Tag: financial trends

How businesses respond to economic uncertainty can determine whether they get ahead or fall behind. To better prepare for the coming months, you must remain up to date on the latest economic developments to better understand and evolve with changing consumer needs. With insight into critical macroeconomic and consumer trends, you can proactively manage your portfolio, enhance your decisioning and seize new opportunities. Grab a cup of coffee and join Experian's Shawn Rife, Client Executive, and Josee Farmer, Economic Analyst, during our fireside chat on February 16 @ 1 P.M. ET/10 A.M. PT. Our expert speakers will provide a view of the latest economic and market trends, their impact on consumers, and how financial institutions can survive and thrive. Highlights include: Macroeconomic and consumer credit trends Economic implications on consumer behavior How financial institutions can adapt Register now

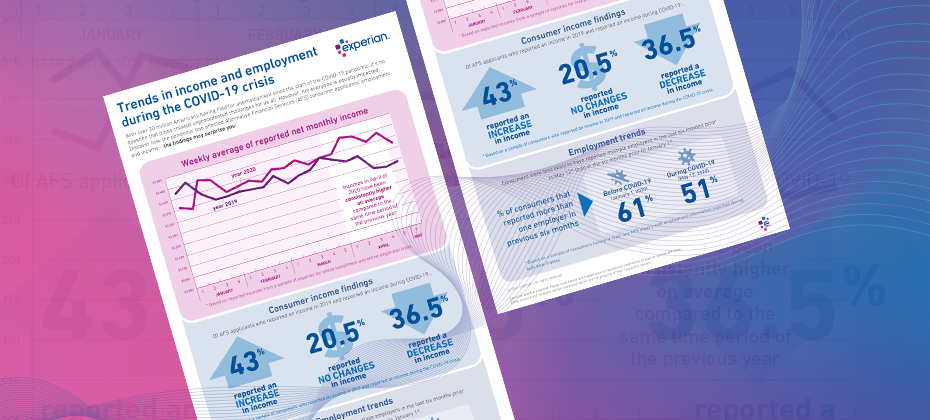

With many individuals finding themselves in increasingly vulnerable positions due to COVID-19, lenders must refine their policies based on their consumers’ current financial situations. Alternative Financial Services (AFS) data helps you gain a more comprehensive view of today's consumer. The COVID-19 pandemic has had far-reaching economic consequences, leading to drastic changes in consumers’ financial habits and behavior. When it comes to your consumers, are you seeing the full picture? See if you qualify for a complimentary hit rate analysis Download AFS Trends Report

