Tag: alternative data

Credit reports and conventional credit scores give lenders a strong starting point for evaluating applicants and managing risk. But today's competitive environment often requires deeper insights, such as credit attributes. Experian develops industry-leading credit attributes and models using traditional methods, as well as the latest techniques in machine learning, advanced analytics and alternative credit data — or expanded Fair Credit Reporting Act (FCRA)-regulated data)1 to unlock valuable consumer spending and payment information so businesses can drive better outcomes, optimize risk management and better serve consumers READ MORE: Using Alternative Credit Data for Credit Underwriting Turning credit data into digestible credit attributes Lenders rely on credit attributes — specific characteristics or variables based on the underlying data — to better understand the potentially overwhelming flow of data from traditional and non-traditional sources. However, choosing, testing, monitoring, maintaining and updating attributes can be a time- and resource-intensive process. Experian has over 45 years of experience with data analytics, modeling and helping clients develop and manage credit attributes and risk management. Currently, we offer over 4,500 attributes to lenders, including core attributes and subsets for specific industries. These are continually monitored, and new attributes are released based on consumer trends and regulatory requirements. Lenders can use these credit attributes to develop precise and explainable scoring models and strategies. As a result, they can more consistently identify qualified prospects that might otherwise be missed, set initial limits, manage credit lines, improve loyalty by applying appropriate treatments and limit credit losses. Using expanded credit data effectively Leveraging credit attributes is critical for portfolio growth, and businesses can use their expanding access to credit data and insights to improve their credit decisioning. A few examples: Spot trends in consumer behavior: Going beyond a snapshot of a credit report, Trended 3DTM attributes reveal and make it easier to understand customers' behavioral patterns. Use these insights to determine when a customer will likely revolve, transact, transfer a balance or fall into distress. Dig deeper into credit data: Making sense of vast amounts of credit report data can be difficult, but Premier AttributesSM aggregates and summarizes findings. Lenders use the 2,100-plus attributes to segment populations and define policy rules. From prospecting to collections, businesses can save time and make more informed decisions across the customer lifecycle. Get a clear and complete picture: Businesses may be able to more accurately assess and approve applicants, simply by incorporating attributes overlooked by traditional credit bureau reports into their decisioning process. Clear View AttributesTM uses data from the largest alternative financial services specialty bureau, Clarity Services, to show how customers have used non-traditional lenders, including auto title lenders, rent-to-own and small-dollar credit lenders. The additional credit attributes and analysis help lenders make more strategic approval and credit limit decisions, leading to increased customer loyalty, reduced risk and business growth. Additionally, many organizations find that using credit attributes and customized strategies can be important for measuring and reaching financial inclusion goals. Many consumers have a thin credit file (fewer than five credit accounts), don’t have a credit file or don’t have information for conventional scoring models to score them. Expanded credit data and attributes can help lenders accurately evaluate many of these consumers and remove barriers that keep them from accessing mainstream financial services. There's no time to wait Businesses can expand their customer base while reducing risk by looking beyond traditional credit bureau data and scores. Download our latest e-book on credit attributes to learn more about what Experian offers and how we can help you stay ahead of the competition. Download e-book Learn more 1When we refer to “Alternative Credit Data," this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data" may also apply in this instance and both can be used interchangeably.

From awarding bonus points on food delivery purchases to incorporating social media into their marketing efforts, credit card issuers have leveled up their acquisition strategies to attract and resonate with today’s consumers. But as appealing as these rewards may seem, many consumers are choosing not to own a credit card because of their inability to qualify for one. As card issuers go head-to-head in the battle to reach and connect with new consumers, they must implement more inclusive lending strategies to not only extend credit to underserved communities, but also grow their customer base. Here’s how card issuers can stay ahead: Reach: Look beyond the traditional credit scoring system With limited or no credit history, credit invisibles are often overlooked by lenders who rely solely on traditional credit information to determine applicants’ creditworthiness. This makes it difficult for credit invisibles to obtain financial products and services such as a credit card. However, not all credit invisibles are high-risk consumers and not every activity that could demonstrate their financial stability is captured by traditional data and scores. To better evaluate an applicant’s creditworthiness, lenders can leverage expanded data sources, such as an individual’s cash flow or bank account activity, as an additional lens into their financial health. With deeper insights into consumers’ banking behaviors, card issuers can more accurately assess their ability to pay and help historically disadvantaged populations increase their chances of approval. Not only will this empower underserved consumers to achieve their financial goals, but it provides card issuers with an opportunity to expand their customer base and improve profitability. Connect: Become a financial educator and advocate Credit card issuers looking to build lifelong relationships with new-to-credit consumers can do so by becoming their financial educator and mentor. Many new-to-credit consumers, such as Generation Z, are anxious about their finances but are interested in becoming financially literate. To help increase their credit understanding, card issuers can provide consumers with credit education tools and resources, such as infographics or ‘how-to’ guides, in their marketing campaigns. By learning about the basics and importance of credit, including what a credit score is and how to improve it, consumers can make smarter financial decisions, boost their creditworthiness, and stay loyal to the brand as they navigate their financial journeys. Accessing credit is a huge obstacle for consumers with limited or no credit history, but it doesn’t have to be. By leveraging expanded data sources and offering credit education to consumers, credit card issuers can approve more creditworthy applicants and unlock barriers to financial well-being. Visit us to learn about how Experian is helping businesses grow their portfolios and drive financial inclusion. Visit us

