Financial Services

In this article...What is reject inference? How can reject inference enhance underwriting? Techniques in reject inference Enhancing reject inference design for better classification How Experian can assist with reject inference In the lending world, making precise underwriting decisions is key to minimizing risks and optimizing returns. One valuable yet often overlooked technique that can significantly enhance your credit underwriting process is reject inferencing. This blog post offers insights into what reject inference is, how it can improve underwriting, and various reject inference methods. What is reject inference? Reject inference is a statistical method used to predict the potential performance of applicants who were rejected for a loan or credit — or approved but did not book. In essence, it helps lenders and financial institutions gauge how rejected or non-booked applicants might have performed had they been accepted or booked. By incorporating reject inference, you gain a more comprehensive view of the applicant pool, which leads to more informed underwriting decisions. Utilizing reject inference helps reduce biases in your models, as decisions are based on a complete set of data, including those who were initially rejected. This technique is crucial for refining credit risk models, leading to more accurate predictions and improved financial outcomes. How can reject inference enhance underwriting? Incorporating reject inference into your underwriting process offers several advantages: Identifying high-potential customers: By understanding the potential behavior of rejected applicants, you can uncover high-potential customers who might have been overlooked before. Improved risk assessment: Considering the full spectrum of applicants provides a clearer picture of the overall risk landscape, allowing for more informed lending decisions. This can help reduce default rates and enhance portfolio performance. Optimizing credit decisioning models: Including inferred data from rejected and non-booked applicants makes your credit scoring models more representative of the entire applicant population. This results in more robust and reliable predictions. Techniques in reject inference Several techniques are employed in reject inference, each with unique strengths and applications. Understanding these techniques is crucial for effectively implementing reject inference in your underwriting process. Let's discuss three commonly used techniques: Parceling: This technique involves segmenting rejected applicants based on their characteristics and behaviors, creating a more detailed view of the applicant pool for more precise predictions. Augmentation: This method adds inferred data to the dataset of approved applicants, producing a more comprehensive model that includes both approved and inferred rejected applicants, leading to better predictions. Reweighting: This technique adjusts the weights of approved applicants to reflect the characteristics of rejected applicants, minimizing bias towards the approved applicants and improving prediction accuracy. Pre-diction method The pre-diction method is a common approach in reject inference that uses data collected at the time of application to predict the performance of rejected applicants. The advantage of this method is its reliance on real-time data, making it highly relevant and current. For example, pre-diction data can include credit bureau attributes from the time of application. This method helps develop a model that predicts the outcomes of rejected applicants based on performance data from approved applicants. However, it may not capture long-term trends and could be less effective for applicants with unique characteristics. Post-diction method The post-diction method uses data collected after the performance window to predict the performance of rejected applicants. Leveraging historical data, this method is ideal for capturing long-term trends and behaviors. Post-diction data may include credit bureau attributes from the end of the performance window. This method helps develop a model based on historical performance data, which is beneficial for applicants with unique characteristics and can lead to higher performance metrics. However, it may be less timely and require more complex data processing compared to pre-diction. Enhancing reject inference design for better classification To optimize your reject inference design, focus on creating a model that accurately classifies the performance of rejected and non-booked applicants. Utilize a combination of pre-diction and post-diction data to capture both real-time and historical trends. Start by developing a parceling model using pre-diction data, such as credit bureau attributes from the time of application, to predict rejected applicants' outcomes. Regularly update your model with the latest data to maintain its relevance. Next, incorporate post-diction data, including attributes from the end of the performance window, to capture long-term trends. Combining both data types will result in a more comprehensive model. Consider leveraging advanced analytics techniques like machine learning and artificial intelligence to refine your model further, identifying hidden patterns and relationships for more accurate predictions. How Experian can assist with reject inference Reject inference is a powerful tool for enhancing your underwriting process. By predicting the potential performance of rejected and non-booked applicants, you can make more inclusive and accurate decisions, leading to improved risk assessment and optimized credit scoring models. Experian offers various services and solutions to help financial institutions and lenders effectively implement reject inference into their decisioning strategy. Our solutions include comprehensive and high-quality datasets, which empower you to build models that are more representative of the entire applicant population. Additionally, our advanced analytics tools simplify data analysis and model development, enabling you to implement reject inference efficiently without extensive technical expertise. Ready to elevate your underwriting process? Contact us today to learn more about our suite of advanced analytics solutions or hear what our experts have to say in this webinar. Watch Webinar Learn More This article includes content created by an AI language model and is intended to provide general information.

