Topics

By: Joel Pruis I am going to take some liberties here. Nowhere in the movie Moneyball does Peter Brand tell us how he got to the magic number of winning 99 games to get to the playoffs. My assumption is that given the way that he evaluates the Oakland A’s, he also evaluations the other teams in their conference. Assessing the competitive landscape provides Brand with the estimated runs their opponents will generate. Now we could take the approach that such analysis would correlate to assessing how your competition is going to perform but I am going to take a different approach. I would compare the conference assessment in Moneyball to be similar to an economic forecast/assessment. We need to assess what are the overall conditions in which we must operate that will allow us to generate the net yield on the assets of our financial institution. Some of the things we need to assess to determine what we will be able to generate related to the net yield on assets would be: Gross yield on assets Current interest rate environment (yield on treasuries, federal home loan bank, etc. Interest rate trends (increasing, declining, trends toward fixed rates, variable rates) Industry information General trend of businesses across the nation How are businesses faring? How well are they paying their creditors? Are they relying more or less on credit? Are new businesses being started? Are they succeeding? Are they failing? General trends (same as above) within your financial institution’s market footprint One such source of the industry information is the Small Business Credit Index generated by Experian & Moody’s Analytics. In the recent release of the Small Business Credit Index, small business is indicating stronger from the prior quarter moving from 104.3 to 109. But this is from a national perspective. Depending on your financial institution, it is important to always get an overall view of the economy but more importantly, what is happening in your particular market footprint. Just as the Oakland A’s in Moneyball maintained an overall perspective of Major League Baseball, their focus for success was targeting their specific conference to reach the playoffs. So as we look at information such as the Small Business Credit Index, we are able to see highlights of regional trends (certain states west of the Mississippi are doing better while certain states along the east coast are not) and specific industry trends. From such data we need to drill down into our specific footprint and current portfolio. We need to review such items as: What industry concentrations do we have that are doing well in the economy and how is our portfolio doing compared to the external data? What industries are we not engaging that may provide a good opportunity for our financial institution? What changes are taking place in the general economy that may impact our ability to achieve our expected results? What external factors must we be monitoring that may impact our strategy (such as the impact of Obamacare and how it will impact the hiring for businesses with more than 50 employees?) Just as in Moneyball, Brand continues to monitor the performance of the overall league (and the individual players for future trades), we need to continually monitor the national, state and local economies to determine what adjustments we will need to make to achieve our strategies. So we have assessed the general environment, on to strategies or “How do we win 99 games with a total payroll of $38 million?”