Many financial institutions have made inclusion a strategic priority to expand their reach and help more U.S. consumers access affordable financial services. To drive deeper understanding, Experian commissioned Forrester to do new research to identify key focal points for firms and how they are moving the needle. The study found that more than two-thirds of institutions had a strategy created and implemented while one-quarter reported they are already up and running with their inclusion plans.1 Tapping into the underserved The research examines the importance of engaging new audiences such as those that are new to credit, lower-income, thin file, unbanked and underbanked as well as small businesses. To tap into these areas, the study outlines the need to develop new products and services, adopt willingness to change policies and processes, and use more data to drive better decisions and reach.2 Expanded data for improved risk decisioning The research underlines the use of alternative data and emerging technologies to expand reach to new audiences and assist many who have been underserved. In fact, sixty-two percent of financial institutions surveyed reported they currently use or are planning to use expanded data to improve risk profiling and credit decisions, with focus on: Banking data Cash flow data Employment verification data Asset, investments, and wealth management data Alternative financial services data Telcom and utility data3 Join us to learn more at our free webinar “Reaching New Heights Together with Financial Inclusion” where detailed research and related tools will be shared featuring Forrester’s principal analyst on Tuesday, May 24 from 10 – 11 a.m. PT. Register here for more information. Find more financial inclusion resources at www.experian.com/inclusionforward. Register for webinar Visit us 1 Based on Forrester research 2 Ibid. 3 Ibid.

“Disruption has caused enormous amounts of innovation,” said Jennifer Schulz, CEO of Experian, North America. “We must continue to be the disruptors in our industry which takes effort, data, technology, bright minds and vision for what the future will be.” Schulz kicked off the 39th Vision conference with a future-focused keynote delivered to a crowd of more than 400 attendees. Alex Lintner, Group President, Experian Consumer Information Services, talked about the next phase of great, highlighting the digital transformation that has taken place in the generations of the past and the disruption and innovation happening today and in the future. Keynote speaker: Dr. Mohamed A. El-Erian Dr. Mohamed A. El-Erian, renowned economist and author, President of Queens’ College, Cambridge, Chief Economic Advisor at Allianz, Chair of President Obama’s Global Development Council and Former CEO and Co-Chief Investment Officer of PIMCO, spoke about the Fed, inflation, negative interest rates and the labor market, as well as the importance of inclusion. El-Erian, who said he reads the Financial Times religiously, acknowledged that we will make mistakes on the journey as we work to be even more inclusive. To navigate what’s ahead, he said we will need resilience, optionality and agility. “It’s important to connect with information, acknowledge the insecurity, in a language people understand, in order to connect,” he said. Session highlights – day 1 The conference hall was buzzing with conversations, discussions and thought leadership. Buy Now Pay Later A large audience was in attendance for a session that introduced Experian’s Buy Now Pay Later Bureau™ and explored how it’s the first and only solution of its kind — serving consumers, BNPL providers, financial institutions and regulators. Identity Identity is constantly evolving, and while biometrics and authentication may have become ubiquitous, there is much activity around the concepts of eIDs, identity wallets and identity networks. Experian is making identities personal and helping businesses to recognize, manage and connect customer identities in new ways using data, analytics and technology. Marketing In today’s hypercompetitive world, businesses need to engage the freshest data and increase velocity when it comes to time to market. An average of 120 days won’t cut it. Ascend Marketing speeds time to market and helps achieve higher ROI. Regulatory Landscape With so much happening at Capitol Hill, a panel of experts from DC discussed a number of topics and proposals (and their impacts), including the defense for risk-based pricing, the impact of suppressing negative data, and trending topics like Buy Now Pay Later and data portability. All the while, the tech showcase had a constant flow of attendees with demos ranging from data and decisioning to financial inclusion and technology. This is just the beginning. And as Schulz said, “There’s more to do.” More insights from Vision to come. Follow @ExperianVision to see more of the action.