The COVID-19 pandemic has created unprecedented challenges for the utilities industry. This includes the need to plan for – and be prepared to respond to – changing behaviors and a sudden uptick in collections activities. As part of our recently launched Q&A perspective series, Mark Soffietti, Experian’s Senior Manager of Analytics Consulting and Tom Hanson, Senior Energy Consultant, provided insight on how utility providers can evolve and refine their collections and recovery processes. Check out what they had to say: Q: How has COVID-19 impacted payment behavior and debt collections? TH: Consumer payment behavior is changing. For example, those who paid as agreed, may not currently have the means to pay and are now distressed borrowers. Or those who were sloppy payers before the pandemic may now be defaulting on a more consistent basis. MS: As we saw with the last recession when faced with economic stress, consumer and commercial payment behavior changes based on their needs and current cash flow. For example, people prioritize their car, as they need it to get to and from work, so they’ll likely pay their auto bills on time. The same goes for their credit cards, which they need to make ends meet. We expect this will also be true with COVID-19. The commercial segment will face more dramatic and challenging circumstances, where complete or partial business closures and lack of federal relief could have severe ramifications. Q: What new restrictions have been put in place surrounding debt collection efforts and outbound calls? TH: To protect consumers who may be experiencing financial distress, most states have imposed new, stringent restrictions to prevent utilities from engaging in certain collections activities. Utilities are currently not charging any late payment fees and are instead structuring payment plans. Additionally, all outbound collections efforts have been suspended and there is fieldwork being executed of services for both commercial and consumer properties. As of now, consumer and commercial fieldwork will likely not commence until after the first year or when the winter moratorium concludes. MS: The new restrictions imposed upon collections activities will likely drive consumer payment behavior. If consumers know that their utilities (i.e. energy and water) will not be shut off if they miss a payment, they will make these bills less of a priority. This will dramatically increase the amount owed when these restrictions are lifted next year. Q: Can we predict how the utilities industry will fare post-COVID-19? TH: The volume of accounts in collections and eligible for disconnect will be overwhelming. Many utility providers fear the unpaid balances consumers and commercial entities accumulate will be nearly impossible to fit into a repayment schedule. Both analyzing internal payment segments and overlaying external factors may be the best way to optimize the most critical go-forward plan. MS: The amount of people who fall into collections is going to greatly increase and utility providers need to start planning for it now to weather the storm. They will need to use data, analytics and tools to help them optimize their tasks, so they can be more efficient with their resources. Like many other industries, the utilities sector will look to increasing digitalization of their processes and having less social interaction where possible. This could mean the need and drive for expediting current smart meter programs where possible to enable remote fieldwork to assist in managing this unprecedented level of activity that is sure to overwhelm field operations (where allowed by state regulators). Q: What should utility providers be doing to plan for an uptick in collections activities post-COVID-19? TH: With regulatory mandated suspensions of collections activities for utility providers and self-selected reductions due to stay at home orders and staff protection, the backlog of payments, calls and inquiries once business resumes as normal is set to overwhelm existing capacity. More than ever, self-service options (text/web), Q&A and alternative communication methods will be needed to shepherd consumers through the collections process and minimize the strain on call center agents. Many utility providers are asking for external data points to segment their consumers by industry or by those whose employment would have been adversely impacted by COVID-19. MS: Utility providers should be monitoring consumer data in order to prepare for when they are able to collect. This will help them strategize the number of resources they will need in their call centers and out in the field performing shut off activities. Given that the rise in cases will be more volume than their call centers can handle, they will need to use their resources wisely and plan to use them efficiently when they are able to resume collections. Q: How can Experian help utility providers reduce collections costs and maximize recovery? TH: Experian can help revise collections tactics and segmentation strategies by providing insight on how consumers are paying other creditors and identifying new segmentation opportunities as we emerge from the freeze on collections activities. Collections cases will be complex, and many factors and constraints will need to balanced against changing goals, making optimization key. MS: Utilizing Experian’s credit data and models can help ensure that resources are being used efficiently (i.e. making successful calls). There is also a need to leverage ability to pay models as well as prioritization models. By using these models and tools, utility providers can optimize their treatment strategies, reduce costs and maximize dollars collected. Learn more About our Experts: Tom Hanson, Senior Energy Consultant, Experian CEM, North America Tom is a Senior Consultant within the Energy Vertical at Experian, supporting regulated energy companies throughout the U.S. He brings over 25 years of experience in the energy field and supports his clients throughout the customer lifecycle, providing expertise in ID verification, account treatment, fraud solutions, analytics, consulting and final bill/field optimization strategies and techniques. Mark Soffietti, Analytics Consulting Senior Manager, Experian Decision Analytics, North America Mark has over 15 years of experience transforming data into actionable knowledge for effective decision management. Mark’s expertise includes solution development for consumer and commercial lending across the credit spectrum – from marketing to collections.

