse makes sense for a merchant. Finally – traditional NFC payments – (before Host Card Emulation in Android) – apart from being needlessly complex – mandated that all communication between the NFC capable device and the point-of-sale terminal be limited to the Secure Element that hosts the credential and the payment applets. Which means if you did not pay your way in to the Secure Element (mostly only due to if you are an issuer) then you have no play. What’s a merchant to do? So if you are a merchant – you are starting off with a disadvantage – as those terminologies and relationships are alien to you. Merchants did not own the credential – unless it was prepaid or private label – and even then, the economics wouldn’t make sense to put those in a Secure Element. Further, Merchants had no control in the issuer’s choice of credential in the Secure Element – which tended to be mostly credit. It was then no surprise that merchants largely avoided this channel – and then gradually started to look at it with suspicion around the same time banks and networks began to pre-ordain NFC as the next stage in payment acceptance evolution. Retailers who by then had been legally embroiled in a number of skirmishes on the interchange front – saw this move as the next land grab. If merchants could not cost effectively compete in this new channel – then credit was most likely to become the most prevalent payment option within. This suspicion was further reinforced with the launch of GoogleWallet, ISIS and now Apple Pay. Each of these wrapped existing rails, maintained status quo and allowed issuers and networks to bridge the gap from plastic to a new modality (smartphones) while changing little else. This is no mere paranoia. The merchants fear that issuers and networks will ultimately use the security and convenience proffered through this channel as an excuse to raise rates again. Or squeeze out the cheaper alternatives – as they did with defaulting to Signature Debit over PIN debit for contactless. As consumers learn a new behavior (tap and pay) they fear that magstripe will eclipse and a high cost alternative will then take root. How is it fair that to access their customer’s funds – our money – one has to go through toll gates that are incentivized to charge higher prices? The fact that there are little to no alternatives between using Cash or using a bank issued instrument to pay for things – should worry us as consumers. As long as merchants are complacent about the costs in place for them to access our money – there won’t be much of an incentive for banks to find quicker and cheaper ways to move money – in and out of the system as a whole. I digress. So the costs and complexities that I pointed to before, that existed in the NFC payments ecosystem – served to not only keep retailers out, but also impacted issuers ability to scale NFC payments. These costs materialized in to higher interchange cards for the issuer when these initiatives took flight – partly because the issuer was losing money already, and had then little interest to enable debit as a payments choice. GoogleWallet itself had to resort to a bit of “negative margin strategy” to allow debit cards to be used within. ISIS had little to no clout, nor any interest to push issuers to pick debit. All of which must have been quite vexing for an observant merchant. Furthermore, just as digital and mobile offers newer ways to interact with consumers – they also portend a new reality – that new ecosystems are taking shape across that landscape. And these ecosystems are hardly open – Facebook, Twitter, Google, Apple – and they have their own toll gates as well. Finally – A retail payment friend told me recently that merchants view the plethora of software, systems and services that encapsulate cross-channel commerce as a form of “Retailer OS”. And if Payment acceptance devices are end-points in to that closed ecosystem of systems and software – they are rightfully hesitant in handing over those keys to the networks and banks. The last thing they want to do is let someone else control those toll-gates. And it makes sense and ironically – it has parallel in the iOS ecosystem. Apple’s MFi program is an example of an ecosystem owner choosing to secure those end-points – especially when those are manufactured by a third party. This is why Apple exacts a toll and mandates that third party iOS accessory manufacturers must include an Apple IC to securely connect and communicate with an iOS device. If Apple can mandate that, then why is it that a retailer should have no say over the end-points through which payments occur in it’s own retail ecosystem? Too late to write about how the retailer view of NFC must evolve – in the face of an open standard, aided by Host Card Emulation – but that’s gotta be another post. Another time. See you all in Vegas. Make sure to join the Experian #MobilePayChat on Twitter this Tuesday at 12:15 p.m. PT during Money2020 conference: http://ex.pn/Money2020. If you are attending the event please stop by our booth #218. This post originally appeared here.

