All posts by Guest Contributor

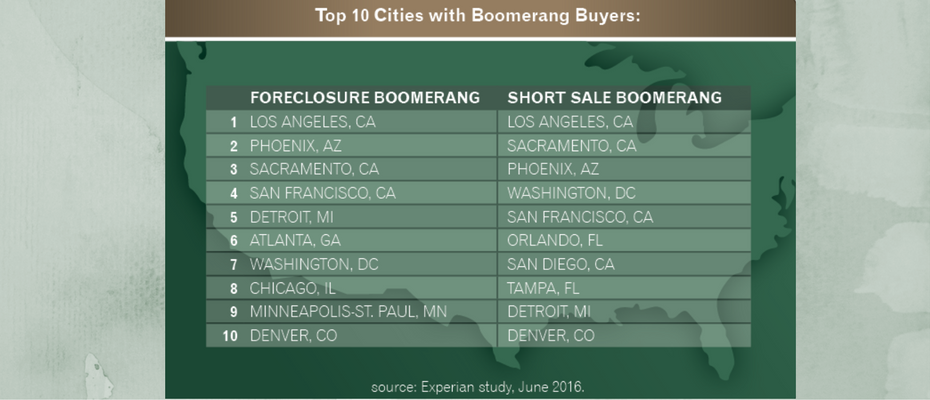

A recent Experian analysis shows that about 2.5 million consumers will have a foreclosure, short sale or bankruptcy fall off their credit report between June 2016 and June 2017 — with 68% of these consumers scoring in the near-prime or high credit segments. Additional highlights include: Nearly 29% of those who short-sold between 2007 and 2010 have opened a new mortgage. Delinquencies for this group are below the national average for bankcard and auto loan payments. More than 12% of those who foreclosed now have boomeranged (opened new mortgages). With millions of borrowers potentially re-entering the housing market, the trends are promising for both the mortgage seeker and the lender. Want to know more?

Late last year, our Third Annual Data Breach Industry Forecast predicted cybercriminals would continue to focus their attacks on healthcare institutions, inspired by the knowledge that the black market value of medical records continues to surpass the value of credit card numbers. Industry experts we interviewed also predicted employee missteps would be a source of healthcare breaches. Entering the final quarter of 2016, our prediction is playing out in the numbers; nearly half of all consumers affected by a data breach so far this year had their personal information exposed through a healthcare-related incident, according to information compiled by the Identity Theft Resource Center. In the first three quarters of the year, 256 medical and healthcare data breaches exposed more than 13.5 million records, the highest number of any sector the ITRC tracks. Records compromised in a healthcare breach accounted for 47.2 percent of all affected records in 2016. The healthcare sector has been a hotbed of attacks throughout the year, largely due to the continued value of medical records sold on the dark web. These records can be used for far more than just filing fraudulent medical claims. One lucrative use is filing fraudulent tax returns. CNBC reported the IRS expects, and has been bracing for, an increase in tax fraud linked to the high number of medical breaches this year. It’s easy to understand why medical records can be so profitable for hackers. While financial accounts such as credit cards may contain a limited amount of personal information, medical records are much more comprehensive. Typically, they contain a wealth of information far beyond mere account numbers. In addition to names, addresses and birth dates, medical records often contain Social Security numbers, which healthcare providers may use as patient identifiers. The employee factor Many of the mega-breaches of 2015 occurred through digital routes that the average consumer would find downright arcane. In 2016, we’ve seen an increase in smaller attacks with mundane origins such as stolen hardware, poorly secured employee email accounts or phishing attacks. Consider these examples reported in the HIPAA Journal: Four staff email accounts were compromised in a phishing attack on employees at City of Hope Hospital in California. To put it more bluntly, four hospital employees fell for scam emails and the result was, as ITRC reports, the exposure of more than 1,000 patient records. More than 200,000 patients of Premier Healthcare in Bloomington, Indiana, received notification letters after a password-protected but unencrypted laptop was stolen from the hospital’s billing department. A St. Louis, Missouri, not-for-profit healthcare system, BJC Healthcare, had to notify more than 2,300 patients their information was exposed after an employee mistakenly sent an email containing protected information to another medical organization. For healthcare institutions, the takeaway from 2016 should be the need to remain vigilant and proactive regarding the many ways in which data breaches can occur. While 2015 was the year of healthcare mega-breaches, 2016 has seen the emergence of smaller breaches that still have the potential to cause significant harm to organizations and patients. Learn more about our Data Breach solutions