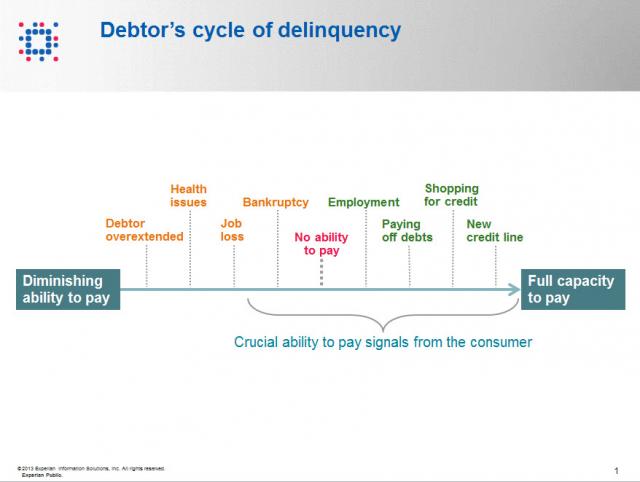

Contact information such as phone numbers and addresses are fundamental to being able to reach a debtor, but knowing when to reach out to the debtor is also a crucial factor impacting success or failure in getting payment. As referenced in the chart below, when a consumer enters the debtor life cycle, they often avoid talking with you about the debt because they do not have the ability to pay. When the debtor begins to recover financially, you want to be sure you are among the first to reach out to them so you can be the first to be paid. According to Don Taylor, President of Automated Collection Services, they have seen a lift of more than 12% of consumers with trigger hits entering repayment, and this on an aged portfolio that has already been actively worked by debt collection staff. Monitoring for a few key changes on the credit profiles of debtors provides the passive monitoring that is needed to tell you the optimal time to reach back to the consumer for payment. Experian compiled several recent collection studies and found that a debtor paying off an account that was previously past due provided a 710% increase in the average payment. Positive improvement on a consumers’ credit profile is one of those vital indicators that the consumer is beginning to recover financially and could have the will—and ability—to pay bad debts. The collection industry is not like the big warehouse stores—quantity and value do not always work hand in hand for the debt collection industry. Targeting the high value credit events that are proven to increase collection amounts is the key to value, and Experian has the expertise, analytics and data to help you collect in the most effective manner. Be sure to check out our other debt collection blog posts to learn how to recover debt more quickly and efficiently.

By: Joel Pruis What is it we as bankers are trying to accomplish? If you have been in the industry for 20+ years, this question may sound ridiculous! We do what we do! We are bankers! What do you mean define what are we trying to do? But that is the question, what is it we are trying to do? I am going to propose we boil it down to the basic/fundamental element – Banks aggregate money from various sources and redeploy these funds to earn a return for the shareholders. Ultimately, our objective is to generate an appropriate return for the shareholders Getting back to the movie Moneyball, Billy Beane and Peter Brand define the objective of the Oakland A’s for the season in terms of projecting the number of wins that are needed to assure, with all probability, that the team makes the playoffs (this would be similar to the objective of banking to generate an appropriate return for the shareholders). But Peter Brand quickly moves into very specific targets that are required for the A’s to make it to the playoffs, namely win 99 regular season games. In order to win 99 regular season games, the A’s offense will need to score 814 runs in the season and defensively only allow 645 runs. Plain and simple. Very objective, very measurable and it is all based upon data, data, data. Let’s break this down. Based upon their conference, the teams in their conference along with the overall schedule, Peter Brand projects that 99 wins are necessary to land a spot in the playoffs. No gut check, no darts or crystal ball but rather historical data that when analyzed provides the benchmark of 99 wins to statistically assure the Oakland A’s that they will make the playoffs. So let’s apply this to banking. Our objective is to generate the appropriate return for our shareholders or the old Return on Equity. So, for example, if our targeted return on equity is 20% (making the playoffs) we need to make sure we generate enough net income (99 wins) through producing the necessary gross yield on assets (814 runs generated by the Oakland A’s offense) less the expected charge offs (645 runs allowed by the Oakland A’s defense). For a quick dive into details, our data would provide for a margin of error on the variable to provide for statistical assurance of achieving the objective (Return on Equity). In the movie there is no guaranty that the 814 runs will win the conference but at the same time there is no guaranty that the Oakland A’s opponents will score 645 runs. Never in the movie does the coach, Billy Beane or Peter Brand tell the team, “You only have to score X number of runs this game, don’t score anymore.” Or even crazier, “You are not letting the other team score enough runs, they need to score 645!” No, the strategy is still to generate as many runs as possible while minimizing the number of runs scored by the opposition. Rather it is the review of the total amount of earning assets of the financial institution and the overall credit quality that we must understand and control to determine our ability to generate the net yield on assets required to generate the return on equity that is required. If we assume too much risk in the portfolio in order to generate the required yield it would be similar to having a poor pitching staff projected to allow 10 runs a game requiring the team to produce 11 runs a game in order to win. It just is not realistic. So basically we need to assess at the high level, are we appropriately structured to allow for the generation of enough profit to provide the appropriate return on equity. At this point, we do not need to complicate it any further than that. Now let’s take a look at the constraints. We know we have them in banking, let’s take a look at probably the single biggest constraint imposed on Billy Beane and the Oakland A’s. In the movie, before Billy Beane is even aware of the Moneyball concept, his is given his constraint by the owner. Beane asks for more money to ‘buy players’ and is flat out rejected by the owner. The owner, in fact, cuts Beane off by asking, “is there anything else I can do for you?”. Net result is that the Oakland A’s have $38 million dollars for payroll vs. the New York Yankees at $120 million. Seriously it does not seem fair. How can you attract the needed talent when you cannot pay the type of salary needed to get the necessary players to win a championship? Let’s rephrases this for banking… How can a bank be expected to deploy its assets when such a high rate of return is required? Boiling it down to a specific example, “How can I originate a commercial loan at this rate of interest when the competition is ½ to 1% lower than our rates?” Up next – Why will 99 games get us to the playoffs? How do we assess the environment?

