All posts by Guest Contributor

When checking access accounts were first introduced, it wasn’t uncommon for banks to provide new customers “basic” transaction services in starter checking accounts. These services typically included an automatic teller machine (ATM) access card and the ability to withdraw cash at their local branch. As consumers developed a relationship and established financial trust with their bank, they eventually would get a checkbook, which allowed check-writing access. This took time and a consumer demonstrating both the willingness and ability to manage finances to the bank’s expectations. Establishing the financial relationship was a trust-building process. With the onset of general-purpose debit cards and a host of other digital money-movement capabilities, such as online banking, the majority of banks now offer just basic and preferred checking. A minimum acceptance standard leaves many consumers out of the financial transaction system, which is something that concerns regulatory bodies such as the Consumer Financial Protection Bureau (CFPB). Approval criteria vary across financial institutions, but a typical basic checking account has some form of overdraft feature enabled, and some consumers may not be able to afford these fees even if they elect to opt in for overdraft functionality. Nonetheless, banks still screen applicants to ensure prior accounts at other institutions were managed with no losses incurred by other banks. In today’s modern world, it is difficult to participate fully in our credit-driven society without a checking account at a recognized bank or credit union. The answer in many cases would be checking accounts for consumers that have either overdraft functionality assigned based on the consumer’s wish to opt in or overdraft access that matches that same consumer’s ability to pay. In early February, the CFPB passed new guidelines to increase access to basic check products. While a step towards making checking accounts available to all, the most recent actions still leave unresolved regulatory actions regarding what the CFPB refers to as “affordable” checking access. For instance, for those consumers without disposable income, the issue of fees for overdraft and nonsufficient funds is still an unresolved regulatory matter. In the most recent announcement, the CFPB took several actions related to its focus on increasing consumer access to checking transaction accounts with banks: Sending a letter to CEOs of the top 25 banks encouraging them to take steps to help consumers with affordable checking account access such as “no fee” and/or “no overdraft” checking accounts Providing several new resources to consumers such as a guide to “Low Risk Checking, Managing Checking and Consumer Guide to Checking Account Denial” Introducing the Consumer Protection Principles, which include a drive toward: Faster funds availability Improved consumer transparency into checking account fee structure, funds availability and security Tailoring products to reach a larger percentage of consumers Developing no-overdraft type checking products, which only a handful of large banking institutions had What lurks ahead for banks is the need to develop products that are designed to reach a larger population that includes under banked and unbanked consumers with troubled financial repayment history. Coupling this product development effort with the CFPB desire for no-overdraft-fee type products makes me wonder if we should look to account features from several decades ago, such as creating a 21st century version of the checking account with digital money-movement features that protects consumers’ privacy, but doesn’t put them in a position to rack up large amounts of overdraft fees they can’t afford to pay in the event they overdraw the checking account. Experian® suggests taking the following steps: Conduct a Business Review to ensure that your product offering includes the type of account the CFPB is advocating and your existing core banking platform can operationalize this account Align your checking account prospect and opening procedures to key segments to ensure more consumers are approved and right-sized to the appropriate checking product Enhance your business profitability by cross-selling credit products that fit the affordability and disposable income of various consumer segments you originate These steps will make your journey “back to the future” much less turbulent and ensure you don’t break the bank in your efforts to address CFPB’s well-intentioned focus on check access for consumers.

Millions of people around the world are wearing green to celebrate St. Patrick's Day today. Some interesting facts on the color: Green is associated with St. Patrick's Day because it is the color of spring, Ireland and the shamrock Green ink originally was used in U.S. currency to prevent counterfeiting and because of its resistance to chemical and physical changes The Chicago River is colored green for the St. Patrick's Day parade each year using 45 pounds of vegetable dye >> Gain insights and earn more green with the Market Intelligence Brief

