Tag: recession

Written by: Mihail Blagoev As there is talk about the global economy potentially heading into a recession, while some suggest that it has already started, there is an expectation that many of the world's countries will see their economic output decline in the next couple of months or a year. Among the negative trends that can occur during a recession are companies making fewer sales and people losing their jobs. Unfortunately, just like any other economic crisis, fraud is expected to go in the opposite direction as criminals continue finding innovative ways to attack consumers when they’re most vulnerable. There is also a concern that first-party fraud attempts might rise as genuine consumers are pushed over the edge by inflation and economic uncertainty. With that in mind, here are six fraud trends that are likely to happen during a recession: Fraudsters exploiting the vulnerable It is well-documented that fraudsters found numerous ways to exploit the vulnerable during the pandemic. Unfortunately, this is expected to happen again in the coming months. As the cost of living rises, criminals will try to use that in their favor by looking for people who can't pay their utility bills or can't afford the price of gas or even food. Fraudsters will try to exploit that by offering them deals, discounts, refunds, or just about anything that will make people believe they are paying less for something that has increased in value or is out of reach at its normal price. Fraudsters have two main goals behind these tactics – stealing personal information to use in other crimes or gaining immediate financial benefits. Although their tactics are well-known – applying pressure on their victims to make quick decisions or offering them something that sounds like a great deal, but in truth, it isn't – that won't prevent them from trying. These scams show that, unlike in other industries, criminals do not rely on high success rates to achieve their goals. All they need is one or two victims out of every few hundred to fall for their schemes. Loan origination fraud Periods of financial instability often result in an increase in first-party fraud, among others. This could take many forms, and there is a possibility for an increase in fraudulent loan applications by genuine consumers to be among the most popular ones. In this type of fraud, bad actors lie on registration forms or applications to gain access to funds they wouldn't normally receive if they added their real information. That could be done by lying about their income and employment information, usually inflating their salaries, extending the amount of time they worked for a certain company, or simply adding a company they have never worked for. Other popular forgeries include anything from supplying fake phone numbers and addresses to providing fake bank statements and utility bills. Money mules Recessions can result in layoffs or people looking for work not being able to find any. That's another opportunity for fraudsters to exploit the vulnerable by offering them “jobs.” This could be achieved by posting job ads on real employment websites or social media. Once recruited, people are asked to open new bank accounts or use their previously opened accounts to transfer funds to accounts that are in the possession of criminals. In the end, the funds get laundered, while the genuine account holder receives a fee for the service. People of all ages are a possible target, but this is especially true for younger generations who often don't understand the consequences of their activities. Friendly fraud Another type of first-party fraud that could go up as a result of the increased economic pressures could be friendly fraud. In this type of fraud that mostly affects the retail industry, consumers charge back genuine payments made by them in order to end up with both the product purchased and the funds for it back in their possession. They could then keep the product or quickly resell it for less than its original value. Luxury goods and electronics could be especially attractive for this type of fraud. Claiming non-deliveries or transactions not being recognized could be among the top reasons used for charging back the transactions. Investment fraud During times of economic hardship, people are often looking for ways to keep their savings from getting eaten by inflation. Investments in property could be one solution, but as it is not affordable for everyone, people are also looking for other ways to invest their money. While this isn’t exactly a vulnerability, it is something that criminals are looking to exploit greatly. They usually reach out to potential victims through social media while also presenting them with fake websites that mimic those by real investors. The opportunities being offered can range from cryptocurrency to various schemes and products that don’t exist or are worthless. However, after the criminals obtain possession of the funds, they discontinue their contact with the victims. Fake goods While this shouldn't happen to the same extent that was seen in 2020, there is a chance that some goods might disappear from certain markets. There could be a variety of reasons for that, from companies limiting their production or going out of business due to inability to pay their bills or shortage in sales to issues with supply chains due to the high gas and oil prices. Expect fraudsters to be the first to move in if there are shortages and start offering fake products or goods that will never arrive. It is still difficult to measure if or when a recession will hit each corner of the world or how long it will take for the next phase in the financial cycle to begin. However, one thing that is certain is that the longer it takes the economy to settle, the more opportunities criminals will have to benefit from their schemes and come up with new ways to defraud people. Businesses should monitor the fraud environment around them closely and be ready to adjust their fraud management strategies quickly. They should also understand the complexity of the problems in front of them and that they will likely need a mixture of capabilities to sort them out while keeping their customer base happy. This is where fraud orchestration platforms could help by offering the needed solutions to solve multiple fraud issues and the flexibility to turn any of these tools on and off when needed. Contact us

Despite the constant narrative around “unprecedented times” and the “new normal,” if the current market volatility tells us anything, it’s to go back to basics. As financial institutions navigate COVID-19’s economic impact, and challenges that are likely to be different or more extreme than in the past, the best credit portfolio management practices are fundamental. The global pandemic impacts today’s data as existing data and analytics may not accurately reflect what is happening now, resulting in inaccurate portfolio assessment. In order to successfully navigate loss forecasting, predicting borrower behavior and controlling loss ratios, lenders must engage new data, analytics and economic scenarios suited for today’s changing times. In Experian’s latest white paper, “Credit Portfolio Management After the COVID-19 Recession,” we’ll explore best practices to combat the following challenges: Forecasting credit losses despite increased economic volatility Businesses have long used a variety of data, analytics and models to anticipate and project the future direction of their organization based on a number of data points; however, with the onset of the global pandemic, long-standing scenarios became suddenly irrelevant. Predicting borrower behavior given increased financial disparities The post-pandemic and pre-pandemic worlds are very different places for some borrowers. Pandemic-related job losses and other economic effects will not be spread evenly and this variability may be reflected in lenders’ portfolios. Controlling loss ratios In the post-COVID world, it will be mission critical for lenders to use high-quality and up-to-date data to balance priorities and identify which areas of their portfolio need attention now. Whether your portfolio is doing better than expected, as expected, or worse than expected, now is the time to refresh portfolio management strategy. Lenders should be watching for early indicators in loan portfolios to better navigate a fluctuating economy and that requires new resources and better tools. Take control of your business’ trajectory. Download now