More than 10 years ago I spoke about a trend at the time towards an underutilization of the information being managed by companies. I referred to this trend as “data skepticism.” Companies weren’t investing the time and resources needed to harvest the most valuable asset they had – data. Today the volume and variety of data is only increasing as is the necessity to successfully analyze any relevant information to unlock its significant value. Big data can mean big opportunities for businesses and consumers. Businesses get a deeper understanding of their customers’ attitudes and preferences to make every interaction with them more relevant, secure and profitable. Consumers receive greater value through more personalized services from retailers, banks and other businesses. Recently Experian North American CEO Craig Boundy wrote about that value stating, “Data is Good… Analytics Make it Great.” The good we do with big data today in handling threats posed by fraudsters is the result of a risk-based approach that prevents fraud by combining data and analytics. Within Experian Decision Analytics our data decisioning capabilities unlock that value to ultimately provide better products and services for consumers. The same expertise, accurate and broad-reaching data assets, targeted analytics, knowledge-based authentication, and predictive decisioning policies used by our clients for risk-based decisioning has been used by Experian to become a global leader in fraud and identity solutions. The industrialization of fraud continues to grow with an estimated 10,000 fraud rings in the U.S. alone and more than 2 billion unique records exposed as a result of data breaches in 2014. Experian continues to bring together new fraud platforms to help the industry better manage fraud risk. Our 41st Parameter technology has been able to detect over 90% of all fraud attacks against our clients and reduce their operational costs to fight fraud. Combining data and analytics assets can detect fraud, but more importantly, it can also detect the good customers so legitimate transactions are not blocked. Gartner reported that by 2020, 40% of enterprises will be storing information from security events to analyze and uncover unusual patterns. Big data uncovers remarkable insights to take action for the future of our fraud prevention efforts but also can mitigate the financial losses associated with a breach. In the end we need more data, not less, to keep up with fraudsters. Experian is hosting Future of Fraud and Identity events in New York and San Francisco discussing current fraud trends and how to prevent cyber-attacks aimed at helping the industry. The past skepticism no longer holds true as companies are realizing that data combined with advanced analytics can give them the insight they need to prevent fraud in the future. Learn more on how Experian is conquering the world of big data.

If rumors hold true, Apple Pay will launch in a week. Five of my last six posts had covered Apple’s likely and actual strategy in payments & commerce, and the rich tapestry of control, convenience, user experience, security and applied cryptography that constitutes as the backdrop. What follows is a summation of my views – with a couple of observations from having seen the Apple Pay payment experience up close. About three years ago – I published a similar commentary on Google Wallet that for kicks, you can find here. I hope what follows is a balanced perspective, as I try to cut through some FUD, provide some commentary on the payment experience, and offer up some predictions that are worth the price you pay to read my blog. Source: Bloomua / Shutterstock.com First the criticism. Apple Pay doesn’t go far enough: Fair. But you seem to misunderstand Apple’s intentions here. Apple did not set out to make a mobile wallet. Apple Pay sits within Passbook – which in itself is a wrapper of rewards and loyalty cards issued by third parties. Similarly – Apple Pay is a wrapper of payments cards issued by third parties. Even the branding disappears once you provision your cards – when you are at the point-of-sale and your iPhone6 is in proximity to the reader (or enters the magnetic field created by the reader) – the screen turns on and your default payment card is displayed. One does not need to launch an app or fiddle around with Apple Pay. And for that matter, it’s even more limited than you think. Apple’s choice to leave the Passbook driven Apple Pay experience as threadbare as possible seems an intentional choice to force consumers to interact more with their bank apps vs Passbook for all and any rich interaction. Infact the transaction detail displayed on the back of the payment card you use is limited – but you can launch the bank app to view and do a lot more. Similarly – the bank app can prompt a transaction alert that the consumer can select to view more detail as well. Counter to what has been publicized – Apple can – if they choose to – view transaction detail including consumer info, but only retains anonymized info on their servers. The contrast is apparent with Google – where (during early Google Wallet days) issuers dangled the same anonymized transaction info to appease Google – in return for participation in the wallet. If your tap don’t work – will you blame Apple? Some claim that any transaction failures – such as a non-working reader – will cause consumers to blame Apple. This does not hold water simply because – Apple does not get in between the consumer, his chosen card and the merchant during payment. It provides the framework to trigger and communicate a payment credential – and then quietly gets out of the way. This is where Google stumbled – by wanting to become the perennial fly on the wall. And so if for whatever reason the transaction fails, the consumer sees no Apple branding for them to direct their blame. (I draw a contrast later on below with Samsung and LoopPay) Apple Pay is