All posts by Guest Contributor

With Black Friday quickly approaching, a recent Experian study shows online Black Friday searches are already tracking ahead of last year. This October, the weekly search share for Black Friday averaged 12% higher than October 2014 and is expected to increase dramatically between now and Thanksgiving week. Top product searches for the week ending October 31, 2015 include: Marketers can design more successful campaigns and maximize rewards for both consumers and brands by staying on top of the latest search trends. >> Holiday Hot Sheet

The online marketplace lending sector’s growth is prompting regulators, raising questions about the safety of financial systems and risks associated.

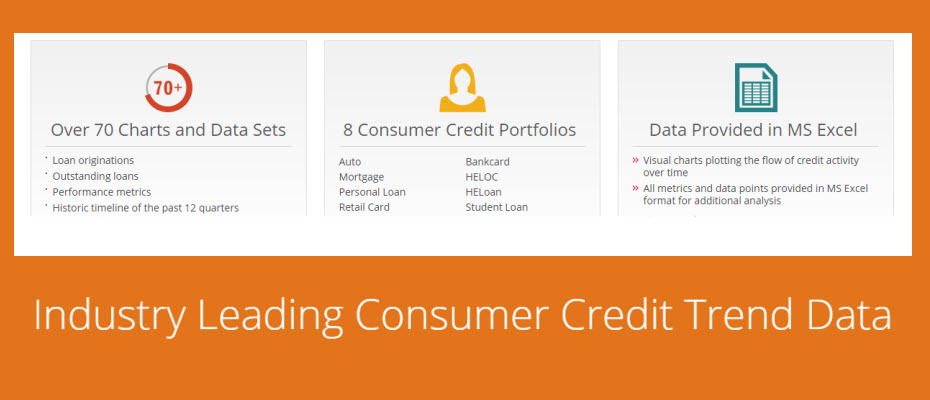

According to a recent survey commissioned by VantageScore® Solutions, millennials cite being unscoreable as the main obstacle to credit access. Among the findings: One-third of millennials cannot obtain the credit they need Of those unable to obtain credit, 34% attribute it to lack of a credit score 49% of millennials agree that competition in the credit-scoring marketplace is beneficial Lenders can help this segment and open the gateway of credit by using advanced risk models that can accurately score consumers considered unscoreable by conventional risk models. >> Infographic: The Giant Credit Gap VantageScore® is a registered trademark of VantageScore Solutions, LLC.

The Responsible Business Lending Coalition, a group of nonbank small-business lenders, recently announced a regulatory program designed to bring greater clarity to the industry’s pricing and consumer protections, including: The right to transparent pricing and terms The right to non-abusive products The right to responsible underwriting The right to fair treatment from brokers The right to inclusive credit access The right to fair collection practices Industry self-regulation is a good way for market leaders to demonstrate self-discipline and is preferable to legislative or regulatory changes because of its flexibility and ability to accommodate evolving market trends. >> Webinar: Online Marketplace Lending

The themes of the game of Risk are relevant to the world of real-life fraud risk prevention. The difference is that the stakes are real and much higher.

Winning the loyalty of millennials continues to be a key area of opportunity for financial institutions.

While marketers typically begin deploying Halloween emails in September, last-minute mailings receive the highest response.

According to the latest State of the Automotive Finance Market report, a record 55.5% of all used vehicles were financed in Q2 2015, compared to 53.8% the previous year.

Auto lending success: Issues within auto lending are unique to other financial services ecosystems. The challenge for many lenders is to…

Key drivers to auto financial services are speed and precision. What model year is your decisioning system? In the auto world the twin engineering goals are performance and durability. Some memorable quotes have been offered about the results of all that complex engineering. And some not so complex observations. The world of racing has offered some best examples of the latter. Here’s a memorable one: “There’s no secret. You just press the accelerator to the floor and steer left. – Bill Vukovich When considering an effective auto financial services relationship one quickly comes to the conclusion that the 2 key drivers of an improved booking rate is the speed of the decision to the consumer/dealer and the precision of that decision – both the ‘yes/no’ and the ‘at what rate’. In the ‘good old days’ a lender relied upon his dealer relationship and a crew of experienced underwriters to quickly respond to a sales opportunities. Well, these days dealers will jump to the service provider that delivers the most happy customers. But, for all too many lenders some automated decisioning is leveraged but it is not uncommon to still see a significantly large ‘grey area’ of decisions that falls to the experienced underwriter. And that service model is a failure of speed and precision. You may make the decision to approve but your competition came in with a better price at the same time. His application got booked. Your decision and the cost incurred was left in the dust – bin. High on the list of solutions to this business issue is an improved use of available data and decisioning solutions. Too many lenders still underutilize available analytics and automated decisions to deliver an improved booking rate. Is your system last year’s model? Does your current underwriting system fully leverage available third party data to reduce delays due to fraud flags. Is your ability to pay component reliant upon a complex application or follow-up requests for additional information to the consumer? Does your management information reporting provide details to the incidence and disposition of all exception processes? Are you able to implement newer analytics and/or policy modifications in hours or days versus sitting in the IT queue for weeks or months? Can you modify policies to align with new dealer demographics and risk factors? The new model is in and Experian® is ready to help you give it a ride. Purchase auto credit data now.