For decades, the credit scoring system has relied on traditional data that only examines existing credit captured on a credit report – such as credit utilization ratio or payment history – to calculate credit scores. But there's a problem with that approach: it leaves out a lot of consumer activity. Indeed, research shows that an estimated 28 million U.S. adults are “credit invisible," while another 21 million are “unscorable."1 But times are changing. While conventional credit scoring systems cannot generate a score for 19 percent of American adults,1 many lenders are proactively turning to expanded FCRA-regulated data – or "alternative data" – for solutions. Types of expanded FCRA-regulated data By tapping into technology, lenders can access expanded FCRA-regulated data, which offers a powerful and complete view of consumers' financial situations. Expanded public record data This can include professional and occupational licenses, property deeds and address history – a step beyond the limited public records information found in standard credit reports. Such expanded public record data is available through consumer reporting agencies and does not require the customer's permission to use it since it's a public record.1 “Experian has partnerships with these agencies and can access public records that provide insight into factors like income and housing stability, which have a direct correlation with how they'll perform," said Greg Wright, Chief Product Officer for Experian Consumer Information Services. “For example, lenders can see if a consumer's professional license is in good standing, which is a strong correlation to income stability and the ability to pay back a loan." Rental payment data Experian RentBureau draws updated rental payment history data every 24 hours from property managers, electronic rent payment services and collection companies. It can also track the frequency of address changes. “Such information can be a good indicator of risk," said Wright. “It allows lenders to make informed judgments about the financial health and positive payment history of consumers." Consumer-permissioned data With permission from consumers, lenders can look at different types of financial transactions to assess creditworthiness. Experian Boost™, for example, enables consumers to factor positive payment history, such as utilities, cell phone or even streaming services, into an Experian credit file. “Using the Experian Boost is free, and for most users, it instantly improves their credit scores," said Wright. “Overall, those 'boosted' credit scores allow for fairer decisioning and better terms from lenders – which gives customers a second chance or opportunity to receive better terms." Financial Management Insights Financial Management Insights considers data that is not captured by the traditional credit report such as cash flow and account transactions. For instance, this could include demand deposit account (DDA) data, like recurring payroll deposits, or prepaid account transactions. “Examining bank account transaction data, prepaid accounts, and cash flow data can be a good indicator of ability to pay as it helps verify income, which gives lenders insights into consumers' cash flow and ability to pay," Wright added. Clarity Credit Data With Experian's Clarity Credit Data, lenders can see how consumers use expanded FCRA-regulated data along with their related payment behavior. It provides visibility into critical non-traditional loan information, including more insights into thin-file and no-file segments allowing for a more comprehensive view of a consumer's credit history. Lift Premium™ By using multiple sources of expanded FCRA-regulated data to feed composite scores, along with artificial intelligence and machine learning, Lift Premium™ can vastly increase the number of consumers who can be scored. For example, research shows that Lift Premium™ can score 96 percent of American adults – a significant increase from the 81 percent that are scorable with conventional scores relying on only traditional credit data. Additionally, such enhanced composite scores could enable 6 million of today's subprime population to qualify for “mainstream" (prime or near-prime) credit.1 How is expanded FCRA-regulated data changing the credit scoring system? The current credit scoring system is rapidly evolving, and modern technology is making it easier for lenders to access expanded FCRA-regulated data. Indeed, this data disruption is changing lender business in a positive way. “When lenders use expanded credit data assets, they see that many unscorable and credit invisible consumers are in fact creditworthy," said Wright. “Layering in expanded FCRA-regulated data gives a clearer picture of consumers' financial situation." By expanding data assets, tapping into artificial intelligence and machine learning, lenders can now score many more consumers quickly and accurately. Moreover, forward-thinking lenders see these expanded data assets as offering a competitive edge: it's estimated that modern credit scoring methods could allow lenders to grow their pool of new customers by almost 20 percent.1 Case study: Consumer-permissioned data To date, over 9 million people have used Experian Boost. The technology uses positive payment history as a way to recognize customers who exhibit strong credit behaviors outside of traditional credit products. “Boosted" consumers were able to add on average 14 points to their FICO scores in 2022 so far, making many eligible for additional financial products with better terms or better product offerings. Active Boost consumers, post new origination performed on par or better than the average U.S. originator, consistently over time. “In other words, having this additional lens into a consumer's financial health means lenders can expand their customer base without taking on additional credit risk," explains Wright. The bottom line The world of credit data is undergoing a revolution, and forward-thinking lenders can build a sound business strategy by extending credit to consumers previously excluded from it. This not only creates a more equitable system, but also expands the customer base for proactive lenders who see its potential in growing business. Learn more 1Oliver Wyman white paper, “Financial Inclusion and Access to Credit,” January 12, 2022.

