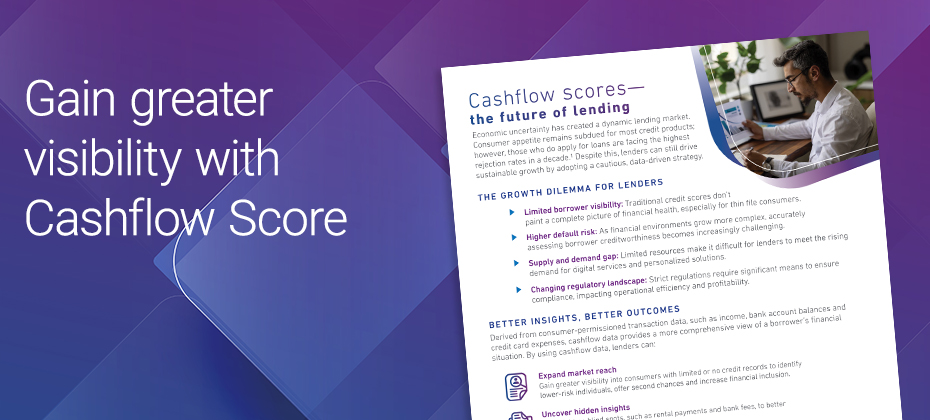

Consumers are experiencing the highest loan rejection rates in a decade, driven by strict lending standards.1 While crucial for mitigating risk, these measures can also limit growth opportunities for financial institutions.

Our latest one pager explores how cash flow data, obtained from consumer-permissioned transaction data, empowers lenders with unique insights into consumers’ financial health, enabling them to expand their portfolios while managing risk effectively.

Read the full one pager to learn how cashflow data can help you make smarter, more confident lending decisions.

12024 Q4 Lending Conditions Chartbook, Experian.