This is the fourth in a series of blog posts highlighting optimization, artificial intelligence, predictive analytics, and decisioning for lending operations in times of extreme uncertainty. The first post dealt with optimization under uncertainty, the second with predicting consumer payment behavior, and the third with validating consumer credit scores. This post describes some specific Experian solutions that are especially timely for lenders strategizing their response to the COVID Recession. Will the US economy recover from the pandemic recession? Certainly yes. When will the economy recover? There is a lot more uncertainty around that question. Many people are encouraged by positive indicators, such as the initial rebound of the stock market, a return of many of the jobs lost at the beginning of the pandemic, and a significant increase in housing starts. August’s retail spending and homebuilder confidence are very encouraging economic indicators. Other experts doubt that the “V-shaped” recovery can survive flare-ups of the virus in various parts of the US and the world, and are calling for a “W-shaped” recovery. Employment indicators are alarming: many people remain out of work, some job losses are permanent, and there are more initial jobless claims each week now than at the height of the Great Recession. Serious hurdles to economic recovery may remain until a vaccine is widely available: childcare, urban transportation, and global trade, for example. I’m encouraged by the resilience of many of our country’s consumer lenders. They are generally responding well to these challenges. If past recessions are a guide, some lenders will not survive these turbulent times. This time, many lenders—whether or not they have already adopted the CECL accounting standards—have been increasing allowances for their anticipated credit losses. At least one rating agency believes major banks are prepared to absorb those losses from earnings. The lenders who are most prepared for the eventual recovery will be those that make good decisions during these volatile times and take action to put themselves in the best position in anticipation of the recovery that will certainly follow. The best lenders are making smart investments now to be prepared to capitalize on future opportunities. Experian’s analytics and consulting experts are continuously improving our suite of solutions that help consumer lenders and others assess consumer behavior and respond quickly to the rapidly fluctuating market conditions as well as changing regulations and credit reporting practices. Our newly announced Economic Response and Recovery Suite includes the ABCD’s that lenders need to be resilient and competitive now and to prepare to thrive during the eventual recovery: A – Analytics. As I’ve written about in prior blog posts, data is a prerequisite to making good business decisions, but data alone is not enough. To make wise, insightful decisions, lenders need to use the most appropriate analytical techniques, whether that means more meaningful attributes, more predictive and compliant credit scores, more accurate and defensible loss forecasting solutions, or optimization systems that help develop strategies in a world where budgets, regulations, and other constraints are changing. For example, Experian has released a set of Spotlight 2020 Attributes that help consumer lenders create a positive experience for customers who have received an accommodation during the pandemic. In many cases motivated by the new race to improve customer experience online, and in other cases as a reaction to new and creative fraud schemes, some clients are using this period as an opportunity to explore or deploy ethical and explainable Artificial Intelligence. B – Business Intelligence. Credit bureaus like Experian are uniquely situated to understand the impact of the COVID recession on America’s consumers. With impact reports, dashboards, and custom business intelligence solutions, lenders are working during the recession to gain an even better understanding of their current and prospective customers. We’re helping many of them to proactively help consumers when they need it most. For example, lenders have turned to us to understand their customer’s payment hierarchy—which bills they pay first when times are tough. Our free COVID-19 US Business Risk Index helps make lending options available to the businesses who need them most. And we’ve armed lenders with recommendations for which of our pre-existing attributes and scores are most helpful during trying times. Additional reporting tools such as the Auto Market Tracker, Ascend Market Insights Dashboard, and the weekly economic update video provide businesses with information on new market trends—information that helps them respond during the recession and promises to help them grow during the eventual recovery. C – Consulting. It’s good to turn data into information and information into insight, but how do these lenders incorporate these insights in their business strategies? Lenders and other businesses have been turning to Experian’s analytics and Advisory services consultants to unlock the information hidden in credit and other data sources—finding ways to make their business processes more efficient and more effective while developing quick response plans and more long-term recovery strategies. D – Delivery. Decision science is the practice of using advanced analytics, artificial intelligence, and other techniques to determine the best decision based on available data and resources. But putting those decisions into action can be a challenge. (Organizations like IBM and Gartner estimate that a great majority of data science projects are never put into production.) Experian technologies—from our analytics platform to our attribute integration and decision management solutions ensure that data-driven decisions can be quickly implemented to make a real difference. Treating each customer optimally has a number of benefits—whether you are trying to responsibly grow your portfolio, reduce credit losses and allowances, control servicing costs, or simply staying in compliance during dynamic times. In the age of COVID, IT departments have placed increased priority on agility, security, customer experience, and cost control, and appreciate cloud-first approach to deploying analytics. It’s too early to know how long this period of extreme uncertainty will last. But one thing is certain: it will come to an end, and the economy will recover someday. I predict that many of the companies that make the best use of data now will be the ones who do the best during the recovery. To hear more ways your organization can navigate this downturn and the recovery to follow, please watch our on-demand webinar and check out our Economic Response and Recovery Suite. Watch the Webinar