not secure: Laughable and pure FUD. This article references an UBS note talking how Apple Pay is insecure compared to – a pure cloud based solution such as the yet-to-be-launched MCX. This is due to a total misunderstanding of not just Apple Pay – but the hardware/software platform it sits within (and I am not just talking about the benefits of a TouchID, Network Tokenization, Issuer Cryptogram, Secure Element based approach) including, the full weight of security measures that has been baked in to iOS and the underlying hardware that comes together to offer the best container for payments. And against all that backdrop of applied cryptography, Apple still sought to overlay its payments approach over an existing framework. So that, when it comes to risk – it leans away from the consumer and towards a bank that understands how to manage risk. That’s the biggest disparity between these two approaches – Apple Pay and MCX – that, Apple built a secure wrapper around an existing payments hierarchy and the latter seeks to disrupt that status quo. Let the games begin: Consumers should get ready for an ad blitz from each of the launch partners of Apple Pay over the next few weeks. I expect we will also see these efforts concentrated around pockets of activation – because setting up Apple Pay is the next step to entering your Apple ID during activation. And for that reason – each of those launch partners understand the importance of reminding consumers why their card should be top of mind. There is also a subtle but important difference between top of wallet card (or default card) for payment in Apple Pay and it’s predecessors (Google Wallet for example). Changing your default card was an easy task – and wholly encapsulated – within the Google Wallet app. Where as in Apple Pay – changing your default card – is buried under Settings, and I doubt once you choose your default card – you are more likely to not bother with it. And here’s how quick the payment interaction is within Apple Pay (takes under 3 seconds) :- Bring your phone in to proximity of the reader. Screen turns on. Passbook is triggered and your default card is displayed. You place your finger and authenticate using TouchID. A beep notes the transaction is completed. You can flip the card to view a limited transaction detail. Yes – you could swipe down and choose another card to pay. But unlikely. I remember how LevelUp used very much the same strategy to signup banks – stating that over 90% of it’s customers never change their default card inside LevelUp. This will be a blatant land grab over the next few months – as tens of millions of new iPhones are activated. According to what Apple has told it’s launch partners – they do expect over 95% of activations to add at least one card. What does this mean to banks who won’t be ready in 2014 or haven’t yet signed up? As I said before – there will be a long tail of reduced utility – as we get in to community banks and credit unions. The risk is amplified because Apple Pay is the only way to enable payments in iOS that uses Apple’s secure infrastructure – and using NFC. For those still debating whether it was a shotgun wedding, Apple’s approach had five main highlights that appealed to a Bank – Utilizing an approach that was bank friendly (and to status quo) : NFC Securing the transaction beyond the prerequisites of EMV contactless – via network tokenization & TouchID Apple’s preference to stay entirely as an enabler – facilitating a secure container infrastructure to host bank issued credentials. Compressing the stack: further shortening the payment authorization required of the consumer by removing the need for PIN entry, and not introducing any new parties in to the transaction flow that could have introduced delays, costs or complexity in the roundtrip. Clear description of costs to participate – Free is ambiguous. Free leads to much angst as to what the true cost of participation really is(Remember Google Wallet?). Banks prefer clarity here – even if it means 15bps in credit. As I wrote above, Apple opting to strictly coloring inside the lines – forces the banks to shoulder much of the responsibility in dealing with the ‘before’ and ‘after’ of payment. Most of the bank partners will be updating or activating parts of their mobile app to start interacting with Passbook/Apple Pay. Much of that interaction will use existing hooks in to Passbook – and provide richer transaction detail and context within the app. This is an area of differentiation for the future – because those banks who lack the investment, talent and commitment to build a redeeming mobile services approach will struggle to differentiate on retail footprint alone. And as smarter banks build entirely digital products for an entirely digital audience – the generic approaches will struggle and I expect at some point – that this will drive bank consolidation at the low end. On the other hand – if you are an issuer, the ‘before’ and ‘after’ of payments that you are able to control and the richer story you are able to weave, along with offline incentives – can aid in recapture. The conspicuous and continued absence of Google: So whither Android? Uniformity in payments for Android is as fragmented as the ecosystem itself. Android must now look at Apple for lessons in consistency. For example, how Apple uses the same payment credential that is stored in the Secure Element for both in-person retail transactions as well as in-app payments. It may look trivial – but when you consider that Apple came dangerously close (and justified as well) in its attempt to obtain parity between those two payment scenarios from a rate economics point of view from issuers – Android flailing around without a coherent strategy is inexcusable. I will say this again: Google Wallet requires a reboot. And word from within Google is that a reboot may not imply a singular or even a cohesive approach. Google needs to swallow its pride