Replay attacks may threaten your customers’ online security Today, consumer online security is more important than ever. This year, the FTC has already received nearly six million reports of fraud, and 1.4 million of those cases were specifically identity theft.[1] In addition, a recent study reported that losses due to identity fraud amounted to almost $23 billion in 2023.[2] And consumers aren’t the only ones at risk. According to CyberArk’s global research report, 93% of organizations had two or more identity-related breaches in the past year.[3] This means it’s not only up to consumers to protect themselves against identity theft. It’s also up to businesses to protect themselves and their customers from the threat of fraud. As security technology advances, so do the tactics of hackers attempting to steal information such as usernames, account numbers, and passwords from innocent online users. One method that hackers use to obtain this information is called a replay attack, which can pose a serious threat to your customers’ online security. What is a replay attack? A replay attack is a network-based security hack in which a hacker intercepts legitimate data transmission and then fraudulently repeats it to gain access to a network or system. These attacks are designed to fool the victim into believing the hacker is a genuine user, and they happen in three steps: Eavesdropping: The hacker listens in on secure network communications, such as information sent through a Virtual Private Network (VPN), to learn about the activity happening on that network. Interception: The hacker intercepts legitimate user information – usernames, user activity, computer specs, passwords, etc. Replay: The hacker illegally resends (or “replays”) the valid information they gathered to trick the receiver into thinking that they are a genuine user. Here’s an example: John transfers funds from one online banking account to another. A hacker illegally captures that transaction message (which is often accompanied by a digital signature or token) and “replays” that same transaction message multiple times to trigger additional fund transfers, all without the genuine user’s knowledge or permission. The bank doesn’t recognize a problem because the “replayed” transaction messages includes the legitimate digital signature/token, so the bank approves the additional transfers. Replay attacks aren’t just used for banking transactions. They can be used for various activities, such as: Internet of Things (IoT) device attacks: IoT devices include a multitude of “smart home” devices such as smart plugs, cameras, locks, appliances, speakers, lights, and more. Vulnerabilities in these devices can allow hackers to replicate commands to these devices that seem legitimate, such as turning on cameras, unlocking doors, and disabling security systems.[4] Remote keyless entry systems for vehicles: Most vehicles use a remote key fob to lock and unlock the doors. This key fob usually uses radio waves to send the lock/unlock signal to the car. Hackers can use a device to receive and transmit radio waves near a person’s vehicle that mimic that same lock/unlock signal, and then “replay” that signal to unlock the person’s car themselves.[5] Text-dependent speaker verification: Some people use voice recognition to verify their identity when accessing an account or system. Hackers can record a person’s voice when the person speaks to verify their identity, and then “replay” that voice recording to fraudulently access the account.[6] How to prevent replay attacks Replay attacks are dangerous because they are often unnoticed or overlooked until the damage has already been done. Fortunately, there are ways to stop hackers from using replay attacks to access your customers’ personal information. Device intelligence: By leveraging unique intelligence about the device being used, replay attacks can be thwarted even when fraudsters are using authentic, but stolen, information. Time stamping: By forcing a timestamp on all sent and received messages, you can prevent hackers from sending repeated messages with legitimate information obtained illegally. Geolocation review: By identifying suspicious language and/or time zones, you can compare access routes to confirm customers are authentic and secure. Why it matters for your business Consumers in the U.S. value network security more than ever, with 70% rating security a top priority, even over personalization and convenience.[7] People want to feel safe online, and if they experience a threat of identity theft or fraud, they’ll need to find a reliable resource to keep their personal information secure. Successful replay attacks allow fraudsters to impersonate real users and potentially gain partial or full access to their personal online accounts. If your customers fall victim to these kinds of attacks, the resulting stress may have a negative impact on your relationship with them. With our fraud management solutions, your business can strengthen your customers’ trust and security by leveraging highly trained fraud analysts to help uncover suspicious activity that might not be noticed otherwise. Lower fraud losses and achieve fraud capture rates that exceed industry averages. Protect your customers by using a covert, frictionless solution the reduces false positives. Improve operational efficiency by prioritizing resources across the board. Protect your consumers with powerful fraud management solutions 63% of consumers say it’s important for businesses to be able to recognize them online, and 81% say they are more trusting of businesses that can accomplish easy and accurate identification.[8] While replay attacks can cause consumers stress and anxiety, taking action to prevent them can fortify a strong, trusting relationship between your business and your customers. Protect your customers and prevent replay attacks with our powerful fraud management solutions. Get started [1] IdentityTheft.org, 2024 Identity Theft Facts and Statistics. [2] Javelin, 2024 Identity Fraud Study: Resolving the Shattered Identity Crisis. [3] CyberArk, Report: 93% of Organizations Had Two or More Identity-Related Breaches in the Past Year, May 2024. [4] Hackster.io, IoT Devices May Be Susceptible to Replay Attacks with a Raspberry Pi and RTL-SDR Dongle, 2017. [5] Automotive World, How to mitigate vulnerabilities in keyless entry systems, 2023. [6] Antispoofing, Audio Replay Attacks and Countermeasures Against Them, 2022. [7] 2018 Experian® Global Fraud Report [8] Experian® 2024 Identity and Fraud Report Highlights Evolving Fraud Landscape This article includes content created by an AI language model and is intended to provide general information.

This series will dive into our monthly State of the Economy report, providing a snapshot of the top monthly economic and credit data for those in financial services to proactively shape their business strategies. The labor market has been a source of strength for the U.S. economy coming out of the pandemic, providing workers with stable employment and solid wages. However, the labor market has slowed in recent months, with lower-than-expected job creation and rising unemployment, causing weakening sentiment in the broader market. This has resulted in increased pressure on the Federal Reserve to begin cutting rates and places more importance on the incoming data between now and the September FOMC meeting. Data highlights from this month’s report include: Job creation declined in July, falling short of economists’ expectations. Unemployment increased from 4.1% to 4.3%. Inflation cooled again in July, with annual headline inflation easing from 3.0% to 2.9%. GDP picked up in Q2 to 2.8%, primarily driven by strong consumer spending. Check out our report for a deep dive into the rest of this month’s data, including the latest trends in originations, retail sales, and the new housing market. Download August's report To have a holistic view of our current environment, it’s important to view the economy from different angles and through different lenses. Download our latest macroeconomic forecasting report for our views on what's to come in the U.S. economy and listen to our latest Econ to Action podcast. For more economic trends and market insights, visit Experian Edge.

Alternative lending is continuing to revolutionize the financial services landscape. From full-file public records to cash flow transactions, alternative credit data empowers financial institutions to make more informed lending decisions. This article focuses on cash flow insights and how they help financial institutions drive profitable and inclusive growth. Challenges with traditional credit underwriting Traditional underwriting often limits access to credit for marginalized communities, including young adults, immigrants, and those from low-income backgrounds. Because the process relies heavily on credit history and credit scores to determine an applicant’s ability to pay, those with less-than-ideal credit profiles could be overlooked. This then creates a cycle — those who are already disadvantaged face further barriers to accessing credit, limiting their abilities to invest in opportunities that can improve their financial situations, such as education or homeownership. Additionally, traditional underwriting models can be rigid. Consumers with stable incomes or significant assets may be denied credit if their financial profiles don’t fit the narrow criteria established by traditional models. As the financial landscape evolves, it’s important for lenders to adopt more inclusive and adaptive approaches to credit underwriting. What is cash flow underwriting? Cash flow underwriting is a modern approach to evaluating a borrower’s creditworthiness. It uses fresh, consumer-permissioned bank account transaction (balance, income and expense) data, giving lenders greater visibility into loan applicants’ financial situation. This process is made possible through open banking, an established, secure framework that enables consumers to quickly and easily share their bank account information with third-party financial service providers. READ: Learn more about the open banking landscape. Let’s look at a few quick examples: A prospective tenant is filling out a rental application. Instead of manually submitting paystubs to verify their income, open banking facilitates the digital sharing of full cash flow data in seconds, enabling property managers to quickly access the applicant’s full cash flow information. A consumer was previously denied credit due to insufficient credit history. With cash flow underwriting, the consumer is offered a second chance to qualify for the loan by including cash flow data in the lender’s decisioning model. The additional information gathered on the consumer’s ability to pay can transform the initial decline decision into an approval. Cash flow underwriting can also be used for credit line management. By assessing a borrower’s income and expense transactions, lenders can recommend optimal credit limits that cater to their spending potential while minimizing risk. Benefits of cash flow underwriting There are many benefits to integrating cash flow data into the credit underwriting process, including: Enhanced risk assessment. Going off credit scores and repayment behaviors alone won’t provide lenders with a complete or current picture of applicants. Through open banking, lenders can gain access to cash flow data in real-time, allowing them to more accurately assess consumers, increase approvals, and reduce credit risk. Inclusive lending. Millions of American adults are considered unscoreable, invisible, or subprime. However, 71% of consumers are willing to share their banking information if it could improve their chances of getting approved for credit.1 With deeper insights into consumers’ income and expenses, lenders can increase credit access in underserved communities. Improved customer experiences. Gaining a more comprehensive view of a consumer’s financial situation enables lenders to determine what loan products they’re eligible for and craft personalized options. READ: Learn more about the benefits of leveraging alternative data for credit underwriting. Get started Cash flow underwriting represents a significant step forward in the world of lending. It offers a more comprehensive approach to assessing creditworthiness, helping financial institutions drive growth and profitability. Cashflow Attributes are one of Experian's open banking solutions that provides lenders with consumer-permissioned insights into borrowers’ financial behaviors. With 940+ attributes derived from transaction data across 133 categories, financial institutions can make smarter, more inclusive lending decisions. Learn more about Cashflow Attributes Learn more about open banking 1Atomik Research survey of 2,005 U.S. adults online, matching national demographics, 2024.