A recent study comparing financial differences between men and women found that, overall, women are better at managing money and debt. Differences between the two populations include:

By: Joel Pruis Times are definitely different in the banking world today. Regulations, competition from other areas, specialized lenders, different lending methods resulting in the competitive landscape we have today. One area that is significantly different today, and for the better, is the availability of data. Data from our core accounting systems, data from our loan origination systems, data from the credit bureaus for consumer and for business. You name it, there is likely a data source that at least touches on the area if not provides full coverage. But what are we doing with all this data? How are we using it to improve our business model in the banking environment? Does it even factor into the equation when we are making tactical or strategic decisions affecting our business? Unfortunately, I see too often where business decisions are being made based upon anecdotal evidence and not considering the actual data. Let’s take, for example, Major League Baseball. How much statistics have been gathered on baseball? I remember as a boy keeping the stats while attending a Detroit Tigers game, writing down the line up, what happened when each player was up to bat, strikes, balls, hits, outs, etc. A lot of stats but were they the right stats? How did these stats correlate to whether the team won or lost, does the performance in one game translate into predictable performance of an entire season for a player or a team? Obviously one game does not determine an entire season but how often do we reference a single event as the basis for a strategic decision? How often do we make decisions based upon traditional methods without questioning why? Do we even reference traditional stats when making strategic decisions? Or do we make decisions based upon other factors as the scouts of the Oakland A’s were doing in the movie Moneyball? In one scene of the Movie, Billy Beane, general manager of the A’s, is asking his team of scouts to define the problem they are trying to solve. The responses are all very subjective in nature and only correlate to how to replace “talented” players that were lost due to contract negotiations, etc. Nowhere in this scene do any of the scouts provide any true stats for who they want to pursue to replace the players they just lost. Everything that the scouts are talking about relates to singular assessments of traits that have not been demonstrated to correlate to a team making the playoffs let alone win a single game. The scouts with all of their experience focus on the player’s swing, ability to throw, running speed, etc. At one point the scouts even talk about the appearance of the player’s girlfriends! But what if we changed how we looked at the sport of baseball? What if we modified the stats used to compile a team; determine how much to pay for an individual player? The movie Moneyball highlights this assessment of the conventional stats and their impact or correlation to a team actually winning games and more importantly the overall regular season. Bill James is given the credit in the movie for developing the methodology ultimately used by the Oakland A’s in the movie. This methodology is also referred to as Sabermetrics. In another scene, Peter Brand, explains how baseball is stuck in the old style of thinking. The traditional perspective is to buy ‘players’. In viewing baseball as buying players, the traditional baseball industry has created a model/profile of what is a successful or valuable player. Buy the right talent and then hopefully the team will win. Instead, Brand changes the buy from players to buying wins. Buying wins which require buying runs, in other words, buy enough average runs per game and you should outscore your opponent and win enough games to win your conference. But why does that mean we would have to change the way that we look at the individual players? Doesn’t a high batting average have some correlation to the number of runs scored? Don’t RBI’s (runs batted in) have some level of correlation to runs? I’m sure there is some correlation but as you start to look at the entire team or development of the line up for any give game, do these stats/metrics have the best correlation to lead to greater predictability of a win or more specifically the predictability of a winning season? Similarly, regardless of how we as bankers have made strategic decisions in the past, it is clear that we have to first figure out what it is exactly we are trying to solve, what we are trying to accomplish. We have the buzz words, the traditional responses, the non-specific high level descriptions that ultimately leave us with no specific direction. Ultimately it allows us to just continue the business as usual approach and hope for the best. In the next few upcoming blogs, we will continue to use the movie Moneyball as the back drop for how we need to stir things up, identify exactly what it is we are trying to solve and figure out how to best approach the solution.

