Tag: marketing

Best practices and innovative strategies for banking to millennials Before we begin, a disclaimer: Banking to millennials is a long-term strategy. Many marketing campaigns will not drive immediate returns on investment, but they lay the groundwork for a lifelong, mutually beneficial relationship. Now, some good news. Millennials are just beginning their financial journey — getting ready to embark on a life that includes homes, cars, families and small businesses. Connecting with this generation today can bode well for a financial institution’s success tomorrow. With a strong relationship in place, millennials will turn to that organization when they are ready to fund their life events. Below are some key strategies that will help financial institutions build and continue banking to millennials. Keeping up with technological expectations Millennials were raised in the digital age, and therefore mobile devices are the hubs of their digital lives. They expect real-time access to their accounts for peer-to-peer payments, deposits, paying bills and customer service. Not meeting their digital expectations could drive them to seek another — more technology-oriented — financial institution that embraces CNP, mobile apps and social media. Authentic and targeted marketing messaging Millennials expect targeted messaging. Generic, catchall offers of the past fall flat for them. They want banks to figure out who they are, what they need and how they can access it with the tap of a finger. Additionally, messages to millennials should have a genuine voice that advises and supports them in achieving their goals. Many millennials are interested in taking control of their financial lives but are not prepared to do so. This is a great opportunity for financial institutions to introduce themselves. Connect millennials to something bigger Earning a millennial’s trust is one of the greatest challenges for financial institutions. While money is important, millennials are motivated by becoming a part of something bigger than themselves. Institutions can connect with millennials by creating opportunities to give back or pay-it-forward. Examples include encouraging growth in underbanked markets, such as lending circles, peer-to-peer lending and small-business lending, or partnering with local universities and nonprofits. Strategic segmentation Millennials are the most diverse population group — yet strategic segmentation is still possible. One ideal segment is recent college graduates. As a group, they yield a much different profile than their counterparts without degrees. These ambitious millennials are more likely to focus on life choices that require major financial considerations, such as getting married, having children, buying their first home and earning higher salaries. These life events will require a diverse set of financial services products, and millennials will turn to the institution that has gained their trust first. Millennials are one of the most important markets as financial institutions look to invest in future, long-term growth. Financial institutions need to show millennials that they’re committed to listening and to laying the groundwork for relationships that will help them achieve their dreams. Remember, though, reaching this audience is not about an immediate return on investment but rather a long-term strategy to develop trust and brand preference. Begin the relationship now to reap the rewards later. For more insights and innovative strategies on how to best market and develop a strong relationship with millennials, download our recent white paper, Building lasting relationships with millennials.

With Black Friday quickly approaching, a recent Experian study shows online Black Friday searches are already tracking ahead of last year. This October, the weekly search share for Black Friday averaged 12% higher than October 2014 and is expected to increase dramatically between now and Thanksgiving week. Top product searches for the week ending October 31, 2015 include: Marketers can design more successful campaigns and maximize rewards for both consumers and brands by staying on top of the latest search trends. >> Holiday Hot Sheet

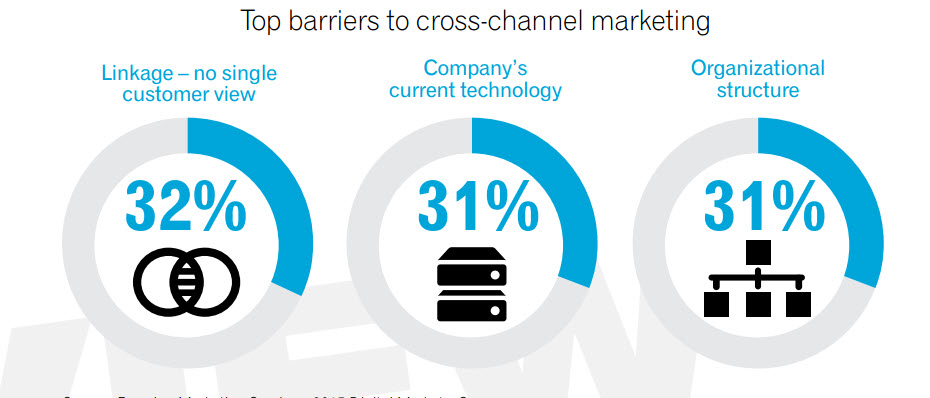

According to a recent Experian Marketing Services study, 99% of companies believe achieving a single customer view is important to their business, but only 24% have a single customer view today.