Gen Z, or "Zoomers," born from 1997 to 2012, are molded by modern transformations. They have witnessed events from post-9/11 impacts to the rise of the internet and the COVID-19 crisis. As early adopters of technology, their lives are intertwined with smartphones, online shopping, social platforms, cloud services, emerging fintech, and artificial intelligence. They are called “digital natives” as they are the first generation to grow up with internet as part of their daily life. Research generally indicates that this post-millennial generation values practicality, favoring financial stability over entrepreneurial pursuits. They appreciate communication tailored to them and often employ social media to cultivate their personal brands. As a generation growing up immersed in technology, they tend to choose digital interactions, seeking to forge robust, secure, genuine, and unconstrained digital experiences. The challenge of identity verification Identity verification presents a considerable challenge for Generation Z. According to a Fortune survey, close to 50% of this demographic regrets not opening financial accounts earlier, citing a lack of readiness to join the financial ecosystem by the age of 18. Consequently, this has given rise to "digital ghosts"—people with minimal or nonexistent financial histories who face challenges when trying to utilize financial services. The 2009 Credit Card Accountability Responsibility and Disclosure Act mandates that individuals under 21 need a cosigner or show income proof to get a credit card, hindering their early financial involvement. Moreover, conventional identity checks are becoming less reliable due to the surge in identity theft. Innovative solutions for verifying Gen Z Verifying identities and preventing fraud among Gen Z presents unique challenges due to their digital-native status and limited credit histories. Here are some effective strategies and approaches that financial institutions can adopt to address these challenges: Leveraging alternative data sources Academic records leverage information from higher learning institutions such as universities, colleges, and vocational schools. This data can be vital for authenticating the identities of younger individuals who may lack a substantial credit history. Employment verification retrieve data confirming the identity and employment status, especially focusing on Gen Z who are new to the job market. Utility and telecom records leverage payment histories for utilities, phone bills, and other recurring services, which can provide additional layers of identity verification. Alternative financial data includes online small dollar lenders, online installment lenders, single payment, line of credit, storefront small dollar lenders, auto title and rent-to-own. Phone-Centric ID Phone-Centric Identity refers to technology that leverages and analyzes mobile, telecom, and other signals for the purposes of identity verification, identity authentication, and fraud prevention. Phone-Centric Identity relies on billions of signals from authoritative sources pulled in real time, making it a powerful proxy for digital identity and trust. Advance authentication technologies Behavioral biometrics analyze user behaviors such as typing patterns, navigation habits, and device usage. These subtle behaviors can help create a unique profile for each user, making it difficult for fraudsters to impersonate them. Adaptive risk-based authentication that adjusts the level of security based on the user's behavior, location, device, and other factors. For example, a higher level of verification might be required for transactions that are deemed unusual or high-risk. Real-time fraud detection AI and machine learning: Deploy AI and machine learning algorithms to analyze transaction patterns and detect anomalies in real-time. These technologies can identify suspicious activities and flag potential fraud. Fraud analytics: Use predictive analytics to assess the likelihood of fraud based on historical data and current behavior. This approach helps in proactively identifying and mitigating fraudulent activities. Secure digital onboarding Digital identity verification: Implement digital onboarding processes that include online identity verification with real-time document verification. Users can upload government-issued IDs and take selfies to confirm their identity. Video KYC (Know Your Customer): Use video calls to conduct KYC processes, allowing bank representatives to verify identities and documents remotely via automated identity verification. This method is secure and convenient for tech-savvy Gen Z customers. Make identity verification easy To authenticate identities and combat fraud within the Gen Z population, financial organizations need to implement a comprehensive strategy utilizing innovative technologies, non-traditional data, and strong protective protocols. Such actions will enable the creation of a trustworthy and frictionless banking environment that appeals to a generation adept in digital interactions, thereby establishing trust and encouraging enduring connections. To learn more about Experian’s automated identity verification solutions, visit our website. Learn more

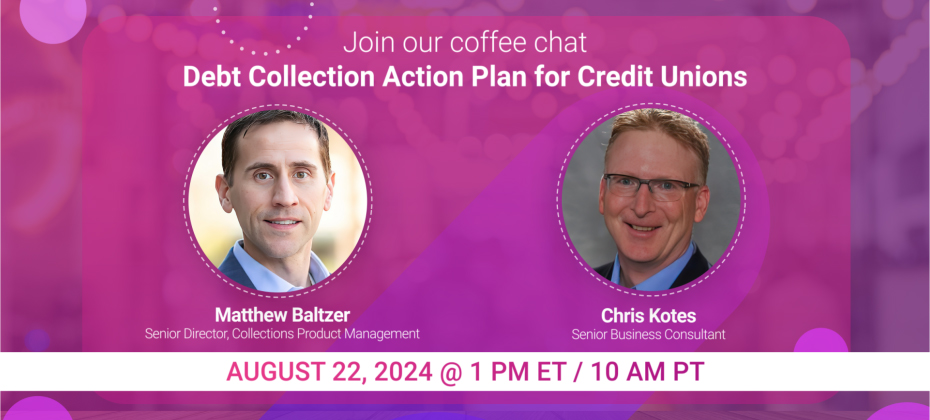

With the noticeable uptick in delinquencies, credit unions face more significant hurdles in effectively managing overdue accounts. In this challenging financial landscape, it’s imperative that you refine your account management processes to remain competitive, preserve the well-being of your members, assure operational efficiency, and increase profitability. Implementing efficient collection approaches not only improves loss rates but also helps with member retention, which is the backbone of your success. Grab a cup of coffee and join our experts on August 22 @ 1:00 p.m. ET/ 10:00 a.m. PT, for an engaging conversation on credit union collection trends and successful account management strategies. Highlights include: Current landscape: Gain valuable insight and understanding into the current debt collection environment for credit unions. Navigating challenges: Discover effective tips and strategies to tackle obstacles in your business, improve loss rates, and enhance member retention. Real-time Q&A: Participate in a live Q&A session where our experts will address your questions. Watch on-demand