By: Matt Sifferlen Ah, fraudulent behavior is currently enjoying a bright shiny moment in the sun in today's pop culture, particularly in the world of sports. Whether it's a college athlete being duped for months by telephone conversations with a non-existent girlfriend, or the world's best known cyclist coming clean on a lifetime of deceit, in both cases we're left shaking our heads and laughing, crying, or cringing while telling ourselves "I'm glad I'm too smart to fall for any of this." But are you just kidding yourself? In the case of the college football player, most of us have been scratching our heads wondering how any adult could possibly get strung along for such an extended period of time by such a scam. But if you take a closer look at the interaction between the athlete and the fraudster, you'll see that the fraudster deployed some typical tactics that allowed him to keep the scam living and breathing. In particular, he continuously kept communicating with the athlete via phone and social media, reinforcing the perception that he's aboveboard and genuinely interested in the athlete's life. We see this in commercial fraud interactions too, where the commercial fraudster will perform expected, normal tasks and activities (e.g. making small payments on loans, placing phone calls to lender support staff) that will reinforce the lender's perception that the fraudster is just another normal client. But unlike the athlete's scenario where the fraudster's story unraveled due to no logical conclusion being planned, commercial fraudsters will string lenders along until they get what they want -- then they vanish. Lenders can't get too complacent in their fraud prevention efforts, assuming that the mere presence of normal account activity equates to a validation of a client's authenticity. To complicate things, while electronic communication methods like text messages, emails, and Twitter or Facebook messages offer many convenience advantages, they are ripe for manipulation by fraudsters who certainly find these methods preferable to any awkward face to face encounters with someone they're victimizing. The cyclist that admitted to a lifetime of lies also shines the light on some other tactics that commercial fraudsters might use -- using perceived image and reputation to deceive. Fraudsters will often steal identities of licensed professionals (think physicians, dentists) with favorable credit profiles and use their information to apply for commercial credit or services, knowing that they will likely be viewed favorably due to their impressive profiles, at least on paper. In today's world where lightly staffed underwriting teams struggle to keep up with their workloads, it's easy to see why this tactic can help increase the odds that an application might escape closer scrutiny. After all, it's a doctor's office so what could possibly go wrong? A lot, if you're approving someone who really isn't the doctor! An objective evaluation and screening process where underwriting and analyst staff consistently verify all applicant data and not just cherry pick the ones that look suspicious on paper can go a long way towards avoiding this typical trap set by commercial fraudsters. And in the final scenario of art imitating life, there is the recent release of a major motion picture comedy about identify theft. I'm sure anyone who has been a victim of identity theft won't find hilarity in the scenes of the victim's life getting turned upside down, suddenly unable to use his credit cards at the gas station and being asked about transactions that took place somewhere else in the country that he's never visited. But undoubtedly many folks will find this humor hilarious because we probably know of some horror story that a friend or acquaintance has shared with us that is similar to one of the wacky scenarios covered in this movie. So we'll laugh and take comfort in the fact that we're too smart to get scammed like this, but if the FTC is stating that identity theft will affect 1 in 6 people each year then we're fooling ourselves in thinking that our number won't be up at some point soon. So what can be learned from these high profile pop culture events? I think a couple things. First, know your customers (or athletes, heroes, girlfriends). It sounds simple, but make sure they are who they say they are. Whether you're lending to a business or a consumer, there are tools out there that can enable you to objectively screen your applicants and minimize any bias that might get exploited by fraudsters in a manual review heavy process. If you're not cautious and get burnt, you might not have to go on Oprah or Dr. Phil to explain to your management team where things went horribly wrong, but the level of financial and reputational damage inflicted could be a painful lesson for you and your institution. Or if you're really (un)lucky, maybe they'll make a movie about your story -- wouldn't that be hilarious? (sarcasm intended)