Millions of consumers are excluded from the credit economy, whether it’s because they have limited credit history, dated information within their credit file, or are a part of a historically disadvantaged group. Without credit, it can be difficult for consumers to access the tools and services they need to achieve their financial goals. This February, Experian surveyed over 1,000 consumers across census demographics, including income, ethnicity, and age, to understand the perceptions, needs, and barriers underserved communities face along their credit journey. Our research found that: 75% of consumers with an average household income of less than $50,000 have less than $1,000 in savings. 1 in 5 consumers with an average household income of less than $35,000 say they’re confident in getting approved for credit. 80% of respondents who are not or slightly confident in getting approved for credit were women. When asked why they believed they would not get approved for credit, participants shared common responses, such as having poor payment history, a low credit score, and insufficient income. Given these findings, what can lenders provide to help underserved consumers strengthen their financial profiles and gain access to the credit they need and deserve? The power of credit education While only 20% of respondents were familiar with credit education tools, the majority expressed interest in these offerings. With Experian, lenders can develop and implement credit education programs, tools, and solutions to help consumers understand their credit and the impact certain choices can have on their credit scores. From interactive tools like Score Simulator and Score Planner to real-time alerts from Credit Monitoring, consumers can actively assess their financial health, take steps to improve their creditworthiness, and ultimately become better candidates for credit offers. In turn, consumers can feel more confident and empowered to achieve their financial goals. Credit education tools not only help consumers increase their credit literacy, confidence, and chances of approval, but they also create opportunities for lenders to build lasting customer relationships. Consumers recognize that healthy credit plays an important role in their financial lives, and by helping them navigate the credit landscape, lenders can increase engagement, build loyalty, and enhance their brand’s reputation as an organization that cares about their customers. Empowering consumers with credit education is also a way for lenders to unlock new revenue streams. By learning to borrow, save, and spend responsibly, consumers can improve their creditworthiness and be in a better position to accept extended credit offerings, driving more cross-sell and upsell opportunities for lenders. More ways experian can help Experian is deeply committed to helping marginalized and low-income communities access the financial resources they need. In addition to our credit education tools, here are a few of our other offerings: Our expanded data helps lenders make better lending decisions by providing greater visibility and transparency around a consumer’s inquiry and payment behaviors. With a holistic view of their current and prospective customers, lenders can more accurately identify creditworthy applicants, uncover new growth opportunities, and expand access to credit for underserved consumers. Experian GoTM is a free, first-of-its-kind program to help credit invisibles and those with limited credit histories begin building credit on their own terms. After authenticating their identities and obtaining an Experian credit report, users will receive ongoing education about how credit works and recommendations to further build their credit history. To learn more about building profitable customer relationships with credit education, check out our credit education solutions and watch our Three Ways to Uncover Financial Growth Opportunities that Benefit Underserved Communities webinar. Learn more Watch webinar

As more consumers apply for credit and increase their spending1, lenders and financial institutions have an opportunity to expand their portfolios and improve profitability. The challenge is ensuring they’re extending credit responsibly and inclusively. Millions of Americans, many of whom are creditworthy, lack access to mainstream credit options. This may be because they have limited or no credit history, negative information within their credit file, or are a part of a historically disadvantaged group. To say “yes” to consumers they otherwise couldn’t or wouldn’t lend to, lenders must gain a deeper understanding of an individual’s stability, ability and willingness to pay. That’s where expanded FCRA-regulated and trended data come in. While traditional credit data has long been the primary means of gauging creditworthiness, it doesn’t tell the full story of a consumer’s financial situation. Let’s explore how differentiated data can help lenders make more informed credit decisions. Using differentiated data for deeper lending Expanded FCRA-regulated data provides supplemental credit data to help lenders gain a more holistic view of their current and prospective customers. Some examples of expanded FCRA-regulated data include alternative financial services data from nontraditional lenders, consumer-permissioned account data, rental payments and full-file public records. Because this data drives greater visibility and transparency around inquiry and payment behaviors, lenders can more accurately determine a consumer’s ability to pay and distinguish between reliable and high-risk applicants. In turn, lenders can approve more creditworthy consumers, grow their portfolios and increase financial opportunities for underserved communities, all while preventing and mitigating risk. 89% of lenders agree that expanded FCRA-regulated data allows them to extend credit to more consumers. Trended data empowers lenders with predictive insights into consumers by providing key balance and payment data for the previous 24 months. This is important as lenders can determine if a consumer’s credit behavior has improved or deteriorated over time. In turn, lenders can: Identify creditworthy customers: Establish if a consumer has a demonstrated ability to pay, is consistently paying more than the minimum payment, or shows no signs of payment stress. Increase response rates: Match the right products with the right prospects. Determine upsell and cross-sell opportunities: Present relevant offers based on anticipated needs and behaviors. Limit loss exposure: Understand the direction and velocity of payment performance to effectively manage risk exposure. Trended data helps lenders better predict future behavior, manage portfolio risk and design the best marketing offers. Turning insights into action Together, trended and expanded FCRA-regulated data benefit lenders and consumers alike. With a more holistic view of their customers, lenders gain powerful insights to lend deeper, ultimately helping them to expand their portfolios and drive greater access to credit for underserved communities. Learn more 1 The Recovery of Credit Applications to Pre-Pandemic Levels, Consumer Financial Protection Bureau, 2021.