Getting customers to respond to your credit offers can be difficult. With the advent of artificial intelligence (AI) and machine learning (ML), optimizing credit prescreen campaigns has never been easier or more efficient. In this post, we'll explore the basics of prescreen and how AI and ML can enhance your strategy. What is prescreen? Prescreen involves evaluating potential customers to determine their eligibility for credit offers. This process takes place without the consumer’s knowledge and without any negative impact on their credit score. Why optimize your prescreen strategy? In today's financial landscape, having an optimized prescreen strategy is crucial. Some reasons include: Increased competition: Financial institutions face stiff competition in acquiring new customers. An optimized prescreen strategy helps you stand out by targeting the right individuals with tailored offers, increasing the chances of conversion. Customer expectations: Modern customers expect personalized and relevant offers. An effective prescreen strategy ensures that your offers resonate with the specific needs and preferences of potential customers. Strict budgets: Organizations today are faced with a limited marketing budget. By determining the right consumers for your offers, you can minimize prescreen costs and maximize the ROI of your campaigns. Regulatory compliance: Compliance with regulations such as the Fair Credit Reporting Act (FCRA) is essential. An optimized prescreen strategy helps you stay compliant by ensuring that only eligible individuals are targeted for credit offers. Financial inclusion: 49 million American adults don’t have conventional credit scores. An optimized prescreen strategy allows you to send offers to creditworthy consumers who you may have missed due to a lack of traditional credit history. How AI and ML can enhance your strategy AI and ML can revolutionize your prescreen strategy by offering advanced analytics and custom response modeling capabilities. AI-driven data analytics AI analytics allow financial institutions to analyze vast amounts of data quickly and accurately. This enables you to identify patterns and trends that may not be apparent through traditional analysis. By leveraging data-centric AI, you can gain deeper insights into customer behavior and preferences, allowing for more precise targeting and increased response rates. LEARN MORE: Explore the benefits of AI for credit unions. Custom response modeling Custom response models enable you to better identify individuals who fall within your credit criteria and are more likely to respond to your credit offers. These models consider various factors such as credit history, spending habits, and demographic information to predict future behavior. By incorporating custom response models into your prescreen strategy, you can select the best consumers to engage, including those you may have previously overlooked. LEARN MORE: AI can be leveraged for numerous business needs. Learn about generative AI fraud detection. Get started today Incorporating AI and ML into your prescreen campaigns can significantly enhance their effectiveness and efficiency. By leveraging Experian's Ascend Intelligence Services™ Target, you can better target potential customers and maximize your marketing spend. Our optimized prescreen solution leverages: Full-file credit bureau data on over 245 million consumers and over 2,100 industry-leading credit attributes. Exclusive access to the industry's largest alternative datasets from nontraditional lenders, rental data inputs, full-file public records, and more. 24 months of trended data showing payment patterns over time and over 2,000 attributes that help determine your next best action. When it comes to compliance, Experian leverages decades of regulatory experience to provide the documentation needed to explain lending practices to regulators. We use patent-pending ML explainability to understand what contributed most to a decision and generate adverse action codes directly from the model. For more insights into Ascend Intelligence Services Target, view our infographic or contact us at 855 339 3990. View infographic This article includes content created by an AI language model and is intended to provide general information.

This series will dive into our monthly State of the Economy report, providing a snapshot of the top monthly economic and credit data for those in financial services to proactively shape their business strategies. While much of the economic data released this month remained steady, including continued downward progress in inflation and resilience in inflation-adjusted spending, June was a pivotal month for the labor market. With downward revisions to job creation over the past few months to an up-tick in unemployment, the potential for a sooner-than-expected rate cut increased. Data highlights from this month’s report include: While above economists’ expectations in June, job creation was 111,000 jobs shy of what was recorded in April and May, signaling some slowdown in the labor market. Inflation-adjusted spending and incomes increased in May, by 0.3% and 0.5%, respectively. Inflation eased more than economists expected, with annual headline inflation cooling from 3.3% to 3.0%. Check out our report for a deep dive into the rest of this month’s data, including the latest trends in job openings, new business survival rates, and bankcard delinquency rates. Download July's report To have a holistic view of our current environment, it’s important to view the economy from different angles and through different lenses. Watch our experts discuss the latest economic and credit trends in the next macroeconomic forecasting webinar and listen to our latest Econ to Action podcast. For more economic trends and market insights, visit Experian Edge.