Experian’s own Chris Ryan and Bobbie Paul recently joined David Mattei from Aite to discuss the latest research and insights into emerging fraud schemes and how businesses can combat them in light of COVID-19 and the resulting economic changes. Between them, Chris, Bobbie, and David have more than 60 years of experience in the world of fraud prevention. Listen in as they discuss how businesses can shape their fraud prevention plan in the short term, including: The impacts of the health crisis and physical distancing The rise of e-commerce and consumer digital engagement Changes in criminal activity Fraud attack vectors 2020 fraud loss projections Critical next steps for the 30-60 day time frame Experian · Make Your Fraud Plan Recession-Ready: 2020 Fraud Trends

The economic impact of the COVID-19 health crisis is ever-evolving and requires great flexibility and planning from lenders. Shannon Lois, Experian’s Senior Vice President, Analytics, Consulting and Operations, discusses what lenders can expect and next steps to take. Q: Though COVID-19 is catalyzing a sharp economic slowdown, many experts expect it to be temporary and liken it more to a global natural disaster than the prior financial crisis. What are your reactions? SL: There is still debate as to whether we will have a U-shaped or a V-shaped recession and its probable severity and longevity. Regardless, we are in a recession caused by a health pandemic with uncertainty of what it will mean for our global economy and without a clear view as to when it will end. The sooner we can contain the virus the more it will help to curtail the size of the recession. The unemployment rates and the consumer lack of confidence in the future will continue to contract spending which in turn will continue to propagate the recession. Our ability to limit COVID-19 over the coming months will have a direct impact in the economy, although the effects will probably linger on for six or more months. Q: From an economic perspective, what are the current trends we’re seeing? SL: Unemployment has skyrocketed and every business sector has been impacted although with different degrees of severity. In particular, tourism/hospitality, airlines, automotive, consumer products and retail have suffered. Consumers’ financial status varies and will continue to fluctuate, and credit conditions tighten while welfare payments increase. The government programs that have started will help, but they’re not enough to counter a prolonged recession. As some states seek to reopen and others extend their shelter in place orders, we will continue to see economic changes, with different sectors bouncing back or dipping further depending on their geographic location. Q: How does the economic slowdown compare to what we may have expected previously? SL: This recession is different than anything we have encountered previously not only because of the health concerns and implication of our population but because of the uncertainty of it all. As an example, social distancing has significantly and immediately impacted consumer demand but overall it is their low confidence in the future that will cause a continuous drop in discretionary and non-discretionary spending. Not only do we have challenges on the demand side, we also are seeing the same on the supply side with no automotive manufacturing occurring in the USA, and international oil flooding the market causing negative impact on domestic oil and the broad energy market. Q: How do the unemployment and liquidity challenges come into play? SL: The unemployment rate has already jumped to a record high. Most consumers are facing liquidity and affordability challenges and businesses do not have enough cash reserves to sustain them. Consumer activity has shifted drastically across all channels while lenders are exercising more caution. If this is a V-shaped recession (and hopefully it will be), then most activity is bound to spring back quickly in Q3. With companies safeguarding some jobs and the help of governments’ supplemental programs, businesses will restore supply and consumer demand will get a kick start. Q: What is the smartest next play for financial institutions? SL: The path forward requires several steps. First, understand your customers, existing and new. Refine your policies with the right information around your customers’ financial situations and extend programs (forbearance and loan payment forgiveness) as needed under the right guidelines. It’s also important to use refreshed data to lend to consumers and businesses who need it now more than ever, with the proper policies and fraud checks in place. Finally, increase your agility to operate effectively and dynamically with automation, interactive communication and self-serving digital tools. Experian is committed to helping lenders throughout these uncertain times. For more resources, visit our Look Ahead 2020 Resource Hub. Learn more About Our Expert Shannon Lois, Senior Vice President, Analytics, Consulting and Operations, Decision Analytics Shannon and her team of analysts, scientists, credit, fraud and marketing risk management experts provide results-driven consulting services and state-of-the-art advanced analytics, science and data products to clients in a wide range of businesses, including banking, auto, credit, utility, marketing and finance. Prior to her current role, she founded the Advisory Services practice at Experian, driving to actionable and proven solutions for our clients’ most pressing business problems.

The effects of the COVID-19 pandemic has created extreme volatility in the US markets. While the high unemployment rate and impact on the stock market can be attributed to the pandemic, there were signs that the economy was already headed for a downturn. In a recent webinar, Mohammed Chaudhri, Experian’s UK Chief Economist, stated, “Even in the absence of COVID-19, […] the consensus was that the US was going into a period of a slowdown. Talks of a recession were building and financial indicators all pointed to an inverse yield curve.” With a global recession on the horizon, economists are using different scenarios to forecast potential outcomes. Chaudhri and his team of Experian economists mapped out four macroeconomic scenarios for economic recovery: V-shape scenario: A scenario in which the U.S. is able to recover losses and is able to recover quickly – possibly within 3 months. The impacts of strict lockdowns and social distancing may allow for a V-shape recovery. This V-shape follows previous pandemics and is the most likely outcome. Delayed V-shape scenario: A scenario in which the economy bounces back (albeit much slower than a regular V-shape). This may occur as various states slowly lift their lockdown guidelines and return to business as usual. This delay can be caused by regulations and guidelines that vary from state to state. U-shape scenario: A scenario in which the U.S. is unable to return to pre-COVID-19. W-shape scenario: A scenario that is much more serious than a U-shape and has the greatest impact on the economy. This can occur if the state lockdowns are lifted too early and a reemergence of the virus occurs. In our latest on-demand webinar, our experts discuss current trends which are indicative of emerging patterns and highlight economic forecasts that show some immediate concentrations of risk and exposure and the implications for your organization. Take a deeper dive into the latest data insights relating to the credit economy, and specifically, the impact brought by COVID-19. Explore the macroeconomic outlook, including: The immediate and near-term economic impact Views on how a downturn could impact consumers’ affordability and emerging signs of vulnerability Views on what KPIs you should focus on Watch the webinar