Update: After closely monitoring updates from the WHO, CDC, and other relevant sources related to COVID-19, we have decided to cancel our 2020 Vision Conference. If you had the chance to experience tomorrow, today, would you take it? What if it meant you could get a glimpse into the future technology and trends that would take your organization to the next level? If you’re looking for a competitive edge – this is it. For more than 38 years, Experian’s premier conference has connected business leaders to data-driven ideas and solutions, fueling them to target new markets, grow existing customer bases, improve response rates, reduce fraud and increase profits. What’s in it for you? Everything to gain and nothing to lose. Are you a marketer? These sessions were made to drive your conversion rates to new heights: Know your customers via omnichannel marketing: Your customers are everywhere, but can you reach them? Learn how to drive business-expansion strategy, brand affinity and customer engagement across multiple channels. Plus, gain insight into connecting with customers via one-to-one messaging. By invitation only, the future of ITA marketing: An evolving landscape means marketers face new challenges in effectively targeting consumers while staying compliant. In this session, we’ll explore how you can leverage fair lending-friendly marketing data for targeting, analysis and measurement. Want the latest in technology trends? Dive into discussions to transform your customer experience: Credit in the age of technology transformation: Machine learning and artificial intelligence are the current darlings of big data, but the platform that drives the success of any big data endeavor is crucial. This session will dive into what happens behind the curtain. Put away your plastic – next-generation identity: An industry panel of experts discusses the newest digital identity and authentication capabilities – those in use today and also exciting solutions on the horizon. How about for the self-proclaimed data geeks? Analyze these: Alternative data: Listen in on an in-depth conversation about creative and impactful examples of using emerging data assets, such as alternative and consumer-permissioned data, for improved consumer inclusion, risk assessment and verification services. The next wave in open data: Experian will share their views on the potential of advanced data and models and how they benefit the global value chain – from consumer scores to business opportunities – regardless of local regulations. And the risk masters? Join us as we kick fraud to the curb: Understanding and tackling synthetic ID fraud: Synthetic IDs present a serious challenge for our entire industry. This expert panel will explore the current landscape – what’s working and what’s not, the expected impact of the next generation SSA eCBSV service, and best practice prevention methods. You are your ID – the new reality of biometrics: Consumers are becoming increasingly comfortable with biometrics. Just as CLEAR has transformed how we use our biometric identity to move through airports, sports venues and more, financial transactions can also be made friction-free. The point is, there’s something for everyone at Vision 2020. It’s not just another conference. Trade in stuffy tradeshow halls and another tri-fold brochure for the insights and connections you need to take your career and organization to the next level. Like technology itself, Vision 2020 promises to connect us, unify us and enable us all to create a better tomorrow. Join us for unique networking opportunities, one-on-one conversations with subject-matter experts and more than 50 breakout sessions with the industry’s most sought-after thought leaders.

Retailers are already starting to display their Christmas decorations in stores and it’s only early November. Some might think they are putting the cart ahead of the horse, but as I see this happening, I’m reminded of the quote by the New York Yankee’s Yogi Berra who famously said, “It gets late early out there.” It may never be too early to get ready for the next big thing, especially when what’s coming might set the course for years to come. As 2019 comes to an end and we prepare for the excitement and challenges of a new decade, the same can be true for all of us working in the lending and credit space, especially when it comes to how we will approach the use of alternative data in the next decade. Over the last year, alternative data has been a hot topic of discussion. If you typed “alternative data and credit” into a Google search today, you would get more than 200 million results. That’s a lot of conversations, but while nearly everyone seems to be talking about alternative data, we may not have a clear view of how alternative data will be used in the credit economy. How we approach the use of alternative data in the coming decade is going to be one of the most important decisions the lending industry makes. Inaction is not an option, and the time for testing new approaches is starting to run out – as Yogi said, it’s getting late early. And here’s why: millennials. We already know that millennials tend to make up a significant percentage of consumers with so-called “thin-file” credit reports. They “grew up” during the Great Recession and that has had a profound impact on their financial behavior. Unlike their parents, they tend to have only one or two credit cards, they keep a majority of their savings in cash and, in general, they distrust financial institutions. However, they currently account for more than 21 percent of discretionary spend in the U.S. economy, and that percentage is going to expand exponentially in the coming decade. The recession fundamentally changed how lending happens, resulting in more regulation and a snowball effect of other economic challenges. As a result, millennials must work harder to catch up financially and are putting off major life milestones that past generations have historically done earlier in life, such as homeownership. They more often choose to rent and, while they pay their bills, rent and other factors such as utility and phone bill payments are traditionally not calculated in credit scores, ultimately leaving this generation thin-filed or worse, credit invisible. This is not a sustainable scenario as we enter the next decade. One of the biggest market dynamics we can expect to see over the next decade is consumer control. Consumers, especially millennials, want to be in the driver’s seat of their “credit journey” and play an active role in improving their financial situations. We are seeing a greater openness to providing data, which in turn enables lenders to make more informed decisions. This change is disrupting the status quo and bringing new, innovative solutions to the table. At Experian, we have been testing how advanced analytics and machine learning can help accelerate the use of alternative data in credit and lending decisions. And we continue to work to make the process of analyzing this data as simple as possible, making it available to all lenders in all verticals. To help credit invisible and thin-file consumers gain access to fair and affordable credit, we’ve recently announced Experian Lift, a new suite of credit score products that combines exclusive traditional credit, alternative credit and trended data assets to create a more holistic picture of consumer creditworthiness that will be available to lenders in early 2020. This new Experian credit score may improve access to credit for more than 40 million credit invisibles. There are more than 100 million consumers who are restricted by the traditional scoring methods used today. Experian Lift is another step in our commitment to helping improve financial health of consumers everywhere and empowers lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. This isn’t just a trend in the United States. Brazil is using positive data to help drive financial inclusion, as are others around the world. As I said, it’s getting late early. Things are moving fast. Already we are seeing technology companies playing a bigger role in the push for alternative data – often powered by fintech startups. At the same time, there also has been a strong uptick in tech companies entering the banking space. Have you signed up for your Apple credit card yet? It will take all of 15 seconds to apply, and that’s expected to continue over the next decade. All of this is changing how the lending and credit industry must approach decision making, while also creating real-time frictionless experiences that empower the consumer. We saw this with the launch of Experian Boost earlier this year. The results speak for themselves: hundreds of thousands of previously thin-file consumers have seen their credit scores instantly increase. We have also empowered millions of consumers to get more control of their credit by using Experian Boost to contribute new, positive phone, cable and utility payment histories. Through Experian Boost, we’re empowering consumers to play an active role in building their credit histories. And, with Experian Lift, we’re empowering lenders to identify consumers who may otherwise be excluded from the traditional credit ecosystem. That’s game-changing. Disruptions like Experian Boost and newly announced Experian Lift are going to define the coming decade in credit and lending. Our industry needs to be ready because while it may seem early, it’s getting late.