With rising consumer debt and an increasing number of consumers defaulting on loans, effective debt recovery strategies have never been more critical. Skip-tracing is the first-step in effective debt collection. This essential practice helps locate individuals who have become difficult to find, ensuring that you can recover outstanding debts efficiently. In this blog post, we'll explore skip-tracing best practices, offering valuable insights and practical tips and tools. Understanding and implementing these collection strategies can enhance your debt recovery efforts, improve overall efficiency, and increase your recovery rates. Understanding the importance of skip-tracing Skip-tracing is the process of locating individuals who have moved or otherwise become difficult to find. This technique is particularly important for financial institutions and debt collectors, enabling them to contact debtors and recover outstanding payments. Given the high stakes involved, mastering skip-tracing best practices is crucial for ensuring successful debt recovery. How to create an effective skip-tracing strategy 1. Use comprehensive skip-tracing data sources One of the foundational elements of an effective skip-tracing strategy is the use of comprehensive skip-tracing data sources. You can gather valuable information about a debtor's whereabouts by leveraging multiple databases, including public records, credit reports, and alternative data sources. The more data sources you utilize, the better chance of making right-party contact. 2. Prioritize data privacy While skip-tracing is essential for debt recovery, it's crucial to prioritize data privacy. Always adhere to the latest consumer contact debt collection regulations. This protects the individual's privacy and safeguards your organization from potential legal issues. 3. Stay updated with regulatory changes The regulatory landscape for debt collection and contacting consumers is constantly evolving. Staying updated with the latest changes ensures that your skip-tracing practices remain compliant with the law. Regularly review industry regulations, obtain proper consent from consumers and adjust your strategies accordingly. 4. Train your team Skip-tracing requires specialized skills and knowledge. Investing in regular training for your team ensures that they are equipped with the latest techniques and best practices. Offer workshops, webinars, and certification programs to keep your team up to date and improve their effectiveness. 5. Utilize skip-tracing software Skip-tracing software can significantly streamline the process and improve accuracy. Look for software solutions that offer comprehensive data integration, advanced search capabilities, and user-friendly interfaces. Implementing the right software can save time and resources while increasing right-party contact. 6. Monitor and evaluate performance Regularly monitoring and evaluating the performance of your skip-tracing efforts is essential for continuous improvement. Track key metrics such as right-party contact rates, time taken to locate individuals, contact method and cost. Use this data to identify areas for improvement and adjust your strategies accordingly. 7. Adapt to changing circumstances The world of debt management is dynamic, and circumstances can change rapidly. Be prepared to adapt your skip-tracing strategies to evolving situations. Whether it's changes in debtor behavior, new technology, or shifts in the regulatory landscape, staying flexible ensures that your skip-tracing efforts remain effective. Why choose Experian® for skip-tracing solutions Skip-tracing is a critical tool for financial institutions and debt collectors, enabling them to locate individuals and recover outstanding debts efficiently. Understanding and implementing collection best practices can improve your efforts and overall success rates. As a global leader in data and analytics, we offer extensive expertise and cutting-edge skip-tracing tools tailored to meet your unique needs. Comprehensive data integration: Our skip-tracing tools integrate data from multiple sources, including credit reports, alternative data, public records, and proprietary databases. This comprehensive approach ensures that you have access to accurate and up-to-date information, improving right-party contact. Recent and reliable data: While many data providers rely on static or stale data, our skip-tracing data is frequently updated, so you can avoid inaccurate, outdated information. More than 1.3 billion updates are made per month, including new phone numbers, new addresses, new employment, payment history, and more. Advanced technology: Our skip-tracing solutions leverage advanced technology, including AI and ML, to analyze data quickly and accurately. Our state-of-the-art algorithms identify patterns and connections to help you locate individuals more efficiently. Commitment to data privacy: We prioritize data privacy and adhere to the highest ethical standards. Our skip-tracing solutions are designed to protect personal information while ensuring compliance with industry regulations. You can trust us to handle data responsibly and ethically. Ready to take your skip-tracing efforts to the next level? Learn more Access white paper

Open banking has been leveraged for years in the U.S. The anticipated U.S. regulation under section 1033 of the Dodd-Frank Act, combined with the desire to expand lending universes, has increased interest and urgency among financial institutions to incorporate open banking flows into their workstreams. With technological improvements, increased data availability, and increasing consumer awareness around the benefits of data value exchange, financial service providers can use consumer-permissioned data to gain new insights. For example, access to bank account transactional data, permissioned appropriately, provides important attributes into risk, spend and income behaviors, and financial health, while equipping institutions with intelligence they can harness to help meet various business objectives. Current state of open banking Open Banking use cases are extensive and will continue to expand as access to permissioned data becomes more common. Second chance underwriting, where a lender retrieves additional insights to potentially reverse the primary declination, is the most prevalent use case in the market today. Where a consumer may have limited or no credit history, this application of cashflow attributes and scores in a decisioning flow can help many consumers access financial services where they cannot be fully underwritten on credit data alone. And it is not just consumer behavior and willingness to permission their data that will accelerate open banking in financial services. The technology enabling access, security, standardization, and categorization is equally critical. New and existing players across the ecosystem are rolling out new solutions to drive results for financial institutions. The benefits of open banking are vast as highlighted recently by Craig Focardi, Principal Analyst at Celent: “The final adoption of the CFPB’s proposed rule under Section 1033 will accelerate open banking in the US,” said Focardi. “Although open banking is operating effectively under existing consumer protection/privacy and related laws and regulations, this modern opening banking rule will enhance consumer control over their data for privacy and security, help consumers better manage their finances, and help them find the best products and banking relationships. For financial institutions, it will level the competitive playing field for smaller financial institutions, increase competition for customer relationships, and incentivize all financial institutions to invest in technology, data, and analytics to adopt open banking more quickly.” Despite the wealth of information that open banking can offer, institutions are at varying stages of maturity when it comes to using this data in production, with fintechs and challenger banks leading the way. However, most banks are researching and planning to take advantage of the insights unlocked through open banking – particularly cashflow data. But why is there not wider adoption when this ‘new’ data can offer such rich and actionable insights? The answer varies, but it is top of mind for risk officers, analysts and marketers. Some financial institutions are worried about application drop-off as consumers move through a data consent journey. Others are taking a wait-and-see approach as they are concerned about incorporating open banking flows only to see regulation upend the application of permissioned data. Regardless of readiness, most organizations are in various stages of testing new permissioned data sources to understand the implications. Experian has helped many financial institutions understand the power of consumer-permissioned data through analytics and specific tests leveraging client transactional data and our cash flow models. On aggregate, we see cashflow data perform well on its own in determining a consumer’s likelihood of going 60 days past due over 12 months; however, it is best used in combination with traditional and alternative credit data to achieve optimal performance of underwriting models. But what about consent? Will consumers be open to permissioning their data? From our research, we see that consumers are willing to give permission if the benefits are explained and they understand how their data will be used. In fact, 70% of consumers report they are likely to share banking data for better loan rates, financial tools, or personalized spending insights.1 Experian reveals new solutions for open banking We at Experian are excited about the benefits open banking can provide, including: Giving more control to consumers: Consumers are hungry for more control over their data. We have seen this ourselves with Experian Boost®. When the benefits of data sharing are properly explained, and consumers can control when and how that data is used, it is empowering and allows consumers the potential to unlock new financial opportunities. Improving risk assessment: As mentioned above, analysis shows that cash flow data (transactional open banking data) is very predictive on its own. Adding our credit data delivers even greater predictability, enabling lenders to score more consumers and offer the right products, services, and pricing. Augmenting existing strategies: Open banking is not a new strategy; it augments and improves many existing processes. Institutions do not need to start something from scratch; they can layer incremental data into existing processes for an improved risk assessment, deeper insights, and a better customer experience. Open banking is not a new strategy; it augments and improves many existing processes. Institutions do not need to start something from scratch; rather, they can layer incremental data into existing processes for an improved risk assessment, deeper insights, and a better customer experience. We’re helping institutions unlock the power of open banking data by transforming transaction data into precise categories, a foundational component of cashflow analytics that feeds into the calculation of attributes and scores. These new Cashflow Attributes can be easily plugged into existing underwriting, analytic, and account management use cases. Early indicators show that Cashflow Attributes can boost predictive accuracy by up to 20%, allowing lenders to drive revenue growth while mitigating risk.2 Open banking is emerging in the industry across various use cases. Many are only just realizing the potential insights and benefits this can have to consumers and their organizations. How will you leverage open banking? Learn more about how we're helping address open banking 1Atomik Research survey of 2,005 U.S. adults online, matching national demographics. Fieldwork: March 17-21, 2024. 2Experian analysis based on GINI predictability. GINI coefficient measures income or wealth inequality within a population, with 0 indicating perfect equality and 1 indicating perfect inequality, reflecting predictive capability.