This is the final part of a three part series of blog posts highlighting key focus areas for your response to the COVID-19 health crisis: Risk, Operations, Consumer Behavior, and Reporting and Compliance. For more information and the latest resources, please visit Look Ahead 2020, Experian’s COVID-19 resource center with the latest news and tools for our business partners as well as links to consumer resources and a risk simulator. To read the first post, click here. To read the second post, click here. Consumer Behavior Changes Consumers will be hit hard by the economic fallout from the virus. They’ll need to manage available credit and monthly income to bridge the gap when many people are faced with lost wages, tips and the ability to work. Often, the only way to monitor these short-term risks is with trended credit attributes, from both traditional and alternative data sources. These attributes were developed to provide additional insights into how consumer credit usage is trending over time. Is their debt and spending increasing? Have their credit lines been reduced? Have they historically been a transactor but have now started revolving balances? Could the account be a synthetic identity, set up for intentional misuse of credit? The most predictive attributes available in these times can transform how you can identify and respond to risk. Reporting and Compliance The regulatory environment is continuing to shift. There are continuous changes to compliance in the digital space for emerging channels and applications. There will be impacts to credit reporting and processes that may echo the response from other major natural disasters. The good news is that the framework developed for Comprehensive Capital Analysis and Review (CCAR) stress testing can be used to run scenarios and understand impacts. Although bank capital is very strong, additional regulation, such as the Current Expected Credit Losses (CECL), with all the latest shifts around compliance, may continue to increase the pressure on financial institutions. Having an adaptable process to forecast and stress-test scenarios to adjust capital requirements, especially in light of government fiscal and monetary stimulus measures, will be at the core of managing financial stability during a period of changes. Conclusion We need to brace for the pending recession after the longest economic expansion in our lifetimes. These are the times where organizations may struggle to survive or thrive in the face of adversity. This is the time to act on your strategic plan, lean on your strategic partners, and leverage industry leading data and capabilities to soften the landing and thrive in the next phase of growth. Let’s prepare and get through this, together. Learn More

For the last several years, as the global economy flourished, the opportunities created by removing friction and driving growth guided business strategies governing identity and fraud. The amount of profitable business available in a low-friction environment simply outweighed the fraud that could be mitigated with more stringent verification methods. Now that we’re facing a global crisis, it’s time to reconsider the approach that drove the economic boom that defined that last decade. Recognizing how economic changes impact fraud At the highest level, we separate fraud into two types; third party fraud and first party fraud. In simple terms, third party fraud involves the misuse of a real customer’s identity or unauthorized access to a real customer’s accounts or assets. First party fraud involves the use of an identity that the fraudster controls—whether it’s their own identity, a manipulated version of their own identity, or a synthetic identity that they have created. The important difference in this case is that the methods of finding and stopping third party fraud remain constant even in the event of an economic downturn – establish contact with the owner of the identity and verify whether the events are legitimate. Fraud tactics will evolve, and volumes increase as perpetrators also face pressure to generate income, but at the end of the day, a real person is being impersonated, and a victim exists that will confirm when fraud is taking place. Changes in first party fraud during an economic downturn are dramatically different and much more problematic. The baseline level of first party fraud using synthetic, manipulated and the perpetrator’s own identity continue, but they are augmented by real people facing desperate circumstances and existing “good” customers who over-extend while awaiting a turn-around. The problem is that there is no “victim” to confirm fraud is occurring, and the line between fraud (which implies intent) and credit default (which does not) becomes very difficult to navigate. With limited resources and pressures of their own, at some point lenders must try to distinguish deliberate theft from good customers facing bad circumstances and manage cases accordingly. The new strategy When times are good, it’s easier to build up a solid book of business with good customers. Employment rates are high, incomes are stable, and the risks are manageable. Now, we’re experiencing rapidly changing conditions, entire industries are disrupted, unemployment claims have skyrocketed and customers will need assistance and support from their lenders to help them weather the storm. This is a reciprocal relationship – it behooves those same lenders to help their customers get through to the other side. Lenders will look to limit losses and strengthen relationships. At the same time, they’ll need to reassess their existing fraud and identity strategies (among others) as every interaction with a customer takes on new meaning. Unexpected losses We’ve all been bracing for a recession for a while. But no one expected it to show up quite like it did. Consumers who have been model customers are suddenly faced with a complete shift in their daily life. A job that seemed secure may be less so, investments are less lucrative in the short term, and small business owners are feeling the pressure of a change in day-to-day commerce. All of this can lead to unexpected losses from formerly low-risk customers. As this occurs, it becomes more critical than ever to identify and help good customers facing grim circumstances and find different ways to handle those that have malicious intent. Shifting priorities When the economy was strong, many businesses were able to accept higher losses because those losses were offset by immense growth. Unfortunately, the current crisis means that some of those policies could have unforeseen consequences. For instance – the loss of the ability to differentiate between a good customer who has fallen on hard times and someone who’s been a bad actor from the start. Additionally, businesses need to revise their risk management strategies to align with shifting customer needs. The demand for emergency loans and will likely rise, while loans for new purchases like cars and homes will fall as consumers look to keep their finances secure. As the need to assist customers in distress rises and internal resources are stressed, it’s critical that companies have the right tools in place to triage and help customers who are truly in need. The good news The tools businesses like yours need to screen first party fraud already exist. In fact, you may already have the necessary framework in place thanks to an existing partnership, and a relatively simple process could prepare your business to properly screen both new and existing customers at every touchpoint. This global crisis is nowhere near over, but with the right tools, your business can protect itself and your customers from increased fraud risks and losses of all sorts – first party, stolen identities, or synthetic identities, and come out on the other side even stronger. Contact Experian for a review of your current fraud strategy to help ensure you’re prepared to face upcoming challenges. Contact us