According to the latest research by Experian Marketing Services, nearly a third of all Americans use at least one type of smart or Internet-connected device* (wearable fitness tracker, smart watch, smart TV, smart home technology). While smart TVs have generated the most consumer interest, at least 14 percent of homes are smart homes (connected lights, locks, thermostats, window coverings, etc). Further, the smart home device category saw the most growth during the holiday season, with interest increasing 54 percent from November to December 2014. By 2020, the number of Internet-connected devices is expected to grow to 26 billion, creating new revenue streams and opportunities for marketers. Understanding how to reach customers in this newly connected world and creating resonant messages will be critical to future business success. Source: Experian Marketing Services, The Internet of Things: Opportunities through the rise in smart devices *Does not include smartphones, tablets or computers

The desire to return to portfolio growth is a clear trend in mature credit markets, such as the US and Canada. Historically, credit unions and banks have driven portfolio growth with aggressive out-bound marketing offers designed to attract new customers and members through loan acquisitions. These offers were typically aligned to a particular product with no strategy alignment between multiple divisions within the organization. Further, when existing customers submitted a new request for credit, they were treated the same as incoming new customers with no reference to the overall value of the existing relationship. Today, however, financial institutions are looking to create more value from existing customer relationships to drive sustained portfolio growth by increasing customer retention, loyalty and wallet share. Let’s consider this idea further. By identifying the needs of existing customers and matching them to individual credit risk and affordability, effective cross-sell strategies that link the needs of the individual to risk and affordability can ensure that portfolio growth can be achieved while simultaneously increasing customer satisfaction and promoting loyalty. The need to optimize customer touch-points and provide the best possible customer experience is paramount to future performance, as measured by market share and long-term customer profitability. By also responding rapidly to changing customer credit needs, you can further build trust, increase wallet share and profitably grow your loan portfolios. In the simplest sense, the more of your products a customer uses, the less likely the customer is to leave you for the competition. With these objectives in mind, financial organizations are turning towards the practice of setting holistic, customer-level credit lending parameters. These parameters often referred to as umbrella, or customer lending, limits. The challenges Although the benefits for enhancing existing relationships are clear, there are a number of challenges that bear to mind some important questions to consider: · How do you balance the competing objectives of portfolio loan growth while managing future losses? · How do you know how much your customer can afford? · How do you ensure that customers have access to the products they need when they need them · What is the appropriate communication method to position the offer? Few credit unions or banks have lending strategies that differentiate between new and existing customers. In the most cases, new credit requests are processed identically for both customer groups. The problem with this approach is that it fails to capture and use the power of existing customer data, which will inevitably lead to suboptimal decisions. Similarly, financial institutions frequently provide inconsistent lending messages to their clients. The following scenarios can potentially arise when institutions fail to look across all relationships to support their core lending and collections processes: 1. Customer is refused for additional credit on the facility of their choice, whilst simultaneously offered an increase in their credit line on another. 2. Customer is extended credit on a new facility whilst being seriously delinquent on another. 3. Customer receives marketing solicitation for three different products from the same institution, in the same week, through three different channels. Essentials for customer lending limits and successful cross-selling By evaluating existing customers on a periodic (monthly) basis, financial institutions can assess holistically the customer’s existing exposure, risk and affordability. By setting customer level lending limits in accordance with these parameters, core lending processes can be rendered more efficient, with superior results and enhanced customer satisfaction. This approach can be extended to consider a fast-track application process for existing relationships with high value, low risk customers. Traditionally, business processes have not identified loan applications from such individuals to provide preferential treatment. The core fundamentals of the approach necessary for the setting of holistic customer lending (umbrella) limits include: · The accurate evaluation of credit and default risk · The calculation of additional lending capacity and affordability · Appropriate product offerings for cross-sell · Operational deployment Follow my blog series over the next few months as we explore the essentials for customer lending limits and successful cross-selling.