The purpose of any type of insurance is to protect your most valuable assets. To combat the prevalence of cyber attacks and data breaches, an increasing number of businesses in the health-care, financial services and technology industries have purchased cyber insurance policies to protect themselves from the crippling cost of a data breach. This is especially popular among start-up tech companies in Silicon Valley in order to safeguard their intellectual property (IP) since their IP is the backbone of their livelihood1. Since small businesses generally don’t have a risk manager and IT department dedicated to data security, a good cyber insurance policy can help mitigate cyber security risks. Although accepted in some sectors, cyber insurance is still not an established part of many companies’ IT data security strategies. This is commonly due to a lack of agreed risk management standards and the challenge of substantiating and quantifying losses, in addition to finding objective data to back up cyber insurance claims. Some security experts feel that the federal government needs to kick start growth in this market by requiring government contractors to purchase cyber insurance to set a standard for other businesses, sending a message that any company who has cyber security insurance is a signal that the company is competently managing its data security. As the cyber insurance industry evolves, here is a list of what the policies generally cover and what to look for: First-party claims – Costs incurred by the loss of trade secrets and intellectual property. Third-party claims – Damages a business must pay to customers who sue them for lost or compromised personal information. Business interruption coverage – In the event a data breach incident prevents the company from operating or functioning, the company would receive payment reimbursement for expenses incurred due to loss of business. A forensic IT investigation – Policies can cover the cost of an examination into how the data breach occurred and some may even cover the costs of regulatory fines and penalties in addition to the crisis management control which includes data breach notification letters. Security professionals stress that cyber insurance is not meant to be a substitute for data protection and security policies. In fact, before underwriting a policy, an insurance company will be hyper vigilant in determining that their customers have proper protections and policies in place since the insurance company will want to reduce its own risk. And since insurance has been a positive influence on other industries to improve performance and safety due to risk mitigation, the theory is if a company has cyber insurance, the hope is they will implement proper preventative measures to ensure that they will never have to use it. Learn more about our Data Breach solutions 1http://www3.cfo.com/article/2013/4/data-security_cyber-attacks-cybersecurity-liability-insurance-smb-growth-companies-risk-hogan-lovells

Financial institutions are revisiting their policies and thresholds for lending to small businesses and are slowly loosening restrictions. In a recent survey by the Federal Reserve Board, 9.2 percent of senior loan officers said they have "somewhat" eased their standards for lending to small firms and provided commercial borrowers more leeway, in the form of slightly bigger credit lines and longer maturity terms.

By: Maria Moynihan Cybersecurity, identity management and fraud are common and prevalent challenges across both the public sector and private sector. Industries as diverse as credit card issuers, retail banking, telecom service providers and eCommerce merchants are faced with fraud threats ranging from first party fraud, commercial fraud to identity theft. If you think that the problem isn't as bad as it seems, the statistics speak for themselves: Fraud accounts for 19% of the $600 billion to $800 billion in waste in the U.S. healthcare system annually Medical identity theft makes up about 3% of 8.3 million overall victims of identity theft In 2011, there were 431 million adult victims of cybercrime in 24 countries In fiscal year 2012, the IRS’ specialized identity theft unit saw a 78% spike from last year in the number of ID theft cases submitted The public sector can easily apply the same best practices found in the private sector for ID verification, fraud detection and risk mitigation. Here are four sure fire ways to get ahead of the problem: Implement a risk-based authentication process in citizen enrollment and account management programs Include the right depth and breadth of data through public and private sources to best identity proof businesses or citizens Offer real-time identity verification while ensuring security and privacy of information Provide a Knowledge Based Authentication (KBA) software solution that asks applicants approved random questions based on “out-of-wallet” data What fraud protection tactics has your organization implemented? See what industry experts suggest as best practices for fraud protection and stay tuned as I share more on this topic in future posts. You can view past Public Sector blog posts here.