This is the second of a three part series of blog posts highlighting key focus areas for your response to the COVID-19 health crisis: Risk, Operations, Consumer Behavior, and Reporting and Compliance. For more information and the latest resources, please visit Look Ahead 2020, Experian’s COVID-19 resource center with the latest news and tools for our business partners as well as links to consumer resources and a risk simulator. To read the introductory post, click here. Strategic Focus on Risk The last recession spurred an industry-wide systemic focus on stressed scenario forecasting. Now’s the time to evaluate the medium- to long-term impacts of the downturn response on portfolio risk measurement. The impact will be wide ranging, requiring recalibration of scorecards and underwriting processes and challenging assumptions related to fees, net interest income, losses, expenses and liquidity. There are critical inputs to understand portfolio monitoring and benchmarking by account types and segments. Higher unemployment across the country is likely. You need a thorough response to successfully navigate the emerging risks. Expanding credit line management efforts for existing accounts is critical. Proactively responding to the needs of your customers will demand a wide range of data and analytics and more frequent and active processes to take action. Current approaches and tools with increased automation may need to be reevaluated. When sudden economic shocks occur, statistical models may still rank-order effectively, while the odds-to-score relationships deteriorate. This is the time to take full advantage of explainable machine learning techniques to quickly calibrate or rebuild scorecards with refreshed data (traditional and alternative) and continue the learning cycle. As your risk management tools are evaluated and refreshed, there are many opportunities to target your servicing strategies where they can produce results. This may take the form of identifying segments exhibiting financial stress that can benefit from deferred payments, loan consolidation or refinancing. It might also involve more typical risk mitigation strategies, such as credit line reduction. There are several scenarios that may emerge over the next nine to 12 months that can offer opportunities to deepen relationships with your customers while managing long-term risk exposure. Optimizing Business Operations One of the most significant impacts to your business is the increase in transaction volumes as a result of the economic shock. We expect material increases in collections, refinancing and hardship programs. These increases are arriving at a time when many businesses have streamlined their teams in concert with periods of low delinquency and credit losses. Additional strain from call center shutdowns and limited staffing can easily overwhelm operations and cause business continuity plans to breakdown. More than ever, the use of digital channels and self-servicing technology are no longer nice-to-haves. Customers expect online access, and efficiency demands automation, including virtual assistants. As more volume migrates to these channels, it’s critical to have the right customer experience and fraud risk controls deployed through flexible, cloud-based systems. Learn More

This is the introduction to a series of blog posts highlighting key focus areas for your response to the COVID-19 health crisis: Risk, Operations, Consumer Behavior, and Reporting and Compliance. For more information and the latest resources, please visit Look Ahead 2020, Experian's COVID-19 resource center with the latest news and tools for our business partners as well as links to consumer resources and a risk simulator. Responding to COVID-19 The response to COVID-19 is rolling out across the global financial system and here in North America. Together, we’re adapting to working remotely and adjusting to our “new normal.” It seems the long forecasted economic recession is finally and abruptly on our doorstep. Recession planning has been a focus for many organizations, and it’s now time to act on these contingency plans and respond to the downturn. The immediate effects and those that quickly follow the pandemic will widely impact the economy, affecting businesses of all sizes, employment and consumer confidence. We learned from the housing crisis and Great Recession how to identify and adapt to emerging risks. We can apply those skills while rebuilding the economy and focusing on the consumer. How should you respond? What strategies should you deploy? How can you balance emerging risks, changing consumer expectations and regulatory impacts? First, let's draw upon the best knowledge we gained from the last recession and apply those learnings. Second, we need to understand the current environment including the impact of major changes in technology and consumer behavior over the last few years. This approach will allow us to identify key themes to help build-out strategies to focus resources, respond successfully and deliver for stakeholders. Anticipate the pervasive and highly impactful market dynamics and trends The impact of this downturn on the consumer, on businesses and on financial institutions will be very different to that of the Great Recession. There will be a complete loss of income for many workers and small businesses. In a survey conducted by the Center for Financial Services Innovation (CFSI), more than 112 million Americans said that they don’t have enough savings to cover three months of living expenses*. These volatile market conditions and consumer insecurity will cause changes to your business models. You must prepare to manage increased fraud attacks, continue to push toward digital banking and understand regulatory changes. Learn More *U.S. Financial Health Pulse, 2018 Baseline Survey Results. https://s3.amazonaws.com/cfsi-innovation-files-2018/ wp-content/uploads/2018/11/20213012/Pulse-2018- Baseline-Survey-Results-11-16.18.pdf