Identity management traditionally has been made up of creating rigid verification processes that are applied to any access scenario. But the market is evolving and requiring an enhanced Identity Relationship Management strategy and framework. Simply knowing who a person is at one point in time is not enough. The need exists to identify risks associated with the entire identity profile, including devices, and the context in which consumers interact with businesses, as well as to manage those risks throughout the consumer journey. The reasoning for this evolution in identity management is threefold: size and scope, flexible credentialing and adaptable verification. First, deploying a heavy identity and credentialing process across all access scenarios is unnecessarily costly for an organization. While stringent verification is necessary to protect highly sensitive information, it may not be cost-effective to protect less-valuable data with the same means. A user shouldn’t have to go through an extensive and, in some cases, invasive form of identity verification just to access basic information. Second, high-friction verification processes can impede users from accessing services. Consumers do not want to consistently answer multiple, intrusive questions in order to access basic information. Similarly, asking for personal information that already may have been compromised elsewhere limits the effectiveness of the process and the perceived strength in the protection. Finally, an inflexible verification process for all users will detract from a successful customer relationship. It is imperative to evolve your security interactions as confidence and routines are built. Otherwise, you risk severing trust and making your organization appear detached from consumer needs and preferences. This can be used across all types of organizations — from government agencies and online retailers to financial institutions. Identity Relationship Management has three unique functions delivered across the Customer Life Cycle: Identity proofing Authentication Identity management Join me at Vision 2016 for a deeper analysis of Identity Relationship Management and how clients can benefit from these new capabilities to manage risk throughout the Customer Life Cycle. I look forward to seeing you there!

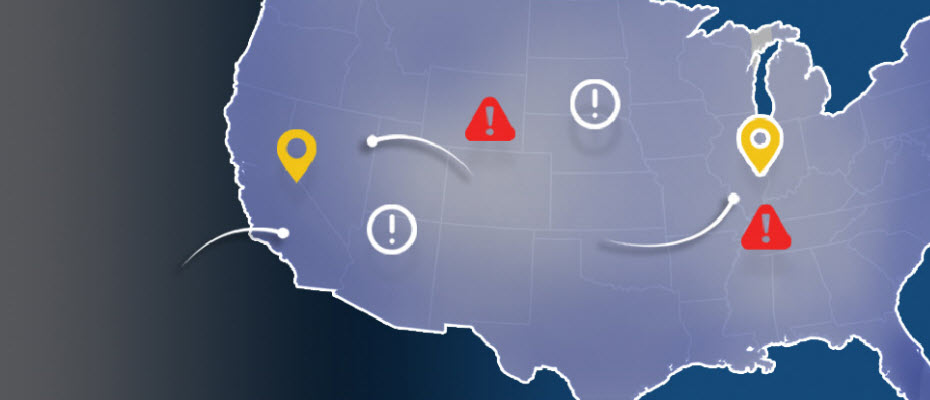

Top states for billing and shipping e-commerce fraud With more than 13 million fraud victims in 2015, assessing where fraud occurs is an important layer of verification for e-commerce. Experian® analyzed millions of e-commerce transactions from 2015 to identify fraud attack rates across the United States. With the switch to chip-enabled credit card transactions and possible growth of card-not-present fraud, online businesses should utilize advanced fraud solutions to monitor their riskiest locations and prevent losses. >> View the Experian map to see 2015 e-commerce attack rates for all states

Bankcard origination volumes reached $97.5 billion in Q4 2015, the highest level on record since Q3 2008 and an increase of 22% over the same quarter in 2014. The 60–89-days-past-due bankcard delinquency rate came in at .53% for Q4 2015 — significantly lower than the 1.22% delinquency rate back in Q3 2008. The increase in bankcard originations combined with lower delinquencies points to a positive credit environment. Lenders should stay abreast of the latest bankcard trends in order to adjust lending strategies and capitalize on areas of opportunity. >> Key steps to designing a profitable bankcard campaign