A recent survey that polled Americans on credit scores found that while nearly half of respondents (49 percent) check their credit scores at least once per year, the rest check once every two years or less, including a worrisome 22 percent who never check. The most common reasons for checking a credit score include purchasing a home (31 percent) or an automobile (32 percent).

VantageScore Solutions’ analysts recently examined how many accounts consumers with prime credit scores typically have in their credit file. Consumers who generally qualify for loans have an average of 13 loans in their credit files, and typically the oldest loan is more than 15 years old.

By: Maria Moynihan Reduced budgets, quickly evolving technologies, a weakened economy and resource constraints are clearly impacting the Public Sector, but it’s not all doom and gloom. Always with new challenges, come new opportunities. Government agencies must still effectively run programs, optimize processes and find growth in revenue streams. Below you will find the top 5 business challenges facing the Public Sector and municipal utilities today and ways to overcome them: 1. Difficulty finding debtors When asked to name the top challenge to their debt collection processes, governments most often indicate the difficulty in locating debtors whose whereabouts don’t in fact match information they have on hand. Skip tracing with right party contact data is key to finding people or businesses for collections and there are several cost effective ways to do this - either through industry leading tools or by tapping into available sources like voter registration information. 2. Difficulty in prioritizing debt collection efforts When resources are limited, it is critical to not only focus efforts by size, but by likelihood to make contact and access debtors with an ability to pay. Credit and demographic data elements like income, assets, past payment behavior, and age can all be brought together to better identify areas of greater ROI over others. 3. Lack of data available By simply incorporating third-party data and analytics into an established infrastructure, agencies can immediately gain improved insight for efficient decision making. Leverage on-hand data sources to improve understandings of individuals or businesses. 4. Difficulty of incorporating tools to improve debt recovery Governments too often attempt to reduce backlogs by simply trying to accelerate processes that are suboptimal to start with. This is both expensive and unlikely to produce the desired result. In the case of debt collection, success is driven by the tools and processes that allow for refined monitoring, segmentation and prioritization of accounts for improved decisioning. 5. Difficulty in determining to outsource or continue to internally collect While outsourcing to debt collection agencies is always an option, it may not be the most resourceful one, or in some cases, even necessary. Cost to value considerations per effort need to be made by agencies and often, the most effective strategy is to perform minimal efforts internally and to outsource older or skip accounts to third party agencies. What is your agency’s biggest business challenge? See what industry experts suggest as best practices for Public Sector collections or download Experian’s guide to Maximizing Revenue Potential in the Public Sector to learn more.

While VantageScore® credit score super-prime consumers carried the lowest average credit card balance of all credit tiers in Q4 2012 ($2,581), this group experienced the greatest average balance increase (6 percent) when compared with the previous quarter. All other credit tiers had little or no change to their average credit card balance.

