Fraud & Identity

To combat auto loan fraud and protect profitability, auto lenders can leverage fintech advancements, machine learning and advanced analytics.

Spoiler alert: Gen AI is everywhere, including the top of Experian’s list of fraud trends 2024. “The speed and complexity of fraud attacks due to new technology and sophisticated fraudsters is leaving both businesses and consumers at risk in 2024,” said Kathleen Peters, chief innovation officer at Experian Decision Analytics in North America. “At Experian, we’re constantly innovating to deliver data-driven solutions to help our customers fight fraud and to protect the consumers they serve.” To deter fraudulent activity in 2024, businesses and consumers must get tactical for their fraud fighting strategies. And for businesses, the need for more sophisticated fraud protection solutions leveraging data and technology is greater than ever before. Experian suggests consumers and businesses watch out for these big five rounding out our fraud trends 2024. Generative AI: Generative AI accelerates DIY fraud: Experian predicts fraudsters will use generative AI to accelerate “do-it-yourself” fraud ranging from deepfake content – think emails, voice and video – as well as code creation to set up scam websites. A previous blog post of ours highlighted four types of generative AI used for fraud, including fraud automation at scale, text content generation, image and video manipulation and human voice generation. The way around it? Fight AI fraud with AI as part of a multilayered fraud prevention solution. Fraud at bank branches: Bank branches are making a comeback. A growing number of consumers prefer visiting bank branches in person to open new accounts or get financial advice with the intent to conduct safer transactions. However, face-to-face verification is not flawless and is still susceptible to human error or oversight. According to an Experian report, 85% of consumers report physical biometrics as the most trusted and secure authentication method they’ve recently encountered, but the measure is only currently used by 32% of businesses to detect and protect against fraud. Retailers, beware: Not all returns are as they appear. Experian predicts an uptick in cases where customers claim to return their purchases, only for the business to receive an empty box in return. Businesses must be vigilant with their fraud strategy in order to mitigate risk of lost goods and revenue. Synthetic identity fraud will surge: Pandemic-born synthetic identities may have been dormant, but now have a few years of history, making it easier to elude detection leading to fraudsters using those dormant accounts to “bust out” over the next year. Cause-related and investment deception: Fraudsters are employing new methods that strike an emotional response from consumers with cause-related asks to gain access to consumers’ personal information. Experian predicts that these deceptive cause-related methods will surge in 2024 and beyond. How businesses and consumers feel about fraud in 2024 According to an Experian report, over half of consumers feel they’re more of a fraud target than a year ago and nearly 70% of businesses report that fraud losses have increased in recent years. Business are facing mounting challenges – from first-party fraud and credit washing to synthetic identity and the yet-to-be-known impacts generative AI may have on fraud schemes. Synthetic identity fraud has been mentioned in multiple Experian Fraud Forecasts and the threat is ever growing. As technology continues to enhance consumers’ connectedness, it also heightens the stakes for various fraud attacks. As highlighted by this list of fraud trends 2024, the ways that fraudsters are looking to deceive is increasing from all angles. “Now more than ever, businesses need to implement a multilayered approach to their identity verification and fraud prevention strategies that leverages the latest technology available,” said Peters. Consumers are increasingly at risk from sophisticated fraud schemes. Increases in direct deposit account and check fraud, as well as advanced technologies like deepfakes and AI-generated phishing emails, put consumers in a precarious position. The call to action for consumers is to remain vigilant of seemingly authentic interactions. Experian can help with your fraud strategy To learn more about Experian’s fraud prevention solutions, please visit https://www.experian.com/business/solutions/fraud-management. Download infographic Watch Future of Fraud webinar