2015 data shows where billing and shipping e-commerce fraud attacks occur in the United States Experian e-commerce fraud attacks and rankings now available Does knowing where fraud takes place matter? With more than 13 million fraud victims in 2015,[1] assessing where fraud occurs is an important layer of verification when performing real-time risk assessments for e-commerce. Experian® analyzed millions of e-commerce transactions from 2015 data to identify fraud-attack rates across the United States for both shipping and billing locations. View the Experian map to see 2015 e-commerce attack rates for all states and download the top 100 ZIP CodeTMrankings. “Fraud follows the path of least resistance. With more shipping and billing options available to create a better customer experience, criminals attempt to exploit any added convenience,” said Adam Fingersh, Experian general manager and senior vice president of Fraud & Identity Solutions. “E-commerce fraud is not confined to larger cities since fraudsters can ship items anywhere. With the switch to chip enabled credit card transactions, and possible growth of card-not-present fraud, our fraud solutions help online businesses monitor their riskiest locations to prevent losses both in dollars and reputation in the near term.” For ease of interpretation, billing states are associated with fraud victims (the address of the purchaser) and shipping states are associated with fraudsters (the address where purchased goods are sent). According to the 2015 e-commerce attack rate data: Florida is the overall riskiest state for billing fraud, followed by Delaware; Washington, D.C.; Oregon and California. Delaware is the overall riskiest state for shipping fraud, followed by Oregon, Florida, California and Nevada. Eudora, Kan., has the overall riskiest billing ZIP Code (66025). The next two riskiest ZIPTM codes are located in Miami, Fla. (33178) and Boston, Mass. (02210). South El Monte, Calif., has the overall riskiest shipping ZIP Code (91733). The next four riskiest shipping ZIP codes are all located in Miami. Overall, five of the top 10 riskiest shipping ZIP codes are located in Miami. Defiance, Ohio, has the least risky shipping ZIP Code (43512). The majority of U.S. states are at or below the average attack rate threshold for both shipping and billing fraud, with only seven states — Florida, Oregon, Delaware, California, New York, Georgia and Nevada — and Puerto Rico ranking higher than average. This indicates that attackers are targeting consumers equally in the higher-risk states while leveraging addresses from both higher- and lower-risk states to ship and receive fraudulent merchandise. Many of the higher-risk states are located near a large port-of-entry city, including Miami; Portland, Ore.; and Washington, D.C., perhaps allowing criminals to move stolen goods more effectively. All three cities are ranked among the riskiest cities for both measures of fraud attacks. Neighboring proximity to higher-risk states does not appear to correlate to any additional risk — Pennsylvania and Rhode Island are ranked as two of the lower-risk states for both shipping and billing fraud. Other lower-risk states include Wyoming, South Dakota and West Virginia. Experian analyzed millions of e-commerce transactions to calculate the e-commerce attack rates using “bad transactions” in relation to the total number of transactions for the 2015 calendar year. View the Experian map to see 2015 e-commerce attack rates for all states and download the top 100 ZIP Code rankings. [1]According to the February 2016 Javelin study 2016 Identity Fraud: Fraud Hits an Inflection Point.