$1.3 trillion. 41.1 million Americans. $31,590. These are the growing numbers associated with student loan debt in the United States: $1.3 trillion in outstanding student loans, spread across 41.1 million people, who are leaving college with an average balance of $31,590. The numbers are staggering, and for the first time student loan debt is playing a prominent role in a presidential election. For all of their differences, presidential nominees Hillary Clinton and Donald Trump seem to agree on one thing: student loan debt is a crushing burden. Both candidates have proposed solutions for student lending. Clinton’s “New College Compact” would allow borrowers to refinance their student loans at current rates available to students taking out new loans. She also wants to reduce interest rates on new student loans, and make it easier for borrowers to enroll in income-driven repayment programs that would cap monthly payments at 10 percent of discretionary income. Trump proposes giving more oversight to colleges to decide whether to grant loans to students based on their prospective major. The plan would also give private banks oversight over government-backed student loans—reversing a 2010 decision under President Obama to make the federal government the lender. Neither candidate, however, has outlined a solution for taming growing tuition costs. Tuition expenses are up 1,225 percent over the past 36 years, outpacing medical costs (634 percent rise) and the consumer price index (279 percent) over the same period, according to the Bureau of Labor Statistics. So it’s not surprising an Experian study shows the student loan rate has grown five percent in the past three years. What is surprising is the number of people and the average age of those people holding student loans. Experian found: 20 percent of people with a credit file hold a student loan that is being repaid or deferred. The average age of a consumer with a student loan is 37, with an average income of $47,200 compared to 53.8 and an average income is $44,500 for consumers without a student loan. The average age of a consumer with at least one deferred student loan is 32.7 with an average income of $32,900 compared to 38.7 and an average income of $53,200 for consumers with at least one non-deferred student loan. Candidate proposals aside, one thing is certain: student loan debt has a very real impact on the daily lives of people, many of whom have delayed buying homes, starting families, and saving for retirement. Until policymakers find a way to address bloated tuitions and student debt, it will take many longer to realize their dreams.

Call if you need to, but protect yourself from TCPA exposure first. Follow these steps when creating your dialing strategy: Obtain customer consent Determine if the number is attached to a landline or a wireless device Verify ownership Scrub your database Calling cell numbers can be a risky business, so be sure to set the proper workflow in motion to remain compliant. >>Learn more

Businesses believe that 23% of their customer or prospect data is inaccurate. Since 84% of companies have a loyalty or customer engagement program in place, poor data is a costly issue. The unfortunate reality is that 74% of companies have encountered problems with these programs — and 12% of revenue is believed to be wasted as a result. Is your loyalty program suffering from poor data? There is a cure. Think of data quality as preventative medicine for a costly and entirely avoidable illness. >>Learn more

Since 1948, International Credit Union Day – a time to recognize the credit union movement – has been celebrated the third Thursday of October. The day is the perfect time to remind your members and consumers about all of the services and benefits your credit union offers. This year’s theme, “The Authentic Difference,” celebrates what makes credit unions stand out. Here are 10 reasons CUs deserve a spotlight: Credit unions are non-profit cooperatives, owned and operated by its members. That means they emphasize consumer value to more than 217 million members worldwide. Profits go back to members in the form of reduced fees, higher savings rates and lower loan rates. Personal relationships are key. Credit unions pride themselves on developing relationships with their members, and CUs are typically staffed by friendly reps who know customers by name. Checking accounts are free. Roughly 80 percent of credit unions offer free checking accounts, compared to less than 50 percent of banks, according to economic research firm Moebs Services. Few ATM fees. Many credit union customers are able to avoid ATM fees because CUs typically give them access to a large network of ATMs by sharing branches and other resources. Savings rates are above average. Because credit unions don't have to pay dividends to shareholders and are exempt from federal taxes they can offer high rates on saving accounts. The average credit union offers CD, money market, and savings rates well above the national banking rates average. Lower interest rates. Credit unions offer lower interest rates on some loans. The difference between banks and credit unions was greatest in car-loan interest rates, according to a September report by SNL Financial. The average 36-month used-car loan interest rate offered by CUs was 2.67 percent compared to 4.45 percent for banks. For new-car loans, CUs offered an average interest rate for 48 months of 2.60 percent compared to 3.94 percent for banks. Invested in the community. A credit union’s core values are focused on its members and the communities where they live and work. Many provide financial education and outreach to consumers. It’s easier to get credit. CUs don’t have to abide by loan restrictions and qualifications mandated by a corporate office, so they have more flexibility to make loans when possible. Small-business support: CUs may know borrowers and are able to take into account intangibles like community reputation and accountability. Also, they understand the value to the community of a small business, its market and credit needs. Joining is easy. Many credit unions base eligibility simply on where you live, instead of restricting membership to a particular employer. Since expanding eligibility, credit union membership has grown by about two percent a year for the past decade.