Last month, Kenneth Blanco, Director of the Financial Crimes Enforcement Network, warned that cybercriminals are stealing data from fintech platforms to create synthetic identities and commit fraud. These actions, in turn, are alleged to be responsible for exploiting fintech platforms’ integration with other financial institutions, putting banks and consumers at risk. According to Blanco, “by using stolen data to create fraudulent accounts on fintech platforms, cybercriminals can exploit the platforms’ integration with various financial services to initiate seemingly legitimate financial activity while creating a degree of separation from traditional fraud detection efforts.” Fintech executives were quick to respond, and while agreeing that synthetic IDs are a problem, they pushed back on the notion that cybercriminals specifically target fintech platforms. Innovation and technology have indeed opened new doors of possibility for financial institutions, however, the question remains as to whether it has also created an opportunity for criminals to implement more sophisticated fraud strategies. Currently, there appears to be little evidence pointing to an acute vulnerability of fintech firms, but one thing can be said for certain: synthetic ID fraud is the fastest-growing financial crime in the United States. Perhaps, in part, because it can be difficult to detect. Synthetic ID is a type of fraud carried out by criminals that have created fictitious identities. Truly savvy fraudsters can make these identities nearly indistinguishable from real ones. According to Kathleen Peters, Experian’s SVP, Head of Fraud and Identity, it typically takes fraudsters 12 to 18 months to create and nurture a synthetic identity before it’s ready to “bust out” – the act of building a credit history with the intent of maxing out all available credit and eventually disappearing. These types of fraud attacks are concerning to any company’s bottom line. Experian’s 2019 Global Fraud and Identity Report further details the financial impact of fraud, noting that 55% of businesses globally reported an increase in fraud-related losses over the past 12 months. Given the significant risk factor, organizations across the board need to make meaningful investments in fraud prevention strategies. In many circumstances, the pace of fraud is so fast that by the time organizations implement solutions, the shelf life may already be old. To stay ahead of fraudsters, companies must be proactive about future-proofing their fraud strategies and toolkits. And the advantage that many fintech companies have is their aptitude for being nimble and propensity for early adoption. Experian can help too. Our Synthetic Fraud Risk Level Indicator helps both fintechs and traditional financial institutions in identifying applicants likely to be associated with a synthetic identity based on a complex set of relationships and account conditions over time. This indicator is now available in our credit report, allowing organizations to reduce exposure to identity fraud through early detection. To learn more about Experian’s Synthetic Fraud Risk Level Indicator click here, or visit experian.com/fintech.