Originally posted by Experian Global News blog At Experian, we have an unwavering commitment to helping consumers and clients manage through this unprecedented period. We are actively working with consumers, lenders, lawmakers and regulators to help mitigate the potential impact on credit scores during times of financial hardship. In response to the urgent and rapid changes associated with COVID-19, we are accelerating and enhancing our financial education programming to help consumers maintain good credit and gain access to the financial services they need. This is in addition to processes and tools the industry has in place to help lenders accommodate situations where consumers are affected by circumstances beyond their control. These processes will be extended to those experiencing financial hardship as a result of COVID-19. As the Consumer’s Credit Bureau, our commitment at Experian is to inform, guide and protect our consumers and customers during uncertain times. With expected delays in bill payments, unprecedented layoffs, hiring freezes and related hardships, we are here to help consumers in understanding how the credit reporting system and personal finance overall will move forward in this landscape. One way we’re doing this is inviting everyone to join our special eight-week series of #CreditChat conversations surrounding COVID-19 on Wednesdays at 3 p.m. ET on Twitter. Our weekly #CreditChat program started in 2012 to help the community learn about credit and important personal finance topics (e.g. saving money, paying down debt, improving credit scores). The next several #CreditChats will be dedicated to discussing ways to manage finances and credit during the pandemic. Topics of these #CreditChats will include methods and strategies for bill repayment, paying down debt, emergency financial assistance and preparing for retirement during COVID-19. “As the consumer’s credit bureau, we are committed to working with consumers, lenders and the financial community during and following the impacts of COVID-19,” says Craig Boundy, Chief Executive Officer of Experian North America. “As part of our nation’s new reality, we are planning for options to help mitigate the potential impact on credit scores due to financial hardships seen nationwide. Our #CreditChat series and supporting resources serve as one of several informational touchpoints with consumers moving forward.” Being fully committed to helping consumers and lenders during this unprecedented period, we’ve created a dedicated blog page, “COVID-19 and Your Credit Report,” with ongoing and updated information on how COVID-19 may impact consumers’ creditworthiness and – ultimately – what people should do to preserve it. The blog will be updated with relevant news as we announce new solutions and tactics. Additionally, our “Ask Experian” blog invites consumers to explore immediate and evolving resources on our COVID-19 Updates page. In addition to this guidance, and with consumer confidence in the economy expected to decline, we will be listening closely to the expert voices in our Consumer Council, a group of leaders from organizations committed to helping consumers on their financial journey. We established a Consumer Council in 2009 to strengthen our relationships and to initiate a dialogue among Experian and consumer advocacy groups, industry experts, academics and other key stakeholders. This is in addition to ongoing collaboration with our regulators. Additionally, our Experian Education Ambassador program enables hundreds of employee volunteers to serve as ambassadors sharing helpful information with consumers, community groups and others. The goal is to help the communities we serve across North America, providing the knowledge consumers need to better manage their credit, protect themselves from fraud and identity theft and lead more successful, financially healthy lives. COVID-19 has impacted all industries and individuals from all walks of life. We want our community to know we are right there with you. Learn more about our weekly #CreditChat and upcoming schedule here. Learn more

Do you have 20/20 vision when it comes to the readiness of your organization? How financially healthy are your customers today? They are likely facing some challenges and difficult choices. Based on a study by the Center for Financial Services Innovation (CFSI), almost half of the US adult population - that’s 112.5 million - say they do not have enough savings to cover at least three months of living expenses. With debt rising and a possible recession on the horizon, it’s crucial to have a solid strategy in place for your organization. Here are three easy steps to help you prepare: Anticipate the recession before it arrives Gathering a complete view of your customers can be difficult if you have multiple systems, which can result in subjective, costly and inefficient processes. If you don’t have a full picture of your customers, it’s hard to understand their risk, behavior and ability to pay and to determine the most effective treatment decisions. Having the right data is only the first step. Using analytics to make sense of the data helps you better understand your customers at an individual level, which will increase recovery rates and improve the customer experience. Analytics can provide early-warning indicators that identify customers most likely to miss payments, predict future behavior, and deliver the best treatment option based on a customer’s specific situation or behavior. With a deeper understanding of at-risk customers, you can apply more targeted interventions that are specific to each customer, so you can be confident your collections process is individualized, efficient and fair. The result? A cost-effective, compliant process focused on retaining valuable customers and reducing losses. What to look for: ✔ Know when customers are experiencing negative credit events ✔ View consumer credit trends that may not yet be visible on your own account base ✔ Watch for payment stress – understand the actual payment consumers are making. Is it changing? ✔ See individual trends and take action – are your customers sliding down to a lower score band? ✔ Understand how your client-base is performing within your own portfolio and with other organizations Take immediate and impactful actions around risk mitigation and staffing Every interaction with consumers needs optimizing, from target marketing through to collections and recovery. Organizations that proactively modernize their business to scale and increase effectiveness before the next economic downturn may avoid struggling to address rising delinquencies when the economy corrects itself. This may improve portfolio performance and collection capabilities — significantly increasing recoveries, containing costs and sustaining returns. Identify underperforming products and inefficient processes by staff. Consider reassessing the data used and the manual processes required for making decisions. Optimize product pricing and areas where organizations or staff could automate the decision processes. Areas to focus: ✔ Identity theft protection and account takeover awareness ✔ Improve underwriting strategy and automation ✔ Maximize profitability — drive spend, optimize approvals, line assignment and pricing ✔ Evaluate collection risk strategies and operational efficiencies Design and deploy a strategy to be organizationally and technologically ready for change Communication is key in debt recovery. Failing to contact customers via their preferred channel can cause frustration and reduce the likelihood of recovery. Your customers are looking for a convenient and discreet way to negotiate or repay debt, and if you aren’t providing one, you’re incurring higher collections costs and lower recovery rates. With developments in the digital world, consumer interactions have changed. Most people prefer to communicate via mobile or online, with little to no human interaction. Behavioral analytics help to automate and decide the next best action, so you contact the right customer at the right time through the right channel. In addition, offering a convenient, discreet way to negotiate or repay debt can result in customers who are more engaged and more likely to pay. Online and self-service portals along with AI-powered chatbots use the latest technology to provide a safe and customer-centric experience, creating less time-consuming interactions and higher customer satisfaction. Your digital collections process is more convenient and less stressful for consumers and more profitable and compliant for you. Visualize the future... ✔ Superior customer service is embraced at the end of the customer life cycle as it is in the beginning ✔ Leverage data, analytics, software, and industry expertise to drive an automated collections process with fewer manual interventions ✔ Meet the growing expectation for digital consumer self-service by providing the ability to proactively negotiate and manage debt through preferred contact channels ✔ When economy and market conditions change for the worst, have the right data, analytics, software in place and be prepared to implement relevant collections strategies to remain competitive in the market Don’t wait until the next recession hits. Our collaborative approach to problem solving ensures you have the right solution in place to solve your most complex problems and are ready for market changes. The combination of our data, analytics, fraud tools, decisioning software and consulting services will help you proactively manage your portfolio to minimize the flow of accounts into collections and modernize your collections and recovery processes. Learn More