When financial planners and tax advisors meet with clients to review their portfolios, chances are they don't go over their credit reports often. Maybe they never do. Kiplinger’s estimates less than half of professional financial advisors take the time to review credit reports with clients. But taking this step is critical to understanding a person’s complete financial situation and creating a realistic plan. Prepare for Future Opportunities Clients may have all the credit they need at the moment, but if their credit score is mediocre or low, they might end up paying for it in the future. Just when they want to refinance a loan, buy more insurance, apply for a dream job or buy a business, they may discover their credit score is an obstacle. Check for Errors Credit bureaus collect billions of data points from millions of businesses each year, and it’s important to check a credit report for accuracy. If there are errors in a client’s file, he or she may be unfairly penalized. Keep in mind that nearly every company checks credit reports to determine who to do business with. Potential employers, business partners and insurance companies give credit files a look before deciding whether or not to make an offer to a person. Awareness Mistakes aren't the only factor leading to a low credit score. Too many hard inquiries, a maxed-out credit card or a number of small loans that could be paid off all cost credit points. Reviewing a credit report is a great way to help clients see the real impact their habits have on their financial life, and they could realize a significant rise in their credit score with little effort. Stand Out in the Crowd Even if a person has an exceptional credit report, a financial or tax advisor will gain credibility by reviewing their information with them. Doing so demonstrates out-of-the-box thinking and concern for a person’s financial health. Let's see a robo-advisor do this. Financial professionals can easily and securely review their clients’ credit reports online. Ready to understand your client’s complete financial situation? Try out our online solution at no cost to you. Interested in integrating with your existing financial or tax planning software? Learn more about integration options with Experian’s API.

Millennials are coming of age and experiencing big life moments — college graduation, their first job, getting married and moving out. But what about buying ahome? Here are some things we know: Millennials are 75 million strong 75% say homeownership is a long-term goal Millennials are now the largest living generation. Are you equipped with the right strategies and tools to serve their lending needs? >>Webinar: Are Millenials Mortgage-Ready?

As we approach the one-year anniversary of the EMV liability shift, we have seen an increase in e-commerce fraud — to the tune of 15% higher than last year. Additional insights from Experian’s biannual analysis on e-commerce fraud include: 44% of e-commerce billing fraud came from Florida, California and New York* 52% of e-commerce shipping fraud came from Florida, New York and California* Miami, Fla., is the most dangerous city in the United States for e-commerce merchants* As fraudsters continue to perpetrate card-not-present fraud, ensure you are prepared. You’ll be thankful if fraudsters come calling. >> E-commerce Attack Rates

In this new Telephone Consumer Protection Act (TCPA) era, calling your customers isn’t a thing of the past. It’s still okay to reach out to your clients by phone, whether to offer a new product or collect on an overdue bill. But strict compliance with TCPA rules is critical for any business that contacts customers by phone. Some of the very best ways you can protect yourself from TCPA exposure is to follow four steps when creating your dialing strategy: Customer consent: It’s important to maintain and update your customers’ contact preferences and consent to call them. Simply having a phone number on an application isn’t sufficient. Companies are required to have written permission, such as “I consent to calling my cell phone when there’s a problem …” Remember, permission may only be granted by the party who subscribes to the cellular service or who regularly uses that cell phone number. Landline or wireless?: Your database should also include the phone type for the telephone numbers you have for your customers. The dialing rules differ depending on the phone type, so it’s critical to know the type of phone you are calling or texting. Verify ownership: Ownership of cell phones should especially be validated to ensure the number hasn’t been reassigned and that the person who gave consent still owns the phone. One call can be made to a reassigned number with no liability, assuming you have no knowledge the number has changed. Repeating the action could lead to fines from $500 to $1,500 per infraction. Scrub Your Database: Have practices in place to remove any confirmed reassigned phone numbers from your database. This will help to improve your right-party contact rate and save you from potential TCPA headaches. No one disagrees that calling cell numbers is a risky business, but it can be done if you set the proper workflow in motion. Click here to learn more about Experian solutions that will help to reduce your TCPA compliance risk.