The future is, factually speaking, uncertain. We don't know if we'll find a cure for cancer, the economic outlook, if we'll be living in an algorithmic world or if our work cubical mate will soon be replaced by a robot. While futurists can dish out some exciting and downright scary visions for the future of technology and science, there are no future facts. However, the uncertainty presents opportunity. Technology in today's world From the moment you wake up, to the moment you go back to sleep, technology is everywhere. The highly digital life we live and the development of our technological world have become the new normal. According to The International Telecommunication Union (ITU), almost 50% of the world's population uses the internet, leading to over 3.5 billion daily searches on Google and more than 570 new websites being launched each minute. And even more mind-boggling? Over 90% of the world's data has been created in just the last couple of years. With data growing faster than ever before, the future of technology is even more interesting than what is happening now. We're just at the beginning of a revolution that will touch every business and every life on this planet. By 2020, at least a third of all data will pass through the cloud, and within five years, there will be over 50 billion smart connected devices in the world. Keeping pace with digital transformation At the rate at which data and our ability to analyze it are growing, businesses of all sizes will be forced to modify how they operate. Businesses that digitally transform, will be able to offer customers a seamless and frictionless experience, and as a result, claim a greater share of profit in their sectors. Take, for example, the financial services industry - specifically banking. Whereas most banking used to be done at a local branch, recent reports show that 40% of Americans have not stepped through the door of a bank or credit union within the last six months, largely due to the rise of online and mobile banking. According to Citi's 2018 Mobile Banking Study, mobile banking is one of the top three most-used apps by Americans. Similarly, the Federal Reserve reported that more than half of U.S. adults with bank accounts have used a mobile app to access their accounts in the last year, presenting forward-looking banks with an incredible opportunity to increase the number of relationship touchpoints they have with their customers by introducing a wider array of banking products via mobile. Be part of the movement Rather than viewing digital disruption as worrisome and challenging, embrace the uncertainty and potential that advances in new technologies, data analytics and artificial intelligence will bring. The pressure to innovate amid technological progress poses an opportunity for us all to rethink the work we do and the way we do it. Are you ready? Learn more about powering your digital transformation in our latest eBook. Download eBook Are you an innovation junkie? Join us at Vision 2020 for future-facing sessions like: - Cloud and beyond - transforming technologies - ML and AI - real-world expandability and compliance

It's been over 10 years since the start of the Great Recession. However, its widespread effects are still felt today. While the country has rebounded in many ways, its economic damage continues to influence consumers. Discover the Great Recession’s impact across generations: Americans of all ages have felt the effects of the Great Recession, making it imperative to begin recession proofing and better prepare for the next economic downturn. There are several steps your organization can take to become recession resistant and help your customers overcome personal financial difficulties. Are you ready should the next recession hit? Get started today

Once you have kids, your bank accounts will never be the same. From child care to college, American parents spend, on average, over $233,000 raising a child from birth through age 17. While moms and dads are facing the same pile of bills, they often don’t see eye to eye on financial matters. In lieu of Father’s Day, where spending falls $8 million behind Mother’s Day (sorry dads!), we’re breaking down the different spending habits of each parent: Who pays the bills? With 80% of mothers working full time, the days of traditional gender roles are behind us. As both parents share the task of caring for the children, they also both take on the burden of paying household bills. According to Pew Research, when asked to name their kids’ main financial provider, 45% of parents agreed they split the role equally. Many partners are finding it more logical to evenly contribute to shared joint expenses to avoid fighting over finances. However, others feel costs should be divvied up according to how much each partner makes. What do they splurge on? While most parents agree that they rarely spend money on themselves, splurge items between moms and dads differ. When they do indulge, moms often purchase clothes, meals out and beauty treatments. Dads, on the other hand, are more likely to binge on gadgets and entertainment. According to a recent survey on millennial dads, there’s a strong correlation between the domestic tasks they’re taking on and how they’re spending their money. For instance, most dads are involved in buying their children’s books, toys and electronics, as well as footing the bill for their leisure activities. Who are they more likely to spend on? No parent wants to admit favoritism. However, research from the Journal of Consumer Psychology found that you’re more likely to spend money on your daughter if you’re a woman and more likely to spend on your son if you’re a man. The suggested reasoning behind this is that women can more easily identify with their daughters and men with their sons. Overall, parents today are spending more on their children than previous generations as the cost of having children in the U.S. has exponentially grown. How are they spending? When it comes to money management both moms and dads claim to be the “saver” and label the other as the “spender.” However, according to Experian research, there are financial health gaps between men and women, specifically when it pertains to credit. For example, women have 11% less average debt than men, a higher average VantageScore® credit score and the same revolving debt utilization of 30%. Even with more credit cards, women have fewer overall debts and are managing to pay those debts on time. There’s no definite way to say whether moms are spending “better” than dads, or vice versa. Rather, each parent has their own strengths and weaknesses when it comes to allocating money and managing expenses.