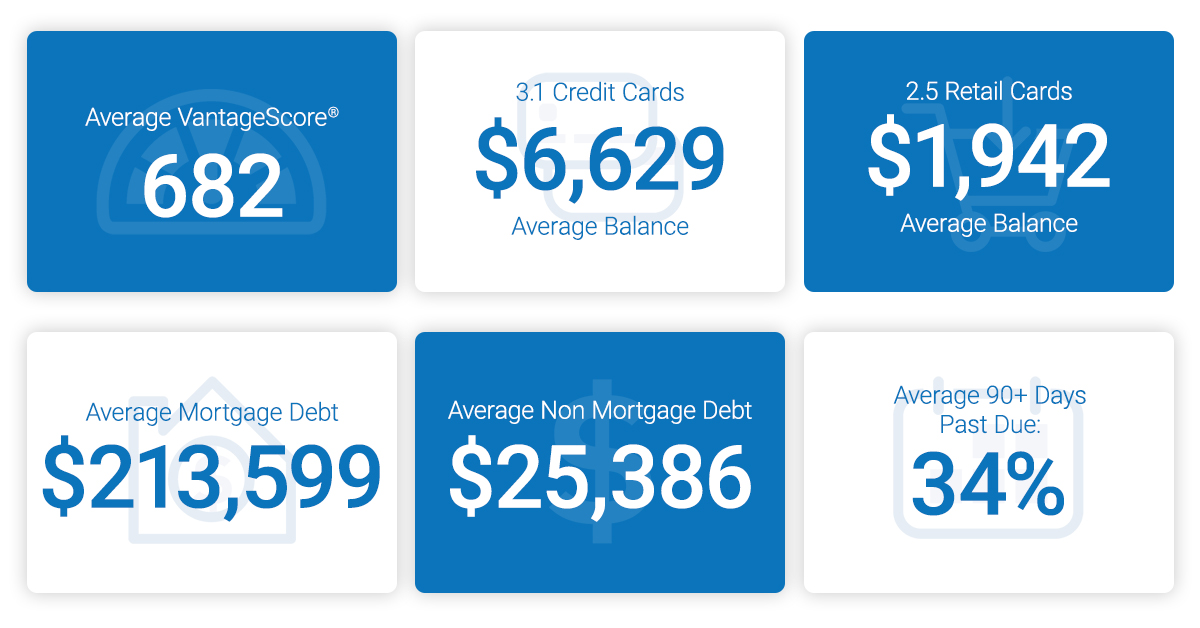

As consumers prepare for the next decade, we look at how we’re rounding out this year. The results? The average American credit score is 682, an eight-year high. Experian released the 10th annual state of credit report, which provides a comprehensive look at the credit performance of consumers across America by highlighting consumer credit scores and borrowing behaviors. And while the data is spliced to show men vs. women, as well as provides commentary at the state and generational level, the overarching trend is up. Even with the next anticipated economic correction often top of mind for financial institutions, businesses and consumers alike, 2019 was a year marked by more access, more spending and decreasing delinquencies. Things are looking up. “We are seeing a promising trend in terms of how Americans are managing their credit as we head into a new decade with average credit scores increasing two points since 2018 to 682 – the highest we’ve seen since 2011,” said Shannon Lois, Senior Vice President and Head of EAS, Analytics, Consulting & Operations for Experian Decision Analytics. “Average credit card balances and debt are up year over year, yet utilization rates remain consistent at 30 percent, indicating consumers are using credit as a financial tool and managing their debts responsibly.” Highlights of Experian’s State of Credit report: 3-year comparison 2017 2018 2019 Average number of credit cards 3.06 3.04 3.07 Average credit card balances $6,354 $6,506 $6,629 Average number of retail credit cards 2.48 2.59 2.51 Average retail credit card balances $1,841 $1,901 $1,942 Average VantageScore® credit score[1, 2] 675 680 682 Average revolving utilization 30% 30% 30% Average nonmortgage debt[3] $24,706 $25,104 $25,386 Average mortgage debt $201,811 $208,180 $231,599 Average 30 days past due delinquency rates 4.0% 3.9% 3.9% Average 60 days past due delinquency rates 1.9% 1.9% 1.9% Average 90+ days past due delinquency rates 7.3% 6.7% 6.8% In the scope of the credit score battle of the sexes, women have a four-point lead over men with an average credit score of 686 compared to 682. Their lead is a continued trend since 2017 where they’ve bested their male counterparts. According to the report, while men carry more non-mortgage and mortgage debt than women, women have more credit cards and retail cards (albeit they carry lower balances). Generationally, Generations X, Y and Z tend to carry more debt, including mortgage, non-mortgage, credit card and retail card, than older generations with higher delinquency and utilization rates. Segmented by state and gender, Minnesota had the highest credit scores for both men and women, while Mississippi was the state with the lowest average credit score for females and Louisiana was the lowest average credit score state for males. As we round out the decade and head full-force into 2020, we can reflect on the changes in the past year alone that are helping consumers improve their financial health. Just to name a few: Experian launched Experian BoostTM in March, allowing millions of consumers to add positive payment history directly to their credit file for an opportunity to instantly increase their credit score. Since then, there has been over 13 million points boosted across America. Experian LiftTM was launched in November, designed to help credit invisible and thin-file consumers gain access to fair and affordable credit. Long-standing commitments to consumer education, including the Ask Experian Blog and volunteer work by Experian’s Education Ambassadors, continue to offer assistance to the community and help consumers better understand their financial actions. From what we can tell, this is just the beginning. “Understanding the factors that influence their overall credit profile can help consumers improve and maintain their financial health,” said Rod Griffin, Experian’s director of consumer education and awareness. “Credit can be used as a financial tool. Through this report, we hope to provide insights that will help consumers make more informed decisions about credit use as we prepare to head into a new decade.” Learn more 1 VantageScore® is a registered trademark of VantageScore Solutions, LLC. 2 VantageScore® credit score range is 300 to 850. 3 Average debt for this study includes all credit cards, auto loans and personal loans/student loans.