Time to dust off those compliance plans and ensure you are prepared for the new regulations, specifically surrounding the Military Lending Act (MLA). Last July, the Department of Defense (DOD) published a Final Rule to amend its regulation implementing the Military Lending Act, significantly expanding the scope of the existing protections. The new, beefed-up version encompasses new types of creditors and credit products, including credit cards. While the DOD was responsible for implementing the rule, enforcement will be led by the Consumer Financial Protection Bureau (CFPB). The new rule became effective on October 1, 2015, and compliance is required by October 3, 2016. Compliance, however, with the rules for credit cards is delayed until October 3, 2017. While there is no formal guidance yet on what federal regulators will look for in reviewing MLA compliance, there are some insights on the law and what’s coming. Why was MLA enacted? It was created to provide service members and their dependents with specific protections. As initially implemented in 2007, the law: Limited the APR (including fees) for covered products to 36 percent; Required military-specific disclosures, and; Prohibited creditors from requiring a service member to submit to arbitration in the event of a dispute. It initially applied to three narrowly-defined “consumer credit” products: Closed-end payday loans; Closed-end auto title loans; and Closed-end tax refund anticipation loans. What are the latest regulations being applied to the original MLA implemented in 2007? The new rule expands the definition of “consumer credit” covered by the regulation to more closely align with the definition of credit in the Truth in Lending Act and Regulation Z. This means MLA now covers a wide range of credit transactions, but it does not apply to residential mortgages and credit secured by personal property, such as vehicle purchase loans. One of the most significant changes is the addition of fees paid “for a credit-related ancillary product sold in connection with the credit transaction.” Although the MAPR limit is 36 percent, ancillary product fees can add up and — especially for accounts that carry a low balance — can quickly exceed the MAPR limit. The final rule also includes a “safe harbor” from liability for lenders who verify the MLA status of a consumer. Under the new DOD rule, lenders will have to check each credit applicant to confirm that they are not a service member, spouse, or the dependent of a service member, through a nationwide CRA or the DOD’s own database, known as the DMDC. The rule also permits the consumer report to be obtained from a reseller that obtains such a report from a nationwide consumer reporting agency. MLA status for dependents under the age of 18 must be verified directly with the DMDC. Experian will be permitted to gain access to the DMDC data to provide lenders a seamless transaction. In essence, lenders will be able to pull an Experian profile, and MLA status will be flagged. What is happening between now and October 2016, when lenders must be compliant? Experian, along with the other national credit bureaus, have been meeting with the DOD and the DMDC to discuss providing the three national bureaus access to its MLA database. Key parties, such as the Financial Services Roundtable and the American Bankers Association, are also working to ease implementation of the safe harbor check for banks and lenders. The end goal is to enable lenders the ability to instantly verify whether an applicant is covered by MLA by the Oct. 1, 2016 compliance date. --- If you have inquiries about the new Military Lending Act regulations, feel free to email MLA.Support@experian.com or contact your Experian Account Executive directly. Next Article: A check-in on the latest Military Lending Act news

A recent survey commissioned by VantageScore® Solutions, LLC found that among consumers who are unable to obtain credit, 27% attribute the situation to lack of a credit score. Most consumers support newer methods of calculating credit scores 49% feel that consistent rental, utility and telecommunications payments should count in determining credit scores 50% agree that competition in the credit scoring marketplace is beneficial Lenders can help solve the credit gap by using advanced risk models that can accurately score more consumers. The result is a win-win: More consumers get access to mainstream credit, and lenders gain more customers. >> Infographic: America’s Giant Credit Gap VantageScore® is a registered trademark of VantageScore Solutions, LLC.

Loyalty fraud and the customer experience Criminals continue to amaze me. Not surprise me, but amaze me with their ingenuity. I previously wrote about fraudsters’ primary targets being those where they easily can convert credentials to cash. Since then, a large U.S. retailer’s rewards program was attacked – bilking money from the business and causing consumers confusion and extra work. This attack was a new spin on loyalty fraud. It is yet another example of the impact of not “thinking like a fraudster” when developing a program and process, which a fraudster can exploit. As it embarks on new projects, every organization should consider how it can be exploited by criminals. Too often, the focus is on the customer experience (CX) alone, and many organizations will tolerate fraud losses to improve the CX. In fact, some organization build fraud losses into their budgets and price products accordingly — effectively passing the cost of fraud onto the consumers. Let’s look into how this type of loyalty fraud works. The criminal obtains your login credentials (either through breach, malware, phishing, brute force, etc.) and uses the existing customer profile to purchase goods using the payment method on file for the account. In this type of attack, the motivation isn’t to receive physical goods; instead, it’s to accumulate rewards points — which can then be used or sold. The points (or any other form of digital currency) are instant — on demand, if you will — and much easier to fence. Once the points are credited to the account, the criminal cashes them out either by selling them online to unsuspecting buyers or by walking into a store, purchasing goods and walking right out after paying with the digital currency. A quick check of some underground forums validates the theory that fraudsters are selling retailer points online for a reduced rate — up to 70 percent off. Please don’t be tempted to buy these! The money you spend will no doubt end up doing harm, one way or another. Now, back to the customer experience. Does having lax controls really represent a good customer experience? Is building fraud losses into the cost of your products fair to your customers? The people whose accounts have been hacked most likely are some of your best customers. They now have to deal with returning merchandise they didn’t purchase, making calls to rectify the situation, having their personally identifiable information further compromised and having to pay for the loss. All in all, not a great customer experience. All businesses have a fiduciary responsibility to protect customer data with which they have been entrusted — even if the consumer is a victim of malware, phishing or password reuse. What are you doing to protect your customers? Simple authentication technologies, while nice for the CX, easily can fail if the criminal has access to the login credentials. And fraud is not a single event. There are patterns and surveillance activities that can help to detect fraud at every phase of your loyalty program — from new account opening to account logins and updates to transactions that involve the purchase of goods or the movement of currency. As fraudsters continue to evolve and look for the least-protected targets, loyalty programs have come to the forefront of the battleground. Take the time to understand your vulnerability and how you can be attacked. Then take the necessary steps to protect your most profitable customers — your loyalty program members. If you want to learn more, join us MRC Vegas 16 for our session “Loyalty Fraud; It’s Brand Protection, Not Just Loss Prevention” and hear our industry experts discuss loyalty fraud, why it’s lucrative, and what organizations can do to protect their brand from this grey-area type of fraud.