Leasing continued its strong growth as the share of new vehicles leased jumped from 26.9% in Q2 2015 to a record high of 31.4% in Q2 2016. As vehicle prices continue to rise, used vehicle loans also set new records. The average used vehicle loan reached an all-time high of $19,101 in Q2 2016, up from $18,671 in Q2 2015. Used vehicle loans accounted for 55.6% of all vehicle loans in Q2 2016. Want to capitalize on this growth? Analytics can help you target borrowers who are creditworthy and in the market for an auto loan or lease. >>Video: Auto Acquisition Strategies

Experian analyzed millions of e-commerce transactions from the first six months of 2016 to identify the latest fraud attack rates across the United States for both shipping and billing locations. As we approach the one-year anniversary of the EMV liability shift, the 2016 e-commerce fraud attack rates look to be at least 15 percent higher than last year’s total. Experian analyzed millions of e-commerce transactions from the first six months of 2016 to identify the latest fraud attack rates across the United States for both shipping and billing locations. Billing fraud rates are associated with the address of the purchaser. Shipping fraud rates are associated with the address where purchased goods are sent. As we approach the one-year anniversary of the EMV liability shift, the 2016 e-commerce fraud attack rates look to be at least 15 percent higher than last year’s total. E-commerce fraud is often an indicator that other fraud activities have already happened, whether a credit card has been stolen, identity fraud has occurred, or personal credentials have been compromised.

Historically, the introduction of EMV chip technology has resulted in a significant drop in card-present fraud, but a spike in card-not-present (CNP) fraud. CNP fraud accounts for 60% to 70% of all card fraud in many countries and is increasing. Merchants and card issuers in the United States likely will see a rise in CNP fraud as EMV migration occurs — although it may be more gradual as issuers and merchants upgrade to chip-based cards. As fraud continues to evolve, so too should your fraud-prevention strategies. Make a commitment to stay abreast of the latest fraud trends and implement sophisticated, cross-channel fraud-prevention strategies. >>Protecting Growth Ambitions Against Rising Fraud Threats

Unfortunately, identity theft can happen to anyone and has far-reaching consequences for its victims. According to the US Department of Justice (DOJ)’s most recent study, 17.6 million people in the US experience some form of identity theft each year. This includes activities such as fraudulent credit card transactions or personal information being used to open unauthorized accounts. The most obvious consequence that identity theft victims encounter is financial loss, which comes in two forms: direct and indirect. Direct financial loss refers to the amount of money stolen or misused by the identity theft offender. Indirect financial loss includes any outside costs associated with identity theft, like legal fees or overdraft charges. The DOJ’s study found that victims experienced a combined average loss of $1,343. In total, identity theft victims lost a whopping $15.4 billion in 2014. Beyond money lost, identity theft can negatively impact credit scores. While credit card companies detect a majority of credit card fraud cases, the rest can go undetected for extended periods of time. A criminal’s delinquent payments, cash loans, or even foreclosures slowly manifest into weakened credit scores. Victims often only discover the problem when they are denied for a loan or credit card application. Last year, Experian found that these types of fraud take the longest time to resolve. Identity theft doesn’t just impact victims financially; it also often takes a significant emotional toll. A survey from the Identity Theft Research Center found that 69 percent felt fear for their personal financial security, and 65 percent felt rage or anger. And, almost 40 percent reported some sleep disruption. These feelings increased over time when victims were unable to settle the issue on their own, according to the report, which can result in problem as work or school, and add stress to relationships with friends and family. Thankfully, consumers are getting smarter about the best ways to protect their information, like using monitoring services or following security best practices. How are you protecting yourself against identity theft? Learn more about our Identity Protection Services

This summer, the Consumer Financial Protection Bureau (CFPB) took a significant step toward reforming the regulatory framework for the debt collection industry. The focus is fueled in part by the large number of consumer complaints the CFPB receives about the debt collection market — roughly 35% of total complaints. Here are highlights from the recent CFPB proposal: Data quality: Collectors would be required to substantiate claims that a consumer owes a debt in order to begin collection Communication frequency: Collectors would be limited to six emails, phone calls or mailings per week, including unanswered calls and voice mails Waiting period: Reporting a person’s debt would be prohibited unless the collector has communicated directly with the consumer first The CFPB said its proposal will affect only third-party debt collectors; however, it may consider a separate set of proposals for first-party collectors. >> Insights into CFPB's latest debt collection proposal