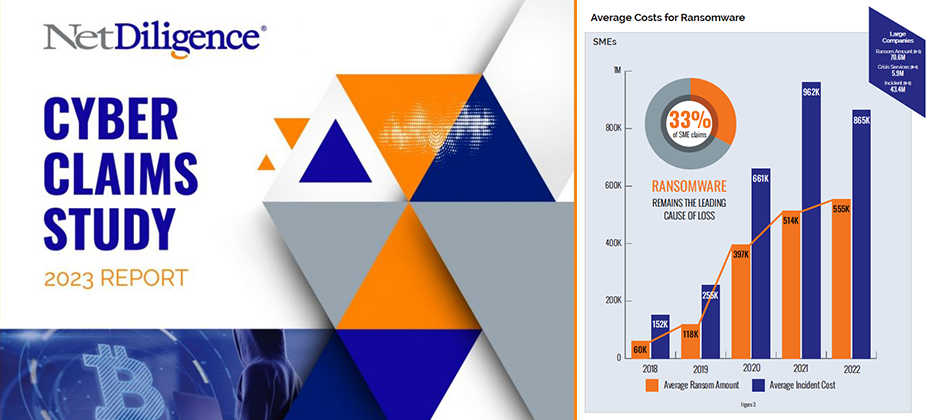

Review of Findings & Front-line Insights Panel Participants: Richard Goldberg (Moderator) – Constangy, Brooks, Smith & Prophete, LLP Michael Bruemmer – Experian Sean Renshw – RSM US, LLP Mark Greisiger – NetDiligence About NetDiligence Cyber Claims Study It is NetDiligence’s 13th year of doing this Cyber Claims Study. A total of 9,028 claims were analyzed during the past five years 2018-2022.An observation from the over 9,000 Cyber Claims (5000 of which are brand new claims this past year in 2023) analyzed is while many of the categories over the last five years have remained the same, the data has changed, sometimes dramatically. About Experian We provide call center coverage, notification coverage, as well as, identity theft protection, and all the consumer resolutions that go along with it for about 5000 data breaches every year, and I was delighted to be on the panel. Key Insights Experian has proudly sponsored the annual NetDiligence Cyber Claims Study for three years. During this time, I’ve witnessed companies adapt and transform their operations to confront the growing tide of cyber threats. The evolution of their infrastructure to anticipate and respond to these challenges has been remarkable and necessary. However, despite my front-row seat in this fast-changing landscape, the results of each study never fail to surprise and intrigue me. The insights from the latest study, conducted in 2023, continue to shape our understanding of the evolving cyber landscape. Ransomware’s Dominance Mark kicked off the discussion by shedding light on the escalating costs associated with cyber incidents. In 2022, the average incident cost for SME organizations remained stable at $169,000 (similar to the combined five-year window from 2018 to 2022 at about 175,000). However, there was a substantial increase for large companies, reaching $20.3 million in 2022 (and if you look at the five-year average, it was about 13 million). This surge raised eyebrows and set the stage for a deep dive into ransomware, a leading cause of concern. Examining Ransomware Trends The conversation swiftly shifted to ransomware, a pervasive threat in the cyber insurance landscape. As I stated, at Experian we see a correlation between the rise in ransomware and third-party breaches. Most of the industry experts on the panel participate in a Ransomware Advisory Group together. Mark brought up a good insight from our advisory group on the brazen tactics employed by threat actors lately, showcasing their intimate knowledge of the cyber insurance world. Business Sectors Under Siege Richard and Sean added to the discussion the top ten business sectors affected by ransomware, with professional services leading the pack. The impact on technology, with a payout of $830,000, stood out as well. Beyond Ransomware The conversation broadened to encompass other types of losses, such as social engineering and business email compromise. The focus on business interruption emerged as a key concern for cyber insurance claims, with the industry grappling with criminal acts versus non-criminal acts. Looking Ahead As the discussion unfolded, industry experts, including myself, expressed eagerness to anticipate the future cyber landscape. Predictions range from the industry mutating to the emergence of new players in the nation-state game. The role of artificial intelligence and innovative solutions from new vendors becomes a focal point of interest. In conclusion, the NetDiligence Cyber Claims Study 2023 Report paints a vivid picture of the challenges and transformations within the cyber insurance domain. The increasing sophistication of threat actors, coupled with evolving business strategies, sets the stage for continuous adaptation and innovation in the fight against cyber threats. As we look ahead, the resilience of businesses and the collaboration between industry stakeholders will play a pivotal role in shaping the cybersecurity landscape. I invite you to access the report and view the discussion replay for a deeper understanding of the challenges and transformations within the cyber insurance claims domain. Get NetDiligece Cyber Claims Study resources on-demand now! Download the report Watch the webinar NetDiligence’s latest Cyber Claims Study and Webinar, sponsored by Experian Data Breach, is available on-demand. This report serves as a resounding call to action, prompting businesses to ready themselves against cyber threats. Dive in to get insights and stay one step ahead of cyber adversaries.

With rapid growth comes an increased risk of fraud, making "Buy Now, Pay Never" a crucial fraud threat to watch out for in 2024.

Ryan Coyne recently participated in a panel with industry experts, delving into third-party cyber risks and mitigation strategies.

Enterprise identity management helps companies manage their customers' digital identities and information.

We've released our 11th annual Experian 2024 Data Breach Industry Forecast to embark on a journey into the future of data breaches.

Leveraging an identity resolution solution, organizations can accurately recognize consumers, build targeted marketing campaigns and more.

Effective online identity verification can help improve your customers' experiences while preventing fraud.

Approaches to payment fraud detection and prevention have evolved over time. Many organizations are now using AI and machine learning models.