2019 is here — with new technology, new regulations and new opportunities on the docket. What does that mean for the financial services space? Here are the five trends you should keep your eye on and how these affect your credit universe. 1. Credit access is at an all-time high With 121 million Americans categorized as credit-challenged (subprime scores and a thin or nonexistent credit file) and 45 million considered credit-invisible (no credit history), the credit access many consumers take for granted has appeared elusive to others. Until now. The recent launch of Experian BoostTM empowers consumers to improve their credit instantly using payment history from their utility and phone bills, giving them more control over their credit scores and making them more visible to lenders and financial institutions. This means more opportunities for more people. Coupled with alternative credit data, which includes alternative financial services data, rental payments, and full-file public records, lenders and financial institutions can see a whole new universe. In 2019, inclusion is key when it comes to universe expansion goals. Both alternative credit and consumer-permissioned data will continue to be an important part of the conversation. 2. Machine learning for the masses The financial services industry has long been notorious for being founded on arguably antiquated systems and steeped in compliance and regulations. But the industry’s recent speed of disruption, including drastic changes fueled by technology and innovation, may suggest a changing of the guard. Digital transformation is an industry hot topic, but defining what that is — and navigating legacy systems — can be challenging. Successfully integrating innovation is the convergence at the center of the Venn diagram of strategy, technology and operations. The key, according to Deloitte, is getting “a better handle on data to extract the greatest value from technology investments.” How do you get the most value? Risk managers need big data, machine learning and artificial intelligence strategies to deliver market insights and risk evaluation. Between the difficulty of leveraging data sets and significant investment in time and money, it’s impossible for many to justify. To combat this challenge, the availability and access to an analytical sandbox (which contains depersonalized consumer data and comparative industry intel) is crucial to better serve clients and act on opportunities in lenders’ credit universe and beyond. “Making information analysis easily accessible also creates distinct competitive advantages,” said Vijay Mehta, Chief Innovation Officer for Experian’s Consumer Information Services, in a recent article for BAI Banking Strategies. “Identifying shifts in markets, changes in regulations or unexpected demand allows for quick course corrections. Tightening the analytic life cycle permits organizations to reach new markets and quickly respond to competitor moves.” This year is about meaningful metrics for action, not just data visualization. 3. How to fit into the digital-first ecosystem With so many things available on demand, the need for instant gratification continues to skyrocket. It’s no secret that the financial services industry needs to compete for attention across consumers’ multiple screens and hours of screen time. What’s in the queue for 2019? Personalization, digitalization and monetization. Consumers’ top banking priorities include customized solutions, omnichannel experience improvement and enhancing the mobile channel (as in, can we “Amazonize” everything?). Financial services leaders’ priorities include some of the same things, such as enhancing the mobile channel and delivering options to customize consumer solutions (BAI Banking Strategies). From geolocation targeting to microinteractions in the user experience journey to leveraging new strategies and consumer data to send personalized credit offers, there’s no shortage of need for consumer hyper-relevance. 33 percent of consumers who abandon business relationships do so because personalization is lacking, according to Accenture data for The Financial Brand. This expectation spans all channels, emphasizing the need for a seamless experience across all devices. 4. Keeping fraudsters out Many IT professionals regard biometric authentication as the most secure authentication method currently available. We see this technology on our personal devices, and many companies have implemented it as well. Biometric hacking is among the predicted threats for 2019, according to Experian’s Data Breach Industry Forecast, released last month. “Sensors can be manipulated and spoofed or deteriorate with too much use. ... Expect hackers to take advantage of not only the flaws found in biometric authentication hardware and devices, but also the collection and storage of data,” according to the report. 5. Regulatory changes and continued trends Under the Trump Administration, the regulatory front has been relatively quiet. But according to the Wall Street Journal, as Democrats gain control of the House of Representatives, lawmakers may be setting their sights on the financial services industry — specifically on legislation in response to the credit data breach in 2017. The Democratic Party leadership has indicated that the House Financial Services Committee will be focused on protecting consumers and investors, preserving sector stability, and encouraging responsible innovation in financial technology, according to Deloitte. In other news, the focus on improving accuracy in data reporting, transparency for consumers in credit scoring and other automated decisions can be expected to continue. Consumer compliance, and specifically the fair and responsible treatment of consumers, will remain a top priority. For all your needs in 2019 and beyond, Experian has you covered. Learn more