Finding a balance between providing secure financial services and user-friendly experiences is no easy task. One of the biggest hurdles? Ensuring identity authentication is robust and reliable. Let's walk through the essentials of identity authentication, its importance, and what effective solutions look like. What is identity authentication? Identity authentication is the process of proving that an individual is who they claim to be. Unlike identity verification, which simply confirms that the provided identity information is valid, identity authentication goes a step further by ensuring that the person presenting the information is indeed its rightful owner. At its core, identity authentication relies on various methods to verify identities. These methods can range from simple password checks to more sophisticated technologies like biometrics and adaptive authentication. The goal is to create multiple layers of security that make it difficult for unauthorized users to gain access. Types of authentication methods Several types of identity authentication methods are used today. Passwords and PINs are the most basic forms, but they are increasingly being supplemented or replaced by more advanced solutions like multi-factor authentication (MFA) , biometric scans, and knowledge-based authentication (KBA). Each method has its advantages and limitations, making it crucial for financial institutions to choose the right mix. Authentication vs. verification While often used interchangeably, identity verification and identity authentication serve different purposes. Identity verification solutions confirm that the provided identity information matches public records, whereas identity authentication solutions ensure that the person presenting the information is its true owner. Identity verification is typically a one-time process conducted at the beginning of a relationship, such as when opening a new bank account. On the other hand, identity authentication is an ongoing process, ensuring that each login or transaction is carried out by a legitimate user. Though different, these processes are crucial for financial institutions. They work together to provide a robust security framework that minimizes the risk of fraud while offering a seamless user experience. READ: Learn how to overcome online identity verification challenges. Why it's important for financial institutions The importance of identity authentication for financial institutions cannot be overstated. With the rise of cyber threats and sophisticated fraud schemes like synthetic identity fraud, robust identity authentication measures are more critical than ever. Enhancing security. Effective authentication significantly enhances the security of financial transactions. By preventing unauthorized access, sensitive information and financial assets are safeguarded. Advanced solutions like multi-factor authentication solutions add extra layers of protection. Building trust with customers. Robust authentication also helps build trust with customers. When users feel confident that their accounts and personal information are secure, they are more likely to engage with the institution and utilize its services. Regulatory compliance. For financial institutions, compliance with regulatory standards is paramount. Many regulations now mandate strong identity authentication measures to protect against fraud and ensure the security of financial transactions. What to look for in an identity authentication solution The ideal solution should offer a balance between security, user experience, and cost-effectiveness. Adaptive authentication solutions use machine learning algorithms to assess the risk level of each transaction. This allows for a dynamic approach to authentication, where additional checks are only required when necessary. Multi-factor authentication (MFA) solutions add an extra layer of security by requiring users to provide multiple forms of identification. This could include something they know (password), something they have (smartphone), and something they are (biometric data). Knowledge-based authentication (KBA) solutions ask users to answer questions based on their personal information. This method is particularly useful for verifying identities during online transactions and account recoveries. Experian’s Knowledge IQSM offers KBA with over 70 credit- and noncredit-based questions to help you authenticate consumers by asking noninvasive questions that can be answered quickly by the true consumer. Comprehensive identity solutions take a holistic approach by integrating various methods and technologies. Experian’s identity solutions offer a range of services, from risk-based authentication to automated identity verification, ensuring comprehensive protection. Importance of user experience. While security is paramount, user experience should not be overlooked. The ideal identity authentication solution should be seamless and user-friendly, minimizing friction during the authentication process. READ: By adopting a consumer-centric approach to digital identity, organizations can offer customers a better experience while minimizing risk. How Experian can help Identity authentication is a critical component of modern financial institutions. By implementing robust and user-friendly solutions, organizations can enhance security, build customer trust, and comply with regulatory standards. Whether it's through adaptive authentication, multi-factor authentication, or knowledge-based authentication, the goal is to create a secure and seamless experience for users. Ready to take your identity strategy to the next level? Explore Experian’s identity solutions today and discover how they can help your institution achieve its security and user experience goals. Learn more This article includes content created by an AI language model and is intended to provide general information.