According to Experian’s latest State of the Automotive Finance Market report, auto loan balances reached an all-time high of $987 billion in Q4 2015 — an increase of 11.5% over Q4 2014.

A recent Experian survey shows a growing concern over identity theft and tax fraud. 42% of consumers are concerned that someone could access their personal data through their tax return, compared with 35% in 2014 and 38% in 2015 28% of consumers have been a victim or know someone who has been a victim of tax fraud Tax season is a busy time of year for identity thieves. While consumers should take steps to protect themselves, businesses also need to employ ID theft protection solutions in order to safeguard consumer information. >> Identify and prevent multiple types of fraud

According to the latest Experian–Oliver Wyman Market Intelligence Report, HELOC originations came in at $43 billion for Q4 2015 — a 22% increase over Q4 2014. HELOC originations for all of 2015 totaled $160 billion — a 21% increase year over year. As HELOC originations continue their growth trend, lenders can stay ahead of the competition by using advanced analytics to target the right customers and increase profitability. >> Revamp your mortgage and HELOC acquisitions strategies

Understanding the behaviors of best-in-class credit risk managers For financial institutions to achieve superior performance, having the appropriate set of credit risk managers is a prerequisite. The ability to gain insight from data and customer behavior and to use that insight for strategic advantage is a critical ingredient for success. At the same time, the risk-management community is under increasing pressure to understand and explain underlying trends in credit portfolios — and to monitor, interpret and explain these trends with ever-greater accuracy. A common problem financial institutions face when confronting staff resource needs is the difficulty in recruiting and retaining experienced risk-management professionals. The risk-management community is notoriously small, and hiring expertise from within this community is extremely difficult. Skilled risk managers truly are a finite resource, but their skill set is in huge demand. Hiring the right talent is crucial to job satisfaction, leading to higher engagement levels and reduced attrition costs. On top of that, employee engagement is vital to an organization’s success. It drives employee productivity and fosters a culture of innovation, which leads to higher profitability for the entire organization. Building, attracting and retaining risk-management resources requires a commitment to engaging in staff personal development. A great way to support employee engagement is to invest in their personal and professional development, including opportunities for training and team building. If an organization can show that it is committed to developing its people and providing opportunities for career growth, employee engagement levels will rise, with all the benefits this entails. Typically, financial institutions bridge the resource skill gap by either hiring skilled statistical and analytical experts or developing in-house resources. Both of these approaches, however, require significant on-the-job training to teach employees how to link raw statistical techniques and procedures to influencing the profit and loss statement of the business line which they support. The challenge is often broadening the understanding of these skill set “silos” and their contribution to the overall portfolio. By opening that view, the organization generates additional value from these resources as lines of communication are improved and insights and opportunities found within the data are shared more effectively across the organizational team. Experian’s Global Consulting Practice provides a solution to this problem. Our two-day Risk and Portfolio Management Essentials training workshop offers the opportunity to understand the behaviors of best-in-class risk managers. What are the tools and enablers required for the role? How do they prepare for the process of managing credit risk? What areas must risk managers consider managers across the Customer Life Cycle? What differentiates the good from the great? To complement the training modules, Experian® offers an interactive, team-based approach that engages course participants in the build options of a defined portfolio. Participants leverage the best-in-class techniques presented in the sessions in a series of competitive, team-based exercises. This set of cross-organizational exercises drives home the best-in-class techniques and further builds understanding that resonates across the organization long after the course is concluded. For our current offerings, locations and to register click here.