and look to converge the Android payments and commerce experience across channels similar to iOS. Any delay or inaction risks a growing apathy from merchants who must decide what platform is worth building or focusing for. Risk vs Reward is already skewed in favor of iOS: Even if Apple was not convincing enough in its attempt to ask for Card Present rates for its in-app transactions – it may have managed to shift liability to the issuer similar to 3DS and VBV – that in itself poses an imbalance in favor of iOS. For a retail app in iOS – there is now an incentive to utilize Apple Pay and iOS instead of all the other competing payment providers (Paypal for example, or Google Wallet) because transactional risk shifts to the issuer if my consumer authenticates via TouchID and uses a card stored in Apple Pay. I have now both an incentive to prefer iOS over Android as well as an opportunity to compress my funnel – much of my imperative to collect data during the purchase was an attempt to quantify for fraud risk – and the need for that goes out of the window if the customer chooses Apple Pay. This is huge and the repercussions go beyond Android – in to CNP fraud, CRM and loyalty. Networks, Tokens and new end-points (e.g. LoopPay): The absence of uniformity in Android has provided a window of opportunity for others – regardless of how fragmented these approaches be. Networks shall parlay the success with tokenization in Apple Pay in to Android as well, soon. Prime example being: Loop Pay. If as rumors go – Samsung goes through with baking in Loop Pay in to its flagship S6, and Visa’s investment translates in to Loop using Visa tokenization – Loop may find the ubiquity it is looking for – on both ends. I don’t necessarily see the value accrued to Samsung for launching a risky play here: specifically because of the impact of putting Loop’s circuitry within S6. Any transaction failure in this case – will be attributed to Samsung, not to Loop, or the merchant, or the bank. That’s a risky move – and I hope – a well thought out one. I have some thoughts on how the Visa tokenization approach may solve for some of the challenges that Loop Pay face on merchant EMV terminals – and I will share those later. The return of the comeback: Reliance on networks for tokenization does allay some of the challenges faced by payment wrappers like Loop, Coin etc – but they all focus on the last mile and tokenization does little more for them than kicking the can down the road and delaying the inevitable a little while more. The ones that benefit most are the networks themselves – who now has wide acceptance of their tokenization service – with themselves firmly entrenched in the middle. Even though the EMVCo tokenization standard made no assumptions regarding the role of a Token Service Provider – and in fact Issuers or 3rd parties could each pay the role sufficiently well – networks have left no room for ambiguity here. With their role as a TSP – networks have more to gain from legitimizing more end points than ever before – because these translate to more token traffic and subsequently incremental revenue – transactional and additional managed services costs (OBO – On behalf of service costs incurred by a card issuer or wallet provider). It has never been a better time to be a network. I must say – a whiplash effect for all of us – who called for their demise with the Chase-VisaNet deal. So my predictions for Apple Pay a week before its launch: We will see a substantial take-up and provisioning of cards in to Passbook over the next year. Easy in-app purchases will act as the carrot for consumers. Apple Pay will be a quick affair at the point-of-sale: When I tried it few weeks ago – it took all of 3 seconds. A comparable swipe with a PIN (which is what Apple Pay equates to) took up to 10. A dip with an EMV card took 23 seconds on a good day. I am sure this is not the last time we will be measuring things. The substantial take-up on in-app transactions will drive signups: Consumers will signup because Apple’s array of in-app partners will include the likes of Delta – and any airline that shortens the whole ticket buying experience to a simple TouchID authentication has my money. Apple Pay will cause MCX to fragment: Even though I expect the initial take up to be driven more on the in-app side vs in-store, as more merchants switch to Apple Pay for in-app, consumers will expect a consistency in that approach across those merchants. We will see some high profile desertions – driven partly due to the fact that MCX asks for absolute fealty from its constituents, and in a rapidly changing and converging commerce landscape – that’s just a tall ask. In the near-term, Android will stumble: Question is if Google can reclaim and steady its own strategy. Or will it spin off another costly experiment in chasing commerce and payments. The former will require it to be pragmatic and bring ecosystem capabilities up to par – and that’s a tall ask when you lack the capacity for vertical integration that Apple has. And from the looks of it – Samsung is all over the place at the moment. Again – not confidence inducing. ISIS/SoftCard will get squeezed out of breath: SoftCard and GSMA can’t help but insert themselves in to the Apple Pay narrative by hoping that the existence of a second NFC controller on the iPhone6 validates/favors their SIM based Secure Element approach and indirectly offers Softcard/GSMA constituents a pathway to Apple Pay. If that didn’t make a lick of sense – It’s like saying ‘I’m happy about my neighbor’s Tesla because he plugs it in to my electric socket’. Discover how an Experian business consultant can help you strengthen your credit and risk management strategies and processes: http://ex.pn/DA_GCP This post originally appeared here.

According to a recent Experian Data Quality study, three out of four organizations personalize their marketing messages or are in the process of doing so.