With more consumers online, bad actors are taking the opportunity to commit more financial crimes, such as account takeover fraud. This online scheme resulted in nearly $13 billion in losses in 2023, up from $11 billion in 2022.1 So, what do organizations need to know about this form of identity theft? And how can they prevent it? Let’s explore one type of account takeover fraud: email account takeover. What is email account takeover? Email account takeover occurs when a fraudster gains access to a legitimate user’s email account through data breaches that expose credentials, purchasing from the dark web, or phishing scams. It's usually one of the first steps in a broader account takeover scheme. Once fraudsters have access to a consumer’s email or social media account, they have access to the private information in that consumer’s inbox: financial statements, health records, and other forms of PII. Fraudsters can also now use the consumer’s email to impersonate them with friends, family, financial institutions or other businesses they interact with. They can also gain access to other accounts and here’s where email account takeover becomes more dangerous. In this attack, the fraudster gains access to an email or mobile account. Once they have an email, they start by trying to guess the user’s password, commonly called a brute force attack, or through password spraying, where they use commonly used passwords, i.e. ‘password’ or ‘123123. A recent Google survey found that 65% of people use the same password for some or all of their online accounts. This, along with a corresponding email address can give fraudsters further entre into a consumer’s other accounts. If unsuccessful, they’ll then execute a ‘forgot password’, password reset, or one-time password. Then, they take over the victim’s account with their financial institution to facilitate the transfer of funds from the compromised account. 57% of businesses are experiencing rising fraud losses associated with account opening and account takeover.2 While email account takeover can be quickly executed, detecting it can take time. Unlike credit card fraud, where an individual may soon notice suspicious activity, an email account takeover can go undetected for longer. The owner may not realize until later that their account has been compromised, especially with a dormant account or secondary account they use less. As a result, criminals have more time to facilitate additional attacks. LEARN MORE: Explore 2024 fraud trends listed by Experian. How does it affect your organization? Account takeover fraud doesn't just impact consumers, it can result in significant financial losses for organizations. For example, if your organization offers credit products, you might have to cover the costs of disputing chargebacks, card processing fees, or providing refunds. In the case of a data breach, you may have to pay fines against your organization for not properly protecting consumer information. Nearly two-thirds of consumers say they’re very or somewhat concerned with online security.3 But email account takeover isn't just costly — it can damage your organization's reputation. Consumers expect organizations to have proper security measures in place to protect their information. If a data breach occurs, your security can seem weak, leading consumers to lose trust in your organization. As a result, they may potentially take their business elsewhere. The importance of prevention While consumers listed identity theft as their top concern when conducting activities online, they’re still interacting, opening new accounts, and transacting digitally.4 Coupled with the rise of account takeover fraud and associated losses, it’s more crucial than ever for organizations to accurately detect and prevent these attacks. To do this, they must have a proactive fraud prevention strategy in place. Account takeover fraud prevention requires your business to maintain and continuously reaffirm confidence in the identity data you collect. Your team can monitor, segment, and proactively act on customer identities that display a higher risk of fraud than was determined at account origination through risk-based fraud detection models, machine learning, and advanced analytics. Experian offers many flexible solutions, including: CrossCore® Solutions are best practice-based groupings of fraud and identity products that enable organizations to solve common to complex issues. For example, our fraud risk solutions include email and phone intelligence to improve verification for thin-files and other challenging populations. Experian offers phone/carrier-based matching capabilities with address validity and occupancy data for >95% of U.S. households. FraudNet is a device intelligence solution that analyzes hundreds of device attributes and prevents fraud on all digital channels. Combining contextual data, behavioral data, and device data, it bridges the gap between physical and digital identity to achieve fraud capture rates that exceed industry averages. To further alleviate account takeover fraud, your organization can offer educational resources for fraud prevention. Using various, strong passwords across their accounts, and changing them regularly, is a foundational way consumers can help ensure their accounts are secure. Leveraging user names that are different from your email can also help. If a fraudster is able to takeover an account and initiate a lost password request, and that password is used for other accounts, that fraudster now has the credentials they need to further defraud that consumer. By spreading awareness about identity fraud risks and providing best practices for prevention, you can better protect your organization and consumers. LEARN MORE: Building a multilayered fraud and identity strategy with CrossCore Solutions Partnering with Experian Email account takeover, along with other types of fraud, can be detected and prevented with the right partner. Experian’s fraud management solutions can help your organization accurately verify customers and assess risk with our account takeover and fraud management solutions. Explore Experian’s account takeover solutions and watch an on-demand recording of our Fraud Risk and Identity Verification Solutions tech showcase. Learn more Watch tech showcase 1 Identity Fraud Cost Americans $43 Billion in 2023, AARP. 2-4 2023 U.S. Identity and Fraud Report, Experian.

Rising balances and delinquency rates are causing lenders to proactively minimize credit risk through pre-delinquency treatments. However, the success of these types of account management strategies depends on timely and predictive data. Credit attributes summarize credit data into specific characteristics or variables to provide a more granular view of a consumer’s behavior. Credit attributes give context about a consumer’s behavior at a specific point in time, such as their current revolving credit utilization ratio or their total available credit. Trended credit attributes analyze credit history data for consumer behavior patterns over time, including changes in utilization rates or how often a balance exceeded an account’s credit limit during the previous 12 months. In a recent analysis, we found that credit attributes related to utilization were highly predictive of future delinquencies in bankcard accounts, with many lenders better managing their credit risk when incorporating these attributes into their account management processes. READ: Find out how custom attributes and models can help you stay ahead of your competitors in the "Build a profitable portfolio with credit attributes" e-book. Using attributes to manage credit risk An enhanced understanding of credit attributes can be leveraged to manage risk throughout the customer lifecycle. They can be important when you want to: Improve credit strategies and efficiencies: Overlay attributes and incorporate them into credit policy rules, such as knockout criteria, to expand your lending population and increase automation without taking on more credit risk. Better understand customers' credit trends: Experian’s wide range of credit data, including trended credit attributes, can help you quickly understand how consumers are faring off-book for visibility into other lending relationships and if they’ll likely experience financial stress in the future. Credit attributes can also help precisely segment populations. For example, attributes can help you distinguish between two people who have similar credit risk scores — but very different trajectories — and will better determine who's the least risky customer. Predicting 60+ day delinquencies with credit attributes To evaluate the effectiveness of credit attributes during account review, we looked at 2.9 million open and active bankcard accounts to see which attributes best predicted the likelihood of an account reaching 60 days past due. For this analysis, we used snapshots of bankcard accounts that were reported in October 2022 and April 2023. Additionally, we analyzed the predictive power of over 4,000 attributes from Experian Premier AttributesSM and Trended 3DTM. Key findings Nine of the top 20 most predictive credit attributes were related to credit utilization rates. Delinquency-related attributes were predictive but weren’t part of the top 10. Three of the top 10 attributes were related to available credit. Turning insight into action While we analyzed credit attributes for account review, determining attribute effectiveness for other use cases will depend on your own portfolio and goals. However, you can use a similar approach to finding the predictive power of attributes. Once you identify the most predictive credit attributes for your population, you can also create an account review program to track these metrics, such as changes in utilization rates or available credit balances. Using Experian’s Risk and Retention Triggers℠ can immediately notify you of customers' daily credit activity to monitor those changes. Ongoing monitoring of attributes and triggers can help you identify customers who are facing financial stress and are headed toward delinquency. You can then proactively take steps to reduce your risk exposure, prioritize accounts, and modify pre-collections strategy based on triggering events. Experian offers credit attributes and the tools to use them Creating and managing credit attributes can be a complex and never-ending task. You need to regularly monitor attributes for performance drift and to address changing regulatory requirements. You may also want to develop new attributes based on expanding data sources and industry trends. Many organizations don’t have the resources to create, manage, and update credit attributes on their own. That’s where Experian’s 4,500+ attributes and tools can help to save time and money. Premier Attributes includes our core attributes and subsets for over 50 industries. Trended 3D attributes can help you better understand changes in consumer behavior and creditworthiness. Clear View AttributesTM offers insights from expanded FCRA data* that generally isn’t reported to consumer credit bureaus. You can easily review and manage your portfolios with Experian’s Ascend Quest™ platform. The always-on access allows you to request thousands of data elements, including credit attributes, risk scores, income models, segmentation data, and payment history, at any time. Use insights from the data and leverage Ascend Quest to quickly identify accounts that may be experiencing financial stress to limit your credit risk — and target others with retention and up-selling opportunities. Watch the Ascend Quest demo to see it in action, or contact us to learn more about Experian’s credit attributes and account review solutions. Watch demo Contact us