As we prepare to attend next week’s FS-ISAC & BITS Summit we know that the financial services industry is abuzz about massive losses from the ever-evolving attack vectors including DDoS, Malware, Data Breaches, Synthetic Identities, etc. Specifically, the recent $200 million (and counting) in losses tied to a sophisticated card fraud scheme involving thousands of fraudulent applications submitted over several years using synthetic identities. While the massive scale and effectiveness of the attack seems to suggest a novel approach or gap in existing fraud prevention controls, the fact of the matter is that many of the perpetrators could have been detected at account opening, long before they had an opportunity to cause financial losses. Synthetic identities have been a headache for financial institutions for years, but only recently have criminal rings begun to exploit this attack vector at such a large scale. The greatest challenge with synthetic identities is that traditional account opening processes focus on identity verification compliance around the USA PATRIOT Act and FACT Act Red Flags guidance, risk management using credit bureau scores, and fraud detection using known fraudulent data points. A synthetic identity ring simply sidesteps those controls by using new false identities created with data that could be legitimate, have no established credit history, or slightly manipulate elements of data from individuals with excellent credit scores. The goal is to avoid detection by “blending in” with the thousands of credit card, bank account, and loan applications submitted each day where individuals do not have a credit history, where minor typos cause identity verification false positives, or where addresses and other personal data does not align with credit reports. Small business accounts are an even easier target, as third-party data sources to verify their authenticity are sparse even though the financial stakes are higher with large lines of credit, multiple signors, and complex (sometimes international) transactions. Detecting these tactics is nearly impossible in a channel where anonymity is king — and many rings have become experts on gaming the system, especially as institutions continue to migrate the bulk of their originations to the online channel and the account opening process becomes increasingly faceless. While the solutions described above play a critical role in meeting compliance and risk management objectives, they unfortunately often fall short when it comes to detecting synthetic identities. Identity verification vendors were quick to point the finger at lapses in financial institutions’ internal and third-party behavioral and transactional monitoring solutions when the recent $200 million attack hit the headlines, but these same providers’ failure to deploy device intelligence alongside traditional controls likely led to the fraudulent accounts being opened in the first place. With synthetic identities, elements of legitimate creditworthy consumers are often paired with other invalid or fictitious applicant data so fraud investigators cannot rely on simply verifying data against a credit report or public data source. In many cases, the device used to submit an application may be the only common element used to link and identify other seemingly unrelated applications. Several financial institutions have already demonstrated success at leveraging device intelligence along with a powerful risk engine and integrated link analysis tools to pinpoint these complex attacks. In fact, one example alone spanned hundreds of applications and represented millions of dollars in fraud saves at a top bank. The recent synthetic ring comprising over 7,000 false identities and 25,000 fraudulent cards may be an extreme example of the potential scope of this problem; however, the attack vector will only continue to grow until device intelligence becomes an integrated component of all online account opening decisions across the industry. Even though most institutions are satisfying Red Flags guidance, organizations failing to institute advanced account opening controls such as complex device intelligence can expect to see more attacks and will likely struggle with higher monetary losses from accounts that never should have been booked.

Outsourcing can be risky business. The Ponemon Institute reports that 65% of companies who outsourced work to a vendor have had a data breach involving consumer data and 64% say it has happened more than once. Their study, Securing Outsourced Consumer Data, sponsored by Experian® Data Breach Resolution also found that the most common cause for breaches were negligence and lost or stolen devices. Despite the gravity of these errors, only 38 percent of businesses asked their vendor to fix the problems that led to the breach and surprisingly, 56% of the companies learned about the data breach accidentally instead of through security protocols and control procedures. These findings come from a survey of 748 people in a supervisory (or higher) job who work in vendor management at companies that share or transfer consumer data mainly for marketing, finance and outsourced IT operations including cloud services and payment processing. The survey also polled the vendors and 57% of them reported that they in turn, outsourced work to a third party. 23% of vendors could not tell how often data loss happened which is a sign that they don’t have proper procedures and policies in place to know when incidents occur. When asked about their data breach notification practices, only 16 percent of vendors said they immediately notified their client after the breach investigation with 25 percent saying they don’t even tell clients about breaches of data. Keeping all work and information in house is not feasible in today’s multi-corporate companies, and outsourcing is a business reality, however, all parties have a responsibility to protect the sensitive and confidential data that is entrusted to them. When outsourcing consumer data to vendors, here are a few guidelines companies need to follow to safeguard the information: 1. Make sure you hold vendors to the same security standards as your own in-house security policies and practices. 2. Make sure the vendor has appropriate security and controls procedures in place to monitor potential threats. 3. Audit the vendor’s security and privacy practices and make sure in your contract with them, the vendor is legally obligated to fix data problems should a breach occur including notifying consumers. 4. Monitor the security and privacy practices of vendors you work with especially if you share consumer data with them. 5. Require background checks for vendor employees who have access to confidential information. The goal of this study was to better understand what companies are doing to protect consumer data they outsource and where improvements could be made to insure privacy and security when sharing private information with third parties. The solution seems to be that all parties must first agree that data privacy and protection is paramount and then work toward the mutual goal of achieving responsible privacy and security practices. Download the Securing Outsourced Consumer Data report