Lenders are under pressure to improve access to financial services, but can it also be a vehicle for driving growth? With the global pandemic and social justice movements exposing societal issues of equity, financial institutions are being called upon to do their part to address these problems, too. Lenders are increasingly under pressure to improve access to the financial system and help close the wealth gap in America. Specifically, there are calls to improve financial inclusion – the process of ensuring financial products and services are accessible and affordable to everyone. Financial inclusion seeks to remove barriers to accessing credit, which can ultimately help individuals and businesses create wealth and elevate communities. Activists and regulators have singled out the current credit scoring system as a significant obstacle for a large portion of U.S. consumers. From an equity standpoint, tackling financial inclusion is a no-brainer: better access to credit allows more consumers to secure safer housing and better schools, which could lead to higher-paying jobs, as well as the ability to start businesses and get insurance. Being able to access credit in a regulated and transparent way underpins financial stability and prosperity for communities and is key to creating a stronger economic system. Beyond “doing the right thing," research shows that financial inclusion can also fuel business growth for lenders. Get ahead of the game There is mounting regulatory pressure to embrace financial inclusion, and financial institutions may soon need to comply with new mandates. Current lending practices overlook many marginalized communities and low-income consumers, and government agencies are seeking to change that. Government agencies and organizations, such as the Consumer Financial Protection Bureau (CFPB) and Office of the Comptroller of the Currency (OCC), are requiring greater scrutiny and accountability of financial institutions, working to overhaul the credit reporting system to ensure fairness and equality. As a lender, it makes good business sense to tackle this problem now. For starters, as more institutions embrace Corporate Social Responsibility (CSR) mandates—something that's increasingly demanded by shareholders and customers alike—financial inclusion is a natural place to start. It demonstrates a commitment to CSR principles and creates a positive brand built on equity. Further, financial institutions that embrace these changes gain an early adopter advantage and can build a loyal customer base. As these consumers begin to build wealth and expand their use of financial products, lenders will be able to forge lifelong relationships with these customers. Why not get a head start on making positive organizational change before the law compels it? Grow your business (and profits) To be sure, financial inclusion is a pressing moral imperative that financial institutions must address. But financial inclusion doesn't come at the expense of profit. It represents an enormous opportunity to do business with a large, untapped market without taking on additional risk. In many instances, unscorable and credit invisible consumers exhibit promising credit characteristics, which the conventional credit scoring system does not yet recognize. Consider consumers coming to the U.S. from other countries. They may have good credit histories in their home countries but have not yet established a credit history here. Likewise, many young, emerging consumers haven't generated enough history to be categorized as creditworthy. And some consumers may simply not utilize traditional credit instruments, like credit cards or loans. Instead, they may be using non-bank credit instruments (like payday loans or buy-now-pay-later arrangements) but regularly make payments. Ultimately, because of the way the credit system works, research shows that lenders are ignoring almost 20 percent of the U.S. population that don't have conventional credit scores as potential customers. These consumers may not be inherently riskier than scored consumers, but they often get labelled as such by the current credit scoring system. That's a major, missed opportunity! Modern credit scoring tools can help fill the information gap and rectify this. They draw on wider data sources that include consumer activities (like rent, utility and non-bank loan payments) and provide holistic information to assist with more accurate decisioning. For example, Lift Premium™ can score 96 percent of Americans with this additional information—a vast improvement over the 81 percent who are currently scored with conventional credit data.1 By tapping into these tools, financial institutions can extend credit to underserved populations, foster consumer loyalty and grow their portfolio of profitable customers. Do good for the economy Research suggests that financial inclusion can provide better outcomes for both individuals and economies. Specifically, it can lead to greater investment in education and businesses, better health, lower inequality, and greater entrepreneurship. For example, an entrepreneur who can access a small business loan due to an expanded credit scoring model is subsequently able to create jobs and generate taxable revenue. Small business owners spend money in their communities and add to the tax base – money that can be used to improve services and attract even more investment. Of course, not every start-up is a success. But if even a portion of new businesses thrive, a system that allows more consumers to access opportunities to launch businesses will increase that possibility. The last word Financial inclusion promotes a stronger economy and thriving communities by opening the world of financial services to more people, which benefits everyone. It enables underserved populations to leverage credit to become homeowners, start businesses and use credit responsibly—all markers of financial health. That in turn creates generational wealth that goes a long way toward closing the wealth gap. And widening the credit net also enables lenders to uncover new revenue sources by tapping new creditworthy consumers. Expanded data and advanced analytics allow lenders to get a fuller picture of credit invisible and unscorable consumers. Opening the door of credit will go a long way to establishing customer loyalty and creating opportunities for both consumers and lenders. Learn more