Financial health means more than just having a great credit score or money in a savings account. Although those things are good indicators of financial well-being, personal finance experts believe that financial health means more: being able to manage daily finances, save for the future and weather a financial shock, such as a job loss. As we approach #FinHealthMatters Day on June 27—a day created to bring attention to the 46 percent of Americans who are struggling financially—let’s take a look at financial health trends of Americans. Young adults not actively saving for retirement: Roughly 31% of non-retired adults have no retirement savings or a pension, according to a survey by the Federal Reserve. Nearly half of 18- to 29-year-olds surveyed had no retirement savings or pension, and about 75% of non-retired people 45 and older had some savings. Still, about 14% of adults 60 or older who are not retired and employed had no retirement savings, according to the report. Managing daily finances a challenge for many: Living paycheck to paycheck is a reality for about 1 in 10 Americans (11%), who say they spend more on monthly expenses than their household income allows, according to a Harris Poll. Of those surveyed, about one-third (32%) say they just make ends meet. Most lack an emergency fund: About 50% of people are unprepared for a financial emergency. Nearly 1 in 5 (19%) Americans have no savings set aside to cover unexpected emergencies, while about 1 in 3 (31%) Americans don’t have $500 reserved for an unexpected emergency expense, according to a survey released by HomeServe USA, a home repair service. Renewed focus on personal savings: On a positive note, Americans are sharpening their focus on personal savings, with slight increases among those who say they are saving more than last year (26% in 2017 vs. 24% in 2016). And the portion of those contributing income toward non-retirement savings has returned to its 2013 level of 69%. The good news is it’s never too late for people to achieve financial health. To do so, they need guidance to develop financial routines that build long-term resilience and opportunity. Promoting financial health is good for the financial services industry, as financially healthy consumers drive new opportunities for increased engagement, loyalty, and long-term revenue streams. We invite you to join the conversation and contribute your support and ideas for a healthier future.

Pay your bills on time, have cash set aside for emergencies, and invest your money for the future. These are the rules financial pros say people should follow if they want to build wealth. Straightforward advice, but for many people these milestones can seem out of reach. A recent financial literacy study by Mintel shows that many Americans are struggling with money management and lack confidence in their financial knowledge, with just 19 percent of respondents giving themselves an “A” grade on financial knowledge. The survey and other reports released recently shed light on how well Americans are handling their money. Here are some of the prevailing trends: Young people are struggling. The Mintel study revealed less than 30 percent of Americans have an emergency savings account that equals 3-6 months of household income. Of that total number, 19 percent of iGeneration has saved for a rainy day, followed by Millennials (20 percent), Gen Xers (28 percent), Baby Boomers (37 percent) and World War II/Swing Generation (40 percent). Not surprisingly, people who make more money save a bigger percentage of their pay. People in the bottom 90 percent of the income scale save close to none of their pay each year, while those in the top 10 percent save close to 15 percent. Most are not planning for the future. The majority of people are not doing everything they can to prepare for retirement, including meeting with a financial adviser to devise a plan, researching Social Security or even talking to friends or family about planning. Even more, 21 percent of Americans are “not at all confident” they will be able to reach their financial goals. Parents plan more than non-parents. People with children have many demands on their money, and as a result think ahead and follow budgets, contribute to retirement accounts and hire a financial adviser to help them create plans and budgets. Consumers who don’t have children don’t have as many competing demands, but aren’t as sensible about following a financial plan. In Mintel’s study, just 10 percent of non-parents have a written financial plan and 26 percent contribute regularly to a retirement account. Most people have a budget. Nearly one in three Americans prepare a detailed written or computerized household budget each month that tracks their income and expenses, but a large majority do not. Those with at least some college education, conservatives, Republicans, independents, and those making $75,000 a year or more are slightly more likely to prepare a detailed household budget than are their counterparts, according to Gallup. The good news is, the majority of Americans are open to more financial education. April—which is Financial Literacy Month—is a great time to look at education efforts for your customers. Financial literacy won’t change overnight, nor in a year. Yet initiatives taken in schools, workplaces, and in communities add up. What are you doing for your customers to build financial literacy?