The rise of remote work has significantly increased the prevalence of employment fraud. Learn how to safeguard your organization.

What is a data breach? It could impact your organization, and it is important for businesses to understand how to operate in it.

Meeting Know Your Customer (KYC) regulations and staying compliant is paramount to running your business with ensured confidence in who your customers are, the level of risk they pose, and maintained customer trust. What is KYC?KYC is the mandatory process to identify and verify the identity of clients of financial institutions, as required by the Financial Conduct Authority (FCA). KYC services go beyond simply standing up a customer identification program (CIP), though that is a key component. It involves fraud risk assessments in new and existing customer accounts. Financial institutions are required to incorporate risk-based procedures to monitor customer transactions and detect potential financial crimes or fraud risk. KYC policies help determine when suspicious activity reports (SAR) must be filed with the Department of Treasury’s FinCEN organization. According to the Federal Financial Institutions Examinations Council (FFIEC), a comprehensive KYC program should include:• Customer Identification Program (CIP): Identifies processes for verifying identities and establishing a reasonable belief that the identity is valid.• Customer due diligence: Verifying customer identities and assessing the associated risk of doing business.• Enhanced customer due diligence: Significant and comprehensive review of high-risk or high transactions and implementation of a suspicious activity-monitoring system to reduce risk to the institution. The following organizations have KYC oversight: Federal Financial Institutions Examinations Council (FFIEC), Federal Reserve Board, Federal Deposit Insurance Corporation (FDIC), national Credit Union Administration (NCUA), Office of the Comptroller of the Currency (OCC) and the Consumer Financial Protection Bureau (CFPB). How to get started on building your Know Your Customer checklist 1. Define your Customer Identification Program (CIP) The CIP outlines the process for gathering necessary information about your customers. To start building your KYC checklist, you need to define your CIP procedure. This may include the documentation you require from customers, the sources of information you may use for verification and the procedures for customer due diligence. Your CIP procedure should align with your organization’s risk appetite and be comply with regulations such as the Patriot Act or Anti-money laundering laws. 2. Identify the customer's information Identifying the information you need to gather on your customer is key in building an effective KYC checklist. Typically, this can include their first and last name, date of birth, address, phone number, email address, Social Security Number or any government-issued identification number. When gathering sensitive information, ensure that you have privacy and security controls such as encryption, and that customer data is not shared with unauthorized personnel. 3. Determine the verification method There are various methods to verify a customer's identity. Some common identity verification methods include document verification, facial recognition, voice recognition, knowledge-based authentication, biometrics or database checks. When selecting an identity verification method, consider the accuracy, speed, cost and reliability. Choose a provider that is highly secure and offers compliance with current regulations. 4. Review your checklist regularly Your KYC checklist is not a one and done process. Instead, it’s an ongoing process that requires periodic review, updates and testing. You need to periodically review your checklist to ensure your processes are up to date with the latest regulations and your business needs. Reviewing your checklist will help your business to identify gaps or outdated practices in your KYC process. Make changes as needed and keep management informed of any changes. 5. Final stage: quality control As a final step, you should perform a quality control assessment of the processes you’ve incorporated to ensure they’ve been carried out effectively. This includes checking if all necessary customer information has been collected, whether the right identity verification method was implemented, if your checklist matches your CIP and whether the results were recorded correctly. KYC is a vital process for your organization in today's digital age. Building an effective KYC checklist is essential to ensure compliance with regulations and mitigate risk factors associated with fraudulent activities. Building a solid checklist requires a clear understanding of your business needs, a comprehensive definition of your CIP, selection of the right verification method, and periodic reviews to ensure that the process is up to date. Remember, your customers' trust and privacy are at stake, so iensuring that your security processes and your KYC checklist are in place is essential. By following these guidelines, you can create a well-designed KYC checklist that reduces risk and satisfies your regulatory needs. Taking the next step Experian offers identity verification solutions as well as fully integrated, digital identity and fraud platforms. Experian’s CrossCore & Precise ID offering enables financial institutions to connect, access and orchestrate decisions that leverage multiple data sources and services. By combining risk-based authentication, identity proofing and fraud detection into a single, cloud-based platform with flexible orchestration and advanced analytics, Precise ID provides flexibility and solves for some of financial institutions’ biggest business challenges, including identity and fraud as it relates to digital onboarding and account take over; transaction monitoring and KYC/AML compliance and more, without adding undue friction. Learn more *This article includes content created by an AI language model and is intended to provide general information.

The online gaming industry has experienced tremendous growth. This surge in popularity has also sparked an increase in online gaming fraud.

To stay competitive and engage high-value customers, you’ll need to optimize your customer acquisition process.