Fintechs have been an enormously disruptive force of change in financial services over the past 10 years. From digital payments, lending, insurance, digital banks, to personal finance and many other subsectors in between, fintechs have rapidly transformed everything from business and operating models to customer expectations. It’s this innovative drive that is celebrated and fostered each year at LendIt Fintech - a conference that brings together the fintech and financial services community to connect and reimagine the future of finance. And there may not be another year on record that called for the reimagining of finance more than 2020. Last year, the financial services industry – from consumers, fintechs and other subdivisions across the globe – endured many changes and challenges due to the COVID-19 pandemic. But it also brought accelerated innovations; and with them, increased customer expectations and a focus on financial equity and inclusion. As consumer credit scores and demand for credit continue to rise, fintechs have an opportunity to re-examine what credit looks like in a post-COVID lending environment, and explore opportunities for growth in 2021. Experian’s Chief Product Officer Greg Wright tackled this topic at the recent Lendit Fintech conference, alongside Ibo Dusi of Happy Money, Myles Reaz of Upgrade and the Garry Reeder with the American Fintech Council. Watch the full panel discussion in the video below and hear more about: How panelists define data, alternative data and how it factors in their lending How alternative data can help drive financial inclusion and get to a ‘yes’ more often with consumers Using data to make the consumer experience more frictionless and seamless For more information about how Experian can help fintech organizations of all sizes reach their business and lending goals, visit our fintech solutions page. Explore Experian's Fintech Solutions

Financial services companies have long struggled to make inclusive decisions for small businesses and for low- and moderate-income consumers. One key reason: to make accurate predictions of the financial risks associated with those customers’ accounts requires lenders to rely on a wider variety of data than a credit score alone. To accurately assess risk, expanded Fair Credit Reporting Act regulated data is helpful – including rental data, trended data, enhanced public records, alternative financial services data and more. This expanded FCRA data is one key to financial inclusion. Without that data, lenders risk rejecting potentially profitable customers, including so-called credit invisibles and thin file consumers. In fact, The Federal Reserve, along with four important financial services regulators, highlighted the consumer benefits of alternative data in their December 2019 interagency statement. That statement also highlighted the increased importance of managing compliance when firms use alternative data in credit underwriting. With hundreds of data sources available to help with important tasks such as verifying identity, checking credit, and assessing the value of automotive and real-estate collateral, why have some lenders been slow to use the most appropriate data attributes when making credit decisions? One reason is a matter of IT Architecture; another is priorities. Changing a business process to take advantage of new data requirements can be prohibitively lengthy and costly – in terms of both analytical and IT resources. This is especially true for older systems—which were seldom adapted to use Application Programming Interfaces (APIs) supporting modern data structures such as JSON. Furthermore, data access to older systems can require specific types of system connectivity such as VPNs or leased lines. Latency is important in this type of application: some of these tasks have to be done instantly in a digital-first or digital-only lending environment. So is time to market: lenders deploying analytics processes cannot wait for overtaxed IT teams to complete lengthy projects. Lenders’ analytics and IT teams have long known they need to be more agile and efficient, faster to market, and increasingly secure. Their answer, largely, has been a slow but steady migration of their systems to the cloud. A 2019 McKinsey survey revealed that CIOs were modernizing their infrastructures primarily to achieve four goals: agility and time to market, quality and reliability, cost, and security. There are other benefits as well. But if the business case for a cloud strategy was somewhat clear to IT and analytics leaders, it became crystal clear to the rest of the business in 2020. As companies shifted to at-home work using cloud-based collaboration tools, especially videoconferencing services, most companies conquered what was perhaps the final barrier to entry—the fear that the issues of data privacy and security were somehow more insurmountable with virtual machines, containers, and microservices than with on-premise infrastructure. Last quarter, the leading cloud providers Amazon Web Services, Google Cloud Platform, and Microsoft Azure reported incredible annual revenue growth: 29%, 45%, and 48% respectively. COVID-19 has proven to be the catalyst that greatly sped up the transition to cloud technologies. The jump to the cloud means that lenders are suddenly more capable than ever at making analytically sound – and therefore more financially inclusive decisions. The key to analytical decision-making is to use the right data and to make the most appropriate calculations (called attributes) as part of a business strategy or a mathematical model. With Experian programs such as Attribute Toolbox now available in the cloud, calculating those all-important attributes is as simple for the IT department as coding an API call. Lenders will soon be able just as easily to retrieve and process raw data from over 100 data sources, to recognize their native formats and to extract the desired information quickly enough for real-time and batch decisioning. The pandemic has brought economic distress to millions of Americans—it is unlike anything in our lifetimes. The growth of cloud computing promises to enable these consumers to obtain additional products as well as more favorable pricing and terms. It’s ironic that COVID has accelerated the adoption of the very technologies that will expand access to credit for many people who cannot currently access it from mainstream financial firms. To learn more about our Attribute Toolbox, click here. Learn More