Key drivers to auto financial services are speed and precision. What model year is your decisioning system? In the auto world the twin engineering goals are performance and durability. Some memorable quotes have been offered about the results of all that complex engineering. And some not so complex observations. The world of racing has offered some best examples of the latter. Here’s a memorable one: “There’s no secret. You just press the accelerator to the floor and steer left. – Bill Vukovich When considering an effective auto financial services relationship one quickly comes to the conclusion that the 2 key drivers of an improved booking rate is the speed of the decision to the consumer/dealer and the precision of that decision – both the ‘yes/no’ and the ‘at what rate’. In the ‘good old days’ a lender relied upon his dealer relationship and a crew of experienced underwriters to quickly respond to a sales opportunities. Well, these days dealers will jump to the service provider that delivers the most happy customers. But, for all too many lenders some automated decisioning is leveraged but it is not uncommon to still see a significantly large ‘grey area’ of decisions that falls to the experienced underwriter. And that service model is a failure of speed and precision. You may make the decision to approve but your competition came in with a better price at the same time. His application got booked. Your decision and the cost incurred was left in the dust – bin. High on the list of solutions to this business issue is an improved use of available data and decisioning solutions. Too many lenders still underutilize available analytics and automated decisions to deliver an improved booking rate. Is your system last year’s model? Does your current underwriting system fully leverage available third party data to reduce delays due to fraud flags. Is your ability to pay component reliant upon a complex application or follow-up requests for additional information to the consumer? Does your management information reporting provide details to the incidence and disposition of all exception processes? Are you able to implement newer analytics and/or policy modifications in hours or days versus sitting in the IT queue for weeks or months? Can you modify policies to align with new dealer demographics and risk factors? The new model is in and Experian® is ready to help you give it a ride. Purchase auto credit data now.

VantageScore® models are the only credit scoring models to employ the same characteristic information and model design across the three credit bureaus.

With the holidays around the corner, retailers are getting ready to release their holiday campaigns.

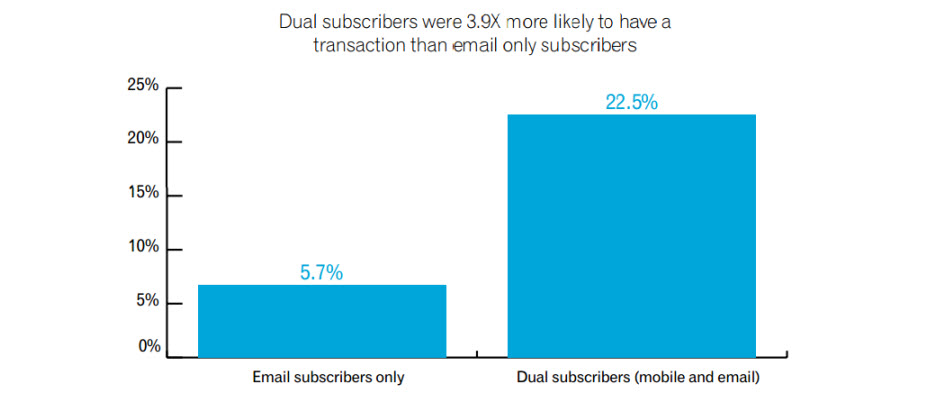

While mobile subscriber lists typically are much smaller than email lists, mobile subscribers tend to be loyal and highly engaged customers.

A recent Experian study found student loans have increased by 84% since the recession (from 2008 to 2014), surpassing credit card debt, home-equity loans and lines of credit, and automotive debt.