What is blockchain? Blockchain is beginning to get a lot of attention, so I thought it might be time to figure out what it is and what it means. Basically, a blockchain is a permissionless, distributed database that maintains a growing list of records (transactions) in a linear, chronological (and time-stamped) ledger. At a high level, this is how it works. Each computer connected to the network gets a copy of the entire blockchain and performs the task of validating and relaying transactions for the whole chain. The batches of valid transactions added to the record are called “blocks.” A block is the “current” part of a blockchain that records some or all of the recent transactions and once completed goes into the blockchain as a permanent database. Each time a block gets completed, a new block is created, with every block containing a hash of the previous block. There are countless numbers of blocks in the blockchain. To use a conventional banking analogy, the blocks would be a full history of every banking transaction for every person, and the blockchain would be a complete banking history. The entire blockchain is sent to everyone who has access, and every user validates the information in the block. It’s like if Tom, Bob and Harry were standing on the street corner and saw a cyclist hit by a car. Individually, all three men will be asked if the cyclist was struck by the car, and all three will respond “yes.” The cyclist being hit by the car becomes part of the blockchain, and that fact cannot be altered. Blockchain generally is used in the context of bitcoin, where similar uses of the structure are called altchains. Why should I care or, at the very least, pay attention to this movement? Because the idea of it is inching toward the tipping point of mainstream. I recently read an article that identified some blockchain trends that could shape the industry in coming months. The ones I found most interesting were: Blockchain apps will be released Interest in use cases outside payments will pick up Consortia will prove to be important Venture capital money will flow to blockchain start-ups While it’s true that much of the hype around blockchain is coming from people with a vested interest, it is beginning to generate more generalized market buzz as its proponents emphasize how it can reduce risk, improve efficiency and ultimately provide better customer service. Let’s face it, the ability to maintain secure, fast and accurate calculations could revolutionize the banking and investment industries, as well as ecommerce. In fact, 11 major banks recently completed a private blockchain test, exchanging multiple tokens among offices in North America, Europe and Asia over five days. (You can read The Wall Street Journal article here.) As more transactions and data are stored in blockchain or altchain, greater possibilities open up. It’s these possibilities that have several tech companies, like IBM, as well as financial institutions creating what has become known as an open ledger initiative to use the blockchain model in the development of new technologies that will enable a wider array of services. There is no doubt that the concept is intriguing — so much so that even the SEC has approved a plan to issue stock via blockchain. (You can read the Wired article here.) The potential is enough to make many folks giddy. The idea that risk could become a thing of the past because of the blockchain’s immutable historical record — wow. It’s good to be aware and keep an eye on the open ledger initiative, but let’s not forget history, which has taught us that (in the wise words of Craig Newmark), “Crooks are early adopters.” Since blockchain’s original and primary usage has been with bitcoin, I don’t think it is unfair to say that there will be some perceptions to overcome — like the association of bitcoin to activities on the Dark Web such as money laundering, drug-related transactions and funding illegal activities. Until we start to see the application across mainstream use cases, we won’t know how secure blockchain is or how open business and consumers will be to embracing it. In the meantime, remind me again, how long has it taken to get to a point of practical application and more widespread use of biometrics? To learn more, click here to read the original article.

According to a recent Experian Marketing Services study, 36% of companies interact with customers in five or more channels.