Big data is bringing changes to the way credit scores are reported and making it easier for lenders to find creditworthy consumers, and for consumers to qualify for the financing they need. Since last year’s annual report, alternative credit data1 has continued to gain in popularity. In Experian’s latest 2020 State of Alternative Credit Data report, we take a closer look at why alternative credit data is supplemental and essential to consumer lending and how it’s being adopted by both consumers and financial institutions. While the topic of alternative credit data has become more well known, its capabilities and benefits are still not widely discussed. For instance, did you know that … 89% of lenders agree that alternative credit data allows them to extend credit to more consumers. 96% of lenders agree that in times of economic stress, alternative credit data allows them to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure. 3 out of 4 consumers believe they are a better borrower than their credit score represents. Not only do consumers believe they’re more financially astute than their credit score depicts – but they’re happy to prove it, with 80% saying they would share various types of financial information with lenders if it meant increased chances for approval or improved interest rates. This year’s report provides a deeper look into lenders’ and consumers’ perceptions of alternative credit data, as well as an overview of the regulatory landscape and how alternative credit data is being used across the lending marketplace. Lenders who incorporate alternative credit data and machine learning techniques into their current processes can harness the data to unlock their portfolio’s growth potential, make smarter lending decisions and mitigate risk. Learn more in the 2020 State of Alternative Credit Data white paper. Download now

In today’s uncertain economic environment, the question of how to reduce portfolio volatility while still meeting consumers’ needs is on every lender’s mind. With more than 100 million consumers already restricted by traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By leveraging alternative credit data, you can continue to support your borrowers and expand your lending universe. In our most recent podcast, Experian’s Shawn Rife, Director of Risk Scoring and Alpa Lally, Vice President of Data Business, discuss how to enhance your portfolio analysis after an economic downturn, respond to the changing lending marketplace and drive greater access to credit for financially distressed consumers. Topics discussed, include: Making strategic, data-driven decisions across the credit lifecycle Better managing and responding to portfolio risk Predicting consumer behavior in times of extreme uncertainty Listen in on the discussion to learn more. Experian · Effective Lending in the Age of COVID-19