Article written by Melanie Smith, Senior Copywriter, Experian Clarity Services, Inc. It’s been almost a decade since the Great Recession in the United States ended, but consumers continue to feel its effects. During the recession, millions of Americans lost their jobs, retirement savings decreased, real estate reduced in value and credit scores plummeted. Consumers that found themselves impacted by the financial crisis often turned to alternative financial services (AFS). Since the end of the recession, customer loyalty and retention has been a focus for lenders, given that there are more options than ever before for AFS borrowers. To determine what this looks like in the current climate, we examined today’s non-prime consumers, what their traditional scores look like and if they are migrating to traditional lending. What are alternative financial services (AFS)? Alternative financial services (AFS) is a term often used to describe the array of financial services offered by providers that operate outside of traditional financial institutions. In contrast to traditional banks and credit unions, alternative service providers often make it easier for consumers to apply and qualify for lines of credit but may charge higher interest rates and fees. More than 50% of new online AFS borrowers were first seen in 2018 To determine customer loyalty and fluidity, we looked extensively at the borrowing behavior of AFS consumers in the online marketplace. We found half of all online borrowers were new to the space as of 2018, which could be happening for a few different reasons. Over the last five years, there has been a growing preference to the online space over storefront. For example, in our trends report from 2018, we found that 17% of new online customers migrated from the storefront single pay channel in 2017, with more than one-third of these borrowers from 2013 and 2014 moving to online overall. There was also an increase in AFS utilization by all generations in 2018. Additionally, customers who used AFS in previous years are now moving towards traditional credit sources. 2017 AFS borrowers are migrating to traditional credit As we examined the borrowing behavior of AFS consumers in relation to customer loyalty, we found less than half of consumers who used AFS in 2017 borrowed from an AFS lender again in 2018. Looking into this further, about 35% applied for a loan but did not move forward with securing the loan and nearly 24% had no AFS activity in 2018. We furthered our research to determine why these consumers dropped off. After analyzing the national credit database to see if any of these consumers were borrowing in the traditional credit space, we found that 34% of 2017 borrowers who had no AFS activity in 2018 used traditional credit services, meaning 7% of 2017 borrowers migrated to traditional lending in 2018. Traditional credit scores of non-prime borrowers are growing After discovering that 7% of 2017 online borrowers used traditional credit services in 2018 instead of AFS, we wanted to find out if there had also been an improvement in their credit scores. Historically, if someone is considered non-prime, they don’t have the same access to traditional credit services as their prime counterparts. A traditional credit score for non-prime consumers is less than 600. Using the VantageScore® credit score, we examined the credit scores of consumers who used and did not use AFS in 2018. We found about 23% of consumers who switched to traditional lending had a near-prime credit score, while only 8% of those who continued in the AFS space were classified as near-prime. Close to 10% of consumers who switched to traditional lending in 2018 were classified in the prime category. Considering it takes much longer to improve a traditional credit rating, it’s likely that some of these borrowers may have been directly impacted by the recession and improved their scores enough to utilize traditional credit sources again. Key takeaways AFS remains a viable option for consumers who do not use traditional credit or have a credit score that doesn’t allow them to utilize traditional credit services. New AFS borrowers continue to appear even though some borrowers from previous years have improved their credit scores enough to migrate to traditional credit services. Customers who are considered non-prime still use AFS, as well as some near-prime and prime customers, which indicates customer loyalty and retention in this space. For more information about customer loyalty and other recently identified trends, download our recent reports. State of Alternative Data 2019 Lending Report

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. If you typed “alternative data and credit” into a Google search today, you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – as Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as homeownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian, we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are others around the world. As I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time, there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-file consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game-changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s getting late.