By: Wendy Greenawalt Marketing is typically one of the largest expenses for an organization while also being a priority to reach short and long-term growth objectives. With the current economic environment, continuing to be unpredictable many organizations have reduced budgets and focused on more risk and recovery activities. However, in the coming year we expect to see improvements and organizations renew their focus to portfolio growth. We expect that campaign budgets will continue to be much lower than what was allocated before the mortgage meltdown but organizations are still looking for gains in efficiency and response to meet business objectives. Creation of optimized marketing strategies is quick and easy when leveraging optimization technology enabling your internal resources to focus on more strategic issues. Whether your objective is to increase organizational or customer level profit, growth in specific product lines or maximizing internal resources optimization can easily identify the right solution while adhering to key business objectives. The advanced software now available enables an organization to compare multiple campaign options simultaneously while analyzing the impact of modifications to revenue, response or other business metrics. Specifically, very detailed product offer information, contact channels, timing, and letter costs from multiple vendors and consumer preferences can all be incorporated into an optimization solution. Once defined the complex mathematical algorithm factors every combination of all variables, which could range in the thousands, are considered at the consumer level to determine the optimal treatment to maximize organizational goals and constraints. In addition, by incorporating optimized decisions into marketing strategies marketers can execute campaigns in a much shorter timeframe allowing an organization to capitalize on changing market conditions and consumer behaviors. To illustrate the benefit of optimization an Experian bankcard client was able to reduced analytical time to launch programs from 7 days to 90 minutes while improving net present value. In my next blog, we will discuss how organizations can cut costs when acquiring new accounts.

By: Wendy Greenawalt Marketing is typically one of the largest expenses for an organization and it is also a priority to reach short- and long-term growth objectives. With the current economic environment continuing to be unpredictable, many organizations have reduced budgets and are focusing more on risk management and recovery activities. However, in the coming year, we expect to see improvements in the economy and organizations renewing their focus on portfolio growth. We expect that marketing campaign budgets will continue to be much lower than those allocated before the mortgage meltdown but organizations will still be looking for gains in efficiency and responsiveness to meet business objectives. Optimizing decisions, creation of optimized marketing strategies, is quick and easy when leveraging optimization technology. Those strategies enable your internal resources to focus on more strategic issues. Whether your objective is to increase organizational or customer level profit, growth in specific product lines or maximizing internal resources, optimization / optimizing decisions can easily identify the right solution while adhering to key business objectives. The advanced software now available to facilitate optimizing decisions enables an organization to compare multiple campaign options simultaneously while analyzing the impact of modifications to revenue, response or other business metrics. Specifically, very detailed product offer information, contact channels, timing, and letter costs from multiple vendors -- and consumer preferences -- can all be incorporated into an optimization solution. Once defined, the complex mathematical algorithm factors every combination of all variables, which could range in the thousands. These variables are considered at the consumer level to determine the optimal treatment to maximize organizational goals and constraints. In addition, by optimizing decisions and incorporating them into marketing strategies, marketers can execute campaigns in a much shorter timeframe allowing an organization to capitalize on changing market conditions and consumer behaviors. To illustrate the benefit of optimization: an Experian bankcard client was able to reduce analytical time to launch programs from seven days to 90 minutes while improving net present value. In my next blog, we will discuss how organizations can cut costs when acquiring new accounts.