All posts by Guest Contributor

Driver of success: Mitigate auto lending risk A culture of learning is a key driver of success. Does your risk culture continue to adapt? There are many issues within auto lending that are unique to other financial services ecosystems: the direct versus indirect relationship, insights of the asset influencing the risk insights, new versus used vehicle transactions influencing risk and terms, and more. However, there is one universal standard common to all financial services cultures — change.. Change is constant, and an institution’s marketing and risk organizations need to be constantly learning to stay abreast of dealer, consumer, competitor and regulatory issues. No one has said it better than Jack Welch: “An organization’s ability to learn, and translate that learning into action rapidly, is the ultimate competitive advantage.” This statement was quickly followed by a command: “Change before you have to.” So the challenge for the portfolio manager is to ensure there are the system features, data sources, management reporting structures, data access features, analytic skills, broad management team skill sets, and employee feedback and incentive plans to drive the organization to a constant state of renewal. The challenge for many smaller and midsize lenders is to determine what systems and skills need to be in-house and what tasks are better left for a third party to handle. For consumer-level data, vehicle history and valuation data, and fraud alert flags, it seems reasonable to leverage solutions from established third parties: credit reporting agencies. After that, the solutions to the many other needs may be more specific to the lender legacy skill set and other support relationships: Are there strong in-house data-management and analytic skills? There is a significant difference between management information and data analysis driving policy and portfolio performance forecasts. Does the internal team have both? Is the current operating platform(s) feature-rich and able to be managed and enhanced by internal resources within tight time frames? Is the management team broadly experienced and constantly updating best-practice insights? Is the in-house team frequently engaged with the regulatory community to stay abreast of new mandates and initiatives? There is a solution. Experian® offers the data, software, solutions, management information, analytic solutions and consulting services to tie everything together for a lender-specific best configuration. We look forward to hearing from you to discuss how we can help.

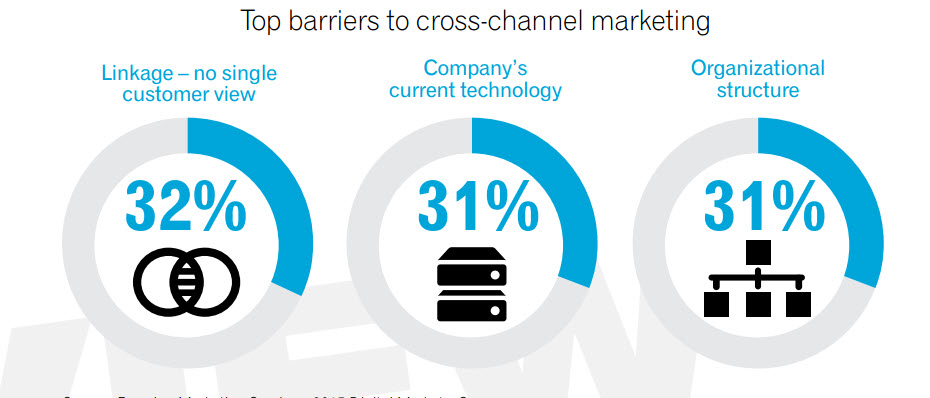

According to a recent Experian Marketing Services study, 99% of companies believe achieving a single customer view is important to their business, but only 24% have a single customer view today.

According to the latest State of the Automotive Finance Market report, consumers are continuing to extend loan terms as a way to keep payments low.

A recent Experian study on data insights found that 83% of chief information officers see data as a valuable asset that is not being fully exploited within their organization, resulting in the need for more organizations to appoint a dedicated chief data officer (CDO).

While auto delinquencies declined slightly year over year (3.01% for accounts 30 days past due or greater in Q2 2015 versus 3.03% a year earlier), it is interesting to note the variance in delinquency by lender channel.

Solving the regulatory compliance issue: In terms of best practice, it all really starts with the data, creating sound risk management strategies, and...

According to the latest Experian-Oliver Wyman Market Intelligence Report, mortgage originations for Q2 2015 increased 56% over Q2 2014 — $547 billion versus $350 billion.

According to a recent Experian analysis, millennials (ages 19–34) are now the largest segment of the U.S. population and are also the least credit savvy group.

Surveillance and fraud staging are the seemingly benign and often-transparent account activities that fraudsters undertake after an account has been compromised but before that compromise has been detected or money is moved.

According to VantageScore® Solutions' annual validation study, VantageScore 3.0 scores 36 million incremental consumers considered unscoreable by conventional credit scoring models.

According to the latest Experian-Oliver Wyman Market Intelligence Report, mortgage originations increased 25% year over year in Q1 2015 to $316 billion.

According to a recent Experian survey, 68% of vacationers spend more money than expected when traveling, often relying on credit cards to make up the difference. Millennials rank even higher when it comes to risky vacation spending. One-third report they have not been saving up in advance of vacation, 72% say they spend more than expected when traveling, and 50% plan to use their tax refund to pay for summer travel this year. Lenders can educate consumers about the impact of utilization on credit scores and reduce loss rates by offering According to a recent Experian survey, 68% of vacationers spend more money than expected when traveling, often relying on credit cards to make up the difference. Millennials rank even higher when it comes to risky vacation spending. One-third report they have not been saving up in advance of vacation, 72% say they spend more than expected when traveling, and 50% plan to use their tax refund to pay for summer travel this year. Lenders can educate consumers about the impact of utilization on credit scores and reduce loss rates by offering personalized credit-education services.personalized credit-education services. >> Infographic: Setting a budget for summer travel

A recent Experian survey found that while consumers are getting better about protecting their information on a regular basis, many do not take the same precautions when traveling. According to the survey, 1 in 5 consumers has had an item with sensitive information lost or stolen while traveling, and 39% have experienced identity theft while traveling or know someone who has. Organizations can protect themselves and customers by using innovative fraud-detection tools designed to reduce potential losses while preserving the customer experience. >> Video: The reputational impact of fraud and identity theft

I would talk about three opportunities that the energy utility vertical could and should take advantage of.

While an influx of small businesses opened during the height of the recession, a recent Experian study found that between 2010 and 2014, small-business start-ups decreased by nearly 45%.