Tag: State of Credit analysis

Consumers continue to manage credit well and the average credit score climbed seven points since 2020 to 695, the highest point in more than 13 years.

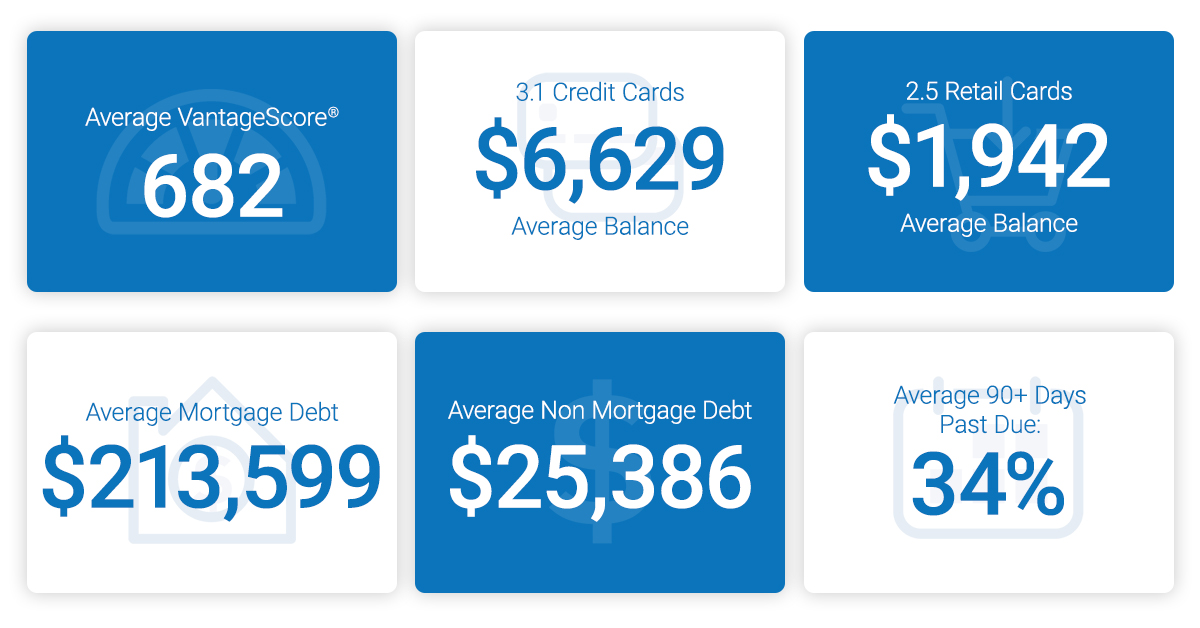

Experian released the 11th annual state of credit report, which provides a comprehensive look at the credit performance of consumers across America.

As look forward to the next decade, things are looking up. The 10th annual State of Credit Report highlights consumer credit scores and borrowing behavior.

Experian's annual State of Credit Report includes consumer credit data trends and a 10 year look back to when America started to enter the recession.

In 2017, a meaningful jump in consumer sentiment bolstered spending, and caused the spread between disposable personal income and consumer spending to reach an all-time high. This increase in spread was mostly financed through consumer debt, which according to the Federal Reserve Bank of New York has brought total consumer debt to a new peak of $12.8 Trillion surpassing the prior peak in 2008. The Experian eighth annual State of Credit report greatly supported the consumer behavior trends observed for the past year. Spanning the generations It is no surprise that generation Z (the “Great Recession Generation”) is conservative and prudent in their approach to credit because they are the most familiar with the post financial crisis economy. Results showed Millennials experienced a drop in overall debt, and an increase in mortgage debt reflects the national homeownership affordability challenge facing this generation. As first time homebuyers, millennials have to relatively tighten their spending as they dedicate an ever-growing portion of their income to housing. On the other end of the spectrum, the results of the study showed that Baby Boomers’ had sizable debt (including mortgage debt), which reflects the generation’s intent to stay active in their communities and in their homes much longer than prior generations have done. A recent Harvard study reported that by 2035, one out of three American households will be headed by an individual 65 years of age or older, compared to current ratio of one out of five households. What’s on the horizon? It is reasonable to assume that these trends may continue into 2018, as the underlying conditions continue to persist. A closer eye should be kept on student and auto loans due to the significant increase in portfolio size and increasing default rates compare to other debt. Editor’s note: This post was written by Fadel N. Lawandy, Director of the C. Larry Hoag Center for Real Estate and Finance and the Janes Financial Center at the George L. Argyros School of Business and Economics, Chapman University. Fadel joined the George L. Argyors School of Business and Economics, Chapman University after retiring as a Portfolio Manager from Morgan Stanly Smith Barney in 2009. He has two decades of experience in the financial industry with banking, credit management, commercial/residential real estate acquisition and financing, corporate finance, mergers and acquisitions, quantitative and qualitative analysis and research, and portfolio management. Fadel currently serves as the Chairman of the Board and President of CFA Society Orange County, and is an active member of the CFA Institute.

Experian’s 8th annual State of Credit report reveals the nation’s average credit score is up two points year-over-year to 675.

Experian’s latest annual State of Credit analysis provides insight into the differences in credit habits by generation. While the youngest group, Millennials, appear to be novice credit managers, Generation Xers have the highest amount of average debt, are slowest to make payments on time and tied with Millennials for highest percentage of credit utilized. The results of the study reinforce the importance of lenders providing transparent consumer education on credit scores and responsible credit behavior. Snapshot of generational debt differences Baby Boomers (47 to 65) Generation X (30 to 46) Millennials (19 to 29) VantageScore® credit score 700 653 628 Average debt $29,317 $30,039 $23,332 Average balance of bankcards $5,347 $5,343 $2,682 Average revolving utilization 30% 37% 37% Late payments 0.33 0.61 0.58 Download our recent Webinar: It’s a new reality ... and time for a new risk score Source: Experian’s State of Credit infographic