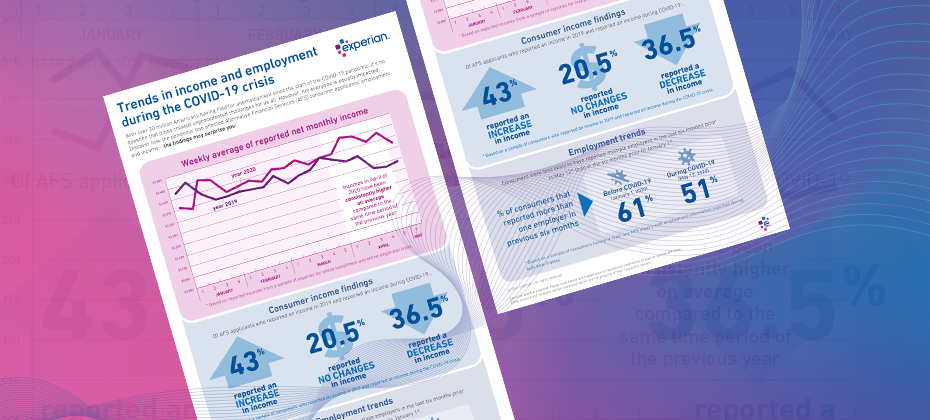

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

The current pandemic will affect the way financial institutions lend and provide credit. Shawn Rife, Experian’s Director of Product Scoring, discusses the ways that financial institutions can navigate the COVID-19 crisis. Check out what he had to say: What implications does the global pandemic have on financial institutions’ analytical needs? SR: In the customer lifecycle, there are 4 different stages: prospecting, acquisitions, portfolio management, and collections. During times of economic uncertainty, lenders typically take additional actions to ensure that there’s a first line of defense against delinquencies and payment stress. Expanding their focus to incorporate account review/portfolio management becomes particularly important. During this time, clients will be looking for leadership, early warning signs, and ways to recession-proof their portfolios (account management), while growing and maintaining their approvals in a healthy way (originations). Lenders may be well advised to delay any focus on collections, since many consumers may be facing major payment stress through no mismanagement of their own doing. Another critical component is with the rollout of government stimulus packages, which lenders can use to identify people in stress who could benefit for second chance opportunities they may not have otherwise been able to receive. As more consumers seek credit, from an analytics perspective, what considerations should financial institutions be making during this time? SR: Financial institutions should be assessing and pre-identifying situations that might place consumers in positions of elevated financial stress. That way, organizations can implement solutions to identify and help at-risk consumers before they fall delinquent. The recent Coronavirus Aid, Relief, and Economic Security Act (CARES Act) – coupled with Experian’s score treatment, are designed to protect consumers against score declines during times of crisis. Furthermore, lenders can provide forbearance and loan deferment programs to help consumers. For lenders, credit risk scores, models, and attributes are the best ways to identify – and even predict - delinquency risk. The FICO® Resilience Index can also identify consumers who are particularly susceptible to delinquency risk directly due to macroeconomic uncertainty. This gives lenders the opportunity to evaluate their portfolios for loss and connect with consumers who may be in need of further support. What is the smartest next play for financial institutions? SR: For financial institutions, the smart play is to add alternative data into their data-driven decisioning strategies as much as possible. Alternative data works to enhance your ability to see a consumer’s entire credit portfolio, which gives lenders the confidence to continue to lend – as well as the ability to track and monitor a consumer’s historical performance (which is a good indicator of whether or not a consumer has both the intention and ability to repay a loan). How will the new attribute subset list benefit financial institutions during this time? SR: Experian’s series of crisis attributes is an example of attributes that can be predictive in times of a crisis. These lists were designed to follow the 3 E’s – Expand, Enhance, and provide Ease of use. Enhance – With these attributes, lenders aren’t limited to traditional data. These attributes allow lenders to look at the entirety of a consumer’s credit or repayment behavior and use more data to make better lending decisions. This becomes crucial in a challenging environment. Expand – This data can also help lenders identify consumers who are in the market for products and services, even if there the lending criteria becomes more stringent. This can open doors and new opportunities for 40-50 million new customers, particularly ones that may not fit initial lending criteria. Ease of Use – Experian has put together the most predictive elements that can identify consumer resilience and potential financial stress in this challenging economy. Experian is committed to helping your organization during times of uncertainty. For more resources, visit our Look Ahead 2020 Hub. Learn more Shawn M. Rife, Director of Risk Scoring, Experian Consumer Information Services, North America Shawn Rife manages Experian’s credit risk scoring models, focused on empowering clients to maximize the scope and influence of their lending universe - while minimizing risk - and complying with ever-changing regulatory standards. Shawn also leads the implementation of Alternative Data within the lending environment, as well as key product implementation initiatives. Prior to Experian, Shawn held key consumer insights and predictive analytics roles for Consumer Packaged Goods and internet companies. Over his career, Shawn has focused on market segmentation, competitive research, new product development and consumer advocacy. He also holds a Master’s degree from Harvard University and a Bachelor’s degree in Political Science and Economics.

In today’s rapidly changing economic environment, the looming question of how to reduce portfolio volatility while still meeting consumers' needs is on every lender’s mind. So, how can you better asses risk for unbanked consumers and prime borrowers? Look no further than alternative credit data. In the face of severe financial stress, when borrowers are increasingly being shut out of traditional credit offerings, the adoption of alternative credit data allows lenders to more closely evaluate consumer’s creditworthiness and reduce their credit risk exposure without unnecessarily impacting insensitive or more “resilient” consumers. What is alternative credit data? Millions of consumers lack credit history or have difficulty obtaining credit from mainstream financial institutions. To ease access to credit for “invisible” and subprime consumers, financial institutions have sought ways to both extend and improve the methods by which they evaluate borrowers’ risk. This initiative to effectively score more consumers has involved the use of alternative credit data.1 Alternative credit data is FCRA-regulated data that is typically not included in a traditional credit report and helps lenders paint a fuller picture of a consumer, so borrowers can get better access to the financial services they need and deserve. How can it help during a downturn? The economic environment impacts consumers’ financial behavior. And with more than 100 million consumers already restricted by the traditional scoring methods used today, lenders need to look beyond traditional credit information to make more informed decisions. By pulling in alternative credit data, such as consumer-permissioned data, rental payments and full-file public records, lenders can gain a holistic view of current and future customers. These insights help them expand their credit universe, identify potential fraud and determine an applicant’s ability to pay all while mitigating risk. Plus, many consumers are happy to share additional financial information. According to Experian research, 58% say that having the ability to contribute positive payment history to their credit files makes them feel more empowered. Likewise, many lenders are already expanding their sources for insights, with 65% using information beyond traditional credit report data in their current lending processes to make better decisions. By better assessing risk at the onset of the loan decisioning process, lenders can minimize credit losses while driving greater access to credit for consumers. Learn more 1When we refer to “Alternative Credit Data,” this refers to the use of alternative data and its appropriate use in consumer credit lending decisions, as regulated by the Fair Credit Reporting Act. Hence, the term “Expanded FCRA Data” may also apply in this instance and both can be used interchangeably.