This series will dive into our monthly State of the Economy report, providing a snapshot of the top monthly economic and credit data for those in financial services to proactively shape their business strategies. During their June meeting, the Federal Reserve continued to hold rates steady and released an updated Summary of Economic Projections. In this update, the committee reduced 2024 rate cut projections from three to one and increased their year-end inflation expectations. Both of these updates were likely driven by a lack of downward progress in inflation in Q1. But as the Federal Reserve extends the period of restrictive rates, it places more weight on each monthly economic data release to inform the Fed’s next move. Data highlights from this month’s report include: Job creation exceeded economists’ expectations with 272,000 jobs added in May. Inflation cooled in May, with annual headline inflation down from 3.4% to 3.3% and annual core inflation down from 3.6% to 3.4%. Auto loan amounts decreased in Q1 as inventories continue to stabilize. Check out our report for a deep dive into the rest of this month’s data, including the latest trends in delinquencies, spending, and the new housing market. Download June's report To have a holistic view of our current environment, it’s important to view the economy from different angles and through different lenses. Watch our experts discuss the latest economic and credit trends in the recording of our latest macroeconomic forecasting webinar and listen to our latest Econ to Action podcast. For more economic trends and market insights, visit Experian Edge.

Dealing with delinquent debt is a challenging yet crucial task, and when faced with economic uncertainties, the need for effective debt management and collections strategies becomes even more pressing. Thankfully, advanced analytics offers a promising solution. By leveraging data-driven insights, you can enhance operational efficiency, better prioritize accounts, and make more informed decisions. This article explores how advanced analytics can revolutionize debt collection and provides actionable strategies to implement treatment. Understanding advanced analytics in debt collection Advanced analytics involves using sophisticated techniques and tools to analyze complex datasets and extract valuable insights. In debt collection, advanced analytics can encompass various methodologies, including predictive modeling, machine learning (ML), data mining, and statistical analysis. Predictive modeling Predictive modeling leverages historical data to forecast future outcomes. By applying predictive models to debt collection, you can estimate each account's repayment likelihood. This helps prioritize your efforts toward accounts with a higher chance of recovery. Machine learning Machine learning algorithms can automatically identify patterns in large datasets, enabling more accurate predictions and classifications. For debt collectors, this means better segmenting delinquent accounts based on likelihood of repayment, risk, and customer behavior. Data mining Data mining involves exploring large datasets to unearth hidden patterns and correlations. In debt collection, data mining can reveal previously unnoticed trends and behaviors, allowing you to tailor your strategies accordingly. Statistical analysis Statistical methods help quantify relationships within data, providing a clearer picture of the factors influencing debt repayment and focusing on statistically significant repayment drivers, which aids in refining collection strategies. Benefits of advanced analytics in delinquent debt collection The benefits of employing advanced analytics in delinquent debt collection are multifaceted and valuable. By integrating these technologies, financial institutions can achieve greater efficiency, reduce operational costs, and improve recovery rates. Enhanced prioritization and decisioning With data and predictive analytics, you can gain a complete view of existing and potential customers to determine risk exposure and prioritize accounts effectively. By analyzing payment histories, credit scores, and other consumer behavior, you can enhance your collectoins prioritization strategies and focus on accounts more likely to pay or settle. This ensures that resources are allocated efficiently, and decisions are informed, maximizing your return on investment. Watch: In our recent tech showcase, learn how to harness the power of our industry-leading collection decisioning and optimization capabilities. Reduced costs Advanced analytics can significantly reduce operational costs by streamlining the collection process and targeting accounts with higher recovery potential. Automated processes and optimized resource allocation mean you can achieve more with less, ultimately increasing profitability. Better customer relationships With debt collection analytics, digital communication tools, artificial intelligence (AI), and ML processes, you can enhance your collections efforts to better engage with consumers and increase response rates. Adopting a more empathetic and customer-centric approach that embraces omnichannel collections can foster positive customer relationships. Implementing advanced analytics: A step-by-step guide Step 1: Data collection and integration The first step in implementing advanced analytics is to gather and integrate data from various sources. This includes payment histories, account information, demographic data, and external data such as credit scores. Ensuring data quality and consistency is crucial for accurate analysis. Step 2: Data analysis and modeling Once the data is collected, the next step is to apply advanced analytical techniques. This involves developing predictive models, training machine learning algorithms, and conducting statistical analyses to identify notable patterns and trends. Step 3: Strategy development Based on the insights gained from the analysis, you can develop targeted collection strategies. These may include segmenting accounts, prioritizing high-potential recoveries, and choosing the most effective communication methods. It’s essential to test and refine these strategies to ensure optimal performance continually. Step 4: Automation and implementation Implementing advanced analytics often involves automation. Workflow automation tools can streamline routine tasks, ensuring strategies are executed consistently and efficiently. Integrating these tools with existing debt collection systems can enhance overall effectiveness. Step 5: Monitoring and optimization Finally, continuously monitor the performance of your advanced analytics initiatives. Use key performance indicators (KPIs) to track success and identify areas for improvement. Regularly update models and strategies based on new data and evolving trends to maintain high recovery rates. Putting it all together Advanced analytics hold immense potential for transforming delinquent debt collection and can drive better return on investment. By leveraging predictive modeling, machine learning, data mining, and statistical analysis, financial institutions and debt collection agencies can perfect their collection best practices, prioritize accounts effectively, and make more informed decisions. Our debt collection analytics and recovery tools empower your organization to see the complete behavioral, demographic, and emerging view of customer portfolios through extensive data assets, advanced analytics, and platforms. As the financial landscape evolves, working with an expert to adopt advanced analytics will be critical for staying competitive and achieving sustainable success in debt collection. Learn more *This article includes content created by an AI